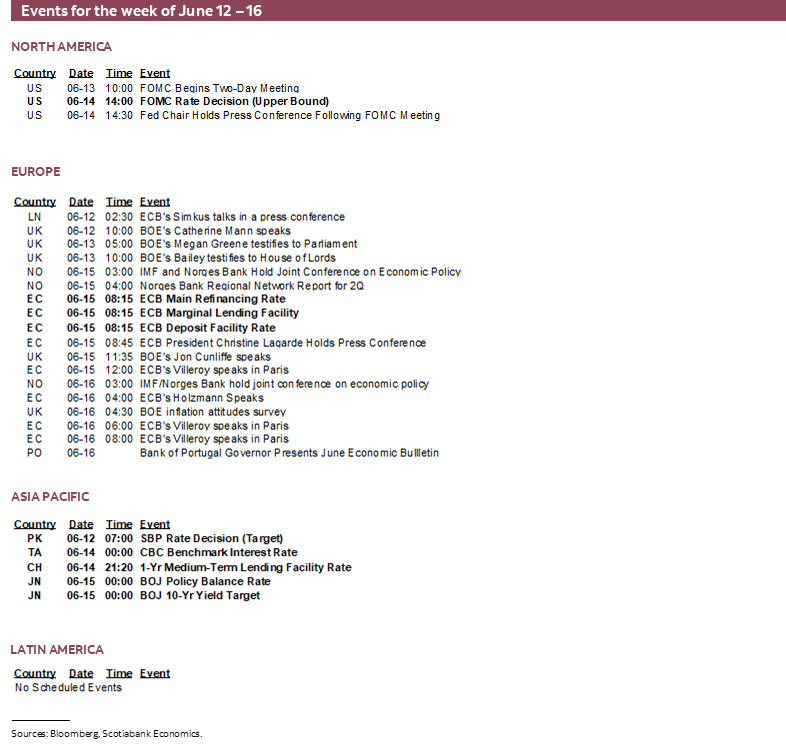

Next Week's Risk Dashboard

- Are more central bank shocks coming?

- FOMC: a data dependent coin flip

- Are markets underpricing the ECB’s terminal rate?

- BoJ under rising pressure

- PBoC stubbornly unchanged

- US CPI: is goods inflation being resurrected?

- Will AI be disinflationary?

- China readings to inform Q2 momentum

- Tracking the US consumer

- UK jobs and wages could impact BoE pricing

- An Australian jobs rebound?

- Other global macro

Chart of the Week

Several of the world’s most influential central banks will be delivering policy decisions this week in the wake of a wave of recently hawkish market surprises from the RBA, Bank of Canada and even RBI forward guidance. Each of the Federal Reserve, ECB, Bank of Japan and PBoC will weigh in alongside several top-shelf macroeconomic reports. Key is whether modest shocks give way to bigger ones.

US INFLATION—SETTING THE STAGE FOR THE FOMC

The fruits or perils of another swing at inflation forecasting arrive just before the FOMC’s two-day meeting commences on Tuesday morning. It’s not the Fed’s preferred gauge which is the price deflator for total consumer spending, or PCE and particularly core PCE, but CPI can provide a decent sense of what to expect for the preferred reading.

I’ve estimated a headline rise of 0.3% m/m SA and year-over-year rate of 4.3%, down from 4.9% the prior month. Core CPI is estimated to rise by 0.4% m/m SA with the year-over-year rate ebbing to 5.3% from 5.5%. If that proves to be accurate, then core inflation will still be riding at almost 5% at a m/m annualized rate and hence far above the FOMC’s 2% headline PCE goal.

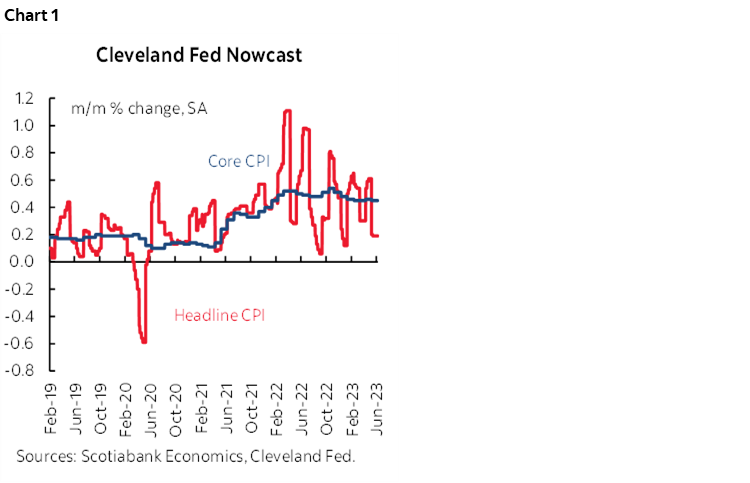

The Cleveland Federal Reserve’s ‘nowcast’ for core CPI is on the fence between a rise of 0.4–0.5% m/m SA with the headline nowcast at 0.2% (chart 1).

