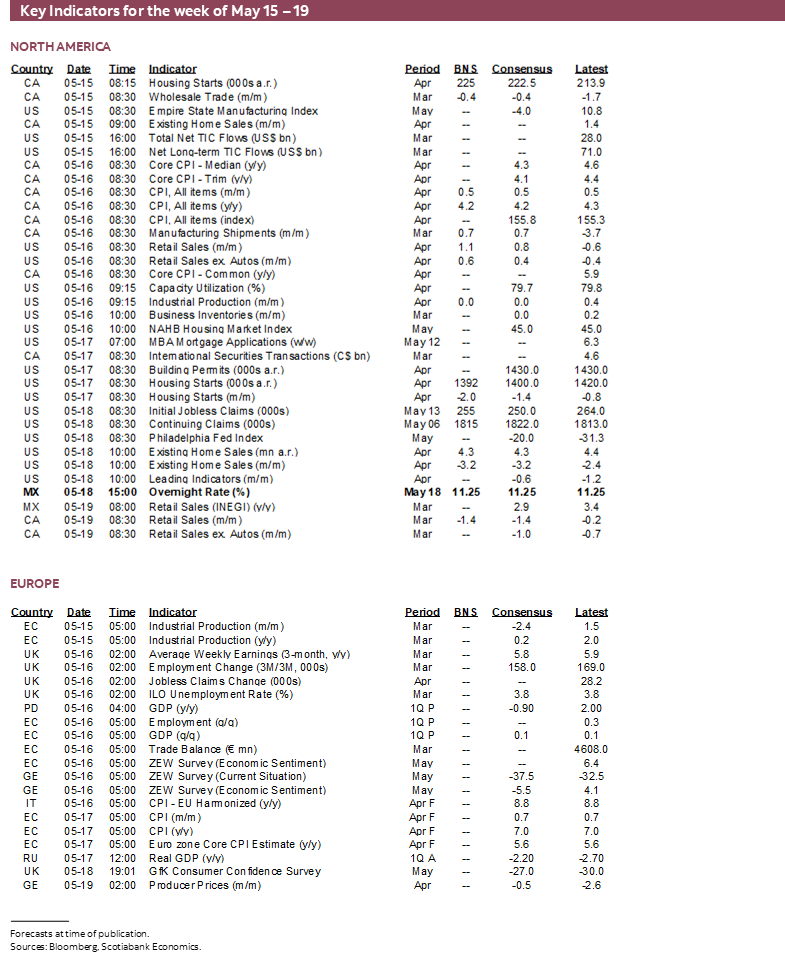

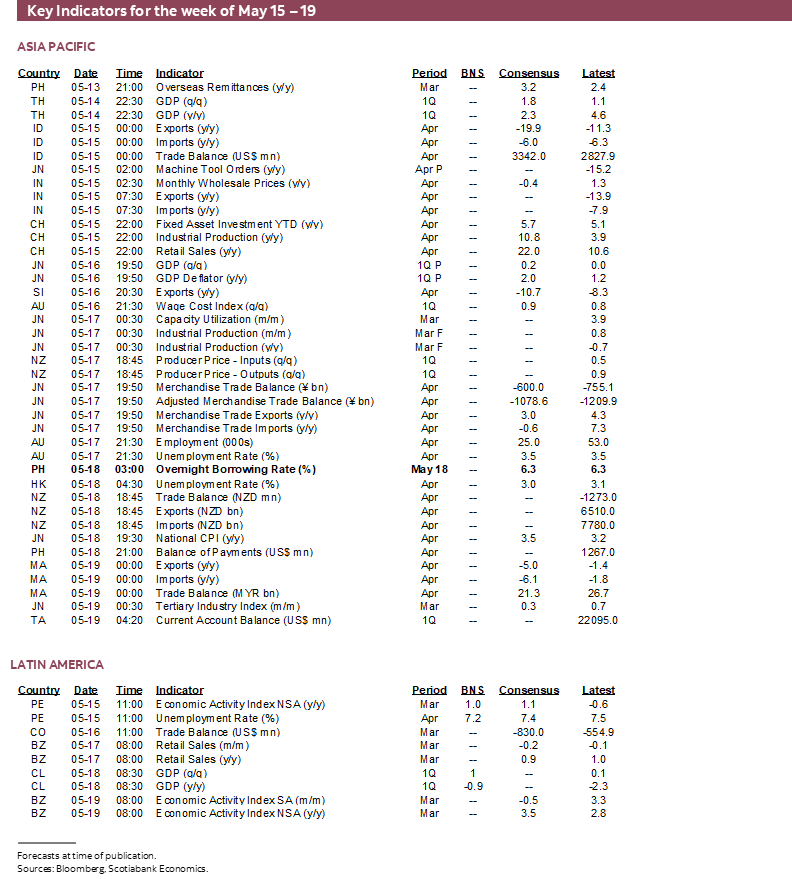

Next Week's Risk Dashboard

- Markets are getting more nervous about the debt ceiling

- The Fed’s neutral rate

- Canadian inflation is likely to remain sticky

- Banxico expected to pause

- PBoC on cut watch

- BSP may hold

- UK job markets driving wage pressures

- Australian wage growth expected to increase

- A prudent NZ budget?

