Risk Dashboard for July 20th – 24th

- US-Iran tensions may enter uncharted waters

- AI rivalry to continue driving tech volatility

- Canadian CPI update has little riding on it

- Fighting forest fires with tariffs is rich on so many counts

- ECB faces a sobriety test

- BI likely to hike again

- Turkey’s central bank will remain highly restrictive

- Russia’s central bank faces a tough choice

- SARB expected to raise its policy rate

- Global macro: PMIs, UK jobs and CPI, Aussie jobs…

- …NZ CPI, Canadian retail sales and PPI, Japanese CPI, SK GDP

Risk Dashboard for July 27th – 31st

- FOMC—Cliff Diving

- BoJ—He’s Back!

- BoE—About that second round

- Canadian GDP—tracking the rebound

- US GDP still resilient

- US core PCE likely to plunge

- BCCH—Slack versus oil

- BanRep—no buyer’s remorse on hiking

- Global macro: China PMIs, US macro readings…

- …CPI in EZ, Australia, Japan…

- …GDP in EZ, Mexico

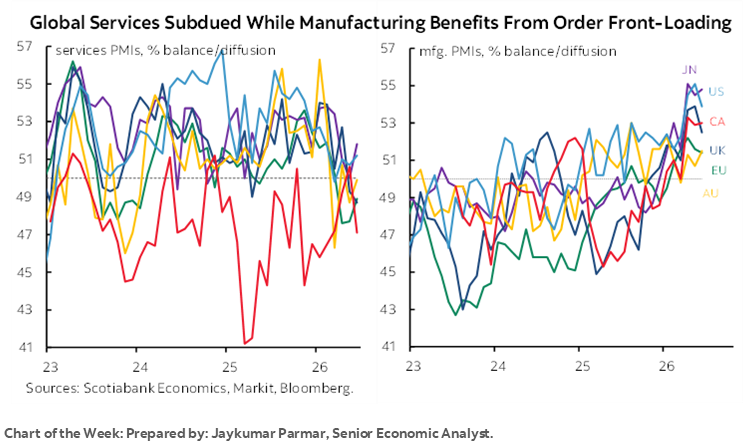

Chart of the Week

This two-week edition is intended to reach ahead and share views on a round of upcoming pivotal developments across central banks, a lot of data and earnings reports and no doubt geopolitical drivers across asset classes.

Perhaps overshadowing all of the calendar-based developments will be intensifying risks around tech valuations and conflict in the Middle East.

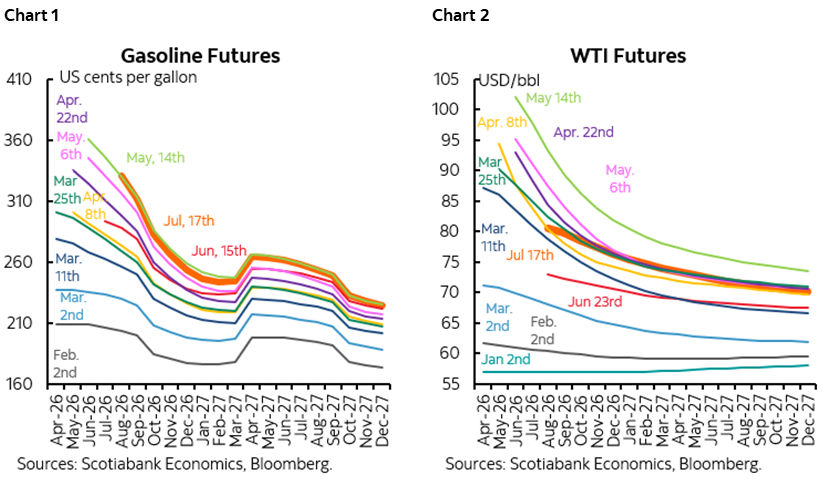

It’s more likely hubris than reality, but President Trump’s warning about soon bombing civilian assets in Iran would be the biggest escalation to date and puts us into uncharted waters on the conflict including forms of retaliation. The MOU is in ashes and was never sustainable in the first place given Iran’s managed irresolution approach to negotiations and given President Trump’s poor polling around handling the war. We’re now looking at the highest gasoline futures curves of the conflict to date (chart 1) with oil futures approaching prior peaks especially further out in time (chart 2).

