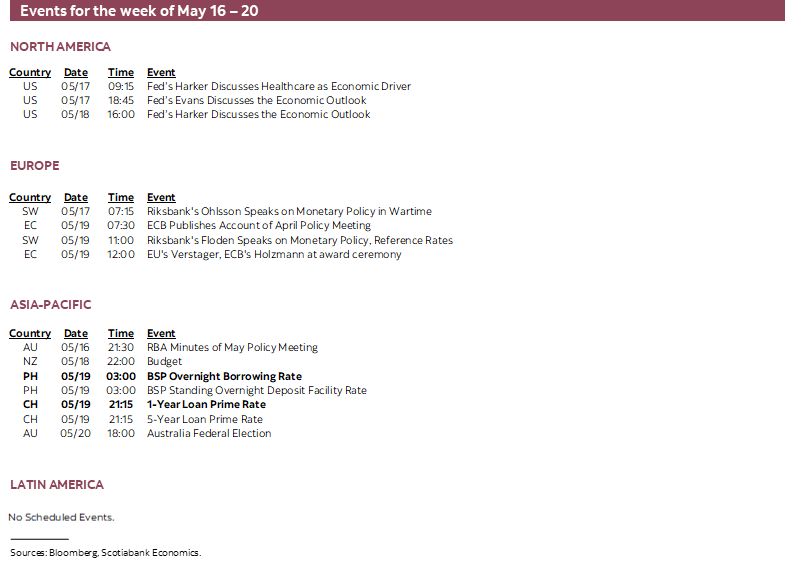

Next Week's Risk Dashboard

• What equity valuations may be saying

• Canadian inflation set to rise again

• UK inflation to hit a 9-handle?

• The PBoC’s competing forces

• NATO expansion plans

• US, UK consumers

• Jobs: UK, Australia

• GDP: EZ, UK, Chile, Colombia, Peru, Japan, Thailand

• Other CBs: SARB, Philippines

Chart of the Week

While there are some gems in the line-up, global calendar-based risk is going to be more subdued over the coming week than during some of the doozies we’ve been dealing with of late. China’s central bank will be the only major one to weigh in with a decision, we’re mostly on the downdraft of the global earnings season, and while there are some important macroeconomic readings on growth and inflation, none are likely to have the star power of, say, US jobs or US and Eurozone inflation.

That may place the emphasis upon off-calendar risk around further developments in China especially in terms of tracking Covid Zero policies, and the war in Ukraine and how Russia may react to expected traction toward seeking NATO membership by Finland and Sweden.

Still, from a market standpoint, stock market corrections will continue to drive debate over whether they merit changing the macroeconomic and policy rate outlook. Alternatively, should one view the movements as offering more attractive entry points? Is still greater caution warranted? Are both perspectives possible depending upon one’s horizon? This contest of narratives will persist and be subject to one’s favourite sloganeering whether it’s “sell in May and go away” but with probably still less overall willingness to go away, the latest screaming contests on financial news channels about deflation, depression and stagflation, or Warren Buffet’s sage advice to be “fearful when others are greedy, and greedy when others are fearful.”

Subject to one’s risk tolerance, horizon, liquidity and other personal attributes, I’m inclined to lean toward the latter expression by seeing more attractive entry points for longer-term investors, though unevenly so across markets. Tightened financial conditions are a necessary way in which tighter monetary policy works its way through the system but can also open up better opportunities for longer term investors compared to peak valuations.

Where you stand on the impact of softer year-to-date equities this year is nevertheless a direct function of where you sit and the worst vantage points have been in the US and China. For example, the S&P500 is about 16½% below its peak at the very start of the year which is approaching what many economists would flag as a material correction in the one-fifth ballpark. The Nasdaq composite is past that at -25%. By contract, local currency (USD) year-to-date changes have been considerably milder in most other markets such as Toronto’s -5½% (~–8%), London’s +0.5% (-9%), the CAC40 and DAX declines of -11% (over -18%), and the Nikkei 225’s -8% (-18%). Chinese stocks have suffered at least as badly as US stocks so far this year with local currency declines ranging between 15–24% (-29–38%). Given a significant home bias to investing within individual countries and depending upon currency movements, not every central bank has been dealing with the same magnitude of correction.

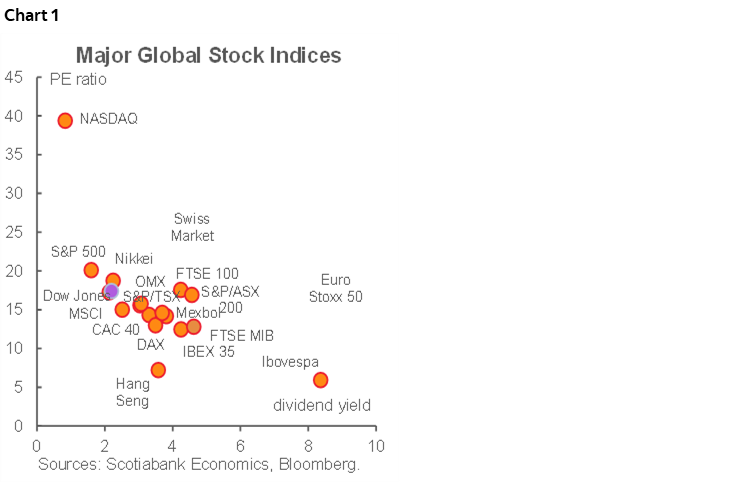

Looking at valuation measures can be more useful than raw price level indices. One perspective is offered in chart 1, and this is followed by a number of measures focused upon the US.