- Japanese inflation to rise again

- US, CDN consumer updates

- BoC’s financial stability assessment

- Out with Erdogan?

- Other global macro

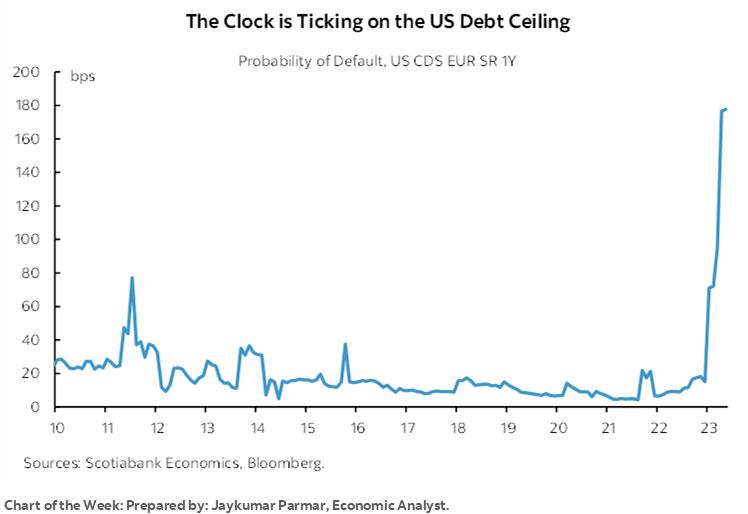

Chart of the Week

Against the backdrop of rising market concern around the status of the US debt ceiling fracas as indicated by this week’s cover chart plus ongoing risks in US banking lies uncertainty toward how restrictive US monetary policy really is. We might hear discussion on this point toward the end of the week while the week kick’s off with the tail risk of easier Chinese monetary policy. Other highlights this week will focus upon Banxico’s expected pause, Canadian inflation, and a wave of global macro reports plus Turkey’s election and the New Zealand budget.

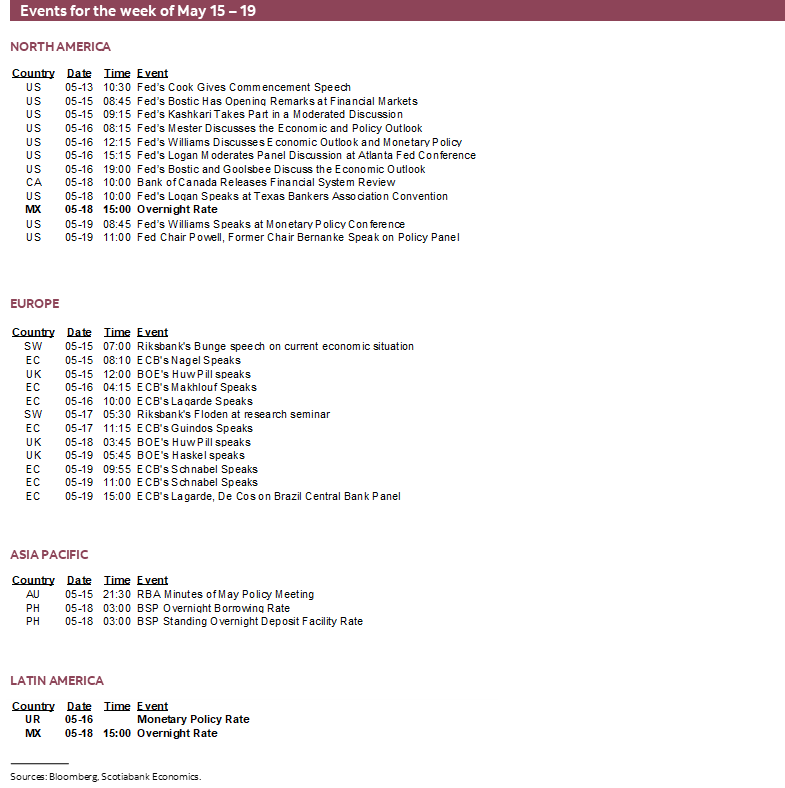

THE FED’S NATURAL RATE OF INTEREST

On Friday, Federal Reserve Chair Powell and past Chair Bernanke will participate in a joint 45-minute panel titled ‘Perspectives on Monetary Policy’ at the Thomas Laubach Research Conference held in honour of the late economist’s contributions (here). There is the mild risk that they broach the topic of whether or not to reassess estimates of the natural rate of interest. Even a nuanced reference to this could be impactful to markets. So could a rejection of any such sentiment. Bear in mind throughout it all the history of retrospective reassessments of natural rates after the fact and the high uncertainty around the inputs to such estimates such as potential GDP growth. My frank view is that estimates of the natural rate tend to be more about trial and error rather than having excess confidence in various frameworks that rely upon shaky inputs.

The natural rate of interest can be thought of as the real (inflation-adjusted) rate of interest that would exist in an economy at equilibrium with inflation on target and therefore offers a benchmark by which to evaluate how restrictive current monetary policy may be. In monetary policy circles, Laubach’s work was well known because it made valuable contributions to the literature on the natural rate of interest among other accolades. It might have been helpful having his perspective on whether this rate has changed today and, if anything, possibly moved higher than previously judged.

