Next Week's Risk Dashboard

- Canadian businesses are doing themselves no favours

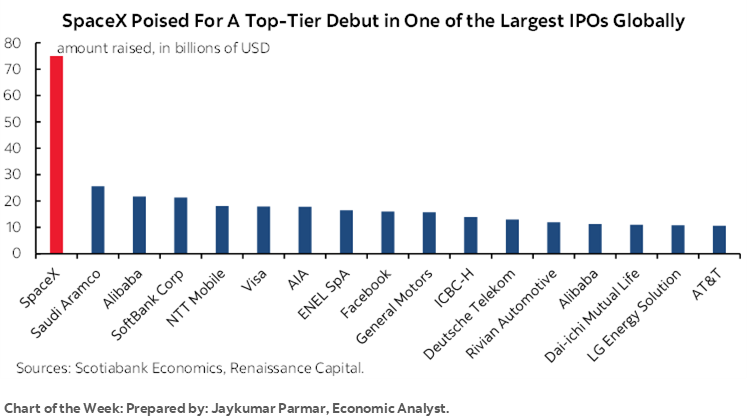

- SpaceX’s record IPO to be the first of three whales

- Nonfarm and US CPI could further test southeast Asian stability

- BoC to look through everything, for now

- ECB to hike, forecasts to inform path

- US inflation — pick your favourite measure

- BCRP to hold…

- …in wake of pending Presidential election results

- Turkey’s central bank to hold

- Global macro

Chart of the Week

The coming week is likely to feed an ongoing tightening narrative among central banks with probable stability concerns.

Asian markets will play catch up to the solid US nonfarm payrolls report (with caveats, here). Currency weakness across Southeast Asian nations and associated stability concerns are likely to intensify in nonfarm’s wake and perhaps more so after Wednesday’s US CPI, questioning how long their governments and central banks may stand pat.

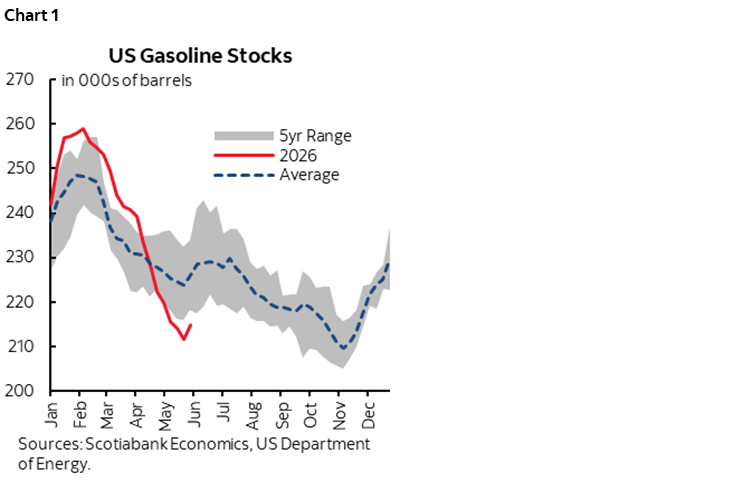

Then the ECB is slated to be the second of the A-league central banks to hike, with the BoJ likely to deliver its latest hike the following week. The ripple effects of the war with Iran and its impact upon commodities and broad supply chains are spilling across the globe. The summertime energy crunch still lies ahead (chart 1).

Stability may also be tested by uncertainty toward how market breadth may be tested by SpaceX’s mammoth record-breaking IPO on Friday (see front chart of the week from Jay) that wedges open the door for Open AI and Anthropic (US$1 trillion?) to follow. Three whales being squeezed into a swimming pool.

Left shrugging their shoulders for now will be the Bank of Canada this week as it stays on hold and in monitoring mode, looking through this, that, and the other thing. A pressure cooker of developments is likely to build over 2026H2 that could pivot the BoC toward our long-held hike call.

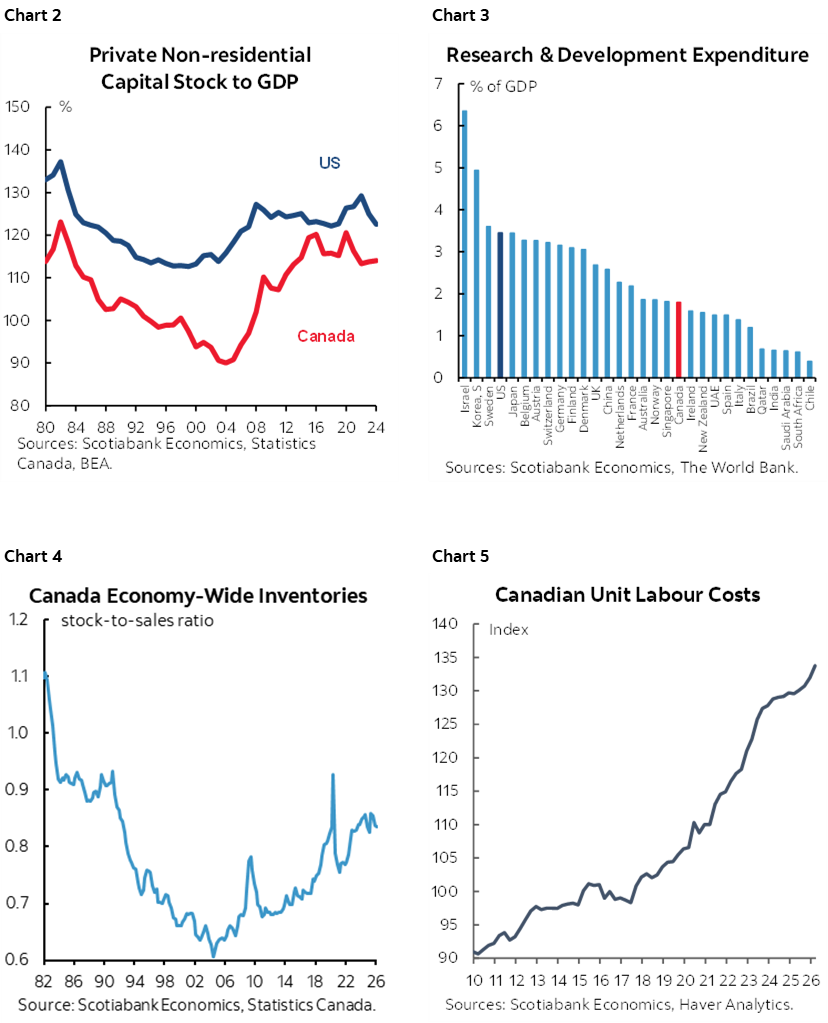

And yet throughout it all I can’t help but question what Canadian businesses are doing about all of this. They didn’t need Trump to cause problems for their outlook and shouldn’t look to government for all the solutions notwithstanding that being a very Canadian thing to do. With important exceptions, they generally underinvest (chart 2), spend very little on R&D (chart 3), are allowing their inventories to balloon perhaps in excess of prudent padding amid supply chain turmoil (chart 4), drive poor productivity growth relative to driving wage costs higher and have allowed productivity-adjusted employment costs to soar by about 35% over the past ten years (chart 5) and are generally—again, with exceptions—on the outside looking in on the AI surge in the US and China.

