Next Week's Risk Dashboard

- Why SVB’s failure shouldn’t impede Fed tightening

- US CPI inflation to inform Fed’s next steps

- ECB: 50 times ‘X’

- US retail sales probably softened post-surge

- RBA watchers to have keen eye on jobs

- PBoC boxed in by the yuan and the Fed

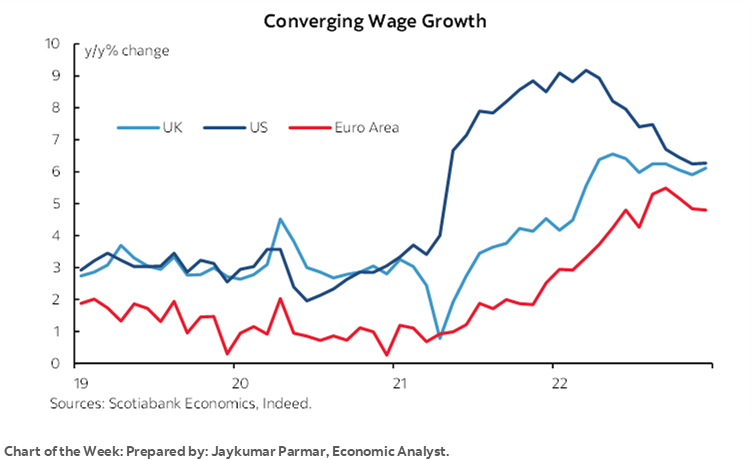

- UK jobs moving sideways

- More Canadian rebound evidence

- BI expected to extend pause

- Other global macro

Chart of the Week

The Federal Reserve’s policy decisions will face more than previously expected uncertainty with the coming week’s developments set to offer further critically important information. US inflation on Tuesday will be a part of this. The other key part will be further developments in the US financial system.

Is the failure of Silicon Valley Bank an idiosyncratic development? Is it a harbinger of strains in the financial system that could blow up into systemic risk? Or is this something that signals opportunity amid ongoing need for change that should be welcomed more than feared? I lean toward the first and third options.

SVB’s failure roiled financial markets but I’m not of the view that it is an existential threat to the financial system. SVB was a relatively small, undiversified bank with just over US$200B in assets in a US$24 trillion banking system. SVB was focused upon risky new tech ventures and it was caught flat footed by the Fed’s rapid rate increases. Regulators have moved swiftly to shutter SVB, make its insured depositors whole through the FDIC and issue receivership certificates to uninsured depositors to be paid out of the proceeds of a potential sale of what’s left of the bank. Its failure is being absorbed within the financial system and so far, there are few signs of contagion.