One argument for the possibility of reassessing the natural rate of interest is that we’re about 18 months into the lagging effects of when bond markets began to price tightened monetary policy, and yet jobs, core inflation and the broader economy remain resilient and sticky. One possible reason for this is that it could suggest that there are differences in this cycle that are serving to maintain momentum, such as stronger household finances than past cycles and improving supply chains in a tightening cycle. Or it could mean that the full lagging effects are still ahead, or some combination thereof.

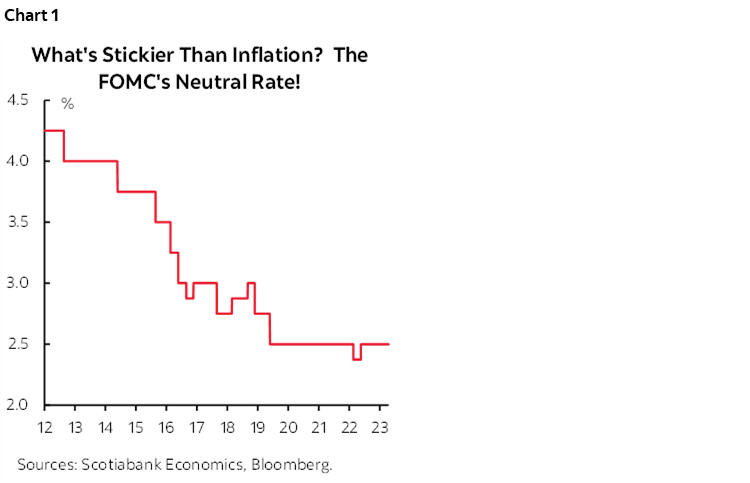

An entirely different possibility is that this recent resilience is revealing that the natural rate may have shifted higher now and perhaps higher than the FOMC’s stock answer of 2½% in nominal terms, or 50bps in real terms assuming a 2% equilibrium target rate of inflation. The FOMC chased estimates of the natural policy rate lower through the prior decade and despite the plethora of changes since then has left its estimate unchanged (chart 1). Chair Powell hasn’t really offered much of a convincing explanation for why.

If the natural rate is being underestimated, then perhaps monetary policy is not as tight as we think. That, in turn, should counsel caution toward related issues like is monetary policy as tight as we think and is it possible that the Fed funds target rate needs to move higher yet.

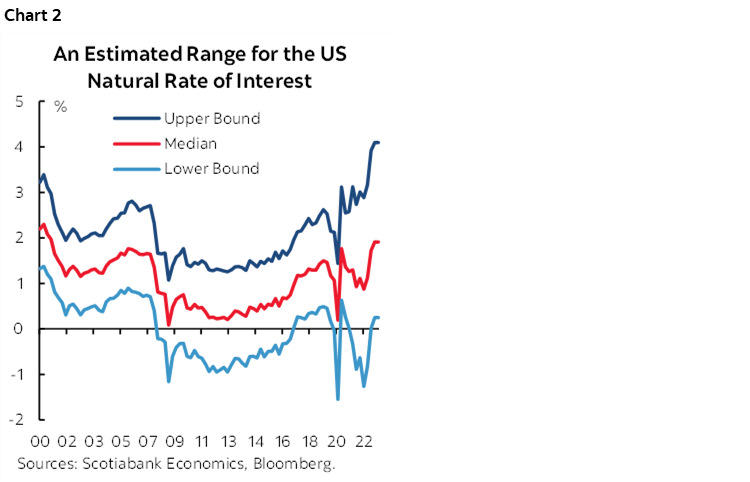

For instance, an alternate approach to estimating the range of real natural rates of interest is shown in chart 2 that shows how it has risen over time and at an accelerating rate of late, and within a very wide interval of possibilities. The Richmond Fed’s economists continue to publish their estimates of the natural rate as explained here. From a real R* of about ¼% just after the GFC, their median estimate of R* now sits at almost 2% which would suggest that today’s equilibrium nominal Fed funds policy rate should be around 4%. Their methodology employs a very wide range of possible natural rates of interest in real terms that run anything from just over 0% to about 4%, or 2–6% in nominal terms. With such estimates, it's possible that today’s real fed funds policy rate is not anywhere close to being as restrictive as often thought and may therefore have to push higher to restore price stability.

Another way of looking at it could be the Bank of Canada’s recent estimate US neutral rate that they said remained unchanged at 2–3% (here). Of course, when central banks try to estimate each others’ neutral rates it isn’t always necessarily the end of the debate. For instance, the Laubach-Williams model applied to Canada by the New York Fed’s economists had estimated the Canadian real R* rate at 1.4% which is well above the BoC’s own recent update of their neutral rate (here).

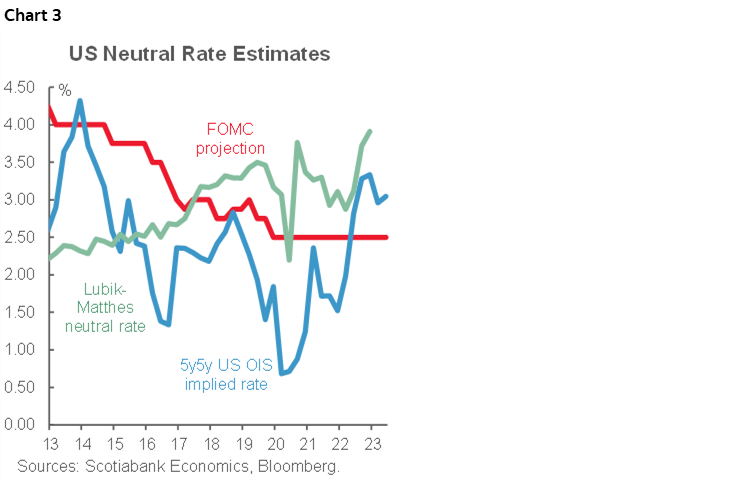

A market perspective is offered in chart 3 using a proxy for how markets may have adjusted their view toward the nominal R* to being above the FOMC’s estimate.