In short, failure to invest, mitigate costs like ULCs and inventories and generate faster productivity gains to mitigate employment costs is as sure a way of asking for it on higher inflation and rates as you could imagine.

As you’ll see in the BoC section, I’m not a fan of trade negotiations as an excuse not to invest in a country ranked #2 for its appeal on Foreign Direct Investment behind the US and in any event the problems have been longstanding.

On a lighter note before tackling the week’s expectations, the FIFA World Cup starts up on Thursday. It has the potential to temporarily distort multiple readings on activity and inflation with eleven US host cities, 3 in Mexico and 2 in Canada.

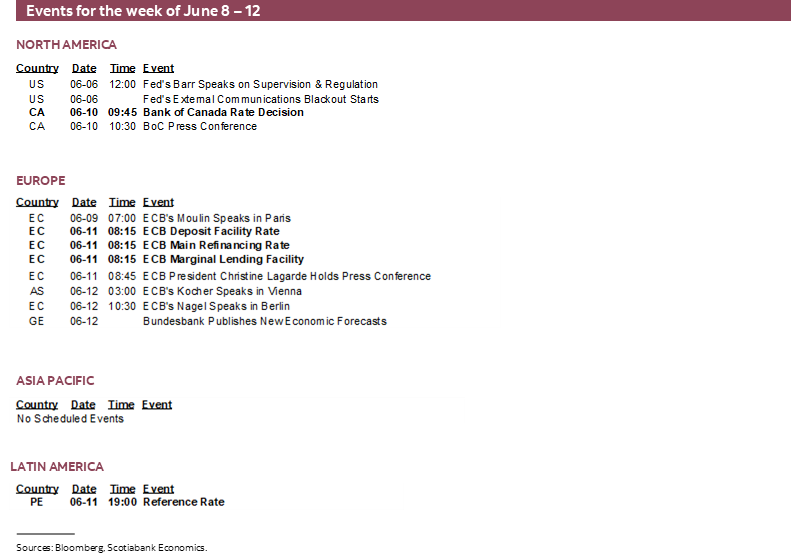

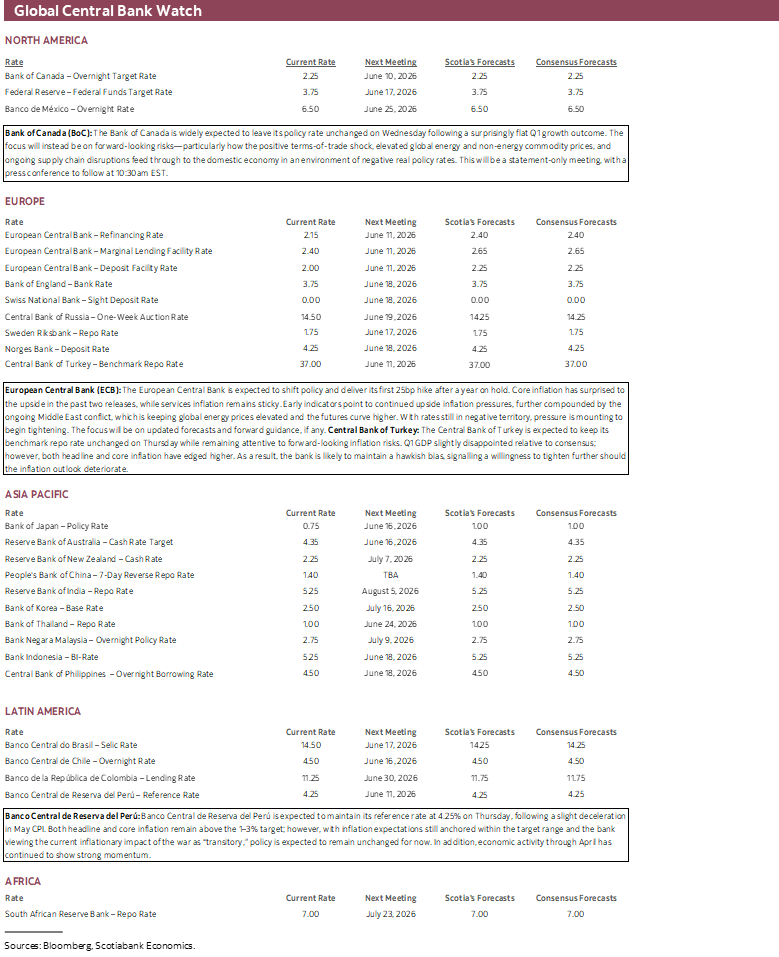

BANK OF CANADA—LOOKING THROUGH EVERYTHING

GDP? Didn’t see that. Job surge? Ignore that too, just one report. Surging commodities? Nope, not that either. Trade negotiations? Where and with whom did you say?? What’s your present outlook? Ask us next month. Have you incorporated the Fed’s extra spending in the Spring statement? Not yet. What does uncertainty over the Federal Reserve’s outlook and CAD do to the BoC especially if the policy rate spread gets even wider? We don’t care, we’re special, we’re independent ya know.

That about sums up expectations for the noncommittal tone from the BoC this week.

The Bank of Canada’s communications on Wednesday are not expected to deliver policy changes and are likely to be largely a placeholder designed to buy time. The statement and Governor Macklem’s opening remarks to his press conference will be released at 9:45amET and the press conference starts at about 10:30amET for around 45 minutes. There will be no forecasts this time as the BoC is between the April and July rounds.

Key will be the statement’s concluding paragraph that is likely to repeat references to how “we stand ready to respond as needed” while “looking through the war’s immediate impact on inflation but will not let higher energy prices become persistent inflation.”

