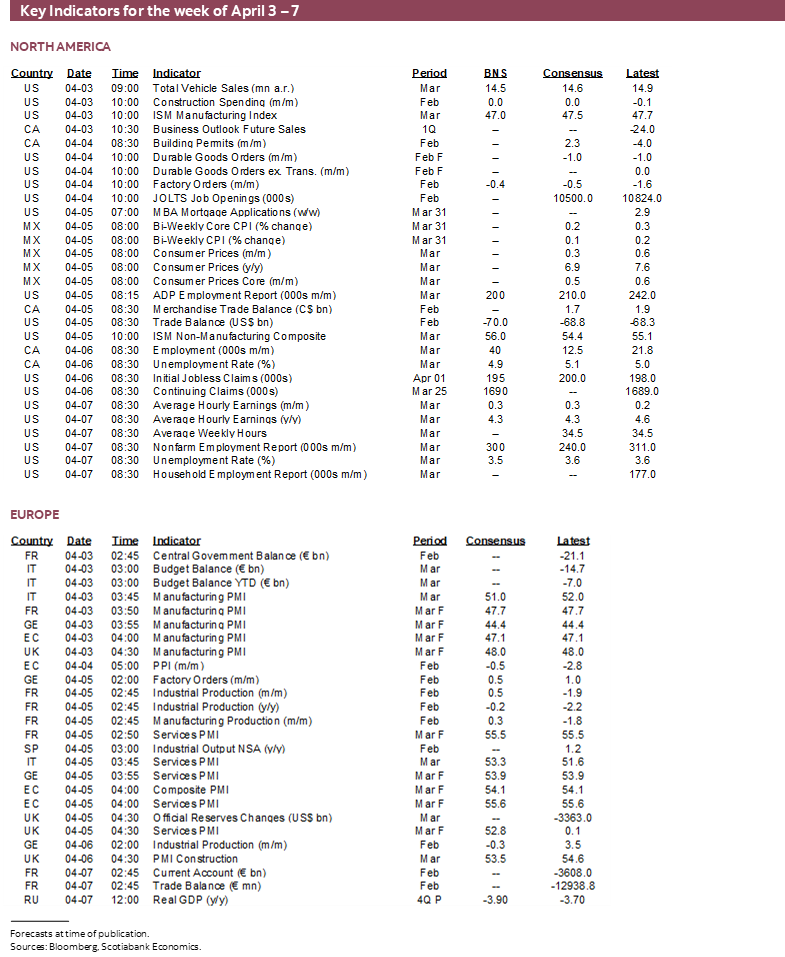

Next Week's Risk Dashboard

- US nonfarm could get a Spring Break bounce

- Ditto for Canadian jobs

- Eurozone inflation & holiday plans

- US services PMI may have jumped

- BoC’s inflation expectations pre-date turmoil

- RBA may pause

- RBNZ could deliver the final hike

- RBI expected to raise its policy rate

- Most expect BCCh to hold

- Inflation: Latam, Asia-Pacific

- Other global macro

Chart of the Week

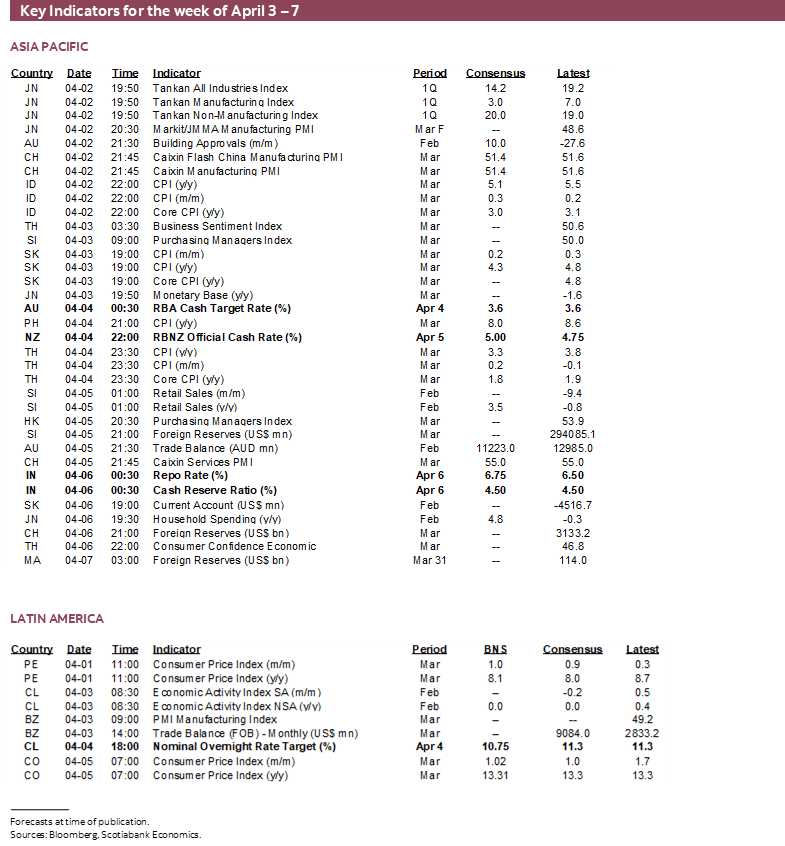

The coming week’s main focal points should be low in frequency but with potentially high impact. Part of the reason for this is that many of the world’s markets will be closed for Good Friday and perhaps Easter Monday depending upon the market and this tends to have a dampening effect on global calendar-based risk.

The coinciding forces of diminishing concern toward the pandemic and seasonal travel may have large effects on macro reports and tracking of high frequency alt-data. Nonfarm payrolls will offer good theater to US markets when much of the rest of the world’s markets won’t be able to react immediately. The focus in Europe will be upon monitoring alt-data for travel activity given potential implications for inflation watchers. Canada also updates jobs. Four regional central banks will deliver decisions and markets will be firming up expectations for the start of the US earnings season the following week.

