Risk Dashboard for:

Week of March 21st – 25th:

• Where to from here for longer-term yields?

• European PMIs to showcase extent of war damage to the economy

• UK inflation to rise again…

• …and set the stage for Sunak to outline tax relief

• Fed’s Powell, ECB’s Lagarde, BoE’s Bailey to speak

• Banxico to hike again, add to guidance

• Ditto for Norges Bank

• SARB to keep hiking

• PBOC, SNB, Philippines expected to hold

• Three more Canadian provincial budgets

• Other macro

Week of March 28th – April 1st Highlights:

• Another strong US nonfarm payrolls?

• Eurozone inflation pressuring the ECB…

• …less than US inflation is doing to the Fed

• US consumers earned more, spent less

• Canada’s economy: soft January, February rebound?

• CBs: Chile, BanRep, BoT

Chart of the Week

With major central banks out of the way for another round of meetings and before getting into discussion of relatively light calendar-based risk ahead, it’s worth tackling a key debate in markets that surrounds how to determine fair value for longer-term bond yields at present and going forward. This issue affects a number of debates such as the relative attractiveness of longer-term bonds as an investment, whether policy tightening by central banks like the Federal Reserve and Bank of Canada could risk inverting the yield curve and triggering recession warnings, and how much of a further hit could be forthcoming to fixed term household and business borrowing costs.

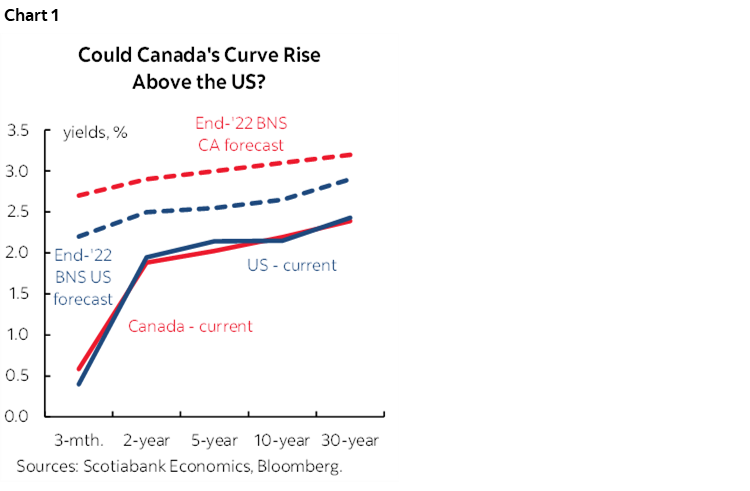

It’s probably logical to start with our forecast. Scotia Economics anticipates the 10- and 30-year yields to end this year toward 2.65% and 2.9% in the US and 3.1% and 3.2% in Canada respectively. Our forecast has the whole Canada yield curve from shorter-term yields through the longer-term moving above the US going forward (chart 1).

Having said that, there is ginormous uncertainty around such forecasts that merits consideration of wide ranges. On balance, we think the longer ends of the curves in both countries remain expensive at present yields but have rather limited conviction in terms of how much that is the case. A reasonable range around our forecast is easily +/-50bps. What follows will hopefully impress upon the reader the fact that overly strong opinions on the direction of the curve in this environment are misplaced such as some of the rather strident claims I’ve seen being made. Instead of emphasizing point estimates, the best approach is to assess reasonable ranges while placing the emphasis upon scenarios in assessing impacts upon portfolio performance and effects upon business plans and hedging risks where suitable and fairly priced. Putting too much faith in point estimates would be unwise and purely speculative.

Rudimentary Expectations Theory

One rudimentary approach is a simple model that is based upon expectations theory that treats longer-term bonds as a proxy for bootstrapped short-term policy rate expectations well into the future. This approach is one of our inputs into the curve forecasts. It’s a contested theory of the term structure with limited supporting evidence, but it offers a starting point. Among the assumptions is that nominal longer-term bond yields should gravitate toward expectations for the nominal neutral policy rate.

An obvious first point is whether such a target can be sustainably hit in future given the pattern to date of large and frequent shocks. We think that we stand a fairer chance at sustainably achieving the terminal rate equivalent of the longer-run nominal neutral policy rate of 2.25-2.5% this time than at any other point in recent years when we haven’t been able to crack 1.75% as a Canadian policy rate throughout the GFC period or sustainably remained at such levels after briefly flirting with them in 2018-19 in the US. Shops with lower longer-term bond yield forecasts than ours have less faith in the ability of central banks to sustainably achieve neutral policy rates this time. This sustainability issue in the face of persistent shocks can account for many tens of basis points of difference in various forecasters’ estimates of longer-term yields.

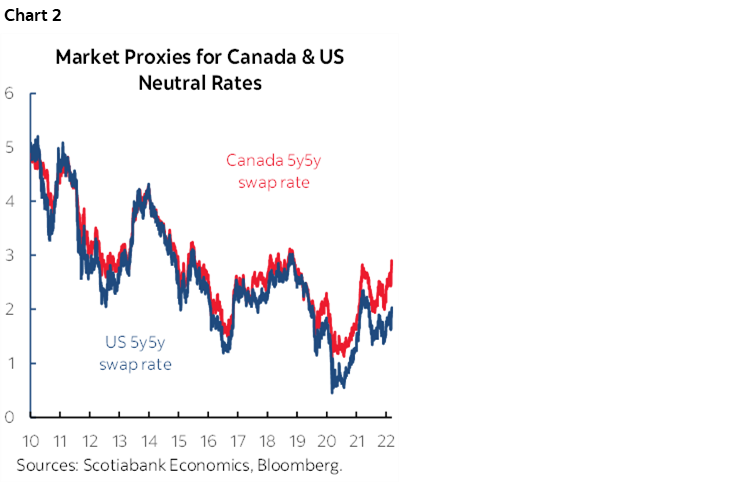

In addition to the issue of perennial shocks, estimates of the nominal neutral policy rates are themselves highly uncertain. Swap market proxies for Canada see the neutral rate at between 2¾% - 3% and US proxies are materially lower (chart 2). The FOMC estimates the US nominal R* rate at 2½% with a range from 2-3%. Federal Reserve economists have estimated that the nominal neutral policy rate may be roughly between 2%-2 ¼% (e.g., the late Laubach with Williams, Lubik-Matthes). The Bank of Canada estimates that Canada’s nominal R* rate is between 1.75% - 2.75% (here). The FOMC figures that the inflation-adjusted or real nominal neutral policy rate is +0.5% with a range of 0–1%. The BoC’s estimate for the real neutral rate would be hinged around the same 2% inflation target and hence between -0.25% and +0.75%.