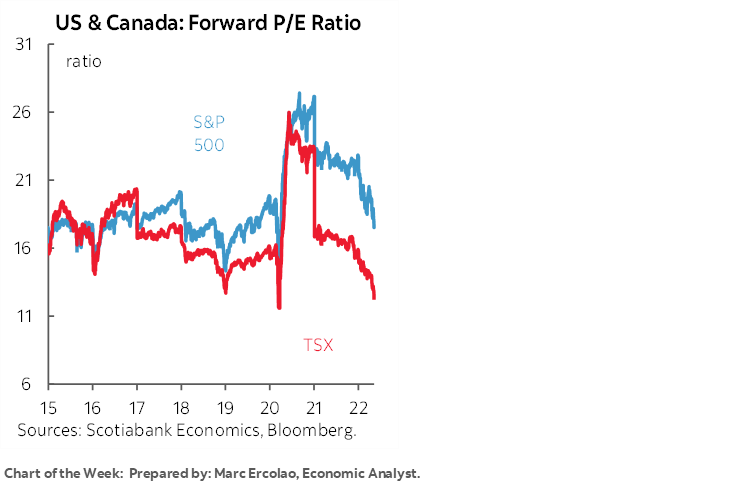

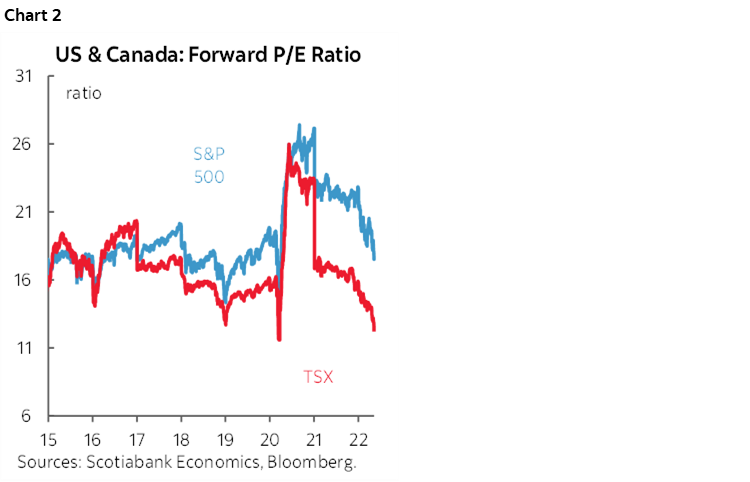

- The ratio of price-to-forward-earnings has returned toward pre-pandemic conditions which is one part a function of removing the pandemic’s distorting effects but another part a function of pointing to how the future expected earnings stream is as discounted or more discounted than it was in most pre-pandemic years (chart 2).

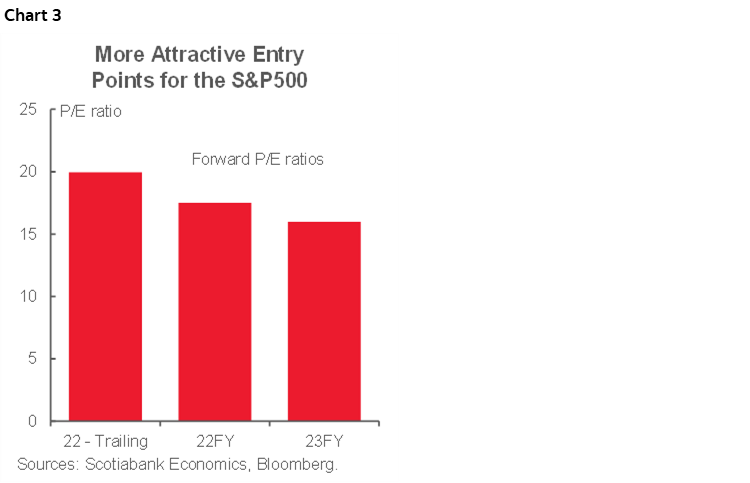

- Price-to-forward-earnings two years ahead strengthens this point and particularly on a relative Canada-US basis that would be strengthened if you—as we do—believe the C$ to be undervalued (chart 3).