The Bank of Canada is also looking through Q1 GDP. SDG Rogers said on Monday following last Friday’s GDP figures that the Bank doesn’t believe the tiny back-to-back contraction in GDP qualifies as a recession (I agree, see here), looks at a broader array of readings, and is encouraged by signs of a rebound into Q2 including solid April GDP.

The BoC also couldn’t have asked for more timely evidence of a rebound than the latest jobs report that blew way past even my estimate toward the top end of consensus (recap here). The momentum in the job market could suggest that April’s GDP jump will build upon itself in the rest of Q2.

So, there you have it. Just look through everything that’s going on. Wait for more evidence. In fairness, I don’t blame them in doing so, for now. The softer than expected recent numbers and slightly more economic slack than expected give them a bit more wiggle room to assess the outlook for inflation in the context of fresh supply shocks and the usually beneficial impacts of higher commodities to the Canadian economy.

Key will be patience. Our forecast is for 50bps of hikes in 2026Q4 and another in early 2027 ending at a nominal policy rate of 3%. We’re the only shop in Canada that called the market move toward pricing hikes in 2026 forecasts dating back to last November.

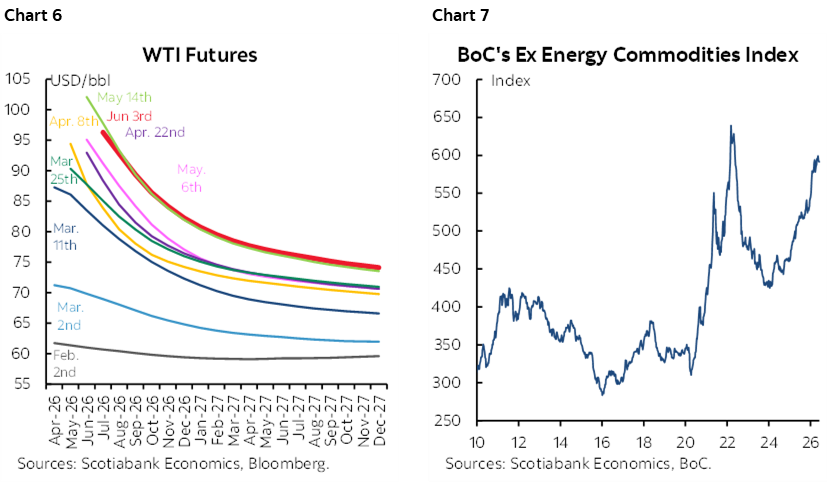

Some of that patience may be eroded at the next decision on July 15th when new forecasts have to be printed. At that point the BoC will need to incorporate higher for longer commodity prices (charts 6, 7) plus the Federal Government’s expansionary Spring statement that was issued in stealth fashion the day before the BoC’s April decision and forecasts. A restrictive-for-longer Fed may also open up some room for the BoC to reassess its stance.

As for trade negotiations, the BoC should stay out of it. Monitor, don’t react to every headline as there will plenty yet to come and many of them may not be pretty. At least not for a while until we have much greater clarity.

Despite flashy headlines, it should surprise no one who pays close attention to the negotiations that the July 1st CUSMA/USMCA deadline will pass with no revised agreement. It means nothing.

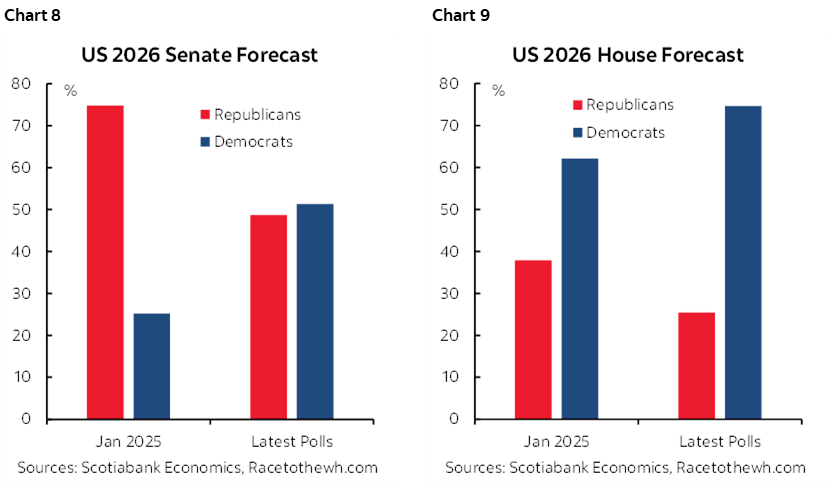

The date that matters is January 3rd 2027 when the new Congress convenes (or later if they delay the date since that's a Sunday, as they’ve done previously). The Dems are possibly going to take both Chambers (charts 8–9). Almost certainly the House. Possibly the Senate. Not getting a trade deal through both chambers in Congress before the new Congress convenes makes the US side of negotiations more complex. The Dems are no friends of Canada’s; recall Biden shot down Keystone XL and maintained Trump 1.0 tariffs while the current crop of Dems is likely to be more agitating on labour and environmental issues.

No one realistically expected the agreement to be rolled over on July 1st. Mexico's issues are much more complex, hence why US negotiations started with them first (borders, back door for China, labour concerns etc). Now things start to get interesting with plenty of runway ahead and no doubt plenty of volatile headlines.

Some of the comments made in public by folks on the Canadian side who were briefed by the negotiators when they returned the other day indicated commitment by the US to get a deal done and keep USMCA/CUSMA. That was the overwhelming feedback given in USTR hearings on the USMCA agreement last Fall. And time and politics are on the side of the Canadians and Mexicans imo. Trump desperately needs something to go right as his war flounders and popularity plummets. Waving a new trade deal and spinning it howsoever would be part of that. By contrast, the Carney administration has a lock on a majority government for years to come.

So my point is to think back to NAFTA 2.0 during Trump 1.0 for the lessons to be drawn here. Keep calm. Trade on. Be mindful toward the risks. Be wary toward the hysteria. And ultimately, there is still a who-cares case.

Most Canadian exports to the US (85–90%, likely 90% as recent dips are technical) are tariff free because of the USMCA/CUSMA compliance carve-out. CAD at >1.39 USDCAD buys a lot of price competitiveness compared to 1.20 a few years ago. Ok US growth (slowing of late) is a pull effect on imports. Most of the details in the negotiations sound like micro issues, not the stuff of broad trade shocks.

All of which is why I've said all along that in my belief, trade risks to Canada are like the mortgage resets issue that some said would derail everything as a macro shock versus my narrative of it being a micro shock. Single-factor narratives of doom and gloom usually don't work out so well even if they're highly marketable. The BoC shouldn’t be in the business of pandering to such narratives that trace themselves to marketing campaigns on the street.

