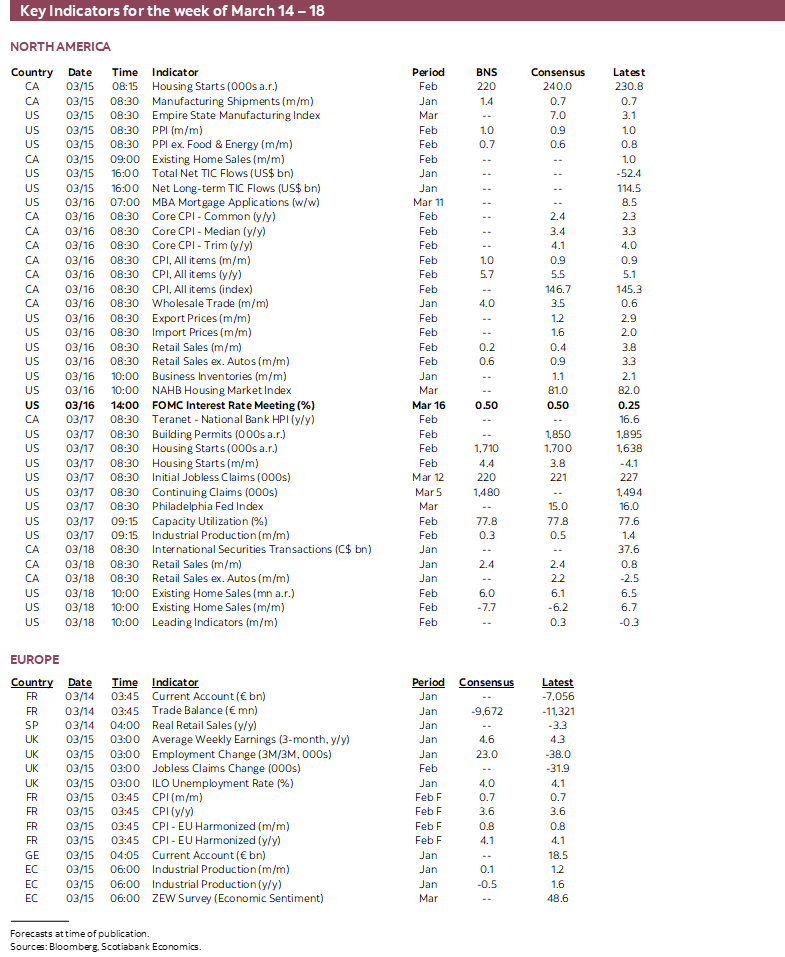

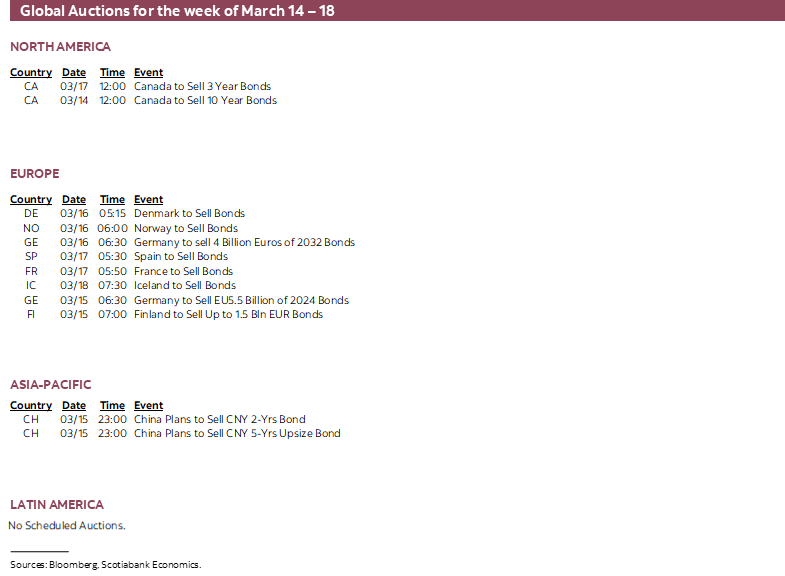

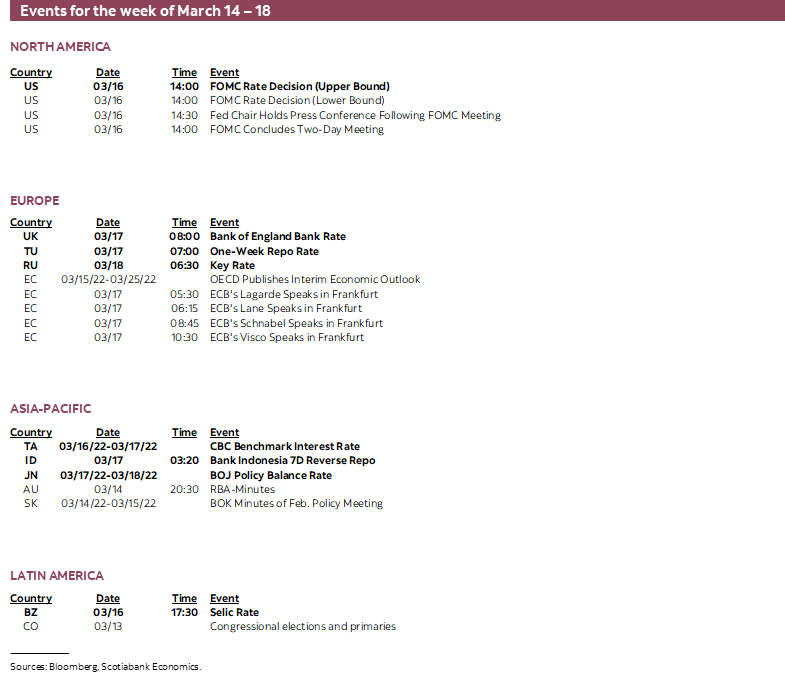

Next Week's Risk Dashboard

• The Federal Reserve’s partially set table

• BoE to hike again, guidance in play

• PBOC on cut watch

• BoJ grappling with high oil

• Brazil likely to hike again

• CBCT, Turkey, BI expected to hold

• Canadian inflation: time to get serious

• Jobs: UK, Australia, South Korea

• Awww, Russia might have to hike again

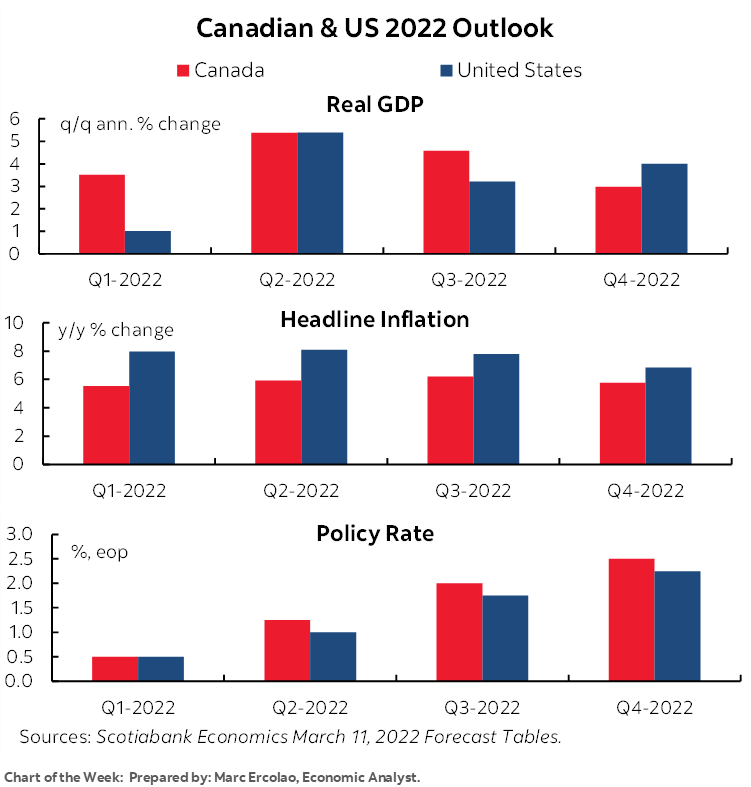

Chart of the Week

FEDERAL RESERVE—A PARTIALLY SET TABLE

In some respects, the script has already been written for this week’s FOMC meeting. It could still, however, prove to be a rather impactful one to markets and with a probable hawkish slant. The two-day meeting starts Tuesday and ends Wednesday when the statement, Summary of Economic Projections, and dot plot will be delivered at 2pmET and followed by Chair Powell’s press conference.

The part of the punchline that seems to have been delivered in advance through Chair Powell’s still fresh semi-annual testimony before Congress on March 2nd – 3rd is as follows:

- they’ll hike 25bps at this meeting;

- they are open to 50bps moves if inflation surprises higher for longer, which implies some patience in evaluating the data versus a surprise jolt at this meeting;

- they plan a series of rate hikes;

- the war in Ukraine represents significant risk to the ultimate path which he noted will be with us for years and is among the arguments for “being nimble” and making necessary decisions along the way, which is experience talking;