Why such discrepancies across estimates of what central bank policy rates would exist around perfect equilibrium conditions in the economy? Uncertainty toward estimates of the neutral nominal policy rate have to do with uncertainty around the economy’s longer-run potential growth rate (the non-inflationary equilibrium growth rate) and inflation expectations that may differ between what central banks say they will target and what markets anticipate. For instance, the FOMC thinks the longer-run potential growth rate of the US economy in inflation-adjusted terms is 1.8% with individual participants thinking the range runs from 1.6–2.2%. The Bank of Canada figures that the economy’s potential growth rate over 2021–23 is about 1.6% with a roughly two percentage point bracket around individual years’ estimates.

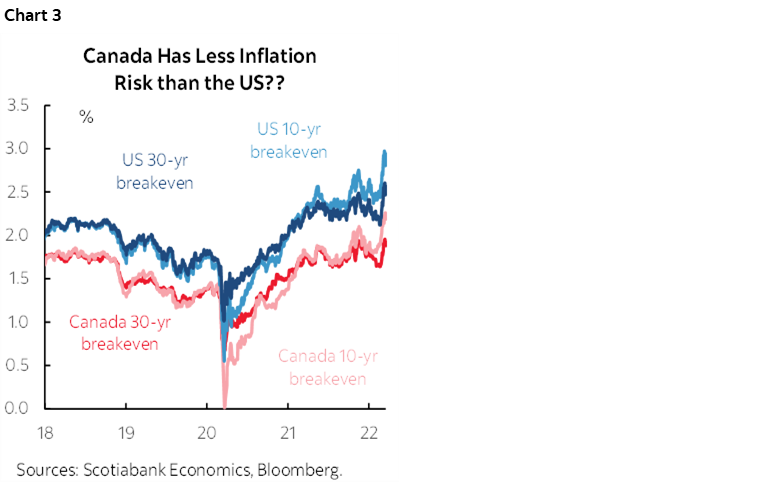

As for inflation expectations, chart 3 shows what is anticipated by investors in real return (inflation-indexed) bonds in both countries. Canadian real return bond holders are implying they believe the BoC will be roughly able to enforce its 2% target over time whereas US investors in Treasury Inflation-Protected Securities (TIPS) think that the Fed may be more challenged and faces greater upward pressure over time. This seems unusual to us in that it’s unclear why the US economy would have so much higher structural rates of expected inflation than Canada and why market proxies would also be pricing lower assumptions on the US neutral policy rate relative to Canada’s. Granted, these are imperfect measures at best. I suppose one possibility is that markets view the Fed as having fundamentally pivoted toward more of a run-hot bias after its revised statement of longer-run policy goals, although the BoC’s inflation renewal agreement late last year raised questions in the minds of investors by mixing messages on inflation targeting and employment objectives.

A starting point to why we’re talking wide ranges for term rates therefore involves recognizing the high degree of uncertainty around where the nominal neutral policy rates may sit in both countries—and hence where real GDP growth and inflation expectations sit—as well as whether the terminal rates may sustainably gravitate toward such measures in the face of uncertainty going forward.

As for longer-run drivers, a key uncertainty is whether we revert to the inflation of the decade or so before the pandemic that resulted in perennially lower-than-forecast rates of inflation, or shift structurally higher. My personal view is that the structural drivers of longer-run inflation have pivoted higher. Trade liberalization that was once disinflationary is gone as supply chains tighten. Technological change that lowered barriers to contestability and information costs may be giving way to greater pricing power by dominant companies. Demographic change may see greater upward pressure upon service prices, especially medical care. If so, then estimates of the nominal neutral policy rate and longer-run inflation expectations may be durably higher than since the GFC.

Time Varying Term Premia

The expectations theory suffers from two main shortcomings. One is that it is based upon rational expectations theory which may not hold at all times (most?) in bond markets.

Secondly, the expectations theory does not consider term premia which is the added yield reward to seeking duration risk. It simply says bond investors only buy 10- or 30-year bonds with the expectation they’ll get compensated for nothing more than what the policy rate is expected to be over the coming year, then one year forward from that, then one year forward two years from now, and so forth. Most bond investors would agree that’s a pretty rudimentary approach that leaves them uncompensated for other forms of risk they may be taking.

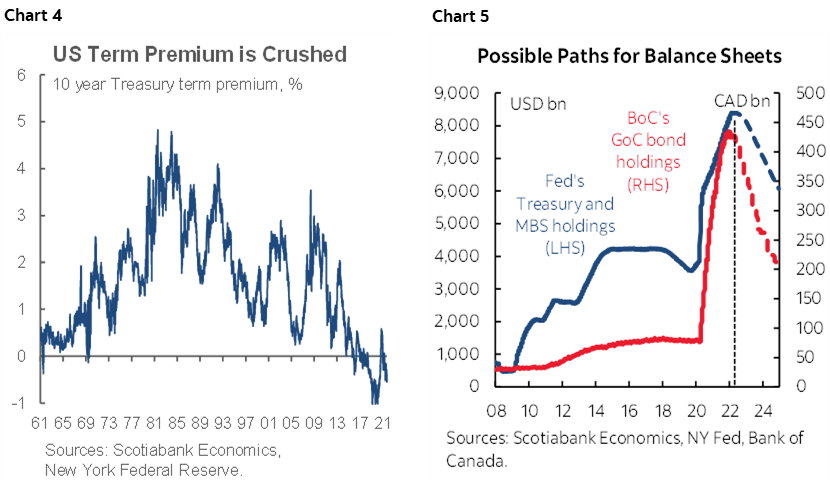

There is high uncertainty around estimates of term premia and how they may evolve going forward. NY Fed economists provide their estimates in chart 4 and there are other estimates as well. Term premia is time varying in nature and can be influenced by various factors including central bank QE programs. At present, the US 10-year term premium is estimated to be about -40bps. It is off the bottom of -1% that was hit when the pandemic first unfolded in 2020, but it is still unusually negative. Going forward, we have assumed that this measure will converge back toward zero or higher in part driven by the Federal Reserve and Bank of Canada shrinking their holdings of bonds purchased during their quantitative easing programs (chart 5). The Bank of England is doing so already, and we expect the ECB to end net bond purchases toward year-end. Because of this coordinated exit from QE programs there could be further upside to this estimated term premia. It would not take much of a positive term premium tacked onto such neutral rate assumptions in order to get the rest of the curve potentially well above 3%.

Time Varying Risk Premia

A time varying risk premia is another influence. There is still a modest safe haven premium that is restraining repricing of longer-run inflation and growth expectations. Some of that is due to the war, some due to China uncertainty and some due to recession risk. The suite of these factors are expected to evolve somewhat more favourably from a market risk appetite standpoint over the year.