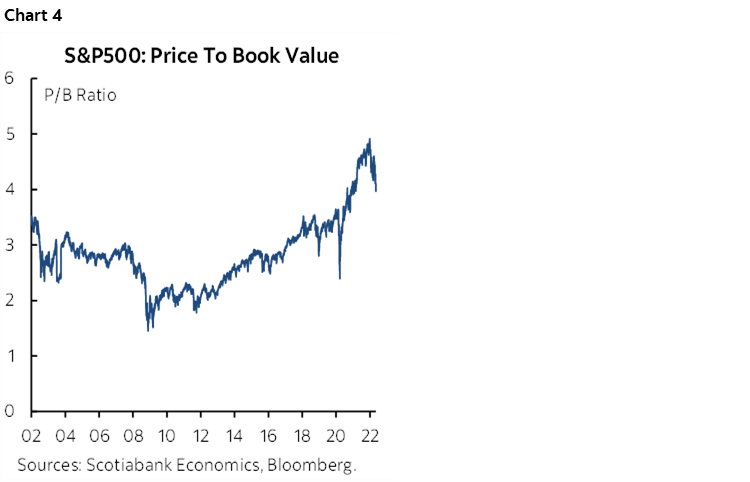

- The S&P500 price-to-book ratio is off its peak but remains elevated (chart 4). Inflation may be particularly impacting this reading if we’ve gone from slower increases in book values to more rapid increases.

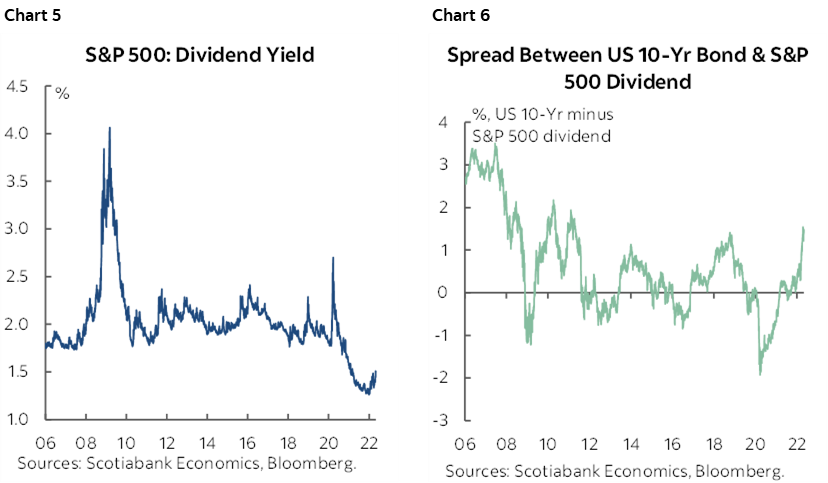

- The S&P500 dividend yield is off its bottom (chart 5) but the selloff in Treasuries has lifted the 10 year yield by more than the rise in the dividend yield (chart 6). In theory this either means that Treasuries are more attractive, that share prices may decline further or that dividend pay-outs may be raised should companies have less confidence in plowing earnings back into their operations.

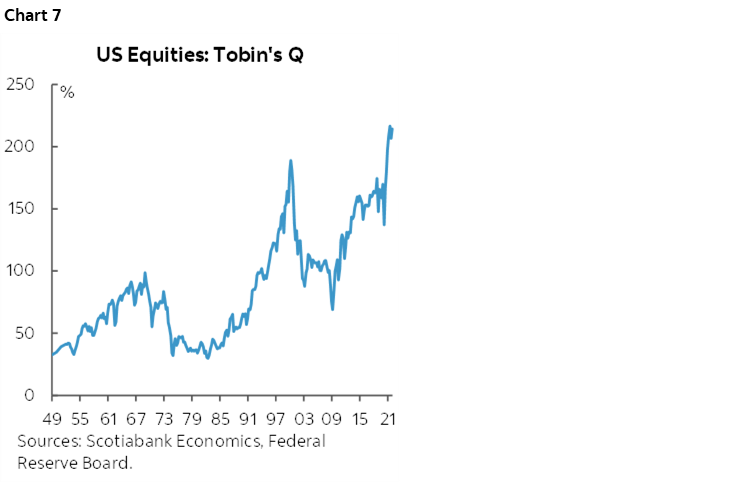

- Tobin’s ‘Q’—the ratio of the market value of a firm’s equities to the firm’s replacement cost—remains toward all-time record highs (chart 7). This is a bearish signal.

- The Cyclically Adjusted Price-to-Earnings ratio that smooths earnings over a long-term cycle continues to be toward the high points of the past couple of decades (chart 8).

The purpose of this set of comments is not to provide investment advice which must be tailored to individual circumstances and perspectives. The main purpose is to highlight the differential effects of market movements on different central banks, and how even amid nearer term market-timing issues around substantial risk to valuations this can still shed light upon longer-term opportunities for solid companies as the cyclical punchbowl gets taken away.