- that they will further discuss but not finalize balance sheet plans at the March meeting and therefore won’t have a decision at the ready on reinvestment plans.

I’d also like to hear somewhat of a dialogue around the Fed’s thinking on how it can manage shock risk and the severity of the shock at hand.

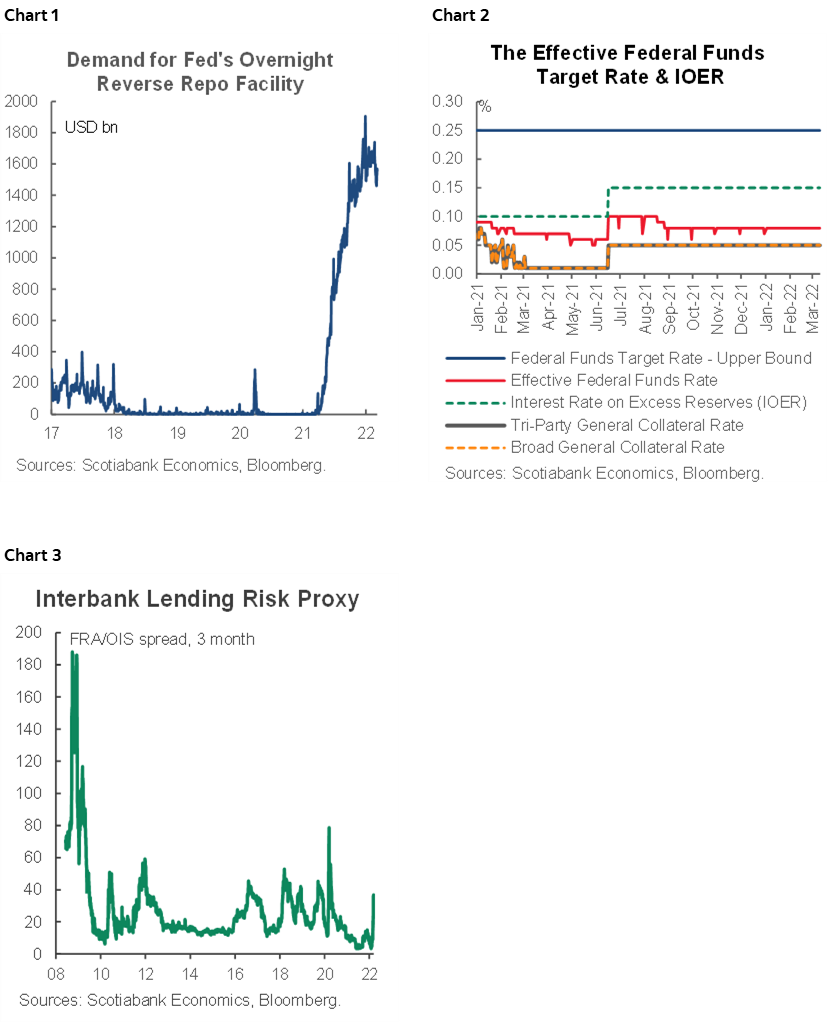

On managing potential shock risk, the Fed tentatively believes it has the market infrastructure in place to manage shocks to dollar funding liquidity as an important source of support to global markets. It’s likely right in believing as much. This includes through its repo book that is holding steady (chart 1) and the standing repo facility plus a different relative rates corridor (chart 2) to more effectively manage relative short-term rates alongside dollar funding and liquidity challenges such as in the event of widespread Russian defaults or some other catalyst. Execution risk may well still matter, but in theory the Fed can reset the price of dollar funding higher while simultaneously maintaining adequate dollar liquidity around its target rate ranges. There may be lower execution risk surrounding the Fed’s response to crises this time because of the Standing Repo Facility that makes markets less vulnerable to guessing what liquidity actions will be announced by the NY Fed’s markets desk, such as amounts, pricing and duration of repo operations. Instead, more of that power is now placed directly into the hands of market participants. Market measures of funding stress tend to believe them so far (chart 3).