Only a minority of four members on the FOMC think the nominal natural rate is higher than 2½% with the highest estimate being the midpoint of a 3.5–3.75% range. That most definitely is not Chair Powell! There is also a time varying aspect to the estimates. Any light that he and Bernanke shine on the topic—given they are holding a conference in honour of someone who was famous partly because of his work on this topic—may be relevant to markets as a tail event to end the week.

Or they could just honour the man and his work and wish everyone a wonderful weekend. Either way, this issue remains key to assessing the possible future direction of Federal Reserve policy.

CENTRAL BANKS—TURNING POINTS?

Three central bank decisions are on tap over the coming week with one of them having the ability to impact global markets and the other being of greater significance to regional markets including within a key market for Scotiabank and its clients.

PBOC—A DELICATE BALANCE

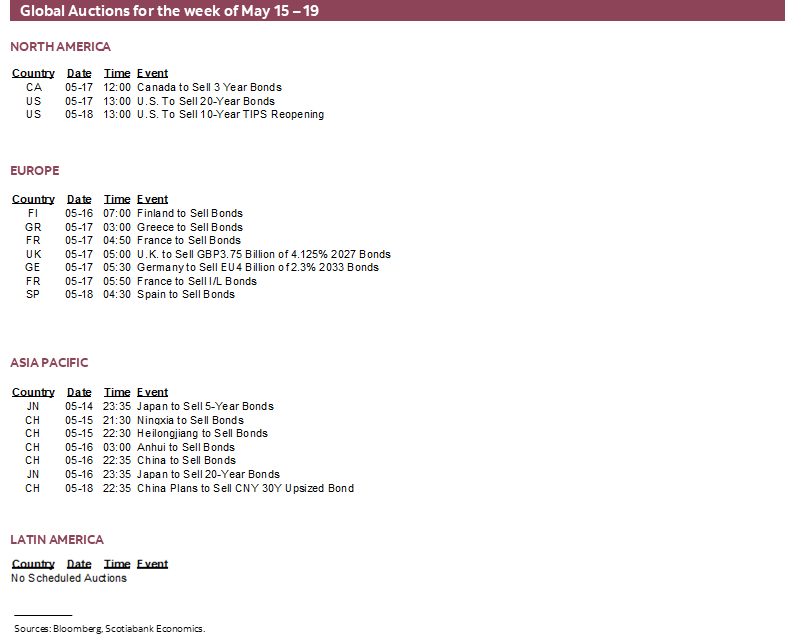

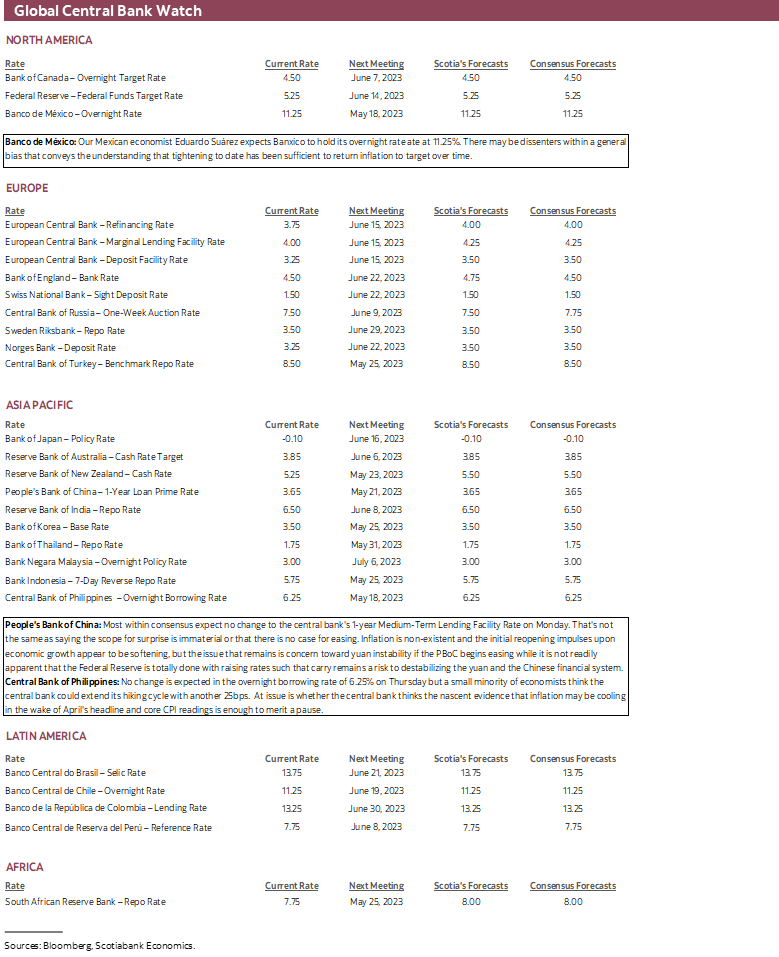

Most within consensus expect no change to the central bank's 1-year Medium-Term Lending Facility Rate at the start of the week (Sunday 9:20pmET). That's not the same as saying the scope for surprise is immaterial or that there is no case for easing. There may well be such potential to kick off the week in a possibly favourable manner in the context of the outlook for the global economy including China’s part of it and the outlook for several types of commodities.