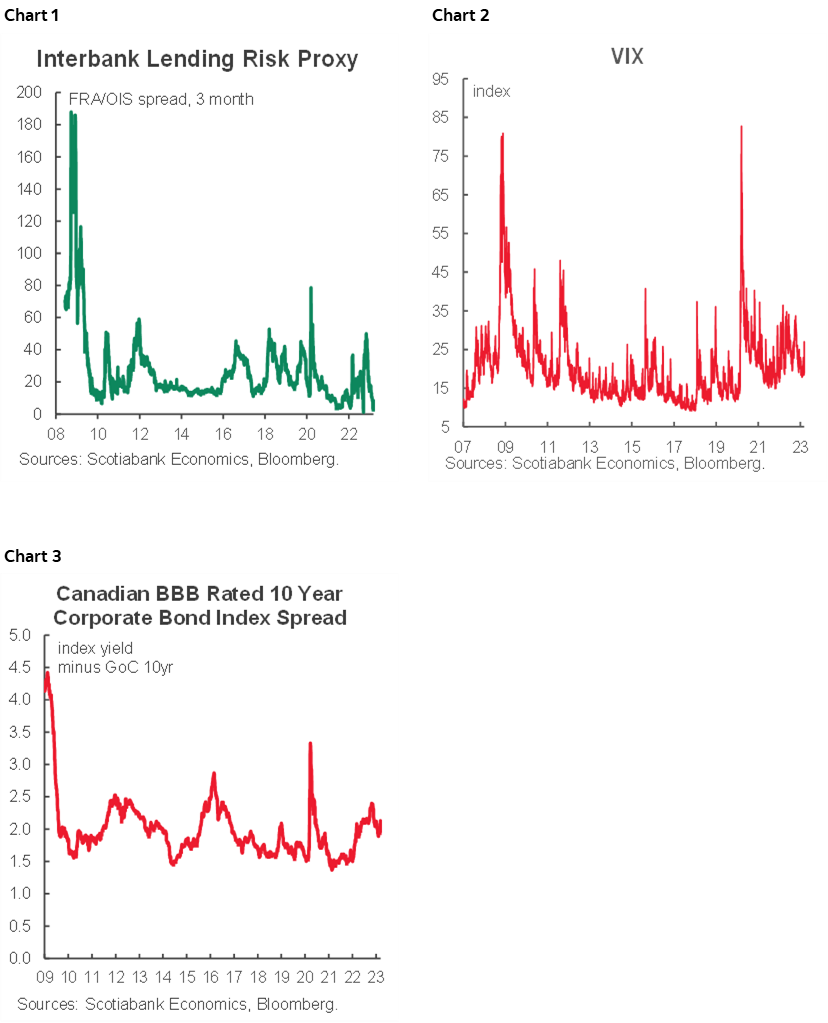

Measures like interbank funding spreads over relatively safe borrowing costs continue to be tight and are not signalling concern toward systemic risk (chart 1). The Vix index of stock market risk has increased but is a fraction of prior spikes (chart 2). Spillover into other markets is fairly modest to this point including, for example, spreads on corporate bonds north of the border (chart 3).

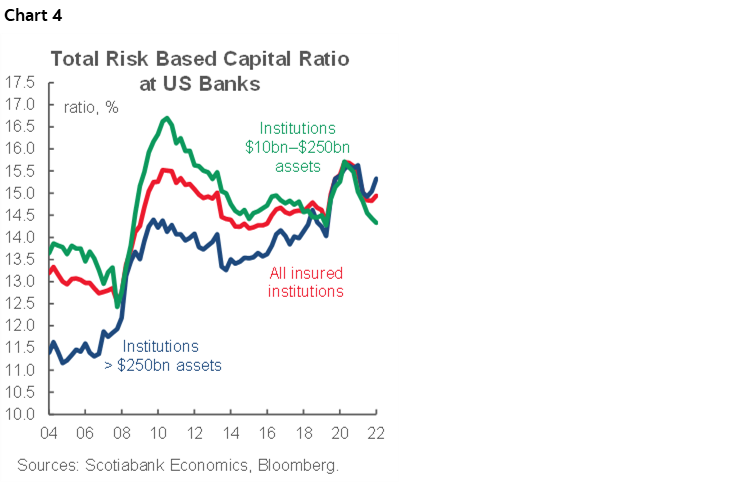

The rest of the US banking system is sound. It is well capitalized (chart 4). But SVB’s failure highlights the vulnerabilities within the peculiar nature of the US financial system that still has far too many small, localized lenders with unsophisticated funding and risk management practices. Students of money and banking and the history of the US financial system know this full well.

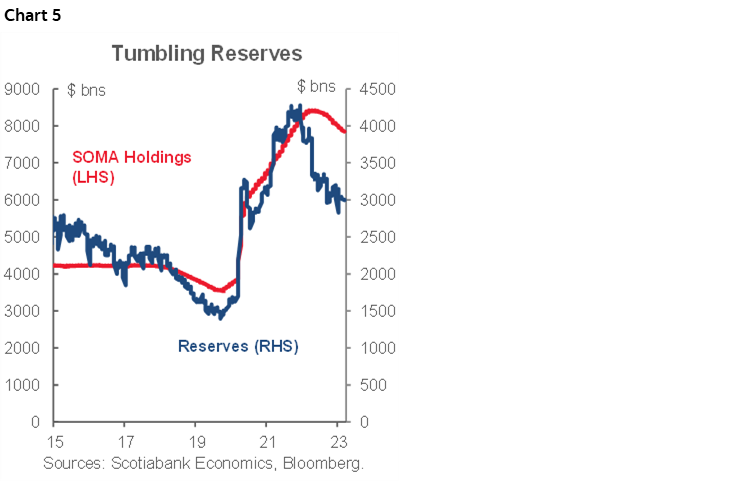

Frailties will be exposed within such a system as the Federal Reserve rolls back the security blanket, in this case through Quantitative Tightening. The Federal Reserve continues to sell down its SOMA portfolio holdings of Treasuries and MBS that were acquired during the quantitative easing phase that was designed to inject liquidity into the banking system and hold down longer-term borrowing costs to help stimulate the economy. That process papered over stresses in the US financial system. As the need for such policies waned, the Fed turned toward selling back its Treasuries and MBS into the market and by corollary this involves the withdrawal of cash as indicated by dwindling reserves held by banks at the Federal Reserve (chart 5). Financial institutions with less sophisticated funding operations benefited from QE but under QT are and will continue to be the most vulnerable to this development as they compete for deposits in more expensive wholesale funding markets.