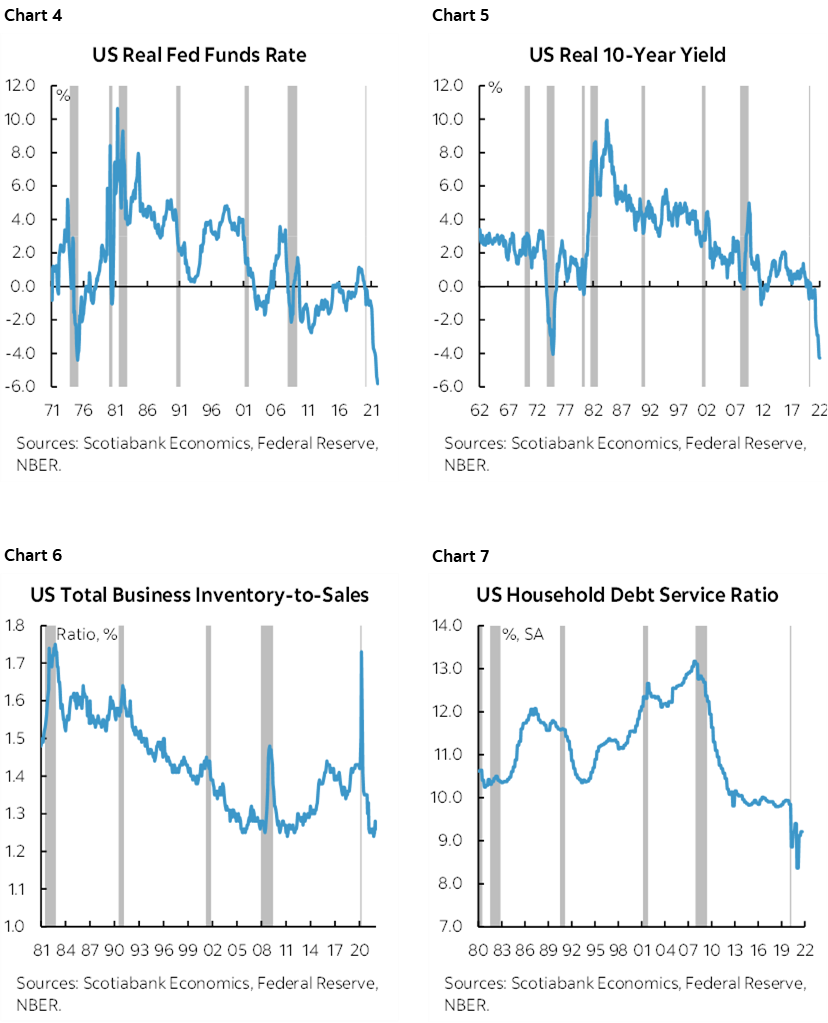

On the probability of sharper downside risk and whether by tightening policy the Fed is courting recession risk that some have recently played up, we need to consider a broad suite of evidence such as shown in charts 4–7 with NBER recessions denoted by grey bars. For instance, it would be super unusual and unprecedented to face recession given how deeply negative the real policy rate and real 10-year Treasury yield have become. It would also be unusual to face such risk given how lean inventory positions have become and the lack of clear evidence that household imbalances are becoming untenable. In fact, by multiple measures, household finances are the best ever which doesn’t mean that consumption growth won’t slow in the face of cost of living pressures but this does provide protection against severe downside risk compared to prior cycles.

But we can’t just leave it at that. There remain three major forms of uncertainty into the meeting.

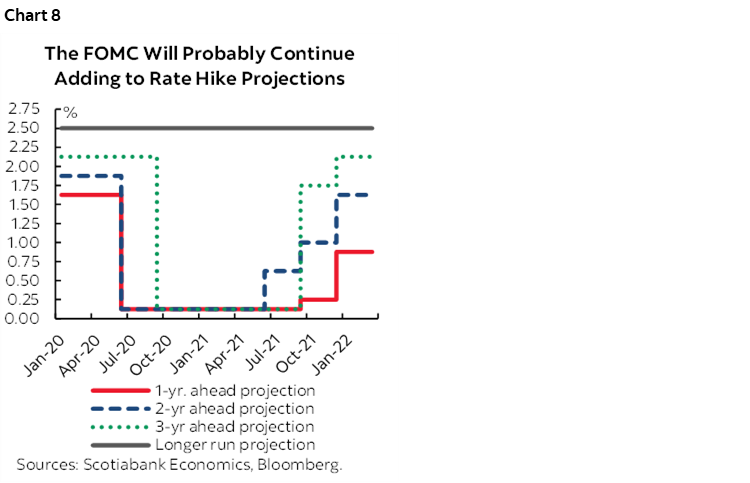

1. The Dots: Way back in December, the median FOMC member’s projection called for three rate hikes in 2022, three more in 2023 and two more in 2024 followed by a longer run equilibrium neutral rate estimate of 2½%. There was a wide dispersion around each of these estimates particularly over 2023–24 as shown in the original document (here). The median projections only began to anticipate rate hikes years down the road starting in December 2020 and have since been progressively brought forward and raised (chart 8). Markets will pay keen attention to how much higher they go and how much sooner. The common expectation is that the FOMC will tread carefully and maybe add a couple more hikes to this year, but the risk could very well slant toward both higher and earlier than previously anticipated.

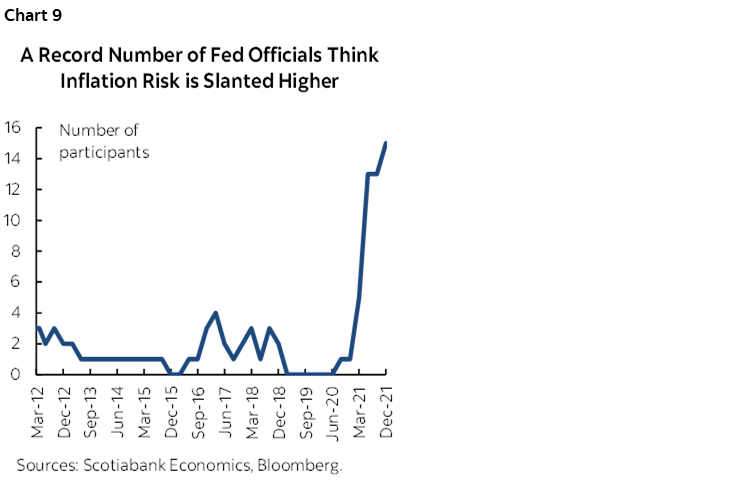

2. Projections: The FOMC participants submit forecasts for GDP, inflation and unemployment rates on the Friday before the meeting and can revise as late as the end of the first day of the two-day meeting. For some time now there have been more and more FOMC members getting increasingly worried about upside risk to inflation (chart 9) and they are likely to further translate such concerns into a material upgrade of inflation forecasts at this meeting. Projections regarding how high and for how long on inflation plus how long and how durably they foresee lower unemployment will help to inform the committee’s stance.