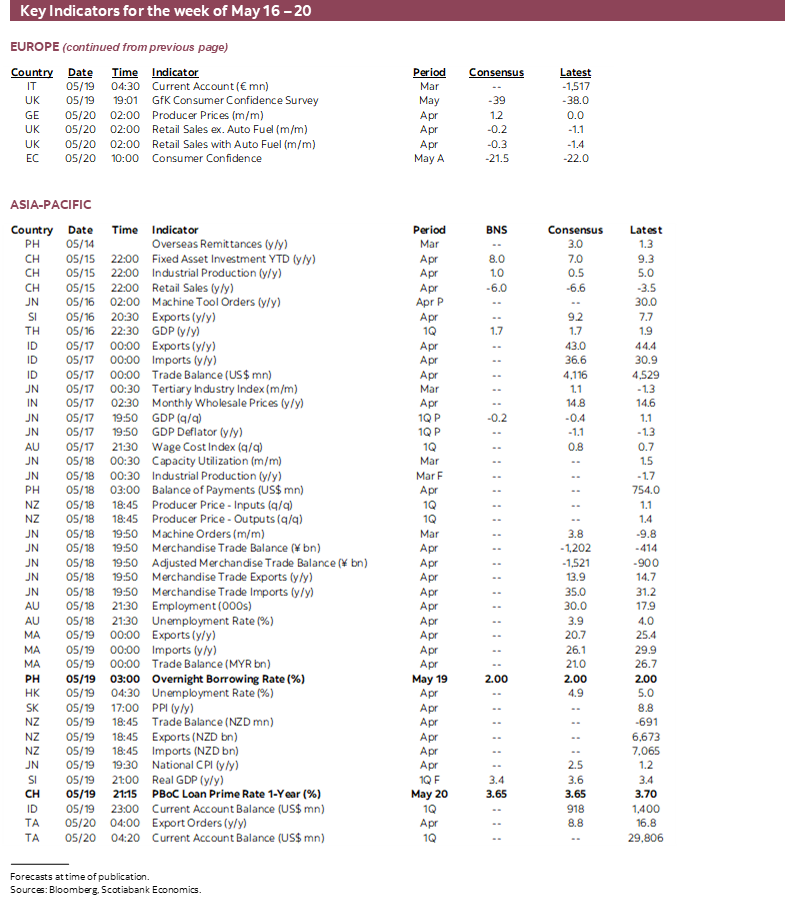

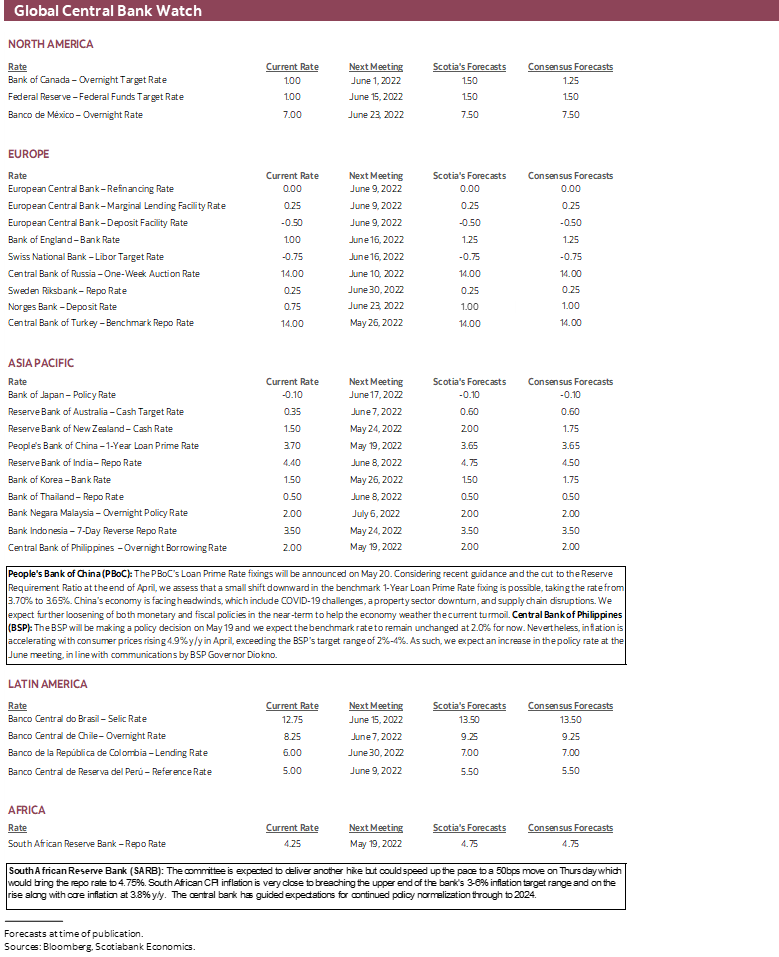

PBoC TO HIGHLIGHT AN OTHERWISE LIGHT CENTRAL BANK LINE-UP

Here we go again! Will the People’s Bank of China cut? In a week largely devoid of other developments across major central banks this decision will dominate.