US NONFARM PAYROLLS—COVID CABIN FEVER COULD BUOY JOBS

The final jobs report before the next FOMC meeting on May 2nd–3rd arrives on Friday and there may be significant upside risk. I’ve gone with an estimate of 300k and a downtick in the unemployment rate to 3.5%. There is always a lot of risk around a nonfarm call and there is also a large 90% confidence interval of +/- 130k (and constantly climbing it seems) to contend with, but I cautiously think there is upside risk to my estimate.

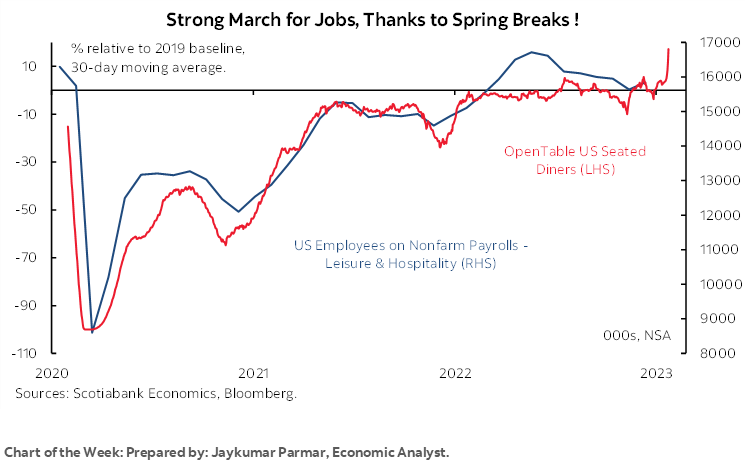

Enter chart 1. It shows a very tight correlation between OpenTable seated diners and the level of employment in the leisure and hospitality category of nonfarm payrolls. Since the data on seated diners is not seasonally adjusted, I’ve also shown seasonally unadjusted employment to be consistent. As restaurants became packed (not the soaring red line), this measure of employment may well have jumped higher. It’s not inconceivable that this category jumped higher by perhaps hundreds of thousands of jobs. March seasonal adjustments usually add around 3% to seasonally unadjusted employment in this category and so the possible surge could be amplified somewhat by seasonal adjustments.