For starters, Reuters reported on April 24th that Chinese authorities were reportedly pressuring banks to cut their deposit rates that were last cut back in September. The next 1- and 5-year LPR settings will be on May 21st after the PBoC sets its 1-year MTLFR this week. A PBoC cut this week would set the stage for banks to follow suit.

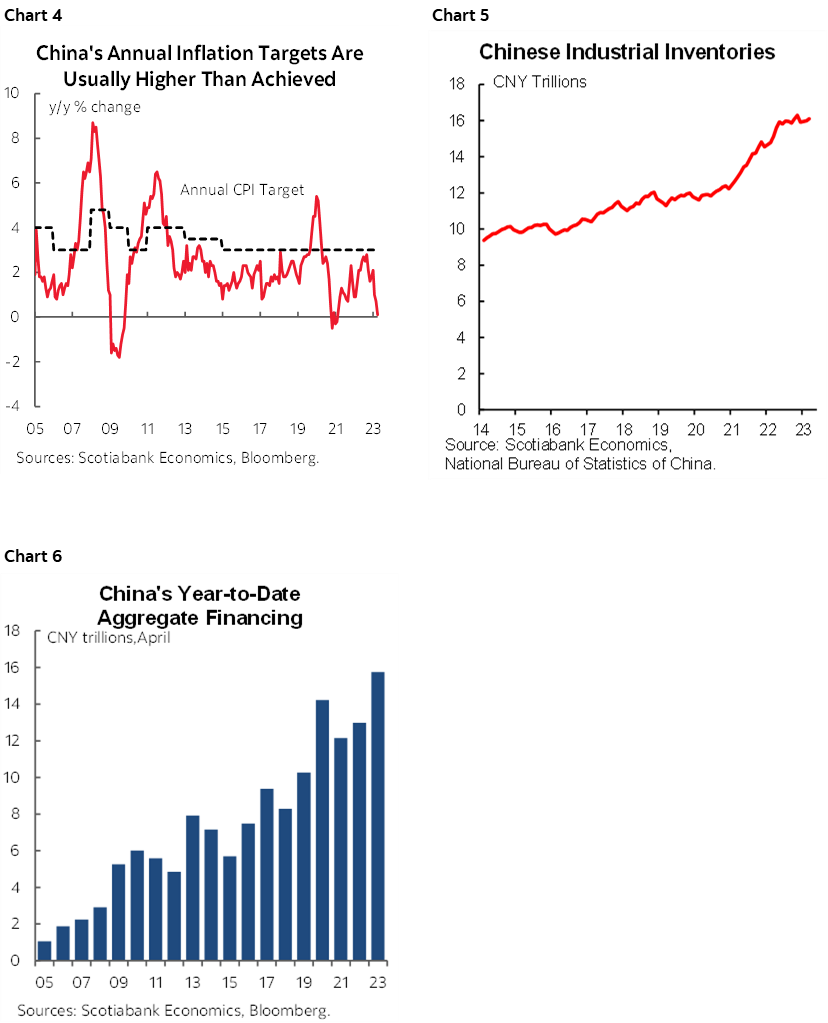

Furthermore, inflation is non-existent and miles beneath the central bank’s inflation target (chart 4) and the initial reopening impulses upon economic growth appear to be softening as evidenced by softening PMIs and a steep drop in imports. Headwinds to Chinese manufacturing including downside risk to key export markets and bloated industrial inventories (chart 5). Credit easing has been a very powerful effect this year with assistance from reductions to required reserve ratios, but the latest figures for April point to lost momentum in April while still keeping year-to-date growth at elevated levels (chart 6).

The concern that remains a powerful argument against easing, however, is the risk of stoking yuan instability. If the PBoC begins easing while it is not readily apparent that the Federal Reserve is totally done with raising rates, then carry could become a more negative risk to destabilizing the yuan and hence the Chinese financial system. A lot will depend upon how PBoC officials view the outlook for the US economy and financial system and the Fed’s part within it all alongside assessments of domestic prospects.