Headline CPI should be weaker than core CPI in no small part because gasoline prices across all grades were down by an estimated 5% m/m SA. At a weight of just over 3% in the CPI basket, that would shave 0.1–0.2% off of CPI. Food price inflation has also been easing over recent months and this is expected to continue.

Core CPI inflation is expected to be supported by several factors.

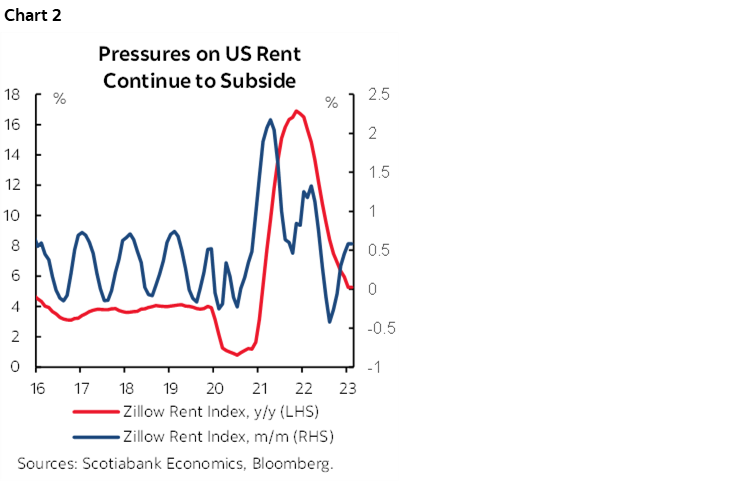

We’re not yet at the point at which owners’ equivalent rent is likely to turn sharply disinflationary and so continued persistence of gains around ½% m/m SA is expected. That repeat-sales house prices stabilized in February and increased by ½% m/m SA is something to carefully monitor if a trend renews persistent upward pressure on OER. Market gauges of rent inflation, such as Zillow’s rent index—continue to ebb in year-over-year terms and with the m/m seasonally unadjusted pattern back to exhibiting normal seasonality (chart 2). There are lagging effects of changes in market rent gauges and when they show up in CPI and they are not likely to emerge until toward year-end into 2024.

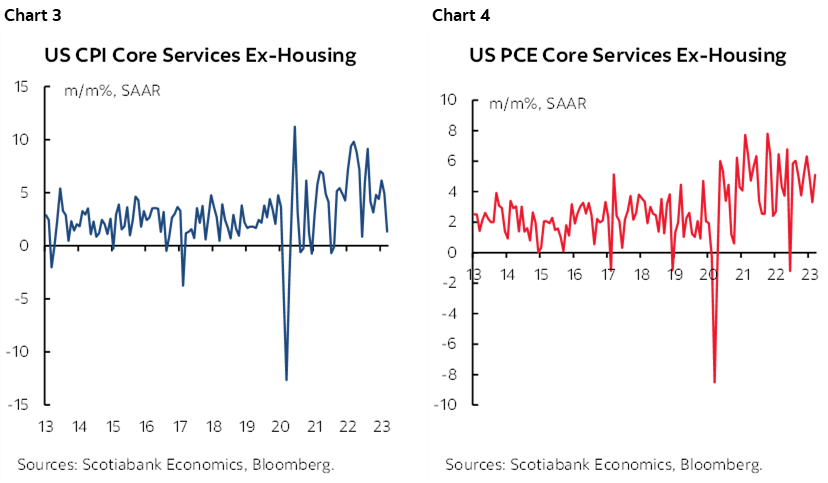

Core services ex-housing is a key gauge that Fed Chair Powell has drawn attention toward. Trend gains remain high with expected persistence, but the dip in such pressures during April sets up an interesting May as among the key details to watch (chart 3). Having said that, the April dip in core services ex-housing CPI did not translate into the equivalent PCE gauge which is preferred by the Fed (chart 4).

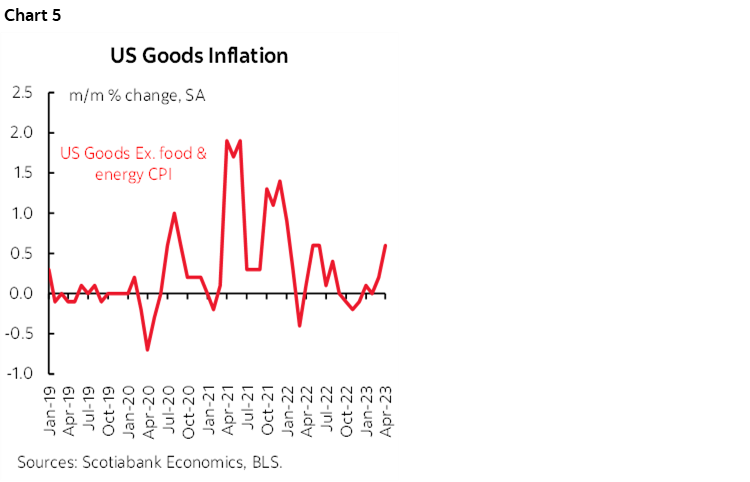

Used vehicle prices were up by over 4% m/m SA with new vehicle prices little changed at a small dip of under 1% m/m SA. Used vehicle prices were on the upswing the prior month as well which indicates that core goods price inflation may be returning (chart 5).