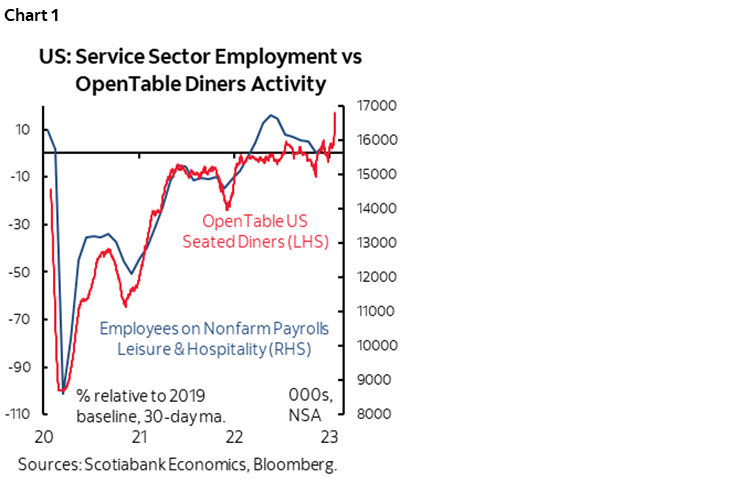

It doesn’t just stop there. Flight data also…hmmm…what’s another way to put it….nuts…took off in March (chart 2). Readings like this suggest that animal spirits were alive and well in a quest to return to more and more normal activities.

This evidence on restaurants and flights may also serve as correlated proxies for other types of activity in the service sectors like retail sales and other services.

Risks into payrolls may be further informed by a series of indicators that are due out before payrolls. Fresh evidence on JOLTS job openings (Tuesday), ADP private payrolls (Wednesday), employment subindices to the ISM-manufacturing (Monday) and services (Wednesday) gauges and Challenger job cuts (Thursday) are among such readings. Job cuts may be elevated but to date there has been an ongoing and powerful rotation effect that has seen hiring sectors offset job losses.

While I’ve also gone with modest wage growth of 0.3% m/m SA it’s feasible that there could be upside risk to this if the above indicators indicate a strong surge in demand for labour.

Such readings on the job market could matter in two respects. One concerns all the talk about peak rates and how the Fed is done or close to being done with markets pricing rate cuts. I think that’s premature but perhaps a strong payrolls number could affect such thinking. Another reason for how it could matter is the connection between strong job readings, a tight labour market and potential future wage growth that could reconnect to Chair Powell’s favourite inflation gauge which is PCE core services ex-housing.

CANADIAN JOBS—MARCH BREAK MAY HAVE PROVIDED A LIFT

Canada also updates jobs for the month of March on Thursday with markets shut for Good Friday. I’ve estimated a gain of 40k and a downtick in the unemployment rate to 4.9%. Like the US, there is a lot of statistical noise around estimated job changes with the 95% confidence interval of +/-57k.