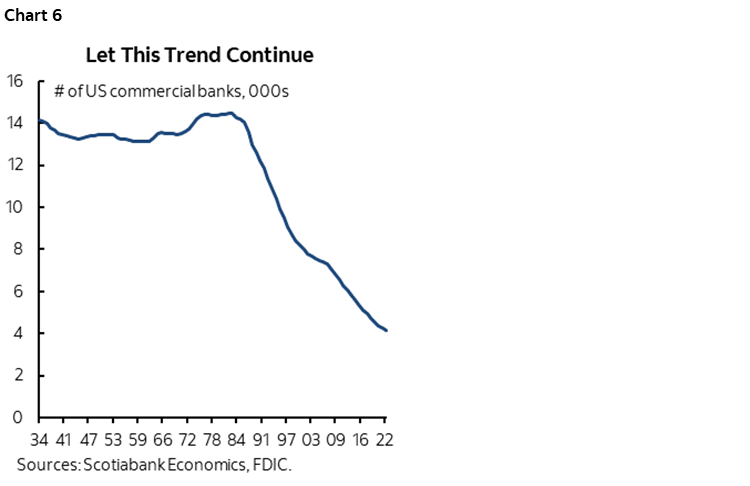

This probably won’t be the last such occurrence of challenges. Within reason, this process should not be feared. It should be welcomed and remains overdue. America continues to have far too many banks. Populist policies set in motion by the McFadden Act of 1927 created barriers to interstate banking and branching and thereby created diseconomies of scale and scope. America shot itself in the foot with this approach and set upon decades and decades of developments that sought to unwind its most pernicious effects upon the stability of the US banking system. The rise of monolines in the 1970s, state banking compacts, developments such as the Thrift Crisis and the Riegle-Neal Act of 1994 that swept away many interstate barriers set in motion a wave of consolidation as shown in chart 6.

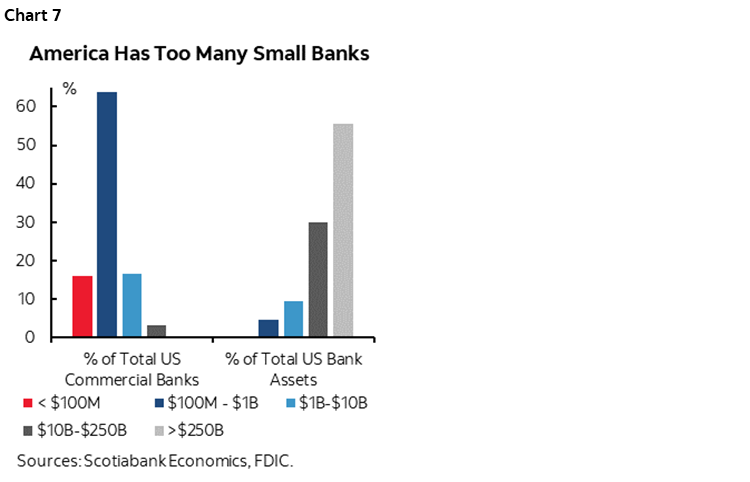

To this day, however, America still ended 2022 with 4,127 commercial banks of which 3,298 had assets of less than US$1 billion which is puny in the world of banking. 80% of banks are small, localized, undiversified and with underdeveloped risk management and Treasury operations and they are too often prone to failures that destabilize the system (chart 7). Think Mr. Mooney.

America should embrace the controlled rollback of the security blanket as the next logical step toward improving the safety, soundness and sophistication of its banks. Many of them—including 12 with assets over US$250B—are world class banks in a deep and sophisticated and highly innovative capital market. Too many are not and with that go opportunities for intramarket and cross border consolidation. The hunt for deposits makes folding some of these localized banks into larger operations relatively attractive and may give new foreign entrants a more attractive toe hold.