A lot may be riding on this estimate which is a segue into how the Fed may interpret the figures.

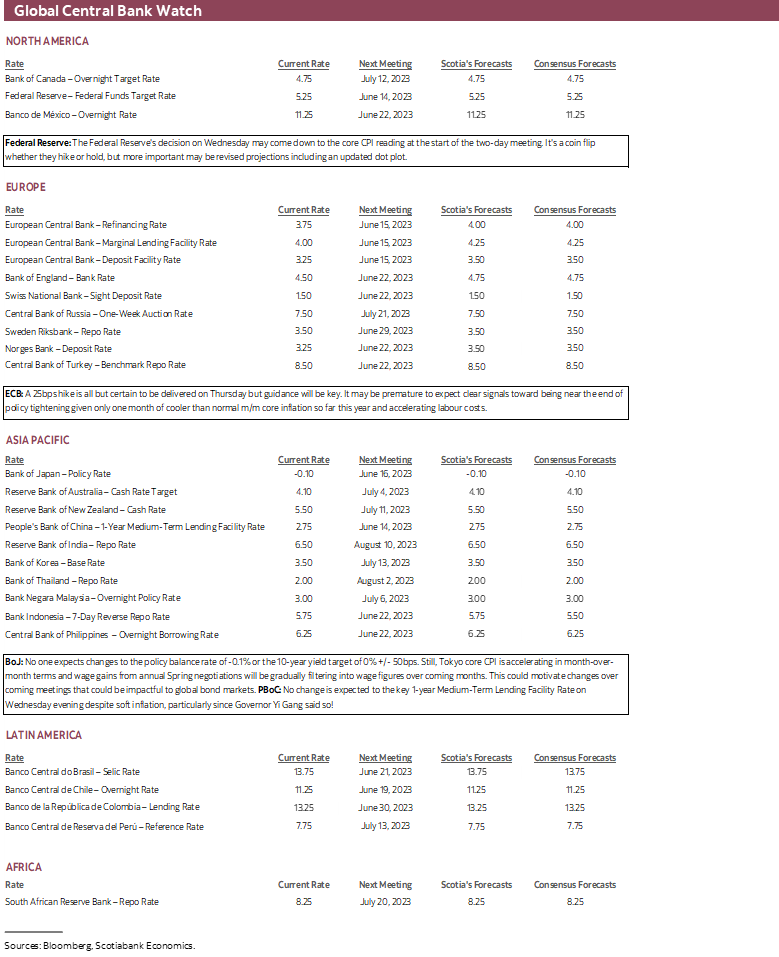

FEDERAL RESERVE—HOLD*

The FOMC will set the narrative not only for the immediate decision at hand but for some time yet to come as the by-product to the two-day meeting commencing on Tuesday. The statement lands at 2pmET on Wednesday along with the updated Summary of Economic Projections plus a fresh dot plot. Chair Powell will host the usual press conference thirty minutes later for around an hour.

Markets are priced for around a one-in-three chance of a 25bps hike this week and a terminal rate of 5¼% that signals market expectations that the Fed is done hiking rates. The vast majority within the consensus of over 100 forecasters of various ilk also expect a hold.

Our base case is a hold accompanied by dot plot guidance toward a higher terminal rate of 5½%, but with a notable asterisk beside this expectation. It’s not a high conviction belief; in fact, hike or hold is probably close to a coin toss.

Why? And how certain should we be toward a hold this week?

Interpreting Fed-speak

At risk of repeating myself, the core case for the Fed to be done hangs on interpretations of Fed-speak starting with Chair Powell’s May 19th remarks and culminating in pre-blackout comments by other officials. Some have taken the suite of those remarks—and particularly the Chair’s—as a clear sign they will pause in June. That may be applying too much literary licence to what they actually said.

Recall that on the 19th, Powell said the following:

“Having come this far, we can afford to look at the data and the evolving outlook to make careful assessments.”

He also noted that no decision had been made about the June meeting’s outcome and that they will take decisions one at a time depending upon the evolution of data and events like the debt ceiling agreement’s passage since those remarks were offered. What I heard the Fed chair say is quite literally that they will “look at the data” which to me sounds more like a shift away from providing explicit advance guidance that they will definitely hike toward taking it one meeting at a time.

Also bear in mind that when Chair Powell spoke, he was concerned about political developments around the debt ceiling and the risk of market dysfunction that has now been swept aside by the highly predictable passage of the agreement in both chambers of Congress.

Markets also took comments from Governor—soon to be Vice Chair—Jefferson as supportive of a June pause. Funny, but here too what I heard him say doesn’t match the market narrative. Jefferson said:

“A decision to hold our policy rate constant at a coming meeting should not be interpreted to mean that we have reached the peak rate for this cycle.”

Note the difference between signalling a potential pause “at a coming meeting” versus, say, “at the next meeting” or “soon” which would have been a June pause signal consistent with language they’ve tended to use to communicate a greater sense of urgency.