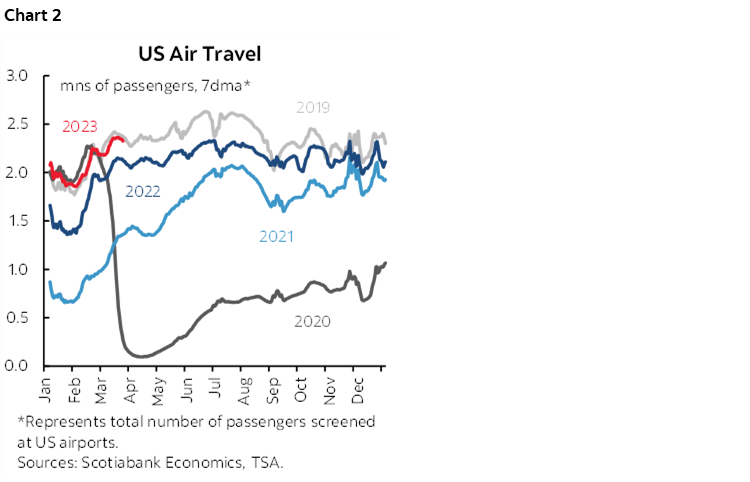

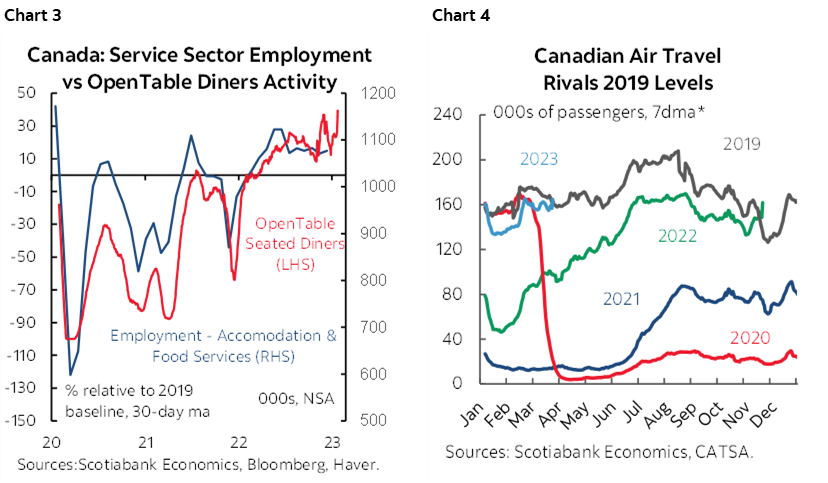

It wasn’t just in the US where Spring break fever hit hard. Canada also had a breakout of its own. Chart 3 is the equivalent to the US chart and displays a decent correlation between employment in the accommodation and food services category and restaurant activity. Flight data was perhaps not as strong as in the US but was still toward pre-pandemic norms (chart 4). Maybe the roughly one-third haircut on the purchasing power of the C$ in US$ terms kept more folks at home in Canada in relative terms.

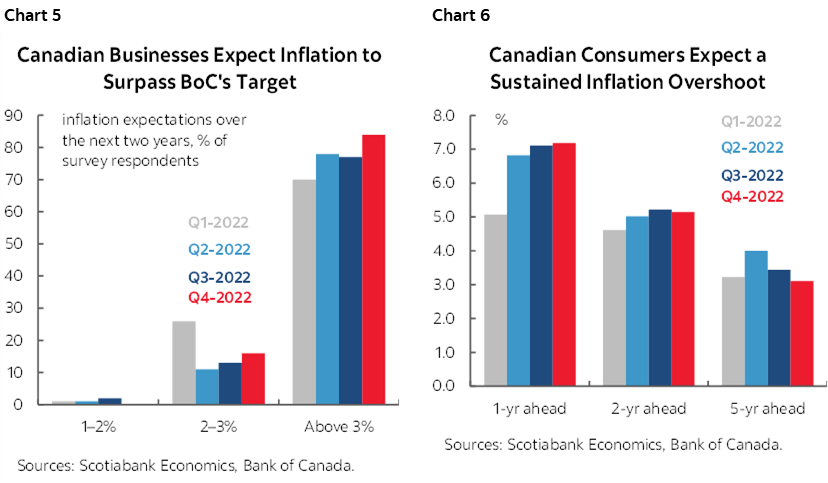

BoC SURVEYS TO INFORM INFLATION EXPECTATIONS

The Bank of Canada will release its twin consumer and business surveys on Monday. Watch measures of inflation expectations in particular given that both surveys are indicating that nobody believes the BoC will hit its inflation target (charts 5, 6).

A significant caveat is that the survey sample periods predate the flaring of pressures in financial markets and banks in the US and Europe. Time will tell if that declares them to be moot characterizations of attitudes and expectations. The Business Outlook survey was sampled in February but the BoC has recently been supplementing the results with an online survey that maybe have pushed further into March while perhaps not yet fully into the period of recent concern.

The consumer survey period was also in February and here too the BoC has been attempting to supplement the results with added sampling that may have also pushed into March.