BANXICO—GAMBLING ON A PEAK

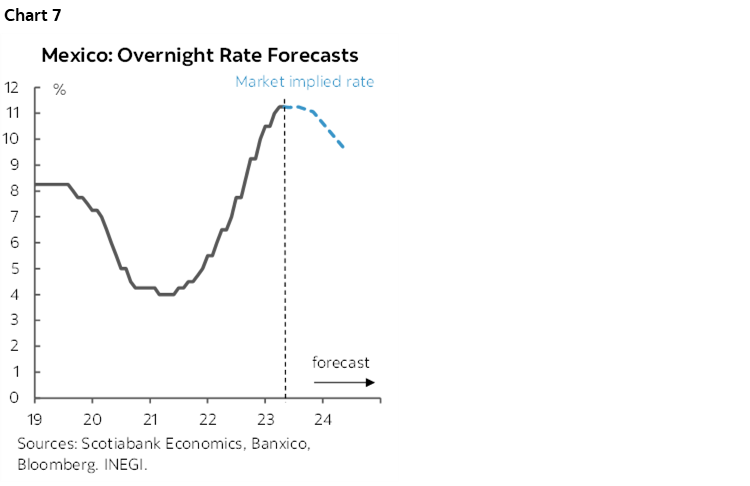

Banco de México (Banxico) is expected to hold its overnight rate at an unchanged 11.25% rate on Thursday (3pmET). There is a minority within consensus that thinks they may hike by another 25bps for which markets are not priced.

Our Mexico City economist, Eduardo Suárez, reasons that the next move is likely lower over the back half of 2023 (chart 7). Markets are pricing for a gentle move in this direction with greater easing priced in 2024.

What the hold camp has in its favour are the nascent signs that inflationary pressures have been ebbing and not just on headline CPI. Core CPI inflation peaked at 8.5% y/y in November and April’s reading was 7.7% with headline inflation falling back to 6¼%. Month-over-month seasonally unadjusted changes in Mexican core CPI were unusually hot last year but so far this year have been tentatively reverting back toward a more typical seasonal pattern especially in April’s reading. That just might be enough to merit a breather, conditional upon how the central bank views further progress toward cooler inflation and conditional upon what the Federal Reserve does going forward.

BSP—THE START OF SOMETHING GOOD?

Bankgo Sentral ng Pilipinas is expected to hold its overnight borrowing rate at 6.25% on Thursday but a small minority of economists think the central bank could extend its hiking cycle with another 25bps. At issue is whether the central bank thinks the very nascent evidence that inflation may be cooling in the wake of April's headline and core CPI readings is enough to merit a pause.

CANADIAN INFLATION—STILL STICKY?

The sausage grinder of Canadian inflation statistics will whir to life again on Tuesday. The impact upon markets will depend upon whether it’s sweet like relish or smothered in mustard. Any such impact could be temporary in the face of required evidence that inflation has to move durably lower over time to convince the BoC that it can ease up on the brakes or even avoid pressing them harder. That evidence might be harder to come by than may be desirable.

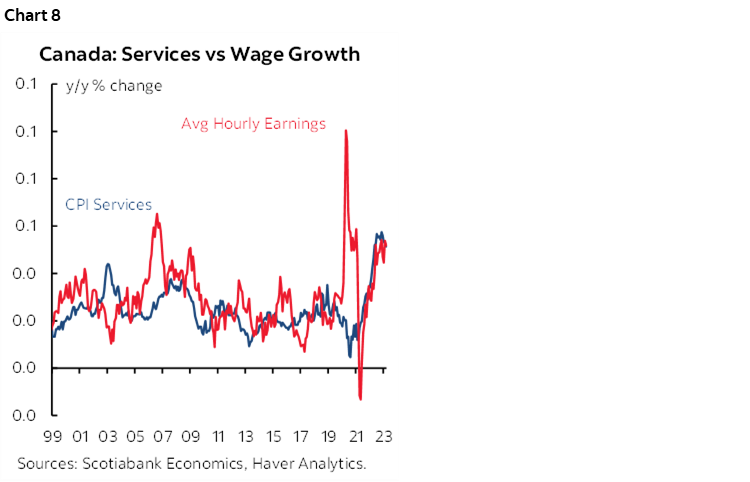

I’ve estimated an increased of 0.5% m/m NSA and in seasonally adjusted terms given that April’s seasonal adjustment factor isn’t much of an issue compared to other months. Gasoline prices should be a fairly neutral contributor to the month-over-month rates. I’ve assumed that services will remain a significant contributor (chart 8) alongside shelter costs with vehicles playing a minor role.

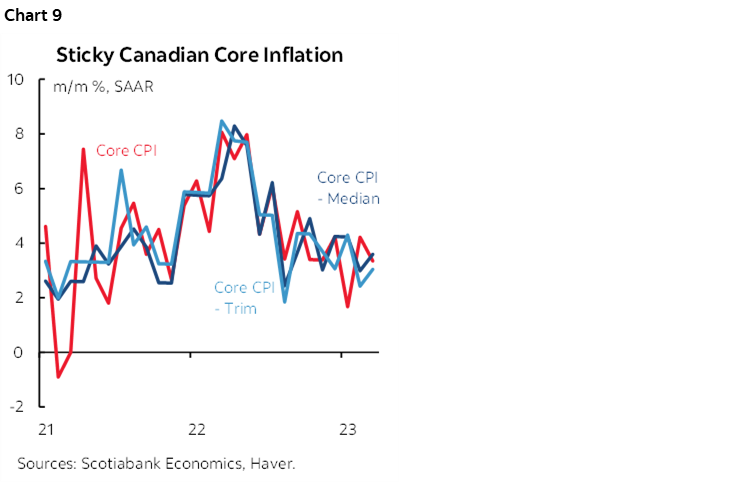

At issue is whether the measures of core inflation remain as sticky as they have been of late with all readings at or slightly above 3% m/m SAAR (chart 9). That matters the most to assessing price pressures and the implications for the Bank of Canada, but too often it’s missed on first passes. There has been progress toward lower month-over-month core inflation measured in seasonally adjusted terms at an annualized rate, but the main gauges are showcasing persistence at rates above the BoC’s 2% inflation target. These various measures weed out extraneous drivers to varying degrees. For instance, mortgage interest cost is just not a factor in driver trimmed mean and weighted median inflation despite its rapid increases in lagging fashion to policy rate adjustments and so it doesn’t impact the BoC’s thinking toward the drivers of inflation.