In fairness to the market interpretation of Fed-speak is the fact that the Fed has thus far done little to lean against expectations either directly before the communications blackout or through more clandestine ways during blackout. With one-in-three odds of a hike this week priced into fed funds futures, it could be that they simply don’t have the conviction to do so. Maybe they want to see CPI and will then ring up the WSJ and others in clandestine fashion like they did pretty much one year ago to the day in order to affect market pricing and mitigate the game day surprise to whatever action they choose to embrace. I doubt it.

Or maybe, just maybe, we’ve transitioned to a different stage with the FOMC no longer treating markets like a toddler and instead leaving markets to their own devices with a higher tolerance for data dependent surprises. That could be more useful in the fine-tuning stages of monetary policy. Keeping markets guessing may be smarter than having to tee up future moves at this point.

The Dots Complicate Things

Another issue with Fed-speak is that it gets a bit complicated with the dot plot. The March dots showed that the median FOMC participant expects 75bps of easing in 2024 and that the FOMC has already hit its terminal rate of 5.25%. Those dots were set when regional banks were failing before since calming down and when the debt ceiling was a forward-looking risk. Hence, the dots may be stale.

If the Fed holds this week and the median projection for the Fed funds rate reinforces that they’ve hit the terminal rate with about 75bps of cuts in 2024 then markets could well rally on the increased confidence that the next move is down relative to the marginal pricing for another hike. FOMC participants could view courting such a market response as premature. Markets would probably fade the longer-run dots and whatever they may show for policy rate moves into 2024. If the Fed hikes this week and signals it is done, then the effects may be similar. The only likely way to engineer a more hawkish market outcome would be to hike and leave the door open to signal further tightening followed by a muted easing path.

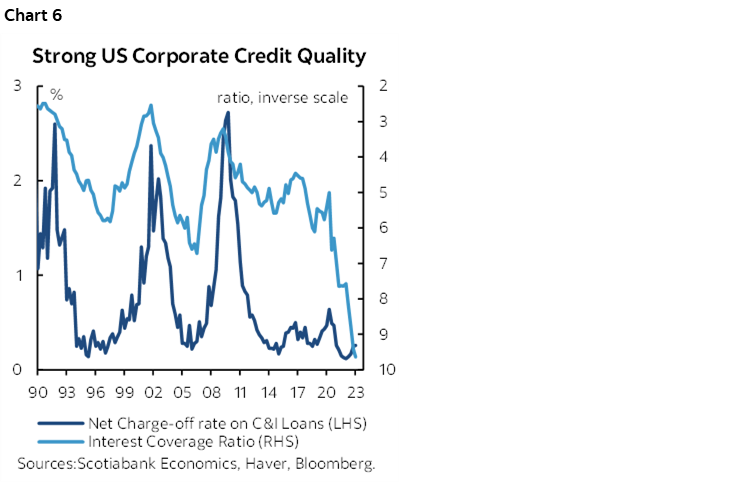

Credit Tightening—Most of the Concern is Years Away

The hold camp also acknowledges that credit tightening is a substitute for further rate hikes that may have been greater in an alternate parallel universe absent regional banks blowing up. That’s feasible, but perhaps exaggerated.

US corporate interest coverage is at a record high into 2023 and explains why charge-off rates on commercial and industrial loans remain very low. Lagging influences shown in chart 6 suggest this could persist. If so, then perhaps challenges at some lenders will be crowded-in by stronger lenders.

Or maybe such challenges will be crowded in by market substitutes for financing.

What hangs over concerns at lenders is the risk of materially tighter capital rules affecting US banks that may limit their ability to grow lending books. That would be unfortunate by way of making stronger institutions pay the price for regional bank frailties in a way that damages the US economy’s growth potential. Nevertheless, we’re probably looking at implementation that lies several years away when the FOMC has to craft monetary policy toward more pressing considerations.

Data Dependency

A lot may be riding on Tuesday morning’s CPI update that was previewed in the prior section. If core CPI is hot again then it may tip the balance toward a hike particularly in the wake of the strong payrolls report that has been plagued by serial underestimation of the gains by consensus estimates throughout 2022–23 (recap here). JOLTS job vacancies also unexpectedly increased which may signal ongoing hiring appetite.

Recall that FOMC participants submit their projections including the dots on Friday before the meeting but can amend them right up to the end of the first day of the FOMC meeting.

AI—NOT THE FED’S FOCUS, YET

One question I’m getting fairly frequently from clients is whether the Federal Reserve should be paying greater heed to the possibly disinflationary effects of Generative Artificial Intelligence. It pops up as a question in the deluge of client meetings that I’ve done so far this calendar year and at events and through more informal exchanges.

With the caution that my understanding of AI’s effects is no doubt at an extremely developing stage, at this point I’m inclined to think that while AI may have powerful effects over time, I’m skeptical toward the early connections being drawn to inflation and central banks in isolation of all else and for four main reasons.