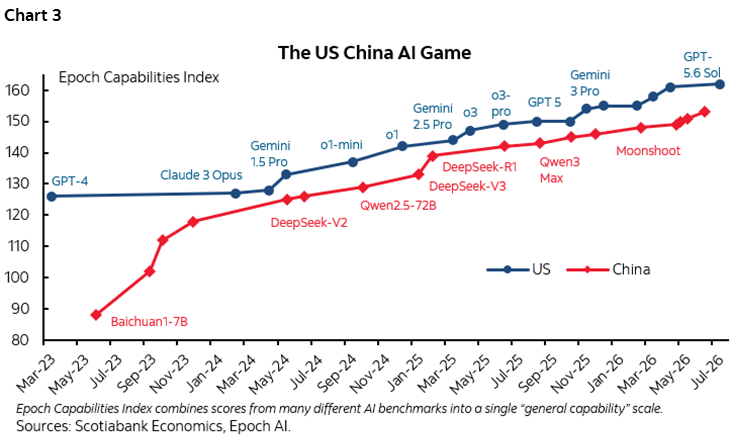

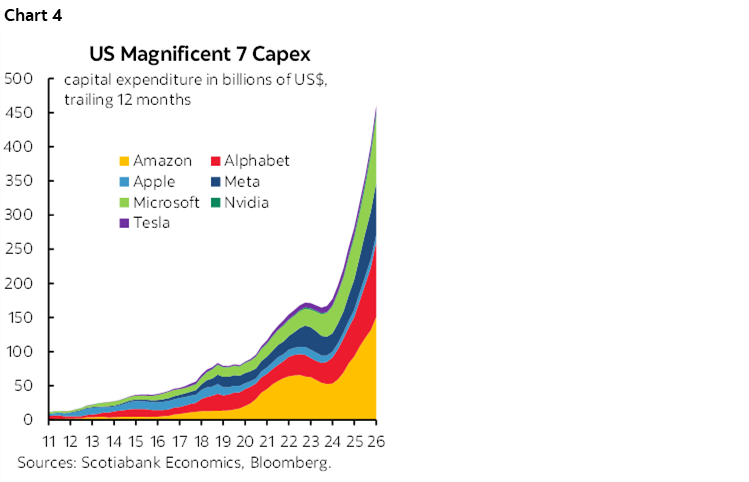

I wouldn’t overreact to AI developments just yet but they’ll continue to drive high market volatility. US firms and Chinese firms continue to jostle for leadership in AI and occasionally trade places but the US has generally managed to stay a step ahead with its own bouts of innovation according to measures like the Epoch Capabilities Index (chart 3). Neither system is likely to have much tolerance for widespread job losses in my opinion, but particularly China’s uni-party state and much less flexible economy. By contrast, China’s capital infusions into AI may be more patient than investors in the US seeking some evidence of monetization of chart 4.

Also watch for developments around Canada-US relations and tariffs as Trump threatens action along with Republicans across northern states. Short of building a wall or lining up every fan in the country at the border to keep the smoke out it’s unclear what is being proposed as solutions or help. Any US trade actions on this matter would be patently unfair and must be met with a stiff response in my view. Recall Trump’s attacks against California’s fire prevention tactics he suddenly now alleges should be made greater use of but in the world’s second largest country by area with massive forests. The problem is not unique to Canada as many regions of the US are experiencing forest fires and so have parts of Europe and Asia over the years. The US is a massive contributor to global warming as it ranks #2 in the world on GHG emissions behind only China and while there are many possible adjustments that can be made for climate, population etc, it is aggregate GHG emissions that drive global warming (here). The Trump administration’s environmental policies are worsening global conditions and in total defiance of the science of climate change. Canada was there to help the US with fires in the past including California by sending water bombers and fire fighters; where’s the US help now?! Penalizing Canada for what has been caused by governments that have turned a blind eye toward environmental concerns is rich beyond belief.