If we thought recession risk was more material and that inflation would turn much lower than we have in our forecasts, then tightening at the front-end could risk curve inversion and commit policy error. That’s not what we’re assuming in the rest of our projections but, if we’re wrong on that, then the longer end would be the first to invert. I think that’s unlikely to happen for this year at least.

Connecting Markets Through Covered Interest Parity

For the most part, the approaches explained thus far implicitly assume that we’re dealing with closed bond markets influenced primarily by estimates of US and Canadian neutral real policy rates and domestic inflation expectations. External factors can influence term premia estimates and risk premia, but they are inadequately captured in the approaches utilized thus far.

Another approach that links global bond markets is the covered interest parity model. In its simplest form, it says that the spot currency exchange rate times the return earned off a domestic interest rate should equal the forward exchange rate times the return earned off a foreign interest rate along similarly matched maturity horizons.

This theory helps to understand what has been a major role in driving term yields lower across the dollar bloc (US, Canada, Aussie, Kiwi). With the ECB running a deposit rate at -0.5%, it is essentially paying investors to borrow from it and invest in higher yielding and riskier assets. The Bank of Japan’s -0.1% policy balance rate is similarly designed. That’s the whole essence of negative policy rates and QE programs. As a consequence, investors have throughout the negative rate environment moved into higher yielding US Treasury and Canadian government securities and in the process raised their prices and depressed their yields below what conventional theories rooted in domestic fundamentals would merit. Lower European rates have dragged the dollar bloc’s rates down with them.

A key debate is therefore when the ECB may begin to raise its deposit rate (we don’t expect the BoJ to do so within any reasonable horizon). Markets are pricing policy rate hikes starting later this year.

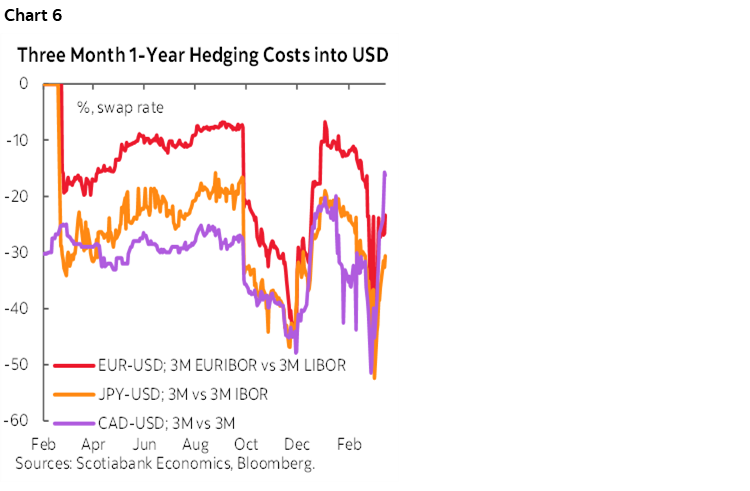

In practice, however, there is a persistent and sizeable error term behind covered interest parity that has emerged over time. Proxies for this so-called ‘basis’ are shown in chart 6. There is a rich literature around why this error term has emerged to be as large as it is. One possible theory is that it widened since the GFC due to a changing regulatory apparatus governing global financial markets. Covered interest parity requires that investors have unmitigated ability to engage in arbitrage by going long or short on relative rates and forward and spot exchange markets in order to keep the relationship aligned. Regulatory policies that limit capital deployment compared to before the GFC may be preventing some of this arbitrage from fully occurring.

Segmented markets

Still here? Good. It’s not over though. I’ve tried to give highlights of the main theoretical drivers of longer-term yields and there are many more considerations than the ones covered here such as technical factors and unexpected issuance supply shocks.

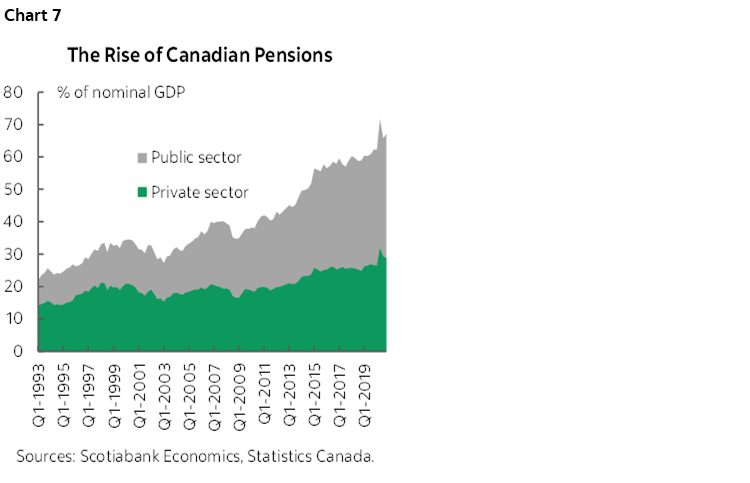

An important one to close on, however, is the rise of longer-term investors. As longer-term investors like pensions have grown, demand for fixed income instruments has risen in order to fund burgeoning actuarial liabilities. This is a structural driver that is closer to its peak than its start given aging populations and a relative shift toward defined contribution pension funds, but it could take years to arrive at such a peak. The rise of pension assets is shown in chart 7. Their rising role has driven greater demand for matched maturity longer-term bonds.

Bond market investors often convey the belief that this structural demand for fixed income instruments relative to the induced scarcity effect upon term premia that has been brought on by central bank buying serves to cap longer-term yields below where fundamentals would dictate. We agree with that, but the key question is to what extent. Our longer-term yield forecasts imply there is further room for upward adjustment but that influences from purely fundamental factors will remain suppressed.

MORE CENTRAL BANKS!

Although the world’s major central banks have all issued recent policy decisions, several of them will follow up those decisions with addresses that may further inform policy expectations. Several regional central banks will also weigh in with decisions all on Thursday.