A practical first point is that central banks’ policy horizons are usually defined in a 1–2 year sense. That’s when the bulk of the lagged effects of their actions show up and that’s the horizon over which they seek to achieve their inflation targets. My sense is that AI has very limited influences on overall growth and inflation in this nearer term. Central banks can’t be crafting monetary policy around what AI might do over 5, 10….etc years in the future.

I’ve read a bunch on AI’s effects on productivity and growth and hence with connections to inflation and to be honest I’ve found much of it to be dissatisfying. That’s not necessarily a criticism versus a frank recognition of the fact that we’re dealing with something that is a total out of sample experience with no real useful benchmarks to guide us.

There seems, however, to be a tonne of hand waving around the estimates. For instance, because it speeds up software development by cutting it in half—or even more—it must therefore double productivity, then attach weights on those sectors and aggregate upward. Pieces by the Brookings Institution in the latest Consensus Economics publication, and by consultants at McKinsey over recent years all seem to embrace similar tactics as they blue sky the implications over the very long term. McKinsey’s now aging estimate is often repeated and says AI could boost global GDP by $13T within seven years for an average annual compounded GDP lift of 1.2% each year. Maybe they’re right, but there is a lot of compounded casual handwaving activity behind the math.

We’ve seen this tendency before; being the tendency to draw profound macroeconomic conclusions based upon tech sector only to then watch as initial expectations get reined in or bubbles pop.

These studies that laud the potential lift to productivity, incomes and living standards by AI all suffer from the same flaw: they almost solely focus upon the supply side and potential productivity benefits without considering demand side implications. But what if aggregate demand curves shift outward as new innovations lead to entirely new markets? What will people do with the higher purported living standards? Will they buy bigger, nicer homes, more toys, more travel, more cap-ex requirements etc? What distributional effects may arise? A general equilibrium approach to AI’s effects can’t just shock the supply side and aggregate upward from there when trying to determine effects on inflation.

There are other structural drivers affecting inflation over time and I think they all point in the opposite direction to AI with uncertain net effects.

For instance, we’re probably still at an embryonic stage of addressing supply chain challenges after various forms of border frictions starting with the Brexit vote and the 2016 US election that combined to introduce more restrictive trade policies, then the pandemic and the Ukraine War and hopefully not greater China-Taiwan frictions. C-suites that outsourced with a sole focus upon lowering operating expenses without having to worry about border frictions and their effects on financial distress costs, like foregone sales or outright bankruptcy, are now having to rebalance that trade-off. This process could invoke supply chain changes that raise operating costs and then pass them on depending upon incidence effects and company pricing power.

It could also be that demographics will be less favourable across much of the developed world by impacting tighter job markets and greater medical service/goods inflation. The US and much of Europe have basically no population growth and so they’d better get the hypothesized offset of AI on productivity.

Carbon pricing and environmental policies likely mean more elevated price pressures. Government spending is soaking up more global excess savings than it was before the pandemic and it’s hard to see this reversing.

ECB—STAYING THE COURSE

The mystery and intrigue surrounding what the Fed may do on Wednesday is not paralleled by expectations into the next day’s ECB communications.

Markets are priced for a 25bps hike from the European Central Bank on Thursday (8:15amET). They are teed up for most of another 25bps hike at the following meeting on July 27th and for a terminal rate that is about cumulatively 50bps higher from here. The consensus of economists is unanimous toward a 25bps hike this week. President Lagarde’s comment at the start of this month on the further “ground to cover” in raising rates pretty much makes a 25bps hike this week a slam dunk.

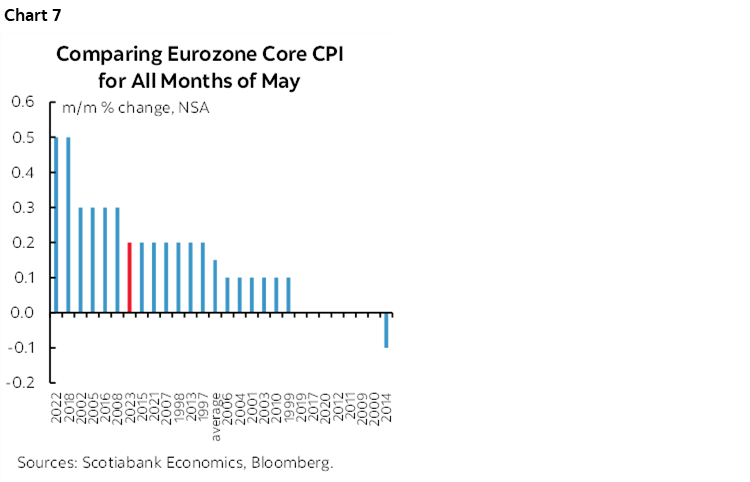

Key will be guidance about what may be done after this meeting. One argument for signalling that the end to the hiking cycle may be near is that core inflation ebbed for once in May by posting a month-over-month seasonally unadjusted gain that was in line with the average for months of May (chart 7). That may be a premature conclusion to reach. This ebbing was the first time this year that this gauge was below the norm for past like months in history. This is a better way of looking at inflationary pressures at the margin instead of looking at year-over-year inflation.