A cut was expected by three-quarters of consensus the last time around on April 14th after Premier Li expressed the view that policymakers needed to step up with greater support for the economy, yet the central bank left rates unchanged and offered only a token quarter-point reduction in the required reserve ratio. I’m at a great distance from it all and China’s opacity makes judging this with much confidence very difficult to do, but from an outsider’s standpoint it certainly seems as though the policy signals have been conflicting for some time now. It also seems that local economists are in the same quandary. This time around, consensus is roughly split with about half of economists expecting no change to the 1-year Medium-Term Lending Facility Rate on Sunday evening (eastern time) and the other half expecting a cut of 5–15bps. Flipping a coin seems to be the tactic being adopted! The decision taken will then inform whether banks will follow in reducing the 1-year and 5-year Loan Prime Rates on Thursday evening (eastern time).

What may inform the PBOC’s decisions will be at least four considerations.

- Chinese inflation recently climbed to 2.1% y/y (1.5% prior) in April but remains lower than the almost-never-met 3% target, yet core CPI inflation fell to 0.9% y/y. Higher energy and food costs are either not being accompanied by greater underlying inflationary pressure, offset by other forces, or crowding out household budgets and sparking disinflationary pressures across other items. All three are simultaneously possible.

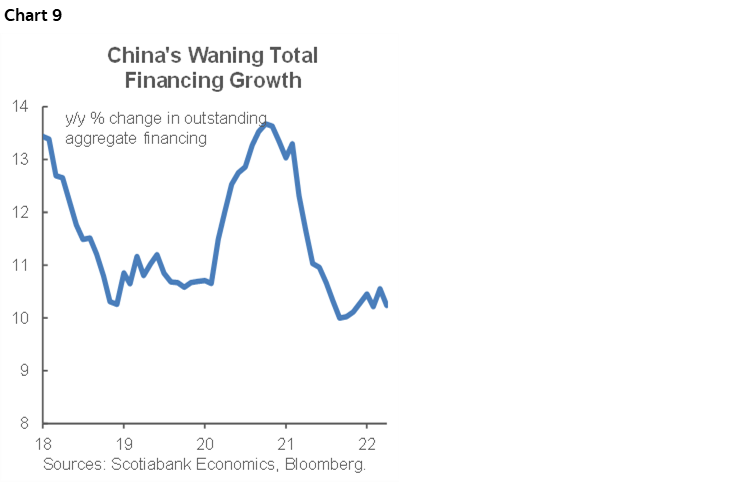

- Financing activity recently disappointed expectations for April in terms of aggregate financing products and core domestic currency loans (chart 9).

- A batch of economic indicators will land on Sunday evening into Beijing’s Monday morning markets. Retail sales, industrial production and the jobless rate are all likely to reflect weakness stemming from Covid Zero lockdown policies. Still, the PBoC’s monetary policy horizon may be skewed toward an eventual reduction or elimination of the policy including in Shanghai later this month and how that may spark a rebound through mid-year. If that happens, then this could also be constructive to global market risk appetite.

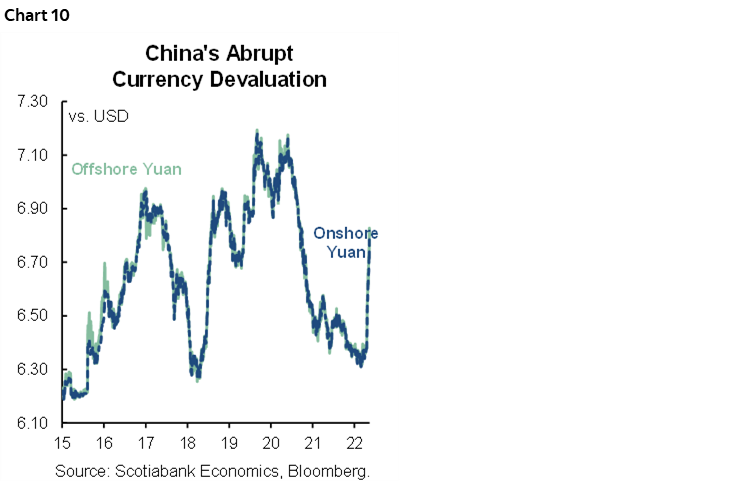

- Finally, China is trying to manage the currency’s depreciation with limited success. A higher recent fixing was one example of leaning against forces—principally Fed-PBoC policy divergence—pushing the yuan closer toward 7 to the USD (chart 10). The PBoC is going to be mindful toward the risks posed by yuan depreciation to financial stability within a fixed exchange rate system that has little capital account convertibility.

Only two regional central banks will be making policy decisions this week. Bangko Sentral ng Pilipinas is expected to hold on Thursday with a minority thinking that accelerating inflation to 4.9% y/y in April might be enough to prompt a surprise rate hike in the wake of Bank Negara Malaysia’s surprise hike this past week. The South African Reserve Bank is expected to hike by 50bps on Thursday with inflation close to breaching the upper limit of the 3–6% inflation target range.