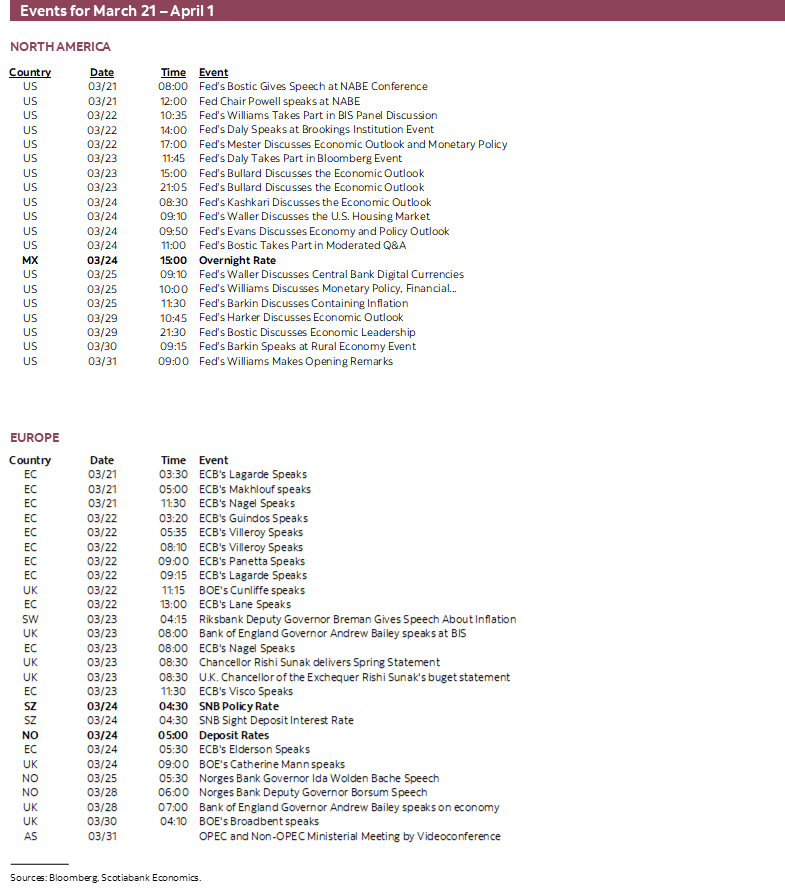

- Federal Reserve Chair Powell speaks on Monday in a moderated session at 12pmET at an annual economists’ convention. Powell speaks again on Wednesday on a panel at an event held by the Bank for International Settlements.

- Bank of England Governor Bailey speaks on the same panel as Powell on Wednesday.

- ECB President Lagarde speaks in a different session at the same BIS conference on Wednesday in a moderated discussion.

- The PBOC is widely expected to leave its one- and five-year loan prime rates unchanged into the start of the week after having left its leading 1-year medium term lending facility rate unchanged recently.

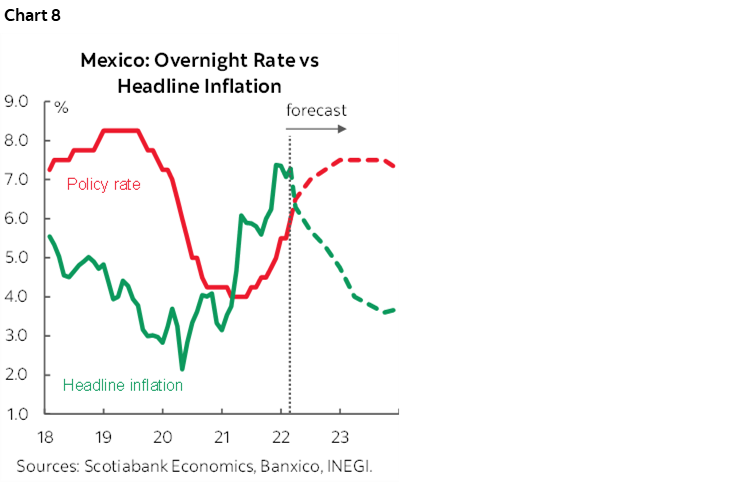

- Banxico (Thursday) is forecast to hike by 50bps. Back in February, Deputy Governor Jonathan Heath stated that “When the Fed increases we’ve always increased at the same pace or more, but never less, so I don’t really see the case for it to be different now. What would make us try to go faster than the Fed is if we don’t see inflation peaking in March or April, maybe a little bit later – that’s the type of data point I would be looking at.” Mexican CPI recently climbed to 7.3% y/y in February with core inflation rising to 6.6%. Uncertainty toward whether Mexican inflation faces a nearer term peak may be diminished in light of the war in Ukraine while the Fed’s more hawkish pivot recently added to expectations for Fed tightening. Chart 8 shows our Mexican economists’ forecasts.