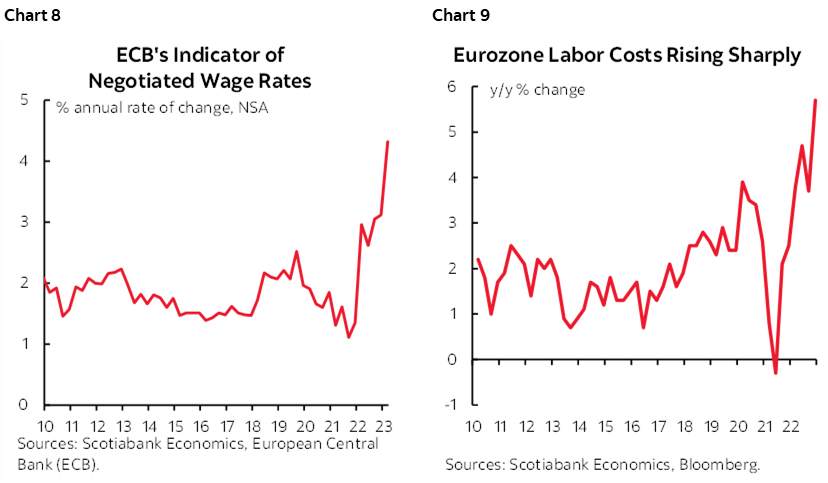

Furthermore, labour cost pressures on inflation continue to intensify across the Eurozone (charts 8, 9). If anything tips the balance toward greater hawkishness than markets expect then this could well be it.

BANK OF JAPAN—LETTING DOWN THEIR GUARD TOO EARLY?

No policy changes are expected when the Bank of Japan delivers its decisions on Friday. The policy balance rate is expected to stay at -0.1% and the 10-year yield target of 0% with +/-50bps bands is very likely to remain intact.

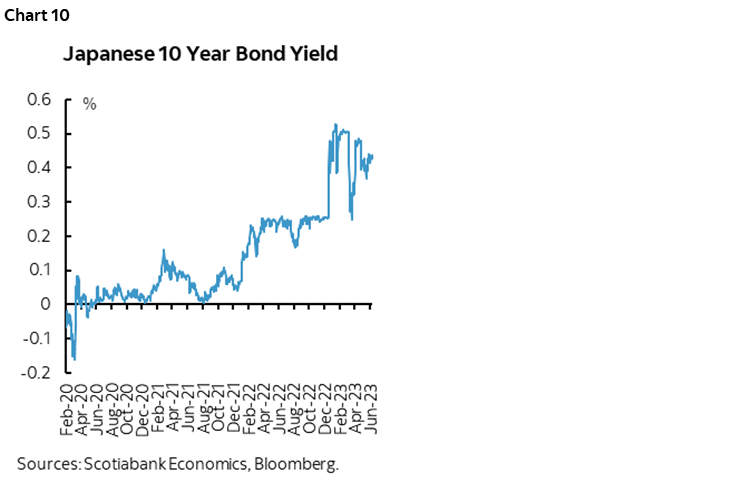

In fact, markets are backed off challenging the upper threshold of the yield target (chart 10). Back in February, the yield on 10-year JGBs was testing the upper bound of +50bps amid speculation toward a BoJ pivot, but then a combination of turmoil in global banking markets and Japanese data lessened the pressures. At week’s close, the 10-year yield is about 41bps.

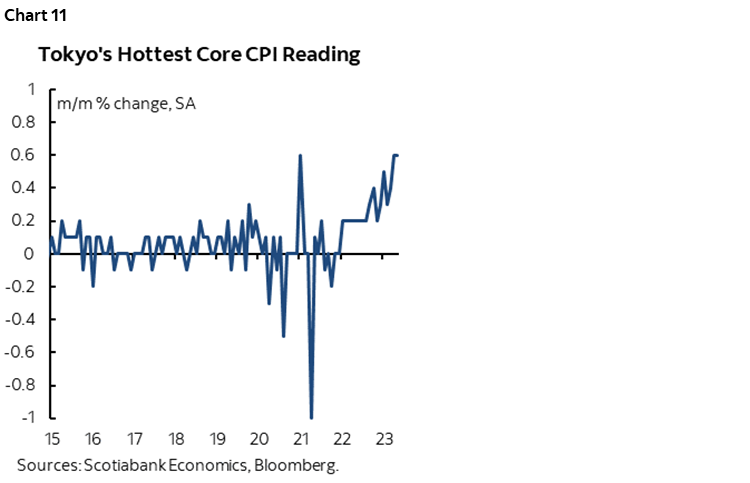

Are markets letting down their guard too early? Perhaps. Inflation is tracking above BoJ expectations. Tokyo core CPI (ex-fresh food and energy) accelerated to 0.6% m/m SA in April for the hottest reading since January 2021 (chart 11).

Inflation-adjusted labour earnings have continued to decelerate with the April reading down 3% y/y, but the effects of the annual Spring wage negotiations registered the biggest pay gains in 30 years at about 3.7% y/y. It can take several months for these gains to filter through official lagging data and so we might not have an accurate handle on nominal and real wage changes for a while yet.