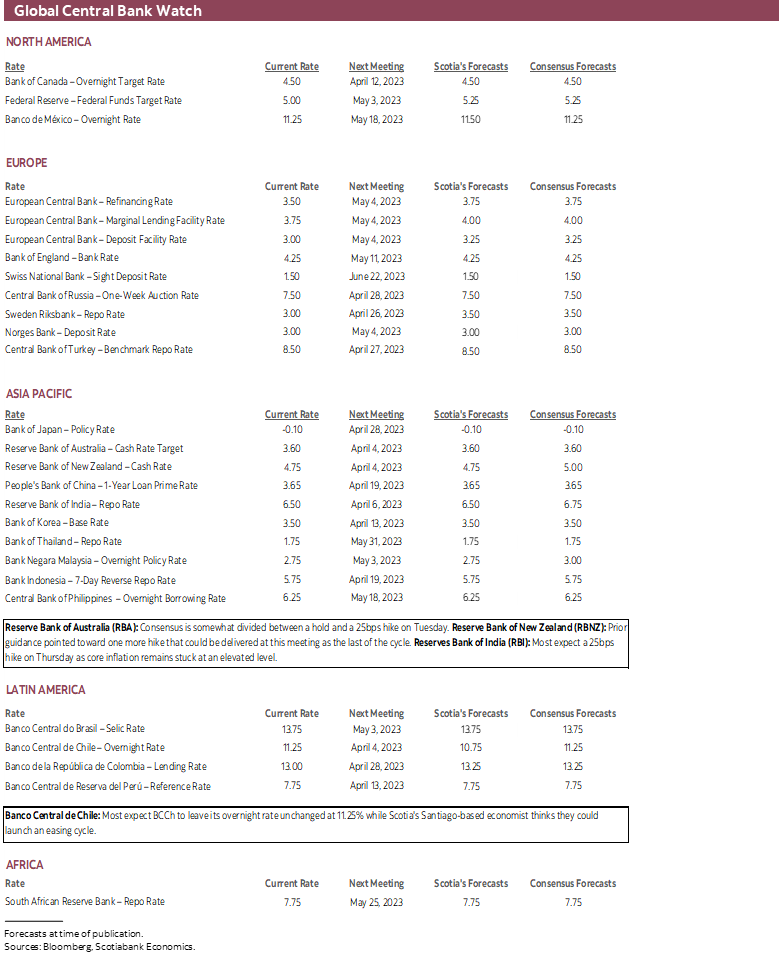

CENTRAL BANKS—MIXED DECISIONS

Four central banks will deliver policy decisions over the coming week with implications more for regional markets than global market conditions.

- RBA (Tuesday): Australia’s central bank faces a somewhat split consensus with the balance of opinion landing marginally in favour of no change to the 3.6% cash rate target. That said, 16 expect such an outcome while a significant number (11) expect a 25bps hike. Markets are priced for no change. CPI recently landed softer than expected at 6.8% y/y (7.2% consensus, 7.4% prior) and the central bank is assessing the extent to which global market turmoil has tightened financial conditions upon Australia’s economy relative to markets (chart 7).

- RBI (Thursday): Most economists expect India’s central bank to deliver another 25bps hike. Markets are less convinced. Core CPI inflation appears to be stuck at around 6¼% y/y which may motivate continued tightening notwithstanding recent turmoil across global banks and markets.

- RBNZ (Tuesday): Consensus almost unanimously expects another 25bps hike to 5%. That would be a downshift from the prior 50bps hike in February when they discussed hiking by either 50 or 75. Forward guidance projected the policy rate to rise to a peak of 5% which could make this the last hike of the cycle pending further developments.

- Chile (Tuesday): BCCh is expected to leave its overnight rate target unchanged at 11.25%. Our Santiago-based economist, Anibal Alarcon thinks they could launch an easing cycle at this meeting.

GLOBAL MACRO—EUROPEAN VACATIONS & INFLATION

The global line-up of other calendar-based forms of risk will be fairly light. One thing to monitor will be alt-data on European travel activity with possible implications for inflation markets and the ECB. Analysts will also be sharpening their pencils with expectations for the US earnings season that kicks off the following week.

European markets face a generally light line-up. Travel plans may figure more prominently given the Good Friday holiday and then the Easter Monday holiday which can be a big deal. Some may tack on the week before, the week after, or maybe both in a ‘why choose’ sense! A rather big problem, however, concerns all of the strikes and protests that are sweeping across Europe. Protests against raising the pension age in France and protesting airport workers in Germany are two examples. Another example is walk-outs by workers at London’s Heathrow airport. Air traffic controllers in Italy plan to walk off the job on Sunday. This could matter to inflation watchers since this travel season can distort headline CPI especially if the quest to return to something more normal confronts travel bottlenecks.

Otherwise, there will be a light line-up of European data. The main focus is likely to come when Germany updates exports (Tuesday), factory orders (Wednesday) and industrial output (Thursday).