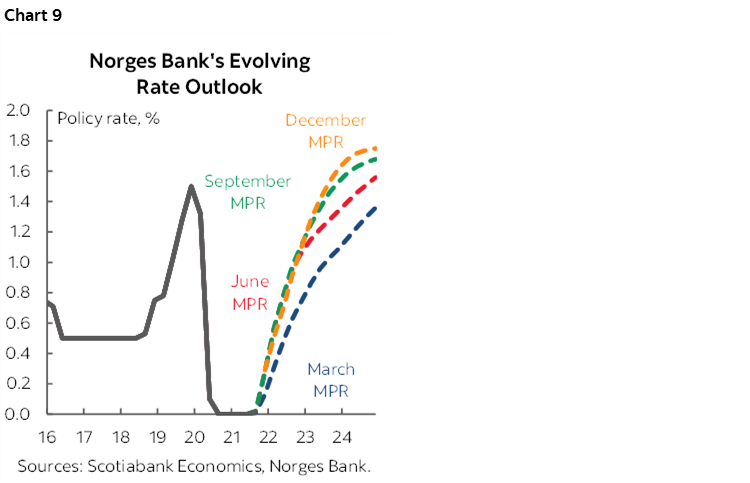

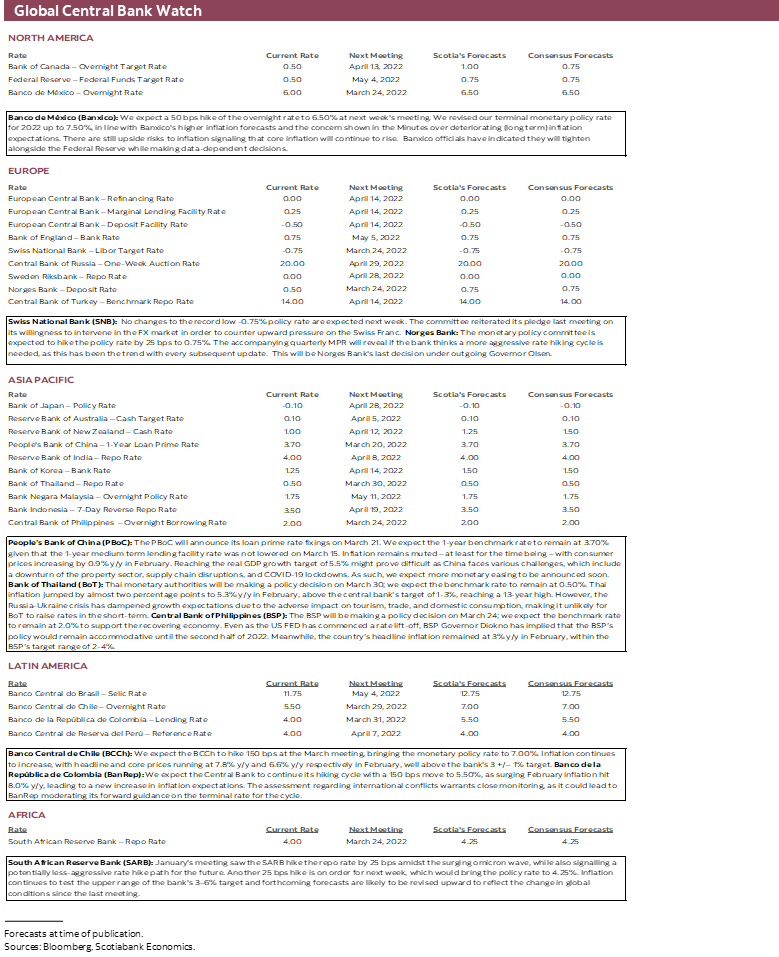

- Norges Bank is widely expected to hike its deposit rate by 25bps on Thursday because, well, they tell you so in advance. The last Monetary Policy Assessment that was published in January stated “the policy rate will most likely be raised in March.” We’ll also get a fresh Monetary Policy Report with this decision. Key may be guidance and whether Norges Bank continues to bring forward higher rate projections in light of additional supply chain and commodity pressures due to the war in Ukraine (chart 9).

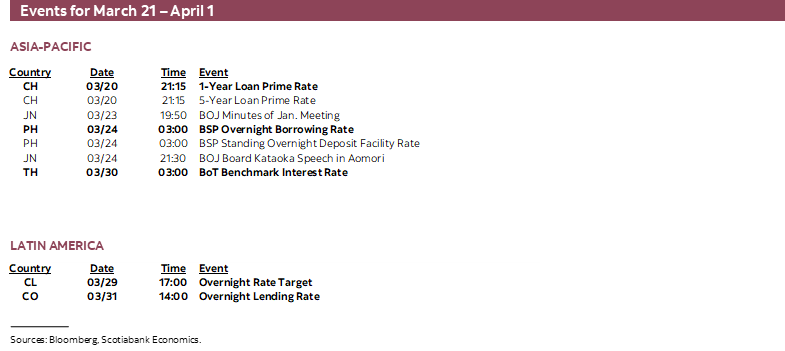

- The Central Bank of Philippines is universally expected to stay on hold at an overnight borrowing rate of 2% on Thursday.

- Swiss National Bank (Thursday) is not expected to alter its -0.75% policy rate. Prior comments on FX intervention may be refreshed given that although the franc has appreciated this month, it has recently pulled off prior peaks.

- South African Reserve Bank (Thursday) is almost universally expected to hike its policy rate by another 25bps on Thursday. That would make for 75bps of hikes since November. The central bank has been tightening on inflation concerns that have probably been inflamed since its last meeting in January.

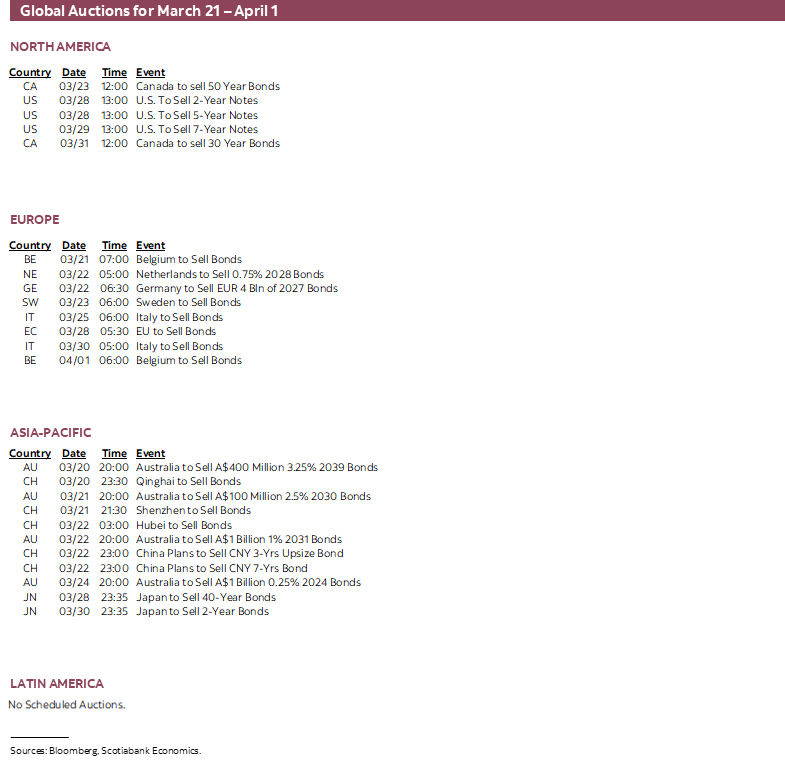

CANADIAN PROVINCIAL BUDGETS

The annual Spring ritual continues with a trio of provinces due to release budgets. That would make it six provinces to file budgets so far including BC, Alberta and PEI that have already announced. That leaves Ontario, Manitoba, Nova Scotia and Newfoundland and Labrador to release. The Federal budget is likely to arrive around Tuesday April 5th.

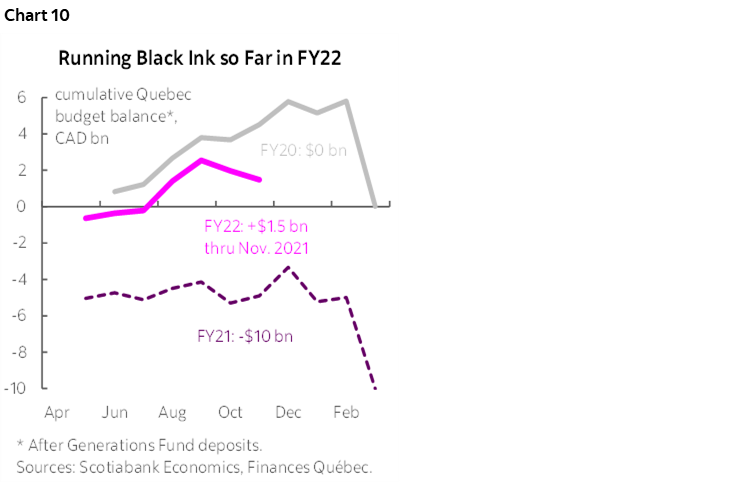

Marc Desormeaux expects Quebec to report modest improvements in its fiscal position—and slightly lower borrowing activity—when it releases the 2022 provincial budget on Tuesday. Nominal GDP growth is tracking more than 1 ppt higher than anticipated for 2021 in the November 2021 mid-year update. April–November 2021 own-source revenues were up more than 21% versus the same period in 2020, in contrast to projected FY22 growth of less than 11% in the mid-year update. Quebec was also running a $1.5 bn surplus as of November 2021 (chart 10) and had already recouped omicron wave job losses as of February. Government messaging suggests that much of the windfall will be devoted to mitigating the effects of inflation—on track to be more severe than previously projected given ongoing supply chain challenges and the Russia-Ukraine conflict.