Governor Ueda is unlikely to rock the boat this week. Markets should be prepared for the possibility, however, and perhaps as soon as this summer. With inflation surpassing expectations and the missing ingredient of wage gains joining the picture, a policy pivot could be in the cards.

That could be an effect on global markets that swamps anything the Fed may do in the near term. Japanese bonds could become higher yielding alongside yen appreciation, and this could reduce demand for US Treasuries and other global bond benchmarks. Covered interest parity is still relevant across markets after adjusting for the post-GFC basis with one theory being that the higher error term on the relationship between spot and forward exchange rates versus short-term interest rate differentials could be a function of changed regulations affecting banks that limited their roles as sources of arbitrage activity in aligning global currency and bond markets. A widened band in the covered interest parity relationship could well still make it a powerful framework for understanding the ripple effects of anything the BoJ does.

PBOC—DOWNPLAYED SENTIMENT

A minority within consensus thinks the People’s Bank of China may respond to weakening momentum by cutting its key 1-year Medium-Term Lending Facility Rate by 10bps on Thursday evening (ET). Most expect no change.

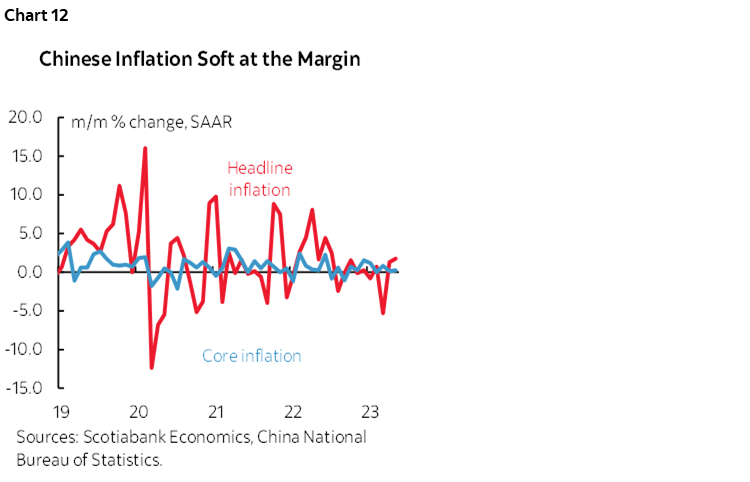

Recent comments from Governor Yi Gang lean in the direction of the no change camp, despite very soft core CPI inflation (chart 12).

GLOBAL MACRO—FOUR KEY SETS OF READINGS

Four key rounds of macro data could also be impactful to the market tone.

Tracking the US Consumer

US retail sales for the month of May arrive on Thursday and will further inform the state of US consumer spending and GDP growth in Q2. I’ve estimated a drop of -0.5% m/m in headline sales in value terms and a small rise in sales ex-autos. One driver is that we know new vehicle sales fell by 5.4% m/m SA and this alone could shave around ¾% off month-over-month retail sales. We also know that gasoline prices fell by about 5% m/m SA which would shave another few tenths off retail sales. The strong gain in sales ex-autos and gasoline during the prior month of April (+0.6% m/m) could be tough to repeat but will make or break the overall tone of the report compared to the known considerations. Tuesday’s CPI for the same month of May could carry important implications for the retail sales estimate given that it is provided in nominal terms.

China’s Slowing Economy

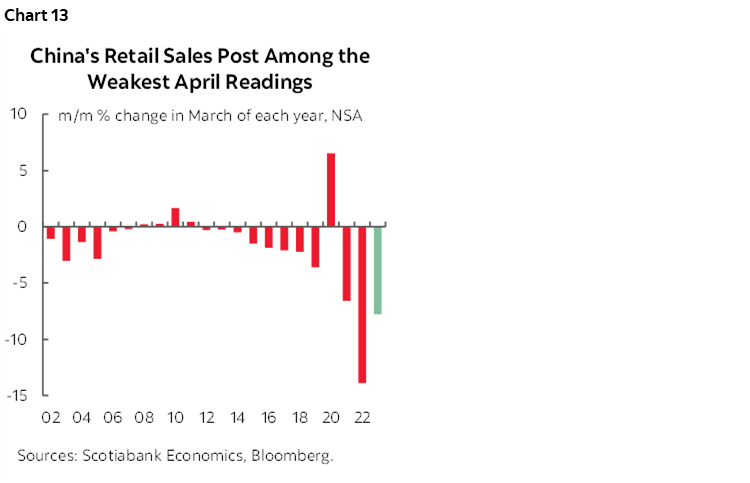

China updates another round of monthly readings that will help us gain a better understanding of Q2 economic growth and hence momentum in China’s economy. Industrial production, retail sales and fixed investment are all expected to register softening year-over-year gains (Wednesday night ET) but m/m momentum will matter more after the prior month registered among the weakest months of March for retail sales on record (chart 13). Credit and money supply readings for May should also arrive this week.