3. Press conference: Chair Powell has freer rein to guide the direction of risks on important matters such as pace and level of rate hikes over time, as well as revealing further colour on the committee’s discussions around roll-off caps that would inform expectations for how quickly they may shrink the SOMA portfolio of Treasury and MBS holdings. To date he has said that the nature of the pandemic versus the aftermath of the Global Financial Crisis merits shrinking the balance sheet more rapidly. Watch for reference to how rapidly.

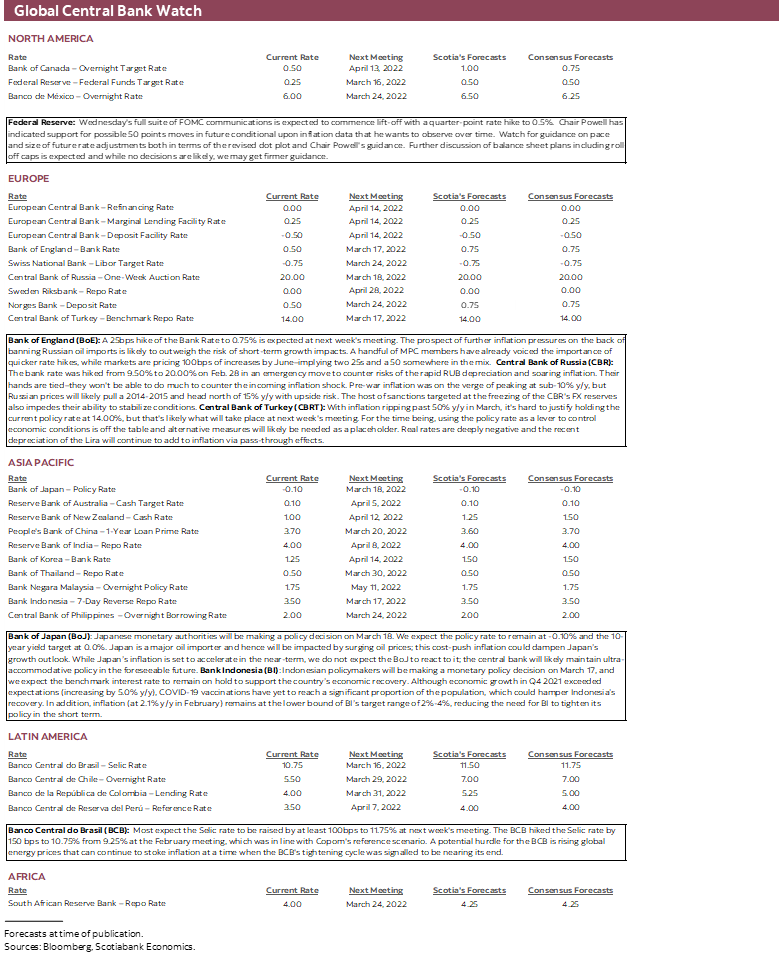

OTHER CENTRAL BANKS—HIKES, HOLDS, MAYBES

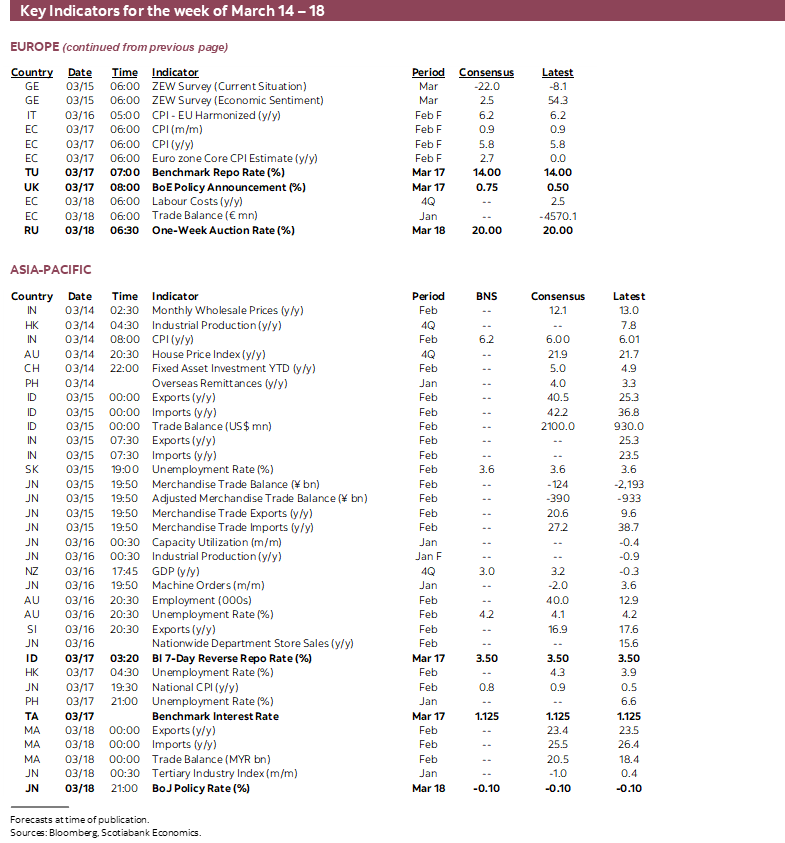

While the Federal Reserve will probably be the most impactful, several other central banks will deliver policy decisions in a mixture of hikes, holds and maybes. Here they are in chronological order.

- PBOC: The People’s Bank of China sets its Medium-Term Lending Facility Rate on Monday evening eastern time. There is a fairly wide dispersion of opinion on this one. About 60% of consensus expects no change to the 2.85% rate, but the remainder expect a cut and probably one on the order of about 10bps. Mounting downside risks to China’s economy at very low inflation rates merit additional policy easing in my view.