On policy, we’ll look for three things. First, a credible return-to-balance timeline that keeps the debt-to-GDP ratio on a downward-sloping path. Second, inflation-fighting measures that are time-limited and targeted to lower-income households most impacted by price pressures. Third, updates on efforts to stimulate provincial business investment and long-run productivity gains. The mid-year update highlighted gaps between Quebec and Ontario on several investment indicators and set a target of 1.6% productivity growth per year for 2021–26.

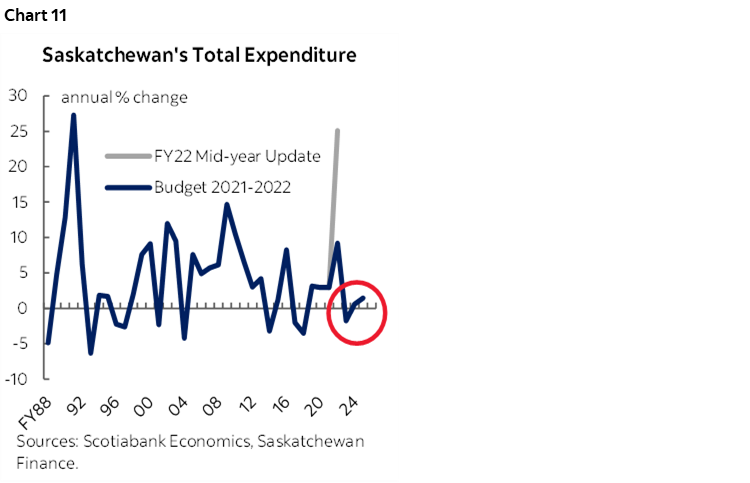

Scotia’s Laura Gu notes that Saskatchewan’s FY23 budget will be released on Wednesday. Recall that last November’s mid-year update projected a record level deficit of $2.7 bn (-3.1% of nominal GDP) in FY22, mainly due to expenses related to the unforeseen drought earlier in the fiscal year (chart 11). That said, we expect favourable commodity prices—mainly oil and crop—to further improve the province’s bottom line. We are likely going to see continued caution in expenditure to achieve the province’s path to balance by FY27 set out in the previous budget. The government’s conservative oil price assumptions should leave room for upside to its current fiscal outlook, which likely means lower borrowing requirements than the $4.7 bn planned for FY22. Nevertheless, Saskatchewan is expected to maintain its fiscal advantage of low net debt-to-GDP ratio in the medium-term.

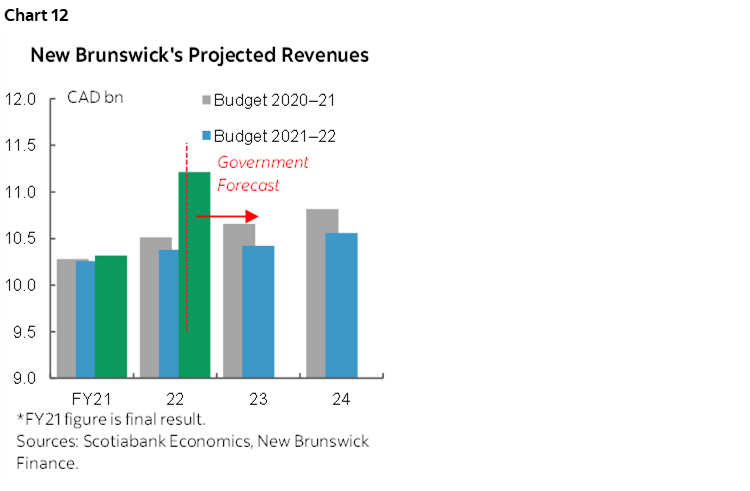

New Brunswick will table a budget on Tuesday and Laura Gu will be covering that event as well. The province projected a considerable $487.8 mn (1.2% of GDP) surplus for FY22 in its third-quarter update—mainly thanks to strong revenue windfalls (chart 12)—the fifth consecutive year in the black. The bottom-line should continue to improve as the economic recovery and population growth persist. The province also tabled a capital plan in December last year, which increased its FY23–FY24 infrastructure spending by almost 19%. The significantly improved fiscal outlook should reduce the province’s borrowing requirements from its latest estimate of $1.25 bn in FY22 as of November 2021, yet higher capital funding needs could offset that effect in part. New Brunswick is expected to reduce its debt burden from 36% of GDP in FY21 to 32.5% of GDP in FY22, and this should decline further as the fiscal outlook continues to improve.

KEY GLOBAL MACRO DEVELOPMENTS

The week’s main economic indicator releases will come from Europe.

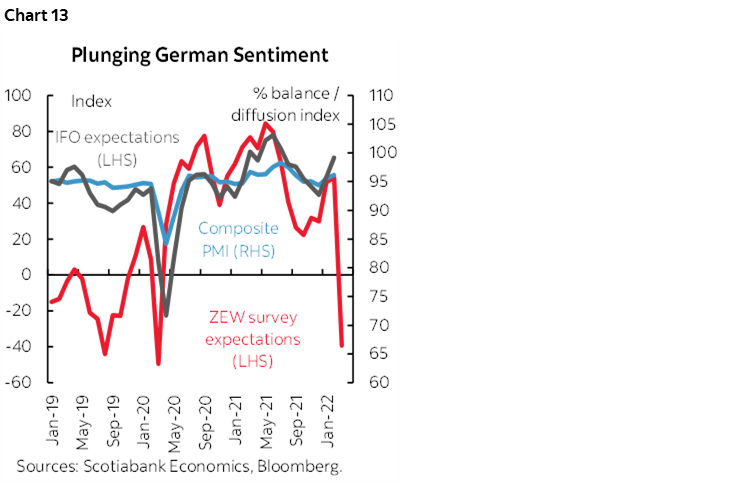

The question at hand is less about direction and more about magnitude in determining how far European purchasing managers’ indices may drop. Eurozone and UK PMIs for March arrive on Thursday. One guide toward what to expect was revealed by Germany’s ZEW investor expectations gauge and the Eurozone version that sank (chart 13). It’s the proverbial canary in the coal mine measure of sentiment gauges in that it precedes release of PMIs and Germany’s IFO business confidence that lands the next day. It also merits noting that both the Eurozone and UK manufacturing PMIs fell significantly after the Russian invasion of Ukraine in 2014, though by nowhere near as much as implied by the ZEW gauge this time.