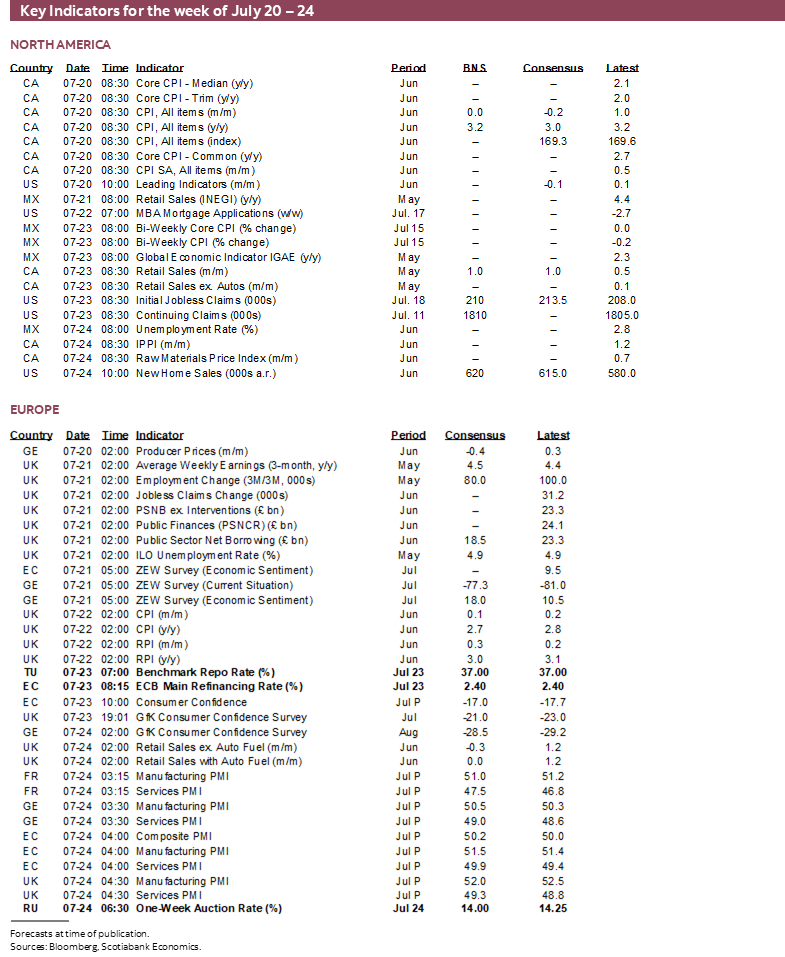

Week of July 20th – 24th 2026

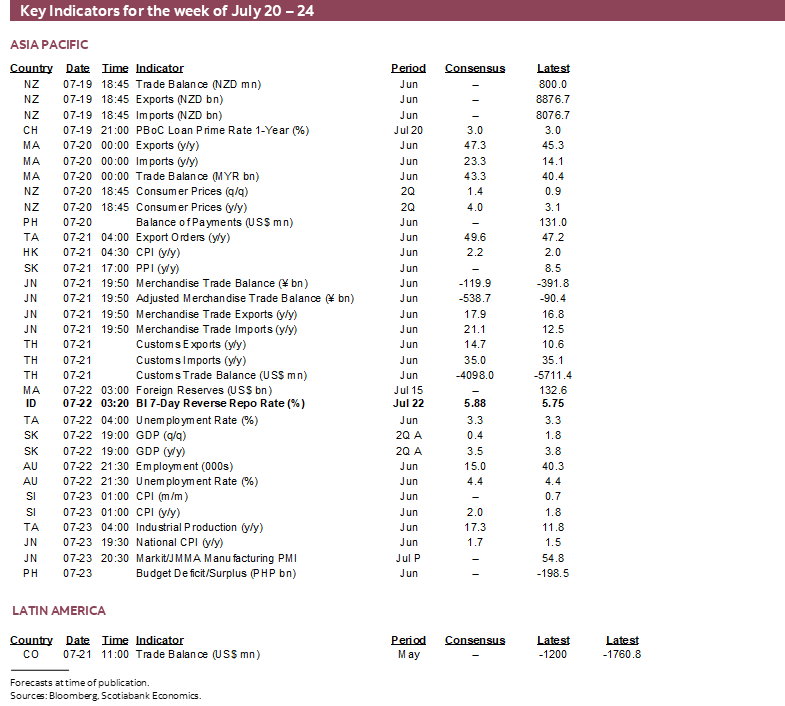

The first week focuses upon a few central bank decisions across majors and EMs (ECB, BI, SARB, Turkey, Russia) plus Canadian inflation, global purchasing managers’ indices, Australian jobs, UK jobs, wages and CPI, New Zealand’s inflation and South Korea’s economy.