So what does it matter if inflation remains sticky or not? Governor Macklem has been placing extra communications efforts into convincing markets that he is serious toward getting inflation durably down to the 2% target as the midpoint of the 1–3% target range. He warns that the next leg lower could require additional policy tightening. The question is the degree to which he really means that, and this isn’t clear.

In my view, there is a stronger case for the next nearer-term move being higher than lower. Inflation risk is pivoting higher in Canada over the coming months and quarters. There is more pent-up services demand in Canada than the US. Housing is at an inflection point that is headed higher in the context of no inventories, a surge of immigration, idled first time homebuyers waiting to pounce with higher down payments, an increasing array of forecasts pointing toward rising expectations for capital gains, another housing stimulus program that was introduced on April 1st (!) and robust job markets. Fiscal policy remains supportive of growth and with that persistent inflationary pressure. Canada has not even begun to take steps toward creating excess capacity in the economy that would be disinflationary. And then there are all of the other layered on structural drivers of inflation over the longer run that I’m still of the view have moved higher compared to the prior decade.

GLOBAL MACRO—SOMETHING FOR EVERYONE

Across the rest of the line-up will be several main focal points that cut across global markets such as consumer updates in the US and Canada, UK and Australian jobs, evidence on momentum in China’s economy, New Zealand’s Budget, Turkey’s weekend election, plus Japanese inflation and GDP.

US retail sales are due on Tuesday and could show a large pop higher. April’s reading should benefit from about a 7% m/m SA rise in new vehicle sales that on its own would add about 1% to m/m retail sales, plus a 3% m/m SA gain in gasoline prices that should add about another quarter point. CPI components pointed toward gains in retail categories that are more oriented toward goods than services. Key will be core sales excluding vehicles and gasoline.

The US will also update readings on industrial production (Tuesday), the Empire (Monday) and Philly Fed (Thursday) manufacturing gauges that will start to inform ISM expectations, plus a pair of housing gauges including starts (Wednesday) and resales (Thursday). Initial jobless claims will be closely monitored to see if the latest week’s increase has legs to it.

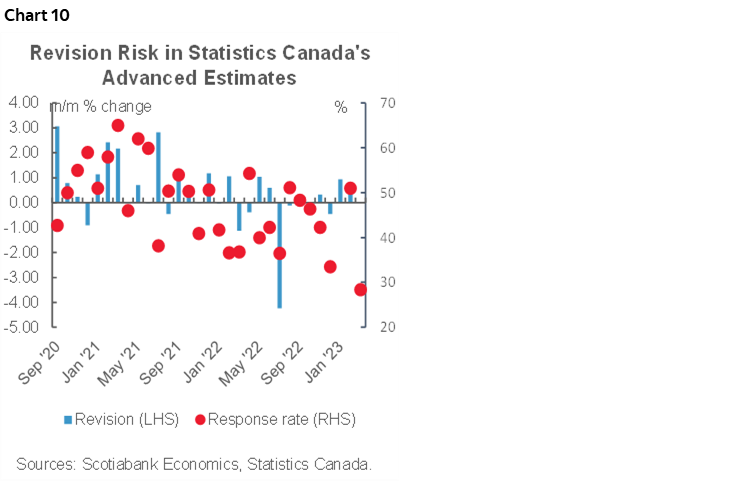

Canada will primarily focus upon CPI, but a few other readings will be on offer. On Friday, we’ll get a pair of retail sales reports that will further inform momentum in a part of the consumer sector. March’s retail sales were previously guided to have declined by 1.4% m/m, but a key problem was the very low 28% sampling rate behind that ‘flash’ measure from Statistics Canada that was the lowest since Statcan started to offer the preliminary readings in 2020. As chart 10 demonstrates, this might indicate high risk of revision in one direction or another. Then the focus will turn to the agency’s preliminary reading on April’s retail sales but with a hopefully improved sampling rate.