In short, rather than viewing this as the proverbial Wile E. Coyote falling-off-a-cliff moment as Larry Summers puts it, the Fed and US regulators should encourage the next step in the evolution of the banking system alongside continued tightening of US monetary policy to counter inflationary pressures. If there is one thing that can retard this evolutionary step in the development of the US banking system, then it would be political divisions. That would be a shame, as ideological opposition to bank consolidation in the United States wouldn’t serve depositors, customers, shareholders and employees of small failure-prone lenders well at all.

US INFLATION—THE MISSING PIECE OF THE FED’S PUZZLE

When Federal Reserve Chair addressed Congress this past week, he guided that decisions like the size of a potential hike on March 22nd (25bps or 50bps) and to what new peak the policy rate might climb were heavily data dependent. Another part of this data dependence arrives on Tuesday with US CPI.

First, recall that Powell said three things:

- "....the ultimate level of interest rates is likely to be higher than previously anticipated."

- "If the totality of the data were to indicate that faster tightening is warranted, we would be prepared to increase the pace of rate hikes."

- "we still have significant data to see before the meeting"

- "two or three releases will be very important to the decision they have not made at the March meeting"

Since his testimony, US payrolls came in strong, but wage growth slightly disappointed and the labour force expanded by enough to indicate that perhaps there is ongoing slack in the US job market that can keep wage-price pressures at bay (recap here). That remains uncertain in a tightening job market but the critical next step involves assessing fresh information on inflationary pressures. What happens to core CPI could carry the day in the Fed’s pending policy decisions.

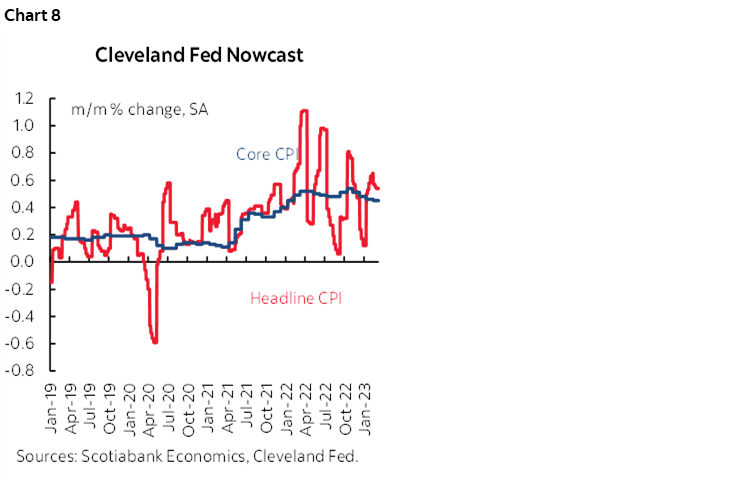

Enter CPI for February on Tuesday. Measures like the Cleveland Fed’s ‘nowcast’ indicate that core CPI may prove to be hot once more with a gain of 0.4–0.5% m/m SA following the 0.4% gain in January (chart 8). I have estimated a gain of 0.3% m/m. Relatively soft vehicle prices, little change in gasoline prices, ongoing pressure on owners’ equivalent rent and rent itself until 2023H2–24, and ongoing pressure on core service price inflation are among the drivers.

More important will be the Fed’s preferred PCE measure of inflation but the core gauge won’t arrive until March 31st and hence well after the March FOMC. Given that the January core PCE gauge surprised higher at 0.6% m/m—over 7% m/m at an annualized rate—versus core CPI at 0.4% this will matter a lot. Methodological differences are the reason since, for example, PCE places about half the weight on housing that CPI does and is therefore less vulnerable to downside pressure from house prices.