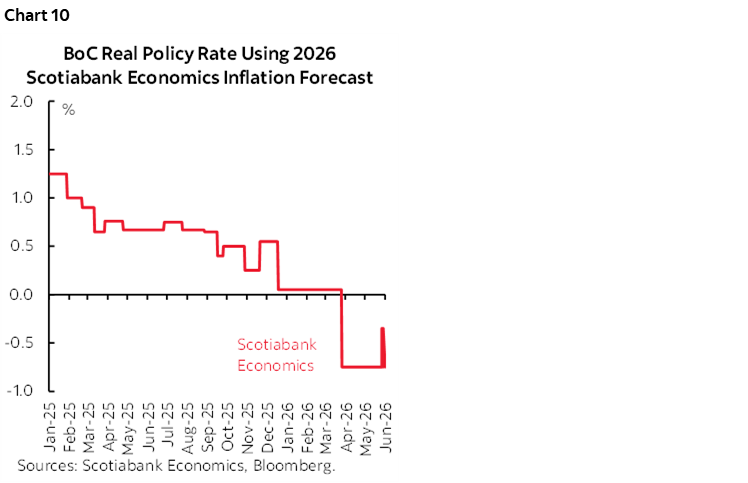

Instead, the question for Governor Macklem is this: Why are you easing into a positive commodity shock with fiscal policy substituting for monetary policy and without evidence of downside risks from trade negotiations? Chart 10 shows that’s what is happening, even if passively. I guess we’re supposed to look through that as well.

US INFLATION—WHAT’S YOUR PREFERENCE?

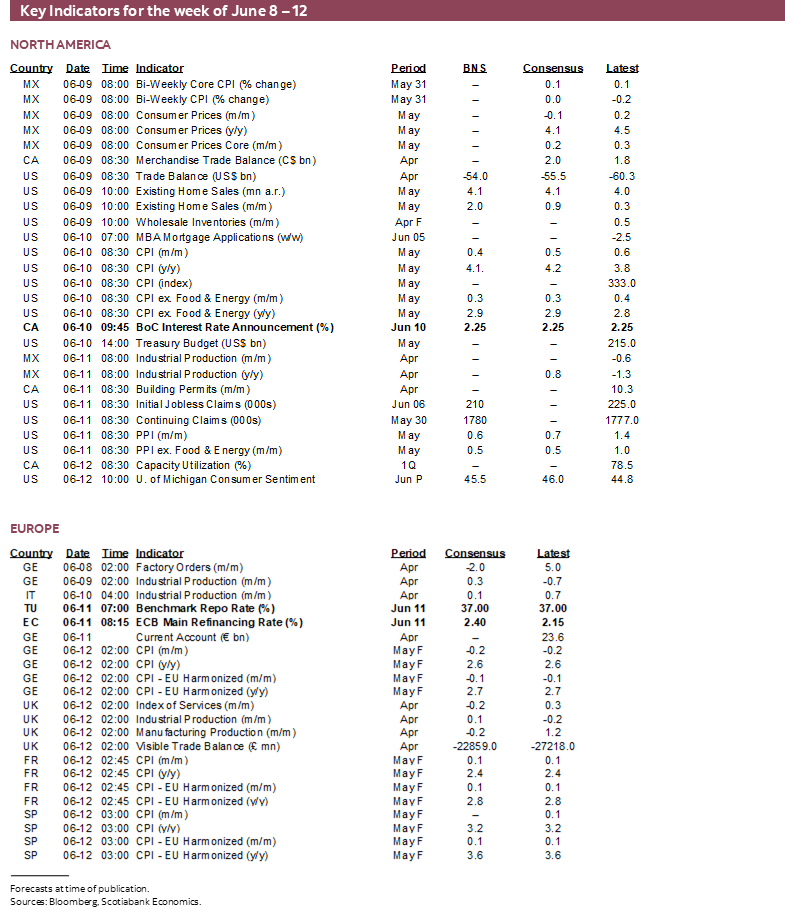

Inflation watch kicks into high gear again with CPI (Wednesday) and producer prices (Thursday) both scheduled for updates. Combined they will inform expectations for the Fed’s preferred PCE inflation readings on June 25th.

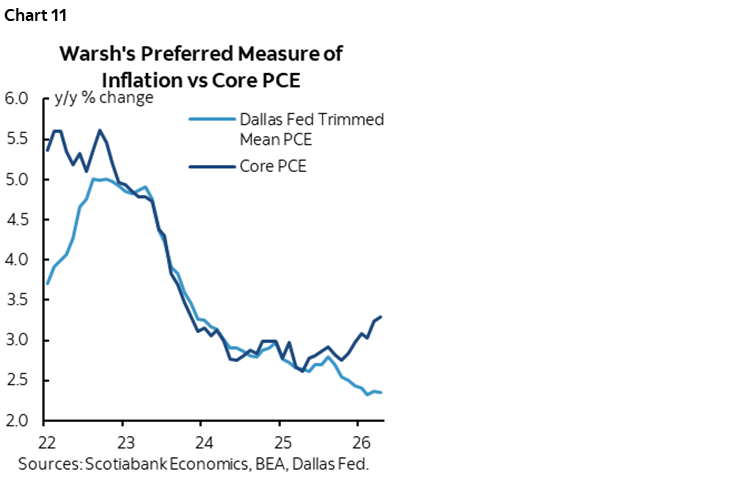

Or at least they used to be the preferred metrics. That’s more in doubt now, as Chair Warsh takes the helm. His seemingly preferred measure—trimmed mean inflation—will be updated by the Cleveland Fed for trimmed mean CPI shortly after CPI, and by the Dallas Fed for trimmed mean PCE after we get those figures.

Depending upon what variation of trimming Warsh may opt for—and hopefully informed by research—there is a case to be made for how today’s inflation is more of a relative price shock across a narrower portion of the US inflation basket than generalized inflation (chart 11). This argument is part of why the Federal Reserve may come to view inflation as not meriting a policy response in terms of hiking while leaving the door open to future easing.

Our forecast remains in favour of easing with the FOMC predicted to cut by 25bps in December and then another cut in Q1. Further on inflation is the point that the US may be less likely to experience second-round effects of supply chain shocks given the Fed existing restrictive stance and the view that the US responds to cost spikes in a different way than elsewhere. US businesses may be more likely to once again cut costs including trimming employment expenses in favour of higher productivity aided by heavy tech investments including but not limited to AI.