CANADIAN INFLATION—FEELING USED

Canada updates CPI inflation for April on Wednesday. It’s likely to be another hot one and with an added twist this time.

I’ve guesstimated inflation at 0.7% m/m in seasonally unadjusted terms (as per the domestic sampling convention) all or most of which should be a seasonally adjusted gain, and 6.9% y/y (prior 6.7%). Base effects would cool the year-over-year rate down toward 6.1% y/y if that were the only consideration. Typical seasonal effects are likely to add somewhat to month-over-month prices. Gasoline prices should add nothing but may drag on seasonally adjusted prices. Modest further weighted contributions are likely from food, shelter and new vehicle prices.

The twist is that with this release, Statistics Canada has also pledged to issue a technical paper outlining methodological plans and timing toward including used vehicle prices in CPI. To be clear, the agency has recently said that used vehicle prices will not be included in the April CPI estimates and therefore this issue will lurk in the background to initial market reactions. Hopefully we’ll find out when they will eventually incorporate used vehicles in the basket like the longstanding practices in markets like the US and UK; perhaps the annual CPI re-weighting in June CPI available in July would be an opportune moment to do so all at once.

The most likely scenario is that Statcan says bygones be bygones, they will start tracking used vehicle prices going forward without making an attempt to include them in historical revisions. That would be the approach that was taken when the agency incorporated cannabis and audio/video streaming services, although the major difference here is that used vehicles have been around, well, forever, and are a significant part of the overall consumer budget. As a consequence, we may never get an accurate reading on inflation but Statcan will conveniently catch the eventual deceleration in used vehicles prices within CPI. I’d love to be proven wrong on that!

Among the areas of uncertainty are what weight will be assigned to used vehicles in CPI, what external benchmark may be used for used vehicle prices, and what adjustments may be made to this benchmark over time to control for matters such as changes in quality and features. There are no easy answers to all of these and a lot of judgement is likely to be applied.

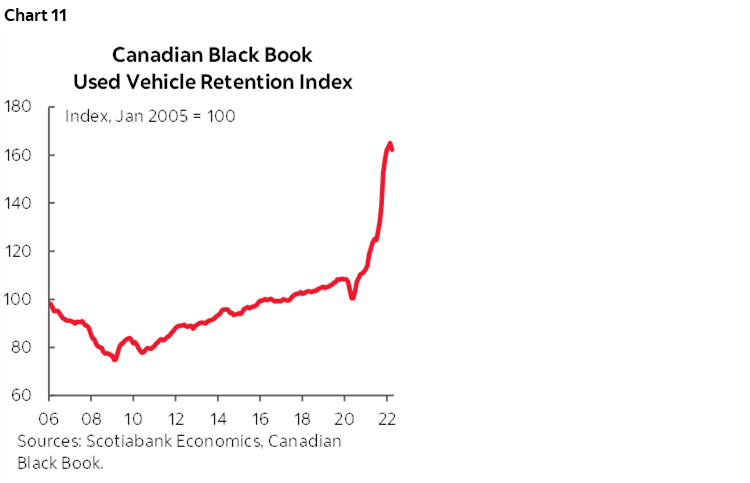

On price benchmarks, among others, there is the one shown in chart 11, or Adesa’s measure here that is akin to the Manheim auction measure in the US that the BLS rejects for US CPI, and Statcan is likely collecting its own sources. By comparison, the BLS uses used vehicle prices from J.D. Power Company but they then draw on prices of a sample of 480 vehicles aged two through seven years. We don’t know if Statcan will similarly use a subsample of relatively younger used vehicles. Furthermore, the BLS estimates depreciated price changes on a rolling one-month basis that used to be a three-month moving average until 2018 and the depreciation rates that may be applied by Statcan are uncertain. For more about the BLS methodology that may be instructive by way of highlighting the uncertainties around how StatCan will do this please go here.

On weights, according to the quarterly breakdown of household consumption expenditures (here), used vehicles only account for about 1.3% of total household spending and about one-quarter of spending on new and used vehicles combined. That would imply a soft weight on used vehicles and a very light share of the current CPI basket weighting on all vehicles (5.7%, here). In the US, by contrast, used vehicles account for about 4.2% of the CPI basket and all vehicles account for over 8% and so if the Canadian weights remain in the same ballpark then it could confirm that Canadians have less of a love affair with their cars and trucks than Americans. Statcan shifted to this source for CPI weights last July based upon 2020 spending patterns and replaced prior usage of its Survey of Household Spending. A caution is that weights from this quarterly survey don’t necessary align with CPI weights and this link explains other supplementary sources that can be drawn upon to derive a fuller perspective on weights used in CPI.

In short, it’s probably safe to say that year-over-year Canadian inflation will continue to be significantly under-reported but that there is significant uncertainty around the decisions the agency may make to begin to capture used vehicle prices in CPI going forward just as peak price pressures from this source are likely to abate over time.