US nonfarm payrolls will dominate the US calendar, but several other releases are also on tap.

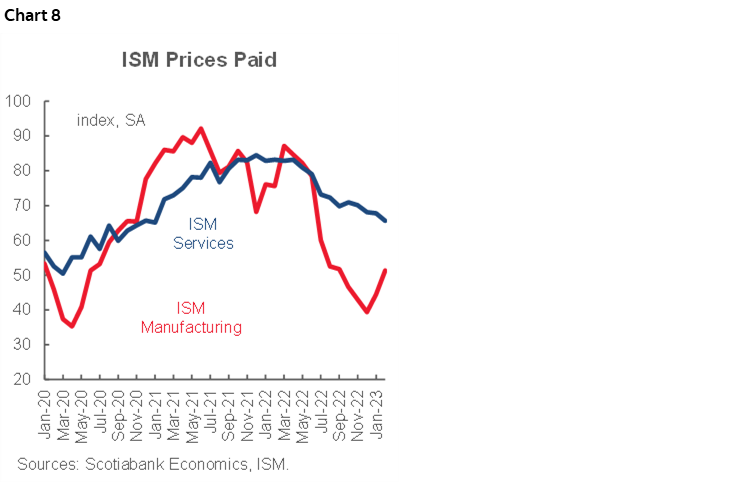

- ISM-services (Wednesday): The March reading could also face upside risk given the evidence on activity at US restaurants and airlines. A reading of 56 is guesstimated, up from 54.5 the prior month. Watch for price signals given that the prices index has been waning over the past year but continues to indicate considerable pressure (chart 8).

- ISM-manufacturing (Monday): Manufacturing probably remained in contraction by this measure.

- Vehicle sales (Monday): The tally for March probably fell by 3–4% m/m SA to about 14½ million based upon industry guidance.

- Construction spending (Monday): This is estimated to have been flat.

- Factory orders (Tuesday): The estimated 1% m/m drop in durable goods orders may be only partly offset by nondurable goods orders.

- Trade (Wednesday): A slightly wider trade deficit may be registered given the already known estimate for the merchandise balance plus a usually fairly stable services balance.

Canada will be primarily driven by its own jobs report plus spillover effects from nonfarm payrolls when Canadian markets reopen the following Monday. Only trade during February (Wednesday) and the Ivey PMI (Thursday) are due out.

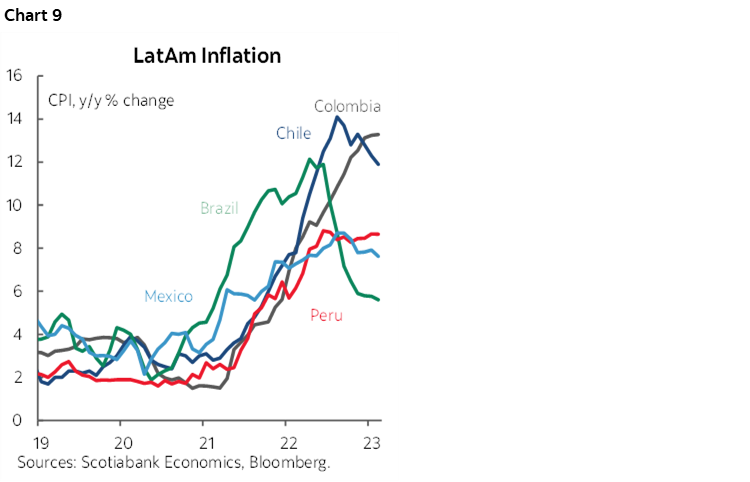

Colombia has among Latin America’s hottest inflation readings of late (chart 9). Divergent patterns are being marked by decelerating pressures in Brazil and, to a lesser extent, in Chile and Mexico while Peru moves sideways. We’ll get updated assessments from Colombia and Mexico on Wednesday and in the wake of their recent hikes, and then from Chile on Thursday.

Asia-Pacific markets face a pretty light line-up themselves. CPI inflation reports arrive in South Korea, Thailand, Philippines, and Indonesia. India updates PMIs (Monday, Wednesday) and China will update its private PMIs (Wednesday).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.