Expected negative annual benchmarking revisions to payrolls in September—about a week before the September FOMC—and expected softness across hiring measures over 2025H2 are added parts of our narrative alongside cooler trend US GDP growth.

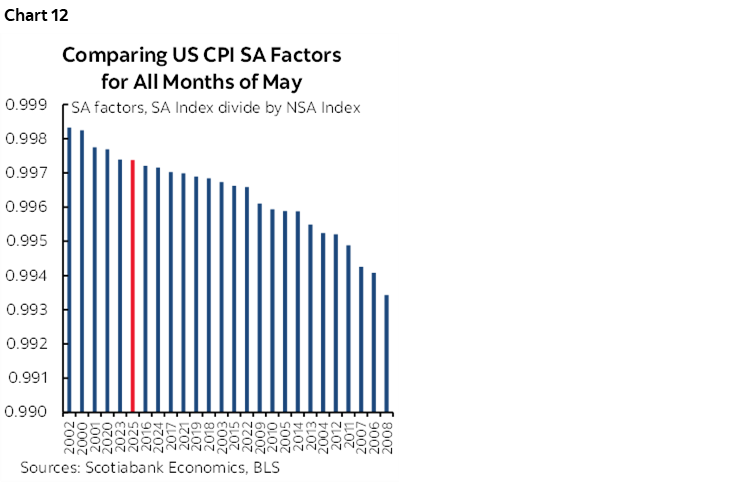

As for CPI, I’ve estimated a rise of 0.4% m/m SA in May (4.1% y/y) with core CPI at 0.3% m/m SA (2.9% y/y). It’s normally a seasonal up-month for unadjusted prices and higher gasoline prices should contribute to this along with food. Seasonal adjustment factors have been haircutting seasonally unadjusted price changes more so in recent years than previously (chart 12) which could have a dampening effect.

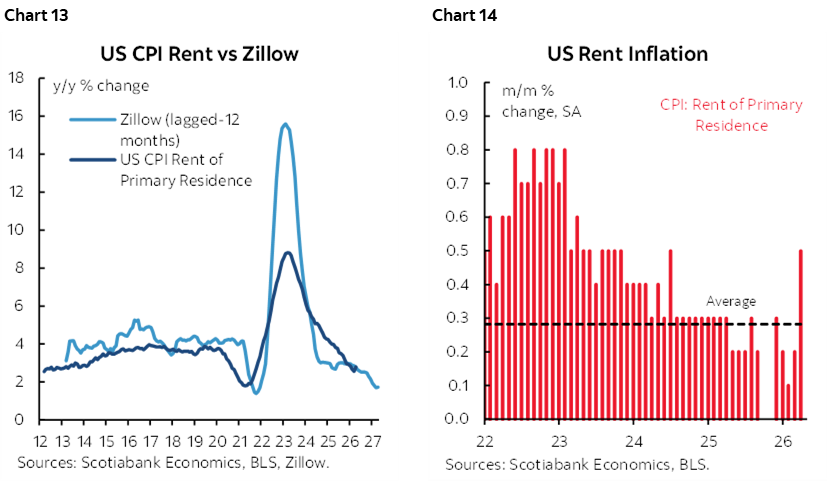

Rent inflation continues to ebb (chart 13). That could mean that the large spikes in primary rent and owners’ equivalent rent during April are unlikely to repeat and could well swing around the other way (chart 14).

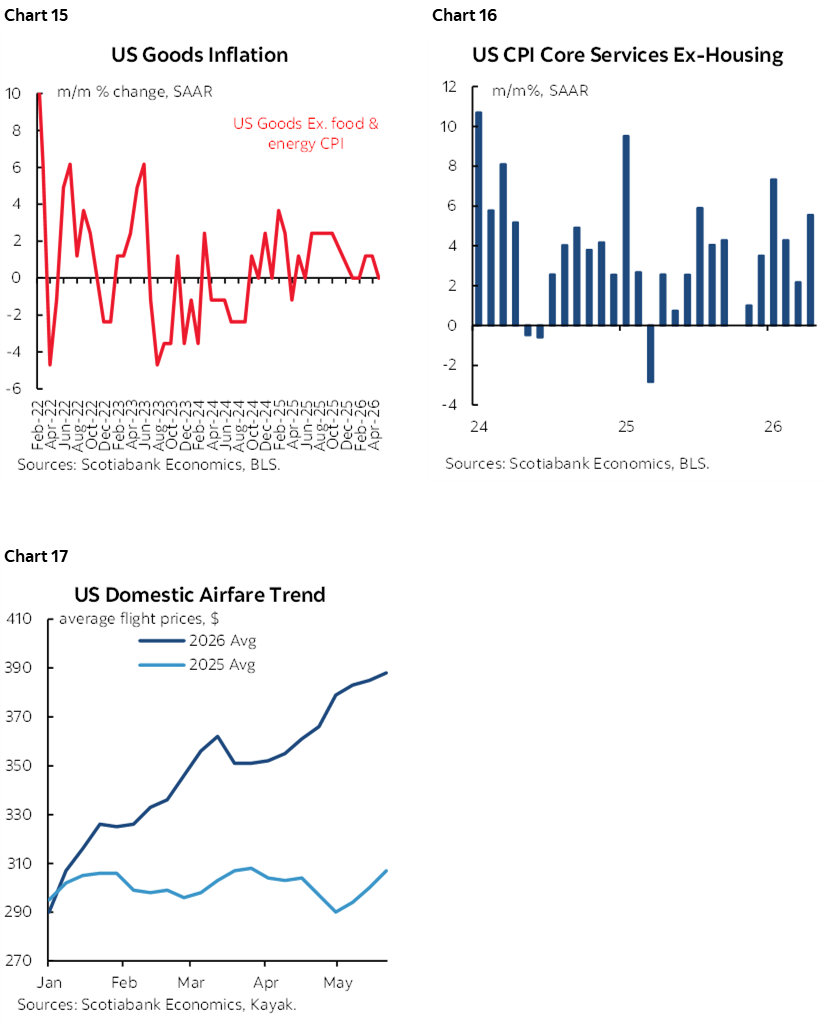

A key factor that makes me nervous about this report is the tango going on between core services and core goods inflation. It’s possible that short-term effects of tariffs on goods prices are ebbing (chart 15), although longer-wave supply chain effects of protectionist US policies remain at a highly nascent stage of evolution. Core services prices (ex-energy and housing services), however, have been skyrocketing (chart 16). An area where further service inflation is likely is through domestic airfare (chart 17), but much of the rest of that portion of the basket is difficult to estimate.