CANADIAN INFLATION—NOT MUCH RIDING ON THIS ONE

Canada refreshes CPI for the month of June on Monday July 20th. I’ve estimated a flat headline reading of 0% m/m NSA that would mean an unchanged rate of 3.2% y/y.

Not a whole lot hangs on this estimate. It’s one or two inflation reports before the BoC’s next decision on September 2nd. There will also be one more jobs report and Q2 GDP before that decision which itself is a non-MPR meeting. Plus, a whole lot of additional information such as developments in commodity markets.

June is normally a seasonal up-month for prices which matters because the polled estimate is seasonally unadjusted. The dip in gasoline prices may be more than offsetting. The prior month’s strong gain in the leisure category of prices—led by a massive rise in travel tour prices—is likely to reverse and be reinforced by a likely drop in airfare. On the upside, I’ve assumed shelter costs will return as a driver.

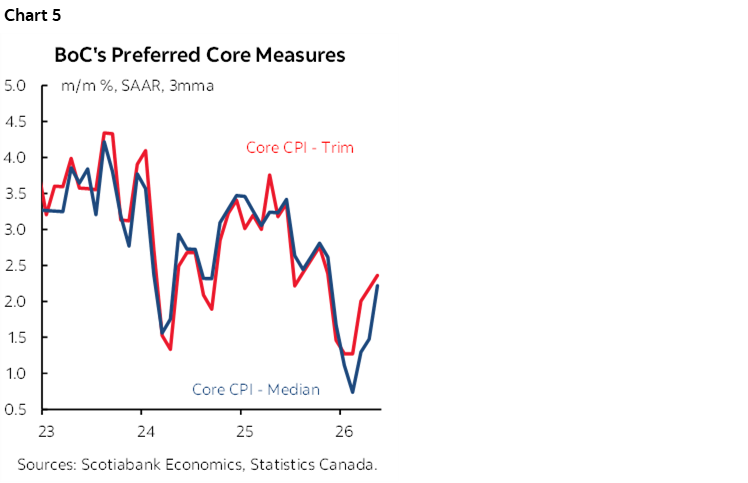

Amid wild swings in the tails of the distribution of prices the key will be the central tendency price measures like trimmed mean CPI and weighted median CPI. It’s fruitless estimating them in the form that matters for evaluating price pressures at the margin. That form is m/m SAAR, for which we have so little price information relative to the sensitivity to exactly what counts in the measures. These measures have been rebounding from a temporary soft patch in keeping with our long-held expectations (chart 5).