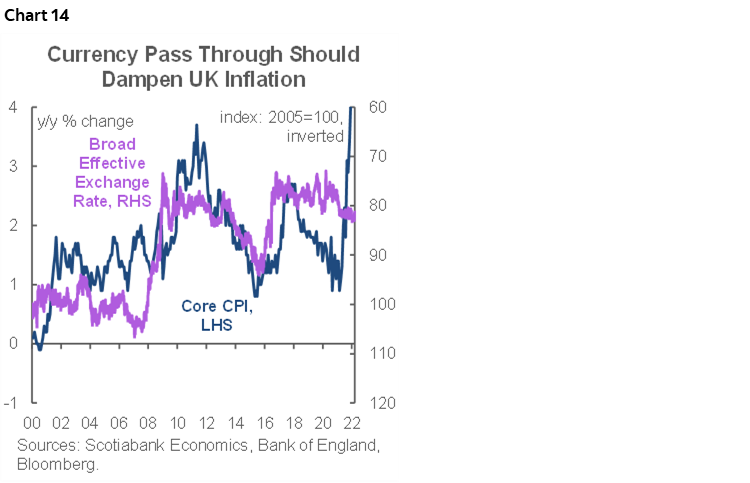

UK CPI inflation for February arrives on Wednesday. The headline rate is likely to approach 6% y/y with core taking a few steps closer toward 5% y/y. Higher food and energy prices will clearly be a driver and one that is likely to push inflation toward the highest reading since 1992. Going forward, if the oil futures curve is on the mark as an imperfect guide to future spot prices then that should combine with dampening influences of exchange rate appreciation (chart 14) to drive inflation significantly lower into year-end. The UK also updates retail sales for February (Friday) which could see higher fuel prices squeezing core sales.

UK Chancellor of the Exchequer Rishi Sunak delivers his Spring Statement on Wednesday. Sunak recently said “My priority going forwards is to cut taxes. My plan over the course of this parliament is to keep cutting taxes, get the tax burden down.” The UK is dealing with the highest tax revenue share of GDP in many decades and so his focus is understandable and means that household and business cash flows could get some relief. One possibility is a reduction of the corporate tax burden. Another is likely to be offsetting measures to cost of living pressures (particularly higher energy costs). Direct assistance could perversely feed inflationary pressures by mitigating the dampening effects upon incomes. Some think Sunak may delay plans to implement a 1 ¼% increase in national health insurance fees.

Canadian markets will be primarily driven by developments abroad and how they may spill over into domestic markets. The only indicator on tap will be producer prices for February (Tuesday) that will translate already known commodity moves into a raw materials index and inform pass-through into intermediate prices. One of the BoC’s Deputy Governors—Sharon Kozicki—will speak about “A World of Difference: Households, the Pandemic and Monetary Policy” on Friday.

US releases will be of the second and third tier variety and include the following:

- New home sales (Wednesday): February’s tally is likely to soften given advance readings such as declining home buyer foot traffic. Pending home sales used as an advance guide to completed resale home transactions are also due out two days later.

- Durable goods (Thursday): February’s tally is expected to dip partly on a decline in aircraft orders. Boeing registered 37 plane orders in February, down from 77 in January, and orders from US airlines fell by half. Sustained momentum in underlying core orders ex-defence and air is expected.

- PMIs: S&P’s (formerly Markit’s) gauges for March arrive on Thursday and may weaken particularly on the manufacturing side given they include foreign operations of US companies that are more exposed to the war’s effects in Europe. By contrast the following week’s ISM gauge focuses upon domestic operations of US companies.

Asia-Pacific markets face very light releases. Australia updates S&P (formerly Markit) PMIs for March on Wednesday and they may face downside risk particularly on the manufacturing side given global developments including the impact of war on Europe but particularly the impact of mounting downside risks to China’s economy. Japan’s Jibun PMIs (Wednesday) face similar downside risk but with the composite gauge already starting from a point of contraction due to the service side. A pair of inflation readings will arrive when Tokyo offers March estimates (Thursday) and Malaysia updates February (Friday), both of which will likely see upside pressure driven by higher oil prices.

Latin American markets also face very light macro developments. Mexico and Brazil will update mid-month CPI estimates for March. Greater upward pressure is expected, but oil prices peaked over the first week of the month and so softer price pressures are likely when the full month’s figures arrive if oil remains off its peak.

SNEAK PEEK AT THE WEEK AHEAD OF THE WEEK AHEAD

Here is a brief look ahead to the main expected developments for the following week of March 28th to April 1st. The accompanying tables provide indicator picks and central bank expectations for this second week ahead.

- US Nonfarm payrolls: Oh, I can just imagine the headlines about how economists got fooled by nonfarm payrolls when they land on Friday April 1st. My estimate is +450k with a slight down-tick in the unemployment rate to 3.7%. Wage growth is expected to accelerate by ~½% m/m and take the year-over-year rate up to 5.6%.

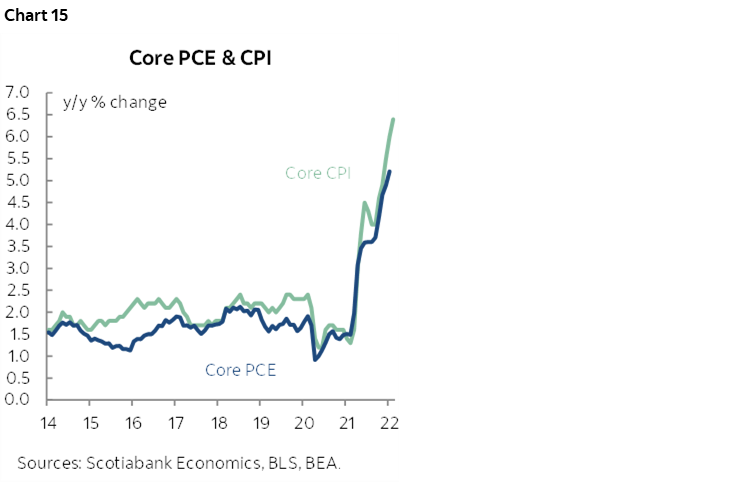

- US PCE inflation: The Fed’s preferred inflation gauges are expected to follow CPI higher (chart 15). PCE inflation is forecast to rise by 0.7% m/m and 6.5% y/y (6.1% prior). Core PCE inflation is forecast to rise by 0.4% m/m and 5.5% y/y (5.2% prior). The same set of numbers is expected to post no growth in total consumer spending as an anticipated lift to services spending will likely be roughly offset by an already known decline in the retail sales control group. Income growth is nevertheless expected to accelerate by ~½ % m/m and rebound from the prior month’s softness that was affected by the end of expedited monthly child benefit payments.