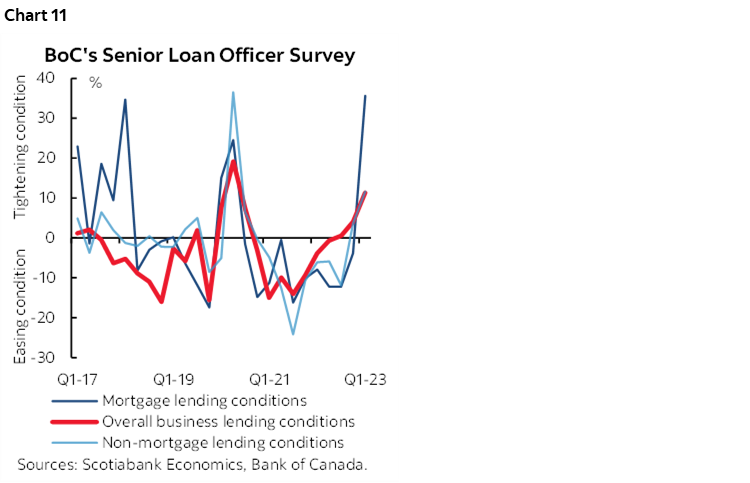

Canada will also update housing starts during April (Monday), an expected dip in wholesale trade (Monday) and an expected rise in manufacturing sales. The Bank of Canada will also release its Financial System Review on Thursday after its sales loan officer opinion survey showed significant incremental tightening of lending conditions for mortgages but little change in other household lending products or business lending (chart 11). It’s vital to interpret these gauges as indicating the net percentage of lenders who say they are tightening at the margin rather than interpreting them to mean cumulative tightening.

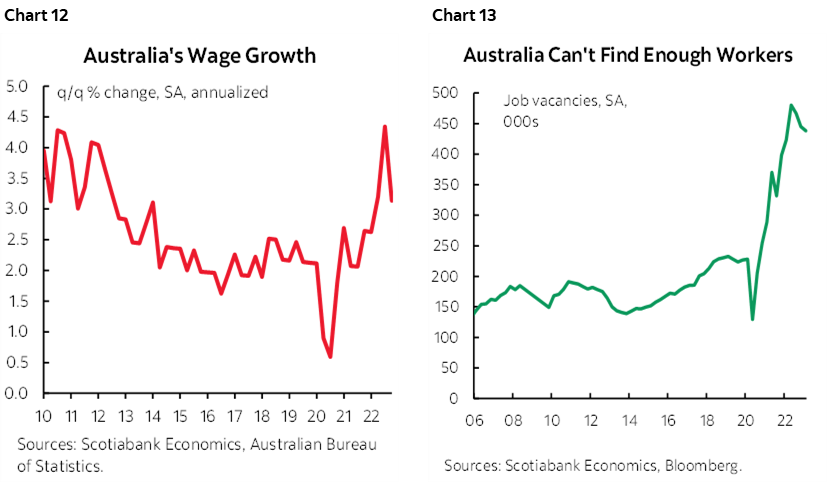

Asia-Pacific markets could be impacted the most by whatever the PBoC does, with a few other gauges of relevance to consider. Momentum in China’s economy will be informed by April’s readings on industrial output, retail sales, the jobless rate and new home prices. Australian jobs (Wednesday) are expected to continue rising and indicate a strong employment market and before that will be the Q1 wages report (Tuesday) that is expected to accelerate from the prior softer reading (chart 12). Australian job vacancies remain very high (chart 13).

Bank of Japan watchers will have one eye on Q1 GDP (Tuesday) and another on April’s CPI report (Thursday). GDP is expected to squeeze out slight growth while inflation continues to edge higher in headline and core terms.

New Zealand’s turn to deliver a budget will be on Wednesday (10pmET). As I wrote in an earlier note, the recent Australian budget was longer on rhetorical prudence than the numbers indicated and so we’ll see if NZ Finance Minister Robertson’s recent guidance against measures that would complicate the inflation fight turns into reality.

Turkey’s weekend election will captivate Europeans with potentially significant geopolitical implications. Recep Erdogan’s longstanding rule is at risk of losing the first round of elections on Sunday. Erdogan’s economic policies have been ruinous to the country as he has overtly meddled in the central bank’s affairs, ordered rate cuts that drove a collapse in the lira and soaring inflation that presently sits at about 44% y/y. He has let’s just say unorthodox views that easier money drives lower inflation which isn’t working out so well. The ruling elite, mind you, isn’t paying the price being borne by the masses.

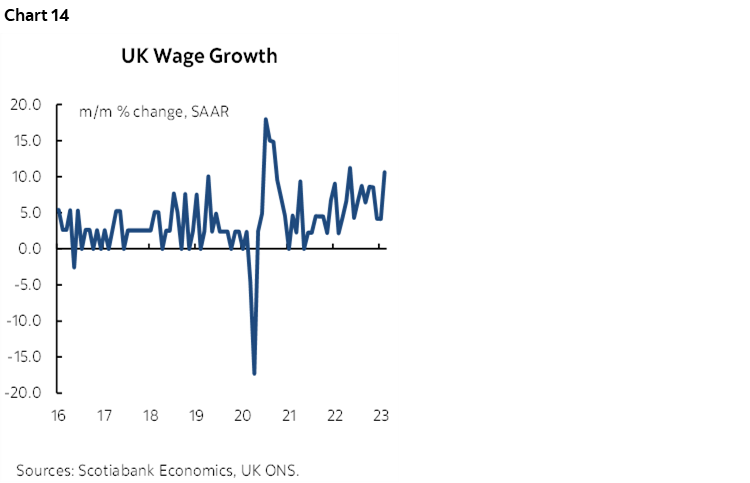

European indicators will include UK total employment and wages for March along with payrolls in April (Tuesday), plus a handful of other measures I’ll write about over the week. That the UK has a serious inflation problem is evident by now, but firm wage growth adds to the risk of persistence (chart 14).

Q1 GDP readings will arrive in the Eurozone (Tuesday), Thailand (Monday), Colombia (Monday), and Chile (Thursday).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.