Producer prices are expected to rise by 0.6% m/m with core PPI up 0.5%. What matter, however, are the components that feed into core PCE including airline passenger services, portfolio management, hospital outpatient care, physician care, home health and hospice care, hospital inpatient care and nursing home care. Those PPI categories contributed a negligible amount to core PCE inflation in April despite the large 1% m/m jump in core producer prices.

ECB—TAKE A HIKE!

The European Central Bank is priced for lift-off with a 25bps hike on Thursday. An updated statement will be accompanied by fresh forecasts that will inform the path thereafter. Markets are on the fence between pricing 1–2 more hikes in 2026 after this one.

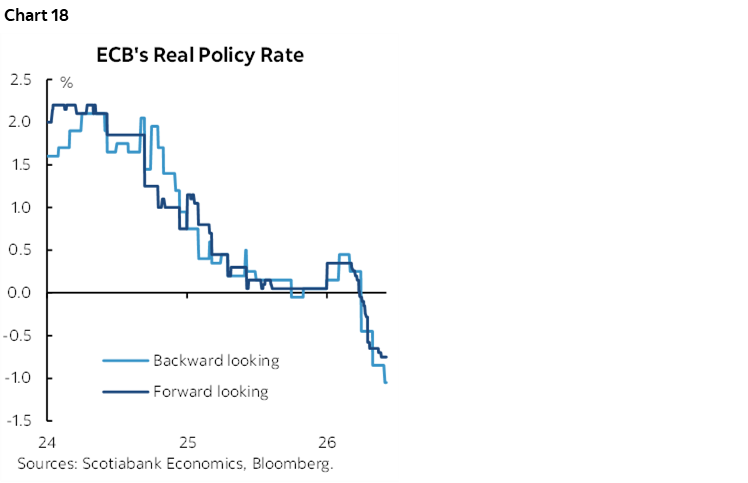

Barring a large, sudden turn of events, this will be the first of a minimum of two hikes designed to neutralize a meaningful portion of the decline in the real policy rate shown using backward looking y/y inflation and one-period forward expected inflation (chart 18). Most economists and models would use the real rate as input into forming projections for growth, inflation and other macro variables. To passively ease through a plunge in the real policy rate in the face of a supply chain shock would be inappropriate in feeding second-round inflation risks and so we’re open minded to potentially even greater tightening ahead. One hike would do little to nothing to neutralize this passive easing and even 2–3 may not be enough depending upon the course of further developments.

The projections for the March 19th communications were based upon inputs as at March 11th. President Lagarde lauded her team for quickly presenting an early assessment of the impact of the supply shocks emanating from the war with Iran. A lot has changed since then and since the additional policy hold on April 30th and so freshened forecasts will be key to the narrative.

Before even finalizing and sharing projections there seems to be fairly high agreement on the Governing Council in favour of tightening policy including remarks by the following officials. Note, however, that some influential officials are more circumspect or more sensitive to pre-committing—like the ECB’s Chief Economist Lane—while others are less direct such as President Lagarde.

- Yannis Stournaras: “The likeliest outcome is an interest rate hike in June.”

- Isabel Schnabel: “We can no longer look through this shock. The risk of de-anchoring inflation expectations is rising.”

- Alvaro Santos Pereira: “I think it’s better to act sooner rather than later.”

- Frank Elderson: “It is increasingly unlikely that we can look through this shock.”

- Oli Rehn: “A rate increase in June would be an insurance one, but not due to entrenched inflationary pressures.”

- Pierre Wunsch: “My concern is that if we wait to check all the boxes in a meeting-by-meeting approach and set a very high bar for hiking, we may end up acting too late.”

- Dimitar Radev: “The cost of acting too late can exceed the cost of acting somewhat earlier.”

- Fabio Panetta: “The forward-looking picture seems to call for a recalibration of the monetary policy stance to counter the risk of persistent inflationary tensions.”

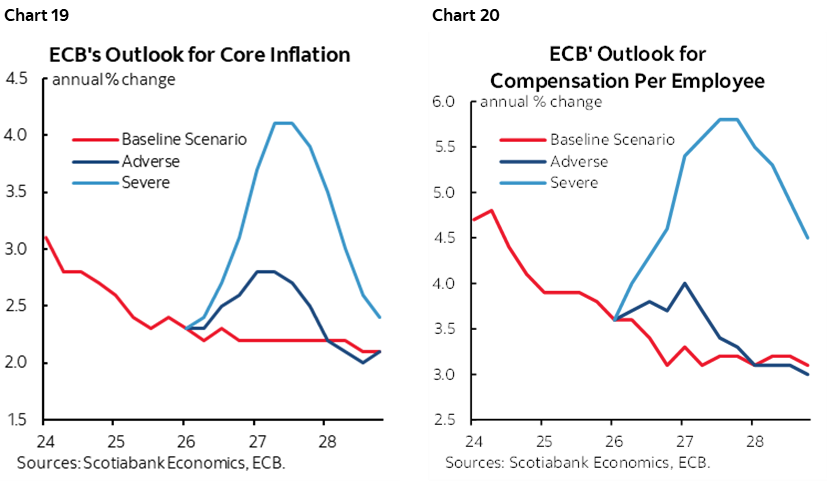

Recall that the March communications included the publication of base case, adverse, and severe scenarios (here). The associated inflation forecasts are shown in chart 19 along with scenarios around second-round wage pressures (chart 20); the base case counsels looking through near-term inflation risk, the adverse scenario counsels policy tweaks in favour of modest tightening and the severe scenario says here we go again. With developments since then, one could argue that Governing Council is evaluating which of the adverse and severe scenarios may become a replacement for the previous base case. That uncertainty governs the decision to tighten but uncertainty about how much further to go.