GLOBAL MACRO ROUND-UP EMPHASIZES A FEW KEY MARKETS

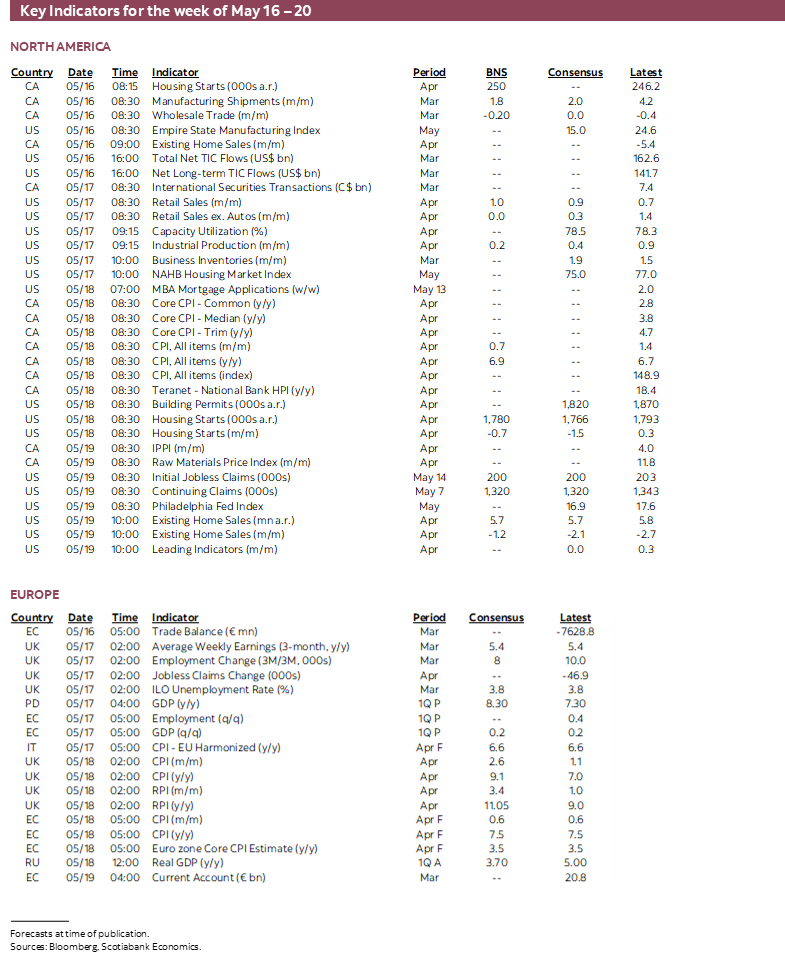

The global line-up of macro readings will be slanted toward the UK, China (see above), US, Australia and Canada.

The UK economy will be in the headlines when inflation (Wednesday) and retail sales (Friday) land for the month of April. Inflation is going tear higher and likely cross the 9% y/y mark from 7% the month before, but the Bank of England is very likely to see through much of the acceleration. The main culprit will be a massive 54% m/m energy price hike by the UK energy regulator, the Office of Gas and Electricity Markets (Ofgem). Ofgem raised its price cap on what energy companies can charge households because of surging wholesale market prices that surpassed the caps and drove losses and exits by several suppliers in the face of Europe’s ongoing energy crisis. The cap had already been raised by 12% last October and may be subject to another increase at the next review this coming October. The magnitude of the relative price shock to households’ energy bills may dampen discretionary household spending and crowd out some pricing power in other parts of the economy. That may be evident in UK retail sales for April that arrive on Friday.

A pair of employment reports land next week with the UK leading on Tuesday and Australia on Wednesday.

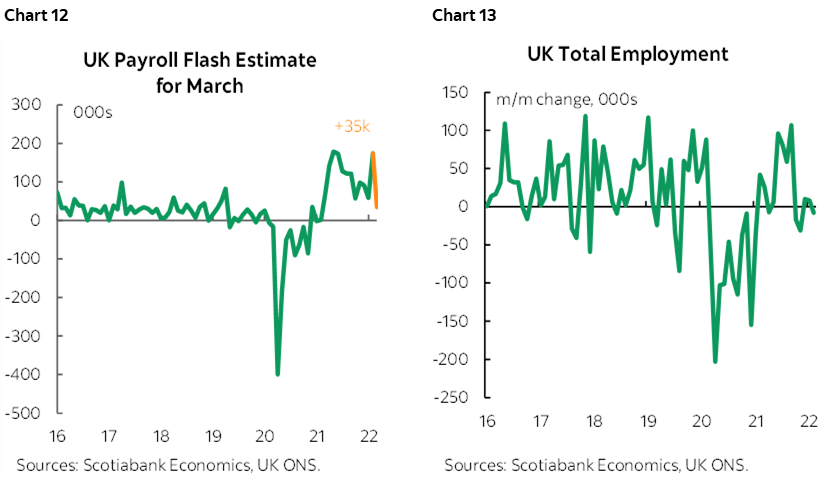

- UK Jobs (Tuesday): Flash payroll data released for March by the Office for National Statistics indicated a slowdown of job growth, albeit still positive, with a net gain of ~35k jobs (chart 12). The total employment picture has stalled a touch, effectively seeing no net new job growth over the last five months (chart 13). The current unemployment rate of 3.8% sits at around pre-pandemic levels, signalling strength in the UK labour market. Upcoming employment readings will be important as they may inform increasing recession risks that loom on the other side of the pond.