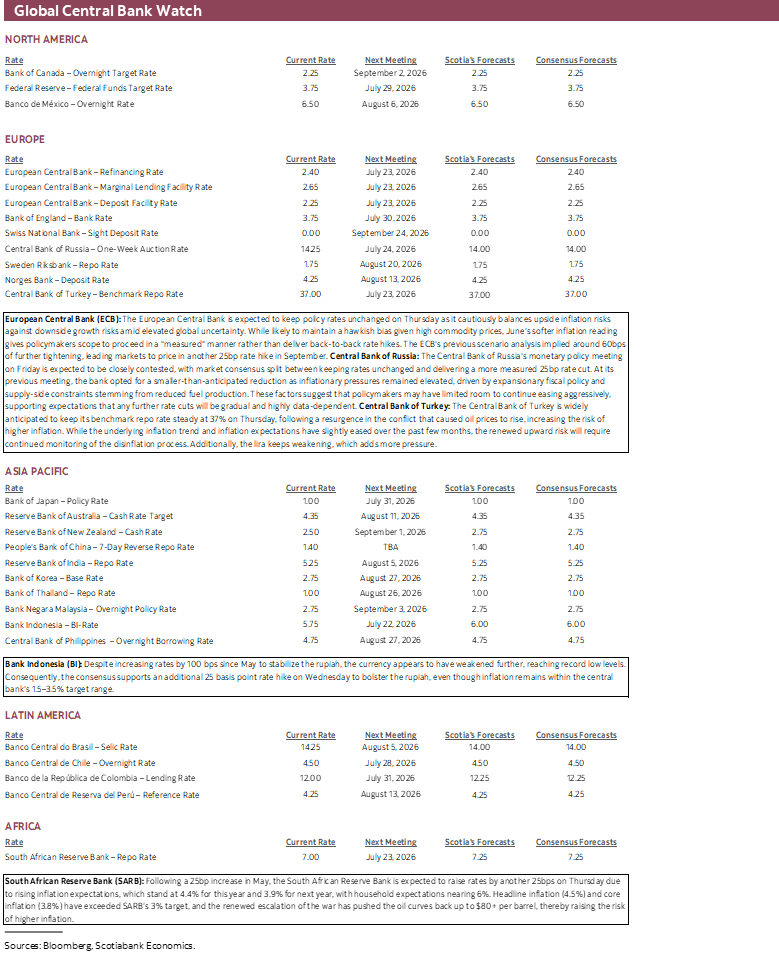

CENTRAL BANKS—DOVES A THREATENED SPECIES

Five central banks deliver policy decisions during the week of July 20th–24th. Key may be guidance from the ECB while several EM central banks weigh in with varying responses to global inflation risk.

Bank Indonesia—Likely to Hike

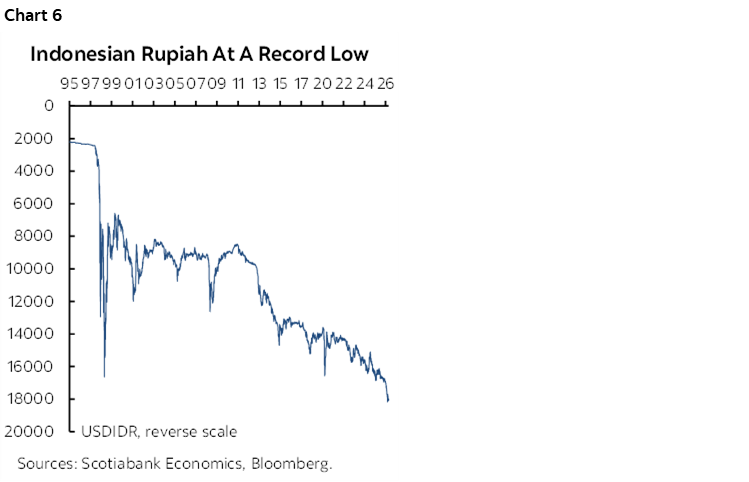

Wednesday’s Bank Indonesia decision is expected to deliver another hike but a minority within consensus thinks they could hold at 5.75% after delivering 100bps of hikes since April. Those hikes included two in June starting with an emergency 25bps increase and then another one at the scheduled meeting nine days later and started with a surprise 50bps hike in May that doubled consensus. The point being the usual reminder about this central bank’s proclivity toward surprises. One factor that may prompt continued tightening this week is continued depreciation of the rupiah and the bank’s stability concerns (chart 6).

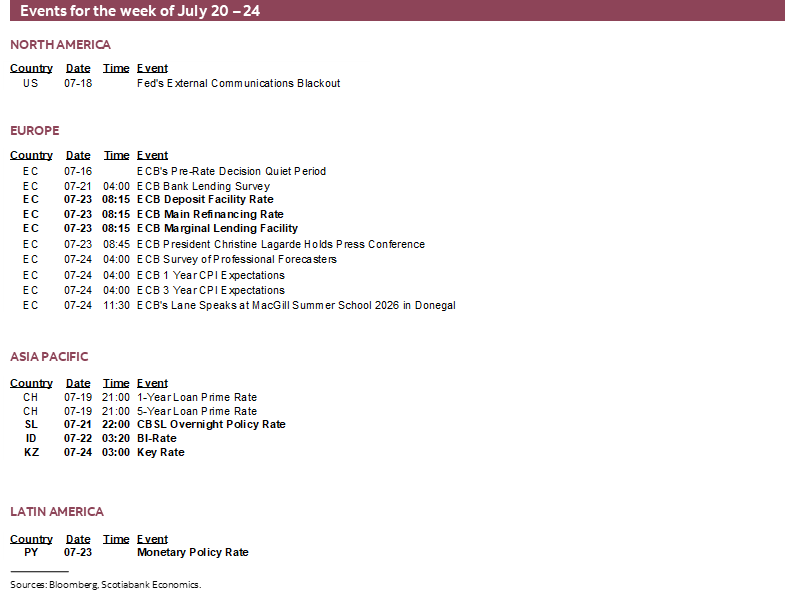

ECB—A Sobriety Test

Policy adjustments don’t need to go in a straight line especially at points of elevated uncertainty. That sentiment appears to be driving market pricing for Thursday’s decision to offer a hold at a deposit rate of 2.25% following the 25bps hike that was delivered on June 11th. Consensus also expects a hold.