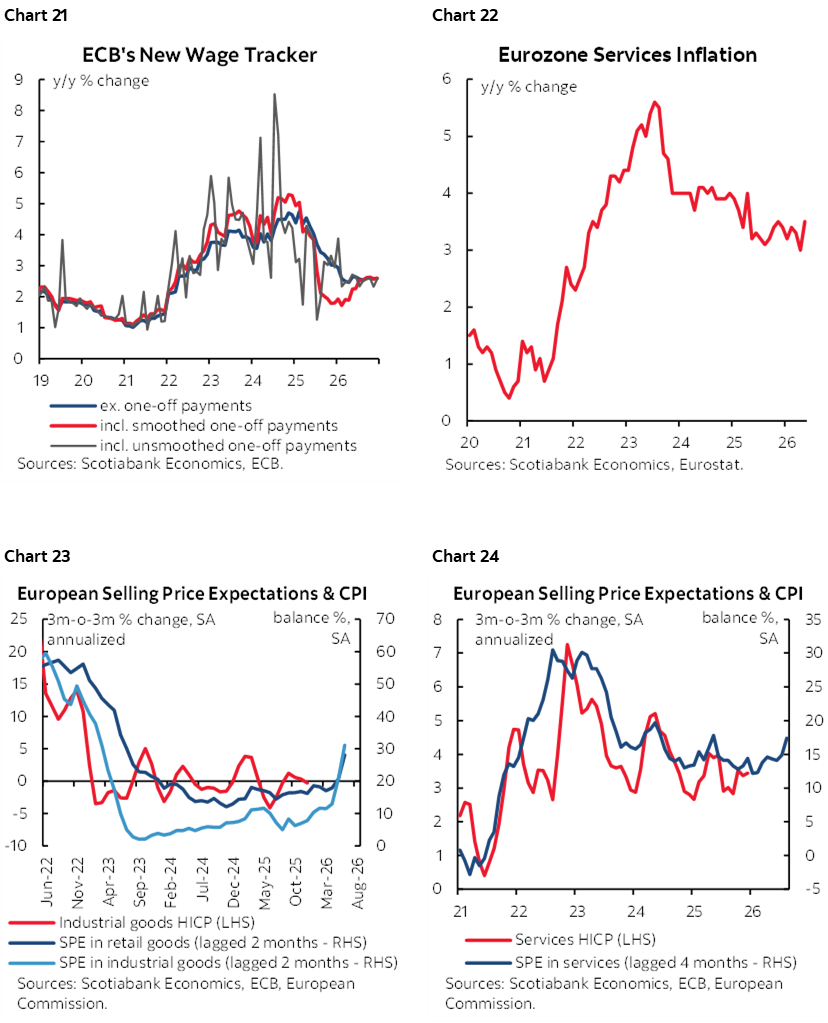

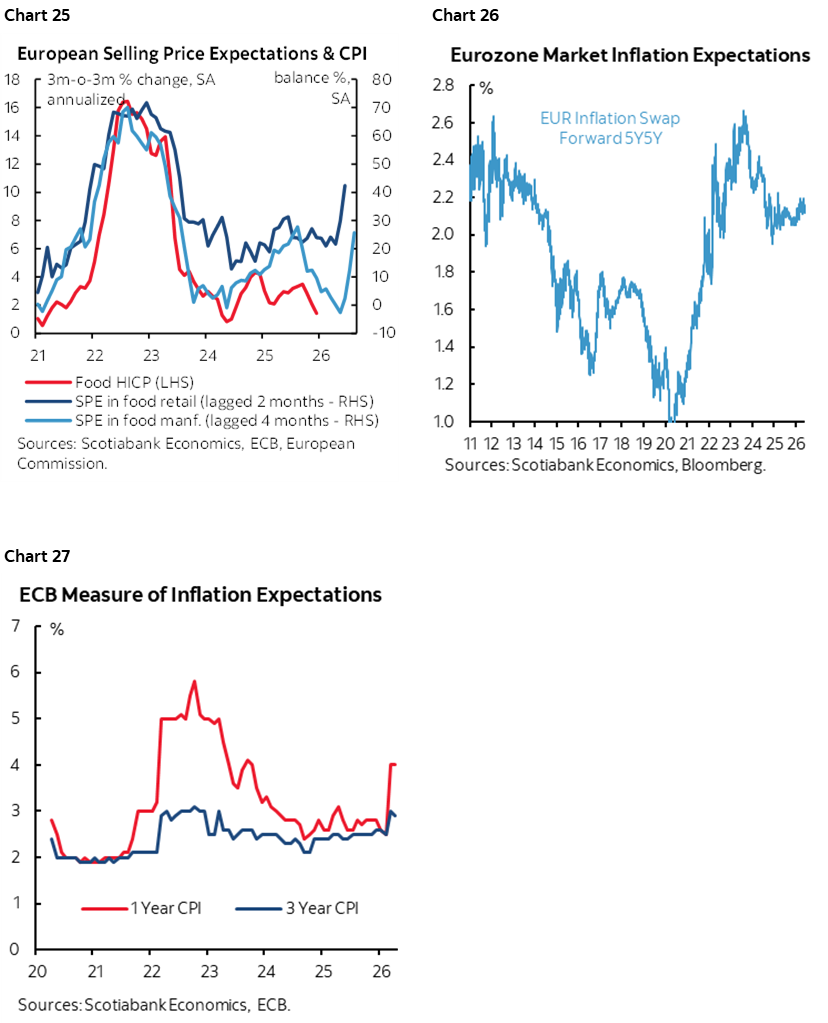

Which is where evaluating the evidence comes in. So far, there isn’t much clear evidence that second-round pressures are creeping into wage setting exercises, but it may be early for the unions behind the collective bargaining exercises to be getting agitated (chart 21). Recent core inflation has been relatively elevated compared to historical like-months of April and May. Services inflation has picked up a little from an already warm pace (chart 22). Selling price expectations drawn from survey evidence point to higher service prices (chart 23), higher retail prices (chart 24) and higher food prices (chart 25). Market measures of long-term inflation expectations have been edging a bit higher but not alarmingly (chart 26) and the ECB’s surveyed measures of 1- and 3-year inflation expectations have been doing likewise especially in the near-term (chart 27).

Having said all that, the ECB likely has a cautious eye on government spending. Fiscal policy may be substituting for monetary policy in a way that merits leaning against it with some policy tightening. As Europe arms itself to the eye teeth on defence and related spending, the trickle down effects on the economy may exacerbate the nature of this inflation shock and perpetuate meaningful second-round effects.

BCRP—LEFT OR RIGHT?