A minority within consensus thinks the People’s Bank of China may respond to weakening momentum by cutting its key 1-year Medium-Term Lending Facility Rate by 10bps on Thursday evening (ET).

UK Macro Data Could Impact BoE Pricing

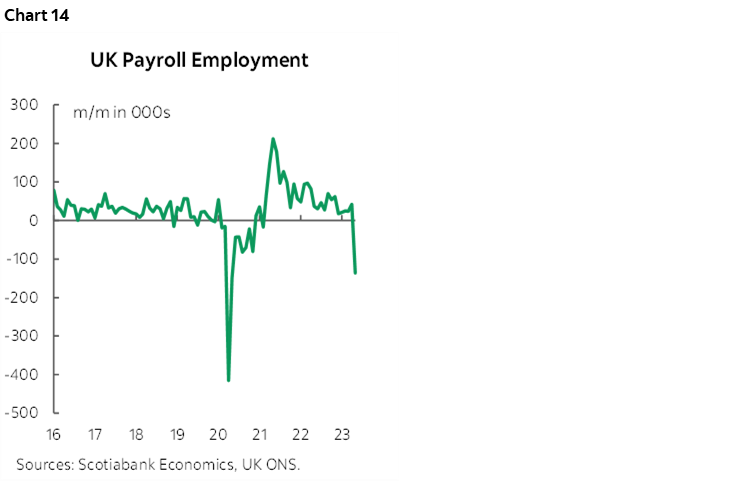

Amid some debate over whether the Bank of England may hike by 25bps or 50bps on June 22nd, this week’s round of macro reports could be decisive influences. High UK job vacancies could drive a rebound in payroll employees on Tuesday after they fell by 136k in April at the peak of global banking developments (chart 14). Lagging total employment had risen by 45k in March. Industrial output is expected to be soft (Wednesday) along with construction output and a small rebound in services output. April GDP is expected to get a small lift that same day.

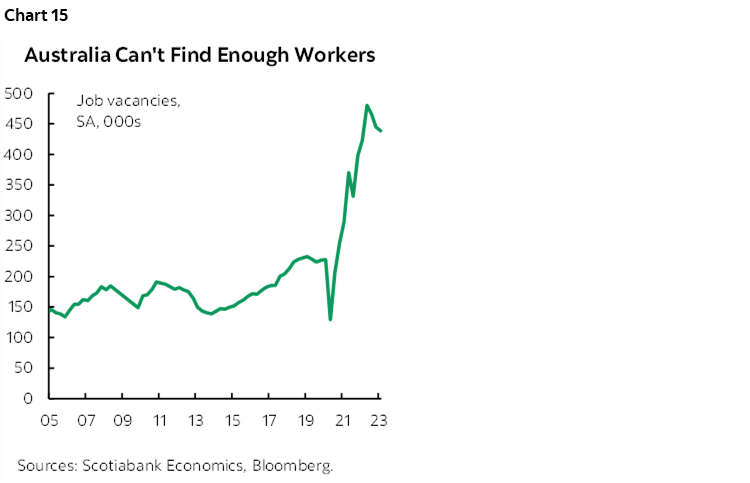

Australian Hiring Rebound?

Australia delivers another jobs report for the month of May on Wednesday. Recall that jobs were little changed in April (-4k) because full-time jobs fell by 27k but this was mostly offset by a gain in part-time jobs. Almost all within consensus expect a rebound of varying amounts. Part of the view here is that job vacancies remain highly elevated and therefore monthly blips in hiring activity are compatible with a general hiring trend (chart 15).

Canadian markets are likely to shift toward being primarily influenced by external developments after this past week’s focus upon the BoC (recap here) and job market conditions (recap here). Relatively minor data will include housing starts during May that will probably ease (Thursday), manufacturing sales that Statcan’s early guidance indicates slipped a touch in April (Thursday), existing home sales during May that probably registered another powerful gain but that almost never impact markets (Thursday) and then wholesale trade that advance guidance indicates posted a strong gain (Friday).

Other US releases will focus on producer prices that are expected to dip due to lower energy prices with core prices more resilient (Wednesday). Initial jobless claims take on more importance after the most recent week’s modest increase (Thursday). Another round of regional manufacturing surveys on the path to the next ISM-manufacturing report will kick off with the Empire and Philly Fed measures on Thursday along with little change expected for industrial production that same day. The week ends with the University of Michigan’s consumer sentiment measure and its 1- and 5–10 year ahead measures of inflation expectations that can impact markets.

Asia-Pacific markets face a light line-up of calendar-based developments not named the BoJ. India updates CPI for May (Monday) and it is expected to decelerate toward 4.4% y/y from 4.7%. New Zealand’s Q1 GDP (Wednesday evening ET) is expected to post another mild drop that would make it the third decline in the past five quarters.

The ECB will dominate attention and a very light calendar will amplify the focus on its deliberations. Swedish CPI inflation for May is expected to register no change in headline or underlying prices in month-over-month terms.

Latin American calendars will also be very light. Argentina’s inflation rate of 109% y/y gets a May update.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.