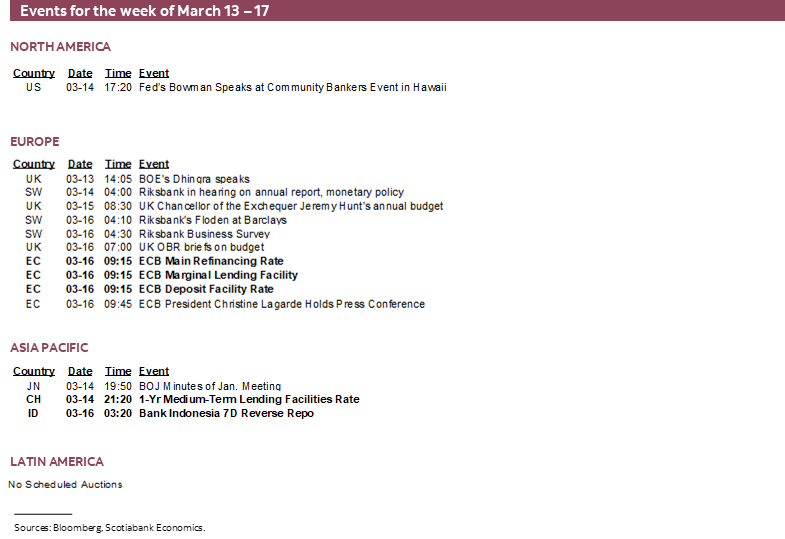

ECB HEADLINES CENTRAL BANK DECISIONS

Three central bank decisions will be forthcoming this week but only one of them is likely to be potentially impactful to global markets.

ECB—50 Times ‘X’

Economists and markets are virtually unanimous in expecting the European Central Bank to hike by 50bps on Thursday. All economists in Bloomberg’s survey are of this opinion and OIS pricing has all but about 5bps to go.

Why? Because they’ve told us their intentions. President Lagarde has said that “In view of the underlying inflation pressures we intend to raise interest rates by another 50 basis points at our next meeting in March.”

What comes afterward is more uncertain. Lagarde followed up such guidance by noting that “We will then evaluate the subsequent path of our monetary policy.”

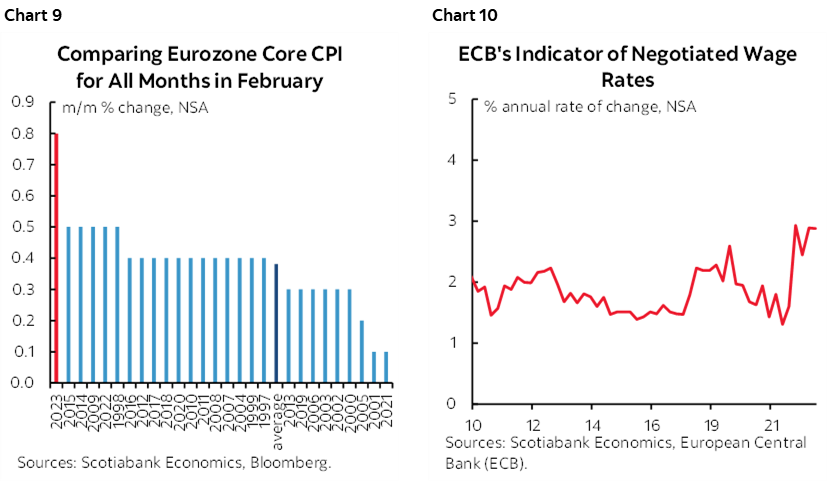

Opinions on this future path are divided across ECB officials. Markets are on the fence between pricing 25bps and 50bps for the May the 4th be with you meeting. Recent data such as the hottest core CPI reading for a month of February on record (chart 9) and accelerating wage gains (chart 10) may tilt the bias to sequential 50bps moves.

PBoC—The Yuan Straightjacket

The People’s Bank of China is widely expected to keep its 1-year Medium-Term Lending Facility Rate unchanged at 2.75% on Tuesday. Inflation provides a forgiving backdrop for easing monetary policy with core CPI recently falling back to just 0.6% y/y. The yuan does not, however, as it has depreciated over the past several weeks toward the 7-to-one ratio versus the USD as the Fed turned more hawkish. The yuan is likely to be more vulnerable to whatever the Fed does going forward than what the PBoC does.

Bank Indonesia—Inflation Versus the Currency

Thursday’s decisions is likely to deliver another policy rate hold at 5.75%. Core inflation recently eased back to 3.1% y/y from 3.3%. The rupiah has been depreciating since late January and so monitor the central bank’s guidance in terms of how it views risks to financial stability and inflation passthrough effects that may reveal a hawkish bias at this meeting.

KEY GLOBAL INDICATORS

The line-up of global indicators offers a number of gems that could inform the next decisions by the Fed, BoE and RBA as well as growth tracking in China, Canada and New Zealand.