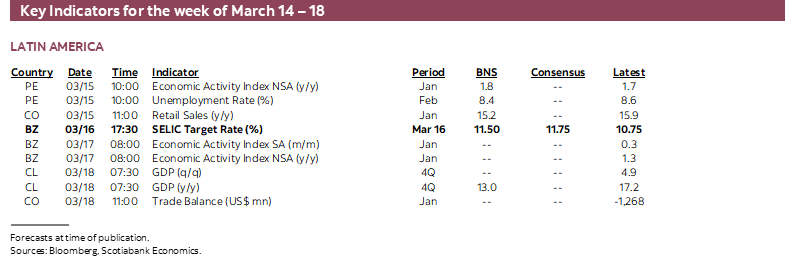

- Brazil: Wednesday’s decision from Brazil’s central bank is expected to hike the Selic rate by another 100bps to 11.75% in the face of mounting inflation risk that could extend the hike cycle.

- Central Bank of China Taiwan (CBCT): No change in the benchmark rate of 1.125% is expected (Thursday).

- Central Bank of Turkey: No change is expected to the one-week repo rate of 14% (Thursday).

- Bank Indonesia: No change is expected to the 7-day reverse repo rate of 3.5% (Thursday).

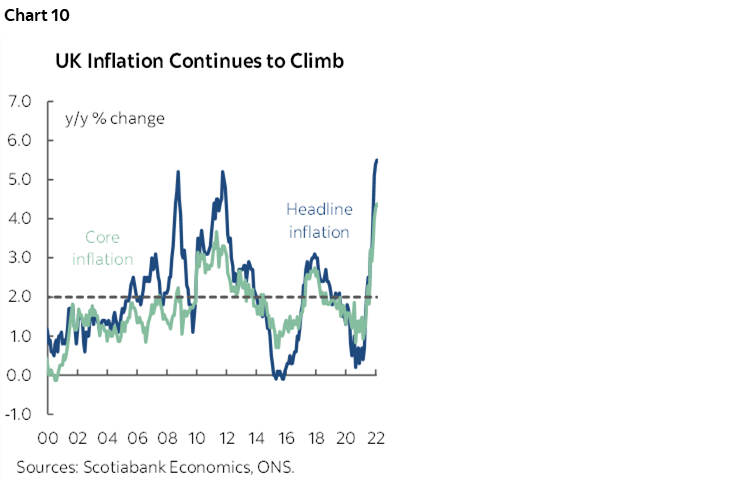

- Bank of England: Thursday’s decision is expected to result in another 0.25% Bank Rate hike to 0.75%. We may see some more hawkish dissent in favour of a larger move. Guidance will be key as upward pressure upon inflation that is already exceeding targets (chart 10) will be weighed against uncertainty stemming from the impact of the war in Ukraine. That might be enough to tamp down reference to “some modest further tightening” being required given the BoE’s closer proximity to the war’s effects, but the BoE’s higher rate of core inflation (4.4% y/y) than the ECB’s, its continued rise, and the likelihood of further upward pressure have me thinking they’ll deliver a hawkish surprise to markets.

- Bank of Japan: The late-week decision is likely to reference downside risks given the country’s heavy dependence upon imported commodities and namely oil. An imported relative price shock is more likely to be viewed as disinflationary on second round effects than inflationary by the BoJ while it keeps policy instruments unchanged at this point.

- Central Bank of Russia (CBR): Consensus is somewhat divided toward the prospects of either holding the key rate at 20% or hiking it further on Friday and after the 10.5 percentage point hike following Russia’s invasion of Ukraine. Bad luck to them I say!

CANADIAN INFLATION—TIME TO GET SERIOUS

Canada updates inflation for February on Wednesday. It will probably be another hot one, but at the same time it will just be a warm-up act for what lies ahead.

I’ve estimated CPI will rise by 1% m/m in seasonally unadjusted terms and that this should pop the year-over-year rate higher to about 5.7% (5.1% prior). Traditional core inflation measured as CPI ex-food and energy should hold steady at around 3½% y/y and modest further upward pressure upon central tendency measures is likely. If it were just up to base effects, then we would be expecting the inflation rate to pull back by about half a percentage point. It’s not and for a few reasons.

February is usually a strong seasonal up-month for prices. Further, higher gasoline prices should add about ¼% m/m in weighted terms and hold steady in terms of year-over-year weighted contributions; gasoline prices would have dragged inflation somewhat lower had it not been for upward pressure on commodities into 2022. A reopening effect may add to price pressures especially, well, when you create 337k jobs in one single month.