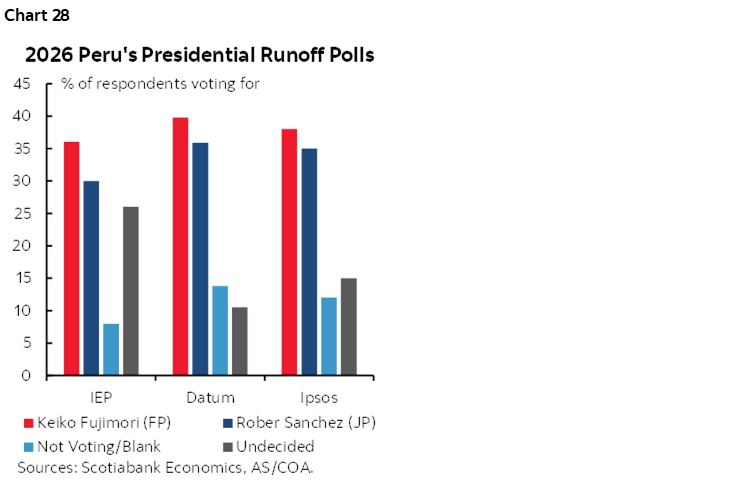

Peru’s central bank is likely to stay on the sidelines on Thursday, leaving the reference rate unchanged at 4.25%. The decision will follow the second round of the country’s Presidential election on Sunday.

That contest is a classic left-versus-right affair that pits Keiko Fujimori against the leftist candidate, Roberto Sánchez. Polls show Fujimori in the lead but not in an overwhelming sense and with a high undecided share (chart 28 and here). Her victory would be more likely to assuage market concerns.

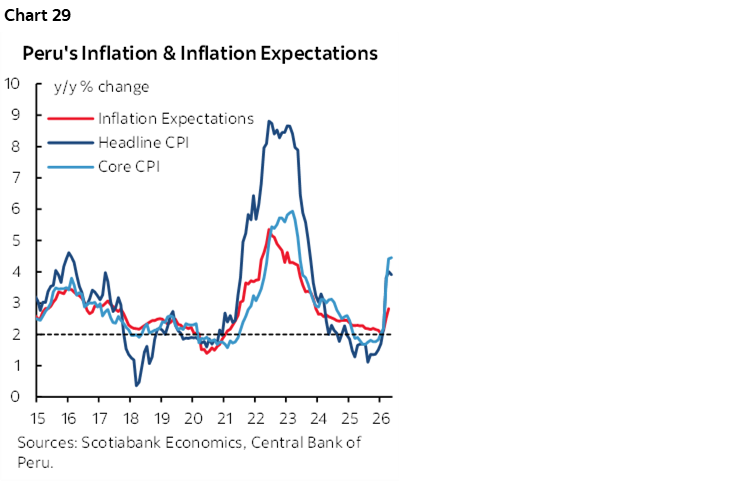

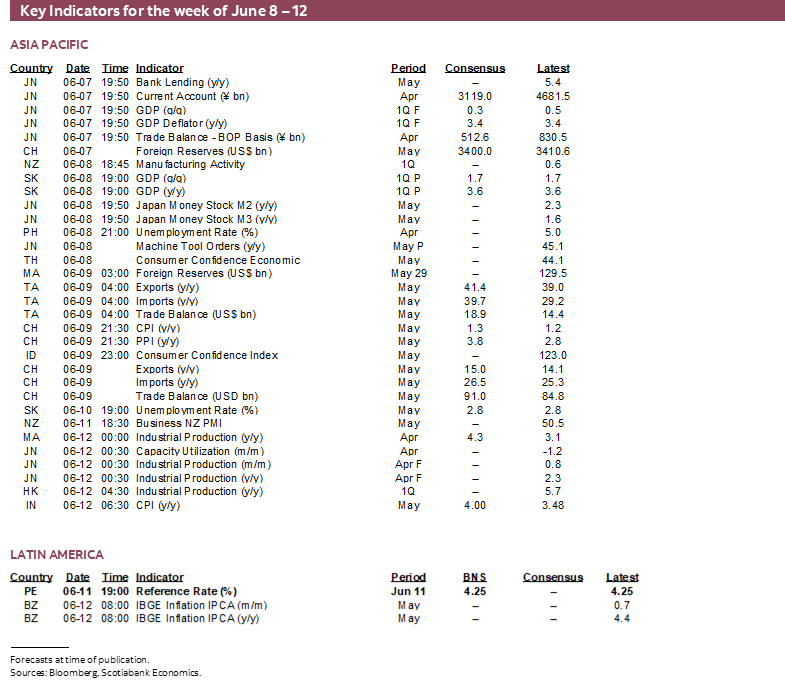

Further, BCRP’s inflation fears were at least temporarily assuaged by a slight deceleration in May CPI as prices fell -0.2% m/m, helping to bring the y/y rate down to a still high 3.9% after soaring from 1.5% at the start of the year. Still, core inflation is running at a hot 4½% y/y (chart 29). Pending the results of the election and the market aftermath this could mean that the policy hold is approaching its expiration date.

GLOBAL MACRO

The rest of the global line-up is summarized in chart 30 after covering most of the expected top-shelf developments aside from off-calendar developments like geopolitical matters. For this section I’ve tag-teamed with my colleague Jay Parmar.

Canada’s calendar will be very light beyond the BoC with just trade figures for April due (Tuesday) that could start to inform Q2 contributions to GDP growth from trade.

The US calendar will also bring out UMich consumer sentiment (Friday), existing home sales during May (Tuesday) that may be little changed based upon pending home sales, weekly claims, and a likely narrower trade deficit in April (Tuesday). The FOMC blackout starts this weekend ahead of the June 16th–17th meeting.

The broader global calendar is also expected to be relatively light, featuring a mix of April GDP and industrial activity data, along with around half a dozen countries releasing May inflation readings.

After a firmer set of inflation readings, the Riksbank will turn its focus to April’s GDP data to gain further insight into the country’s economic momentum, helping to assess the degree of flexibility it has to remain on hold while evaluating the impact of the conflict and supply chain pressures.

In the UK, April GDP, industrial production, and trade are due Friday, offering an early read on Q2 activity. After two consecutive upside surprises in monthly GDP, the focus shifts to whether momentum holds as incoming data start to capture the effects of the ongoing conflict.

Finally, May inflation prints are due across a range of countries ahead of their respective central bank meetings in the coming weeks. The updates are unlikely to be market-moving, with most central banks expected to remain on hold—Brazil being the exception, where another 25bps cut is anticipated at the next meeting. The week starts with Chile on Monday, followed by China and Mexico on Tuesday and Norway on Wednesday before Brazil, Malaysia and India close on Friday.

The Central Bank of Turkey is expected to hold its benchmark repo rate on Thursday while staying alert to inflation risks. Q1 GDP disappointed, but inflation has edged higher. As such, the bank is likely to retain a hawkish bias, with scope to tighten further if the outlook worsens.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.