Chair Powell did say ‘two or three’ when he indicated that critical pieces of new information would be considered on the path toward the decisions on March 22nd. The state of the job market is one set of new information. This coming week’s CPI is another. So what’s the third possibility? It could be found within the rest of the week’s line-up below and particularly in terms of two readings.

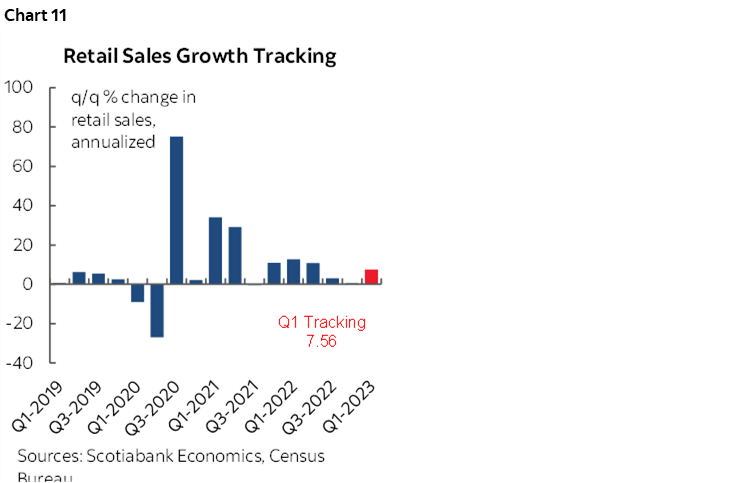

- Retail sales (Wednesday): February’s reading might give back some of the strong 3% m/m rise in retail sales during January and the 2.6% increase excluding vehicles and gasoline. Lower vehicle sales and little change in gasoline prices during February are expected to combine with a softening in core sales. The magnitude of the softening in core retail sales may partially influence FOMC thinking on the state of the US consumer (chart 11).

- UofM sentiment (Friday): This measure of consumer confidence has been cited by Chair Powell into past decisions and particularly in terms of what it reveals in terms of inflation expectations.

Other readings will include NFIB measures of small business hiring appetite during February (Tuesday) and weekly jobless claims after the minor increase in the latest week (Thursday). Industrial data including total production and manufacturing production (Friday) plus the Philly Fed (Thursday) and Empire (Wednesday) regional manufacturing gauges for March (Thursday) will inform momentum. Producer prices for February will inform their margins.

Canadian markets will trade in the aftermath of dual jobs reports in Canada and the US and will be primarily influenced by developments abroad and particularly through the US. The domestic calendar will be fairly light with a mixture of economic indicators on tap that could further inform the Q1 rebound narrative.

- Manufacturing (January): Statistics Canada has already guided that manufacturing shipments probably grew by nearly 4% m/m in January in nominal terms. Part of this is no doubt due to the rebound in the flow of oil into the US following the oil spill in Kansas during December. Part of it is also probably due to rebounding Canadian oil prices as the discount to WTI has been cut in half compared to where it was in early December.

- Wholesale trade (January): Statcan has already guided that wholesale sales were tracking a gain of 3% m/m in January. Revisions and details may be pertinent.

- Housing starts (February): Wednesday’s new home construction starts may weaken in lagging response to declining building permit volumes for new dwellings.

- Existing home sales (February): Wednesday’s figures will inform sales momentum, listing activity, months supply and nationwide prices.

UK job market conditions during January and the subset of payroll estimates for February are due out on Tuesday. Jobs have been largely moving sideways for much of the past year while wage growth has been catching more attention at the Bank of England.

RBA watchers will pay keen attention to February’s job market tallies on Wednesday evening (eastern time as always in this publication). After a drop of 12k jobs with full-time down 43k, consensus thinks a strong rebound could be in the cards.

China will update February readings to help with Q1 GDP growth tracking. They will include retail sales, industrial output and fixed investment all on Tuesday.

India’s inflation could back off the acceleration in January when February’s figures are released at the start of the week.

New Zealand’s economy is expected to contract a touch when Q4 GDP is released on Wednesday evening (ET). Mind you, this would follow a powerful non-annualized seasonally adjusted gain of 2% in Q3.

Latin American markets face light calendars over the coming week. Argentina will update high CPI inflation for February (Tuesday). Colombia will report industrial output, retail sales and trade over the back half of the week. Mexico updates industrial output during January (Monday) and Peru’s labour market conditions will be updated on Wednesday.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.