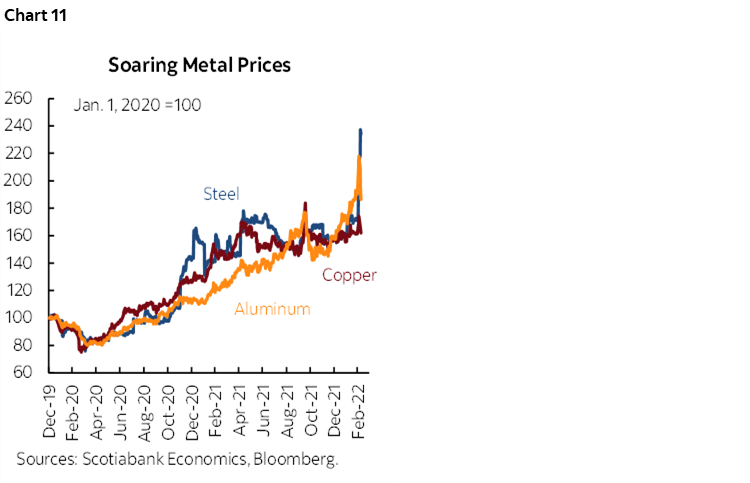

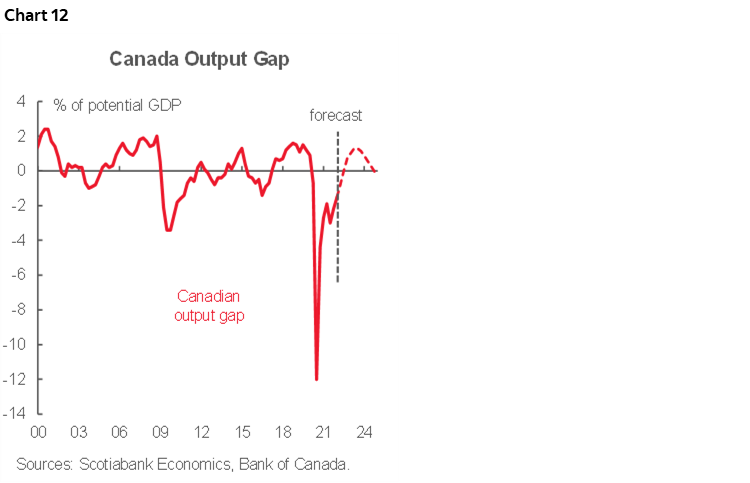

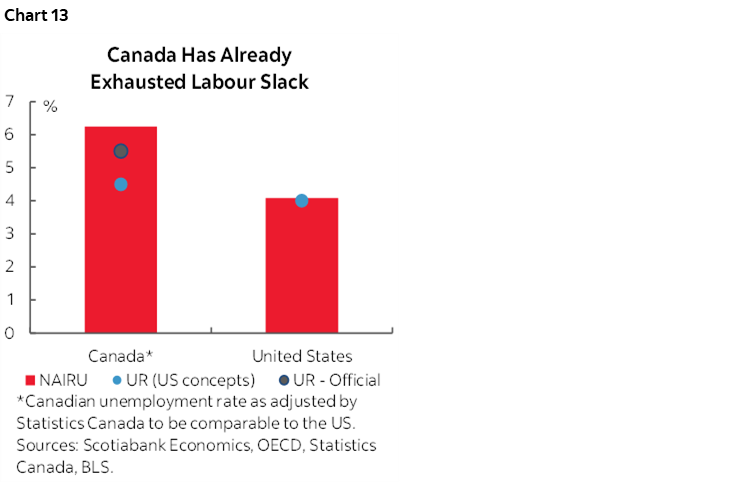

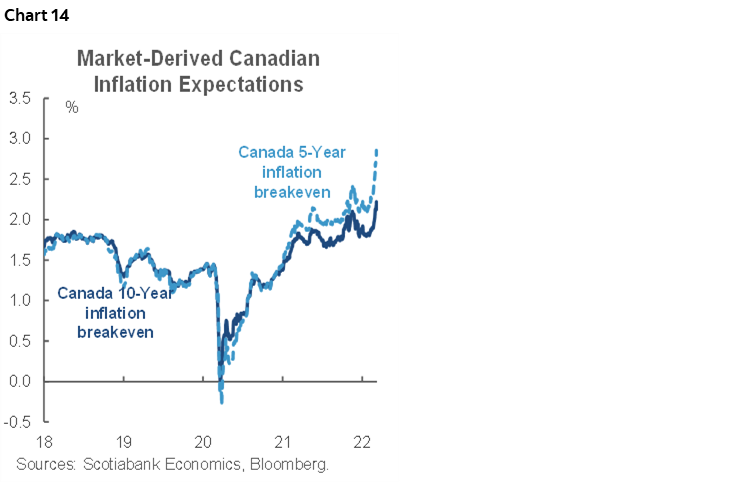

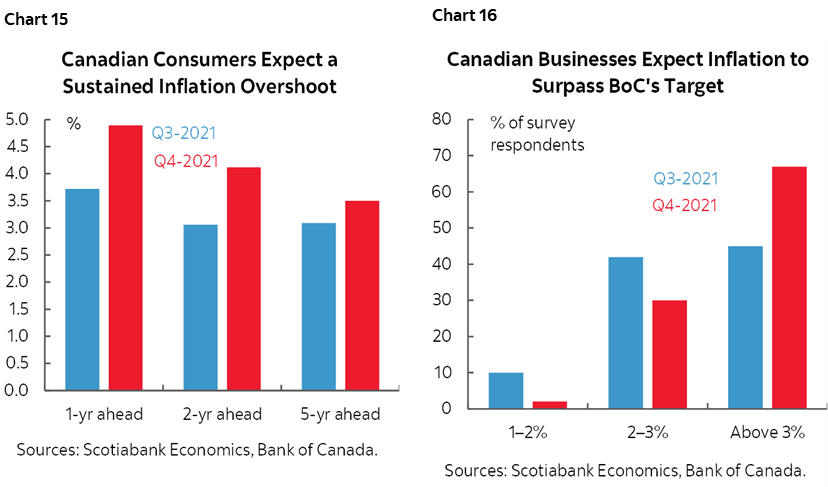

It’s the path forward that has us more concerned. If oil prices remain at similar levels for longer than the period since early December, then the BoC’s rule of thumb that assumes a 10% rise in oil prices adds ~0.3 ppts to year-over-year CPI inflation would have energy lifting CPI by around two percentage points later this year given the magnitude of the changes in WTI plus the spread compression in Western Canadian Select relative to WTI. CAD weakness may bolster upside risk. A panoply of soaring non-energy commodity prices will add to pass-through price pressures (chart 11). Canada is venturing into the realm of excess aggregate demand (chart 12). Canada’s unemployment rate is beneath estimates of the noninflationary level of unemployment that is usually deemed to be structurally higher than in the United States (chart 13). Measures of inflation expectations are taking off including market gauges (chart 14) and survey gauges that were last updated in January and pending April updates that will sample household and business expectations over the period from mid-February to early March when commodities were taking off (charts 15, 16).