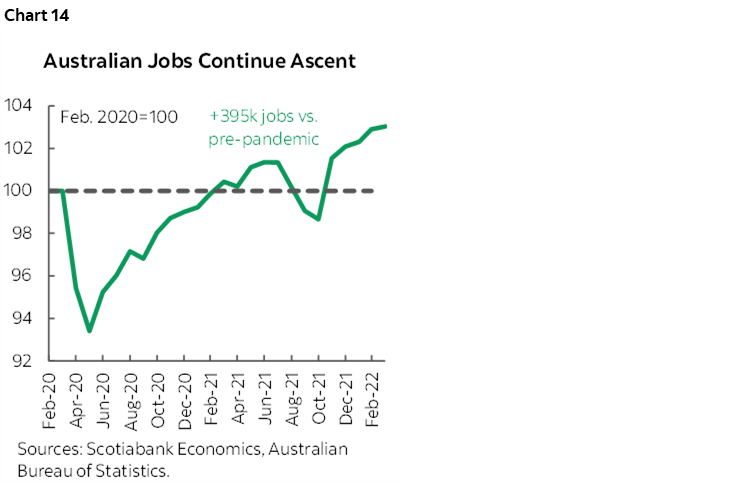

- Australia jobs (Wednesday): Australia’s labour market continues to show signs of strength as figures for March saw another net gain of +18k jobs, with over half-a-million jobs created over the last five months (chart 14). The gain in March would probably have been larger if not for floods along the east coast which dampened the overall jobs figure. April jobs should rebound while adding to the potential case of the RBA raising rates by as early as June.

US macro readings will inform growth tracking in Q2 and will do so by focusing upon industrial and household sector readings.

- Retail sales (Tuesday): April’s release should post a healthy gain that may heavily rely upon autos. Auto sales volumes were up by about 7% m/m SA according to Wards, and the BLS CPI figures pointed to a 1.1% rise in new vehicle prices. Since autos and parts carry about a one-fifth weighting in retail sales they should be enough to keep sales in the black. Downside risks include lower gasoline prices that could shave about 0.6% off retail sales in weighted terms albeit pending what happened to volumes.

- Industrial output (Tuesday): ISM-manufacturing’s production subindex has been softening but continues to point to modest gains in manufacturing output. Resource prices should assist the mining component of total industrial output that also includes utilities.

- Regional manufacturing surveys: Keep an eye on the Empire manufacturing (Monday) and Philly Fed (Thursday) manufacturing gauges for May for fresher readings on growth and inflation readings.

- Housing starts (Wednesday): Starts are expected to have softened a touch in April on a recently weakening trend in building permits.

- Existing home sales (Thursday): A weakening trend in pending home sales is expected to drive another decline in completed resales transaction when April’s numbers arrive. Pending home sales and mortgage purchase applications point to further housing weakness ahead.

Canada’s main event will be the CPI report for April (see above), but activity readings will inform GDP tracking for the end of Q1 and how it is transitioning to Q2. Advance guidance based on incomplete sampling by Statistics Canada has pointed toward a strong gain of just under 2% in the value of manufacturing sales and a mild dip in wholesale sector sales (both Monday). Housing starts probably held little changed around 250k in April (Monday). Existing home sales likely face further softness when April’s estimate arrives on Monday. The prior month’s 5.4% m/m SA drop at least partly reflected pulled-forward demand in February’s 4.6% m/m SA rise on rate hike expectations.

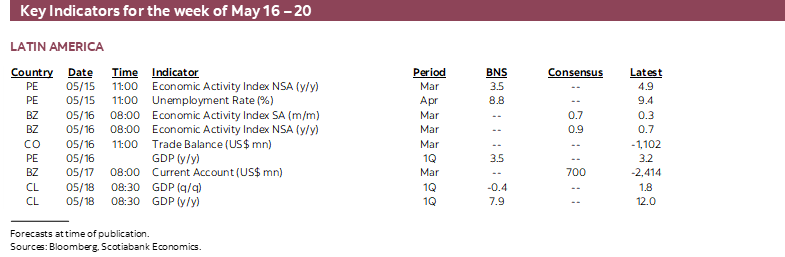

A batch of Q1 GDP readings will be released by Thailand (Monday), the Eurozone (Tuesday), Colombia (Monday), Chile (Wednesday) and Japan (Wednesday). Japan also updates CPI for April (Thursday) that is expected to more than double on a headline and core basis as higher oil prices and yen softness contribute to higher prices.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.