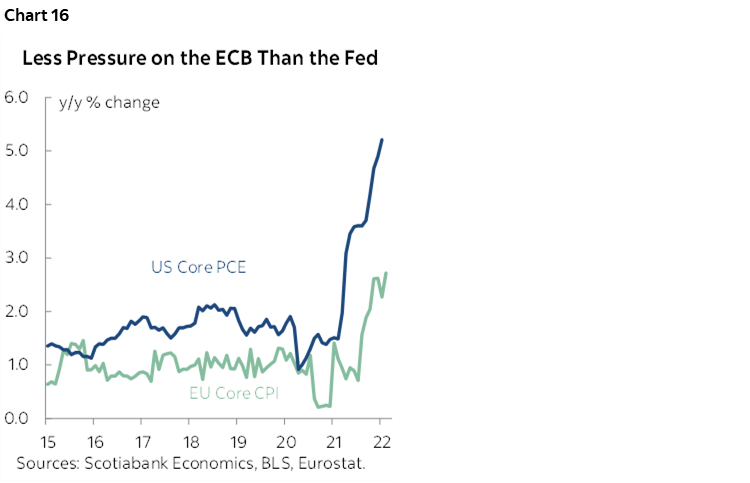

- Eurozone CPI: March’s reading lands just before nonfarm payrolls on April 1st. Further upward pressure is expected on headline inflation given the rise in commodity prices, especially oil. That the ECB faces less inflationary pressure than the Fed and hence less urgency to act is showcased in chart 16.

- Canadian GDP: January GDP arrives on March 31st. Very mild growth is expected based upon advance guidance from Statistics Canada. Advance guidance for February should be more favourable given the strong jobs report.

- PMIs: US ISM-manufacturing will probably showcase additional price stability and supply chain pressures on April 1st. China’s state PMIs are due out two days beforehand.

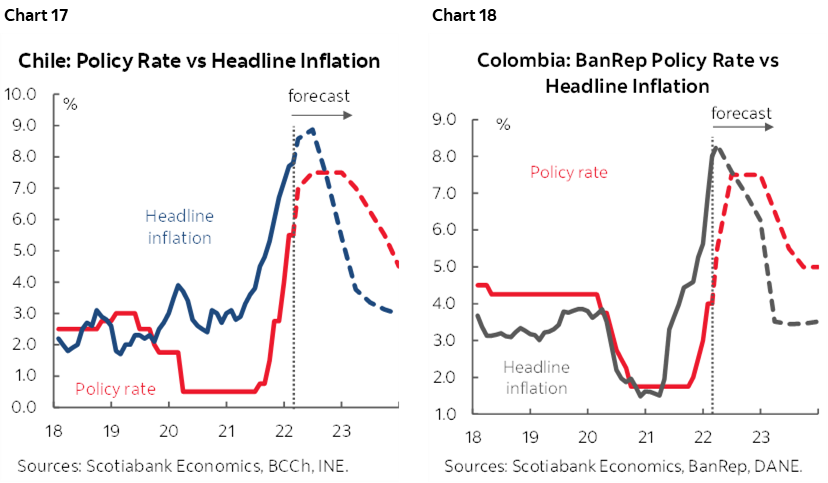

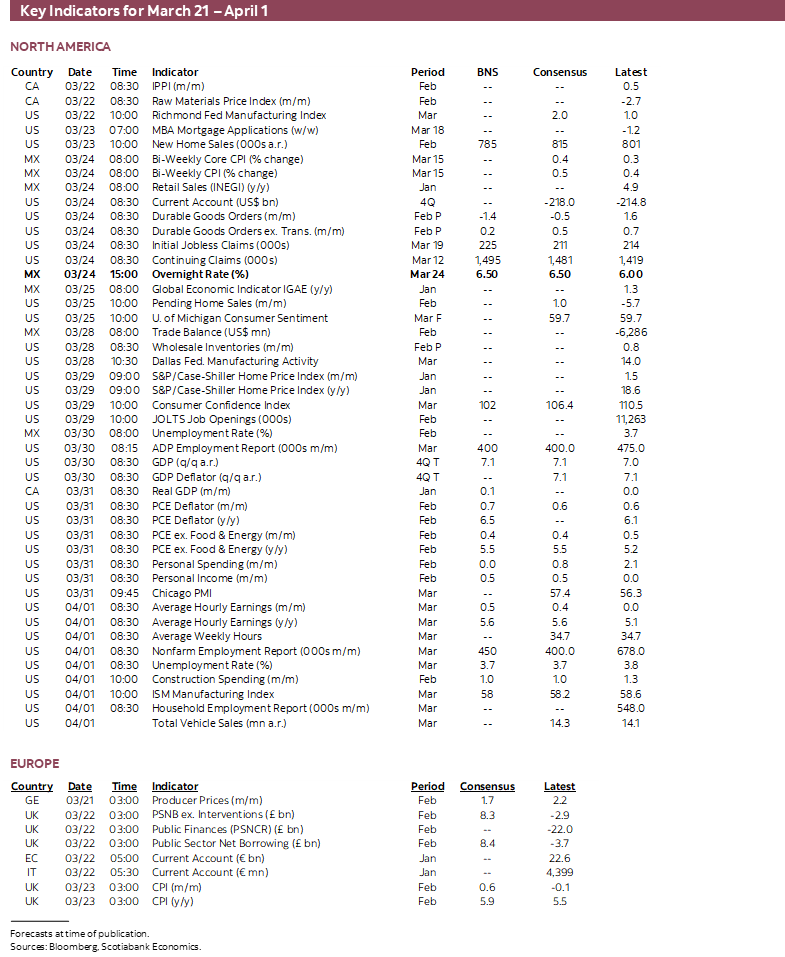

- Central Banks: Chile’s central bank is forecast to hike by 150bps on March 29th. Colombia’s central bank is forecast to raise by an identical amount two days later. Charts 17 and 18 show each country’s expected policy and inflation rates. Bank of Thailand is expected to stay on hold at 0.5% on March 30th.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.