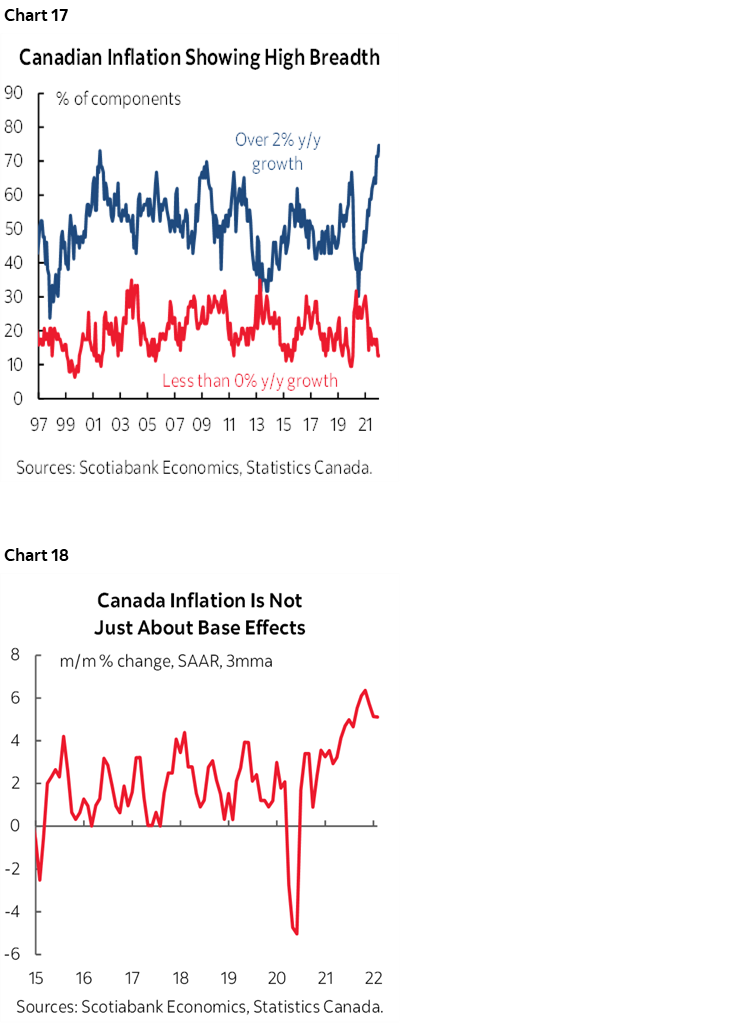

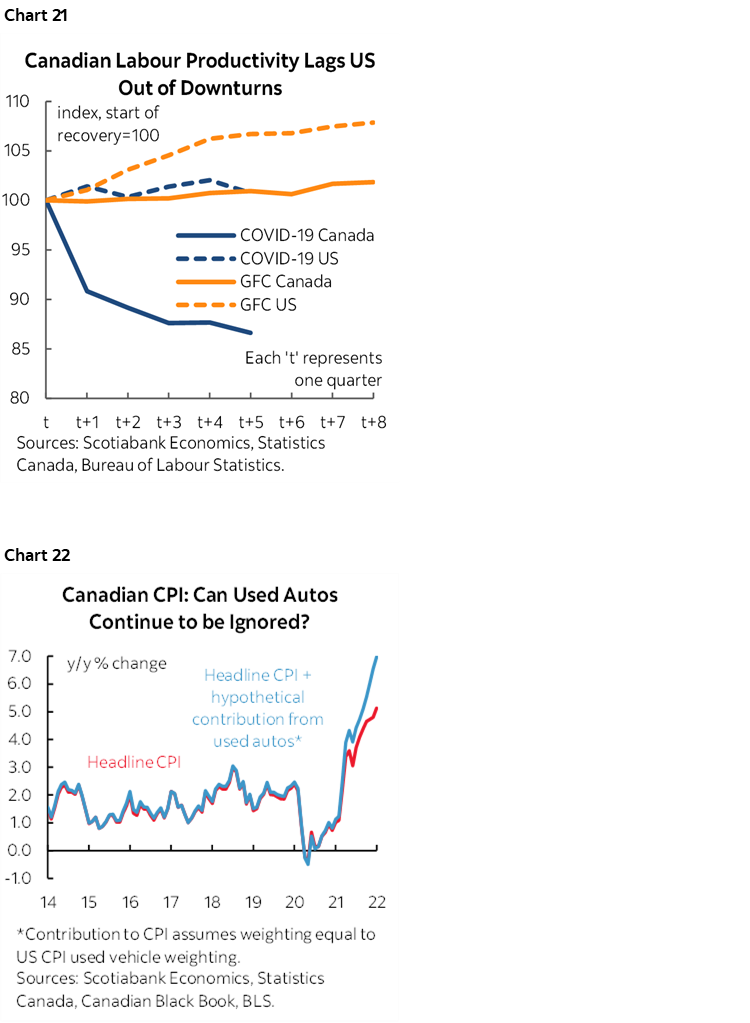

Further, the breadth of price gains is historically very high (chart 17). Inflation is being sustainably driven by serial shocks and structural pressures as opposed to silly talk of base effects (chart 18). Inventories are at bare bones levels (chart 19). Productivity growth is entirely absent so far this cycle (chart 20). Money supply has exploded (chart 21). We also have high confidence that official statistics understate true inflation and hence make it farcical to claim that Canada is managing inflation better than others around the world; one example is the Canada cooks the figures by excluding some of the hottest items (chart 22).

At risk is the further unmooring of inflation expectations. That puts the country into uncharted waters in its roughly thirty-year history of inflation targeting. While economists endlessly debate how much of inflation is due to supply-side versus demand-side versus idiosyncratic factors, perhaps more sensible folks on mainstreet and in markets could no longer care less. They are driving extrapolative expectations for further inflation. Adaptive expectations are in the driver’s seat. That is the alarm bell to central bankers in that it’s the clearest evidence to date of a credibility problem.

So we have to ask, are you an inflation-targeting central bank? Or an inflationist? If it’s the former, then perhaps step up and prove it at the April meeting.

MACRO READINGS—REGIONAL INFLUENCES

There are no knock-out releases on tap across global markets, but several readings could be impactful to local markets.

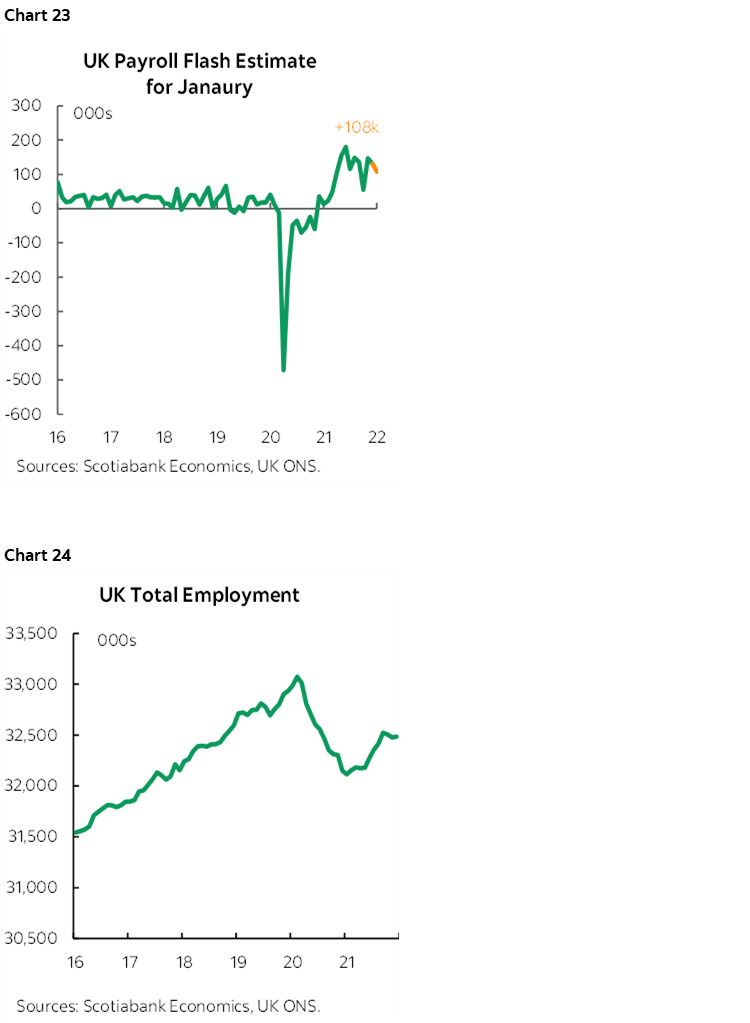

For starters, a round of employment figures land next week with UK and South Korean jobs leading on Tuesday followed by the Aussies on Wednesday.

Flash UK payroll data published by the Office for National Statistics in advance of Labour Force Survey data pointed to a reading of +108k jobs in January–December’s gain was revised down to a gain of +131k from the original +184k reading (chart 23). The unemployment rate for the three-month rolling period ending January is expected to fall a tenth of a percent from 4.1% to 4.0% which sits just shy of the pre-pandemic unemployment rate. Despite total employment growth having slowed a touch in recent months (chart 24), the labour market is still showing signs of tightness with job vacancies notching record highs.

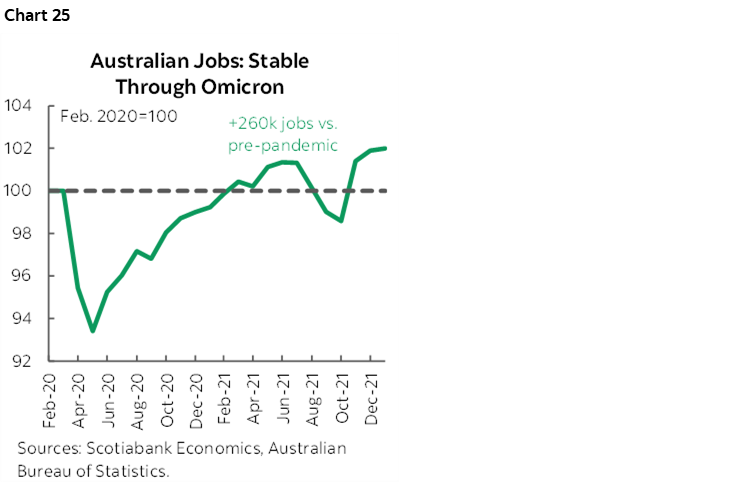

Australia’s labour market more than weathered the omicron storm with a net gain of +13k jobs in January (chart 25), while already overshooting heading into the wave. As expected, the hit came in the form of a temporary blow to hours worked, which should more than recover in the coming months. Continuing job gains are expected for February and we could see the unemployment rate continue its descent to 4.1%, well below pre-pandemic levels.

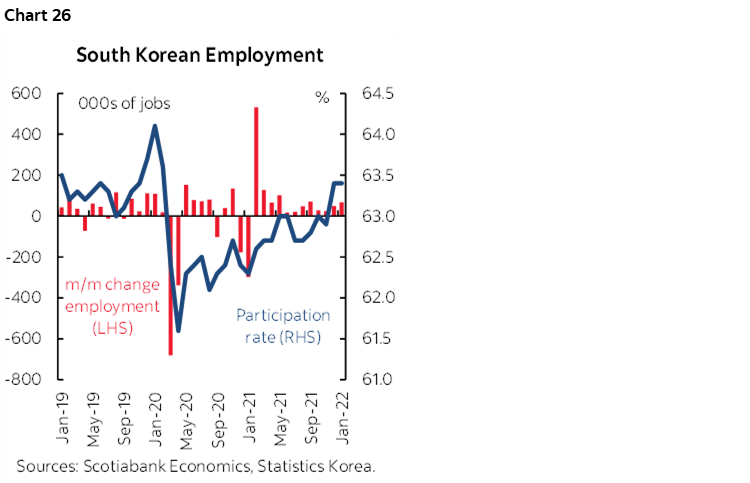

South Korea, unlike many of its Western counterparts, has not yet seen the peak of its omicron-driven wave, with much of the acceleration happening in the month of February. It’s not inconceivable to see job readings take a temporary hit followed by a strong rebound in following months. Labour participation is recovering well, and net positive job gains have occurred over the last 12-months (chart 26). The unemployment rate is expected to remain steady at 3.6%.

While the FOMC will dominate, other US macro reports will fill in tracking of household and industrial sector activities. Tuesday brings producer prices for February that will provide a first glimpse at how market pressures are impacting margins, as well as the Empire manufacturing survey that starts another round of monthly manufacturing reports. On Wednesday, retail sales face downside risk in the wake of the strong gains in January when sales advanced by 3.8% m/m. Housing starts should rebound in February’s report (Thursday) when we’ll also get expected growth in industrial production to go alongside the Philly Fed’s manufacturing gauge. Friday closes out with existing home sales that will probably face downside risk given softness in pending home sales.

Beyond CPI, Canada only updates housing starts for February (Tuesday), manufacturing conditions in January (Tuesday) and retail sales during January plus likely tentative guidance for February’s sales (Friday).

Other than Brazil’s central bank, data risk should be fairly light across LatAm markets. Chile’s Q4 GDP growth rate is expected to be ~13% y/y as the initial strong rebound in 2021 off of the weakness in 2020 gradually ebbs (Friday).

Across Asia-Pacific markets, China will release monthly gauges for February on Monday including retail sales, industrial production and the jobless rate. India’s inflation rate in February (Monday) is expected to hold steady at 6% y/y. New Zealand’s economy is expected to rebound in Q4 from the impact of prior restrictions and post solid growth of over 3% q/q SA non-annualized (Wednesday). Japan updates CPI for February on Thursday with small increases to what are still likely to be sub-1% y/y readings in headline and core measures.

Other European macro reports will include ZEW investor confidence as the first of the month’s fresh batch of sentiment gauges before PMIs and IFO business confidence measures. Swedish inflation (Monday) is expected to come under further upward pressure toward 4% y/y with underlying inflation excluding energy climbing to 3% y/y.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.