President Lagarde’s last major remark was on July 1st when she noted “I think risks by the way that we have to the upside on inflation and to the downside of growth are probably more broadly balanced than they were a few weeks ago as a result of what we’re seeing, which happens at speed.”

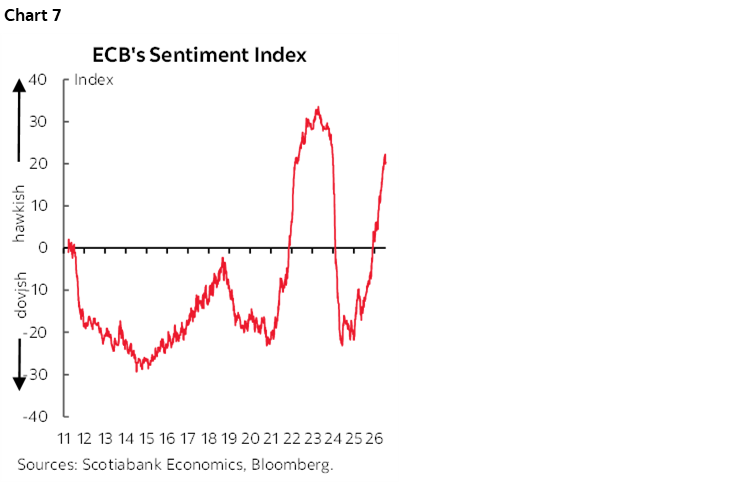

Since then, it has been back on for the US war with Iran. WTI and Brent have both risen by about a dozen dollars per barrel. The German 2-year yield has climbed by about a quarter of a percentage point. Somewhat of an offset was the June inflation report that likely buys time for the ECB to further assess conditions given its data dependent mantra; CPI fell -0.1% m/m with core CPI pulling back to 2.4% y/y from the 2.6% prior level that was the highest since April of last year. Still, sentiment gauges clearly show that the hawks largely remain in control (chart 7).

Turkey’s Central Bank—The Best Laid Plans…

The Central Bank of Turkey is expected to hold at a one-week repo rate of 37% on Thursday. It halted an easing campaign after January’s 100bps cut when the Iran war broke out. The lira has since depreciated by about 8% to the dollar, adding to import price pressures driven by commodities and namely oil.

SARB—Could be a Little, or a Lot

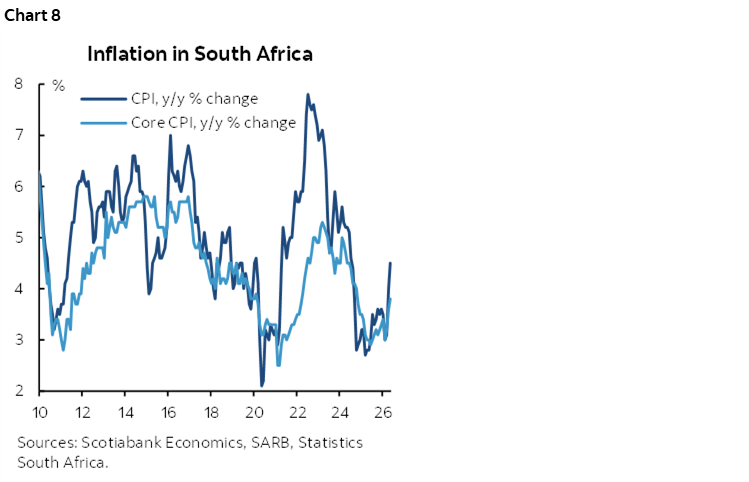

The South African Reserve Bank is widely expected to hike its repo rate by 25bps to 7.25% on Thursday. Inflation is on the rise with May clocking in at 4½% y/y and core at 3.8% y/y ahead of Wednesday’s June update (chart 8). It’s possible there will be dissenters as there were in the prior month’s 4–2 vote to hike. Scenarios that were presented at the prior meeting suggested that tightening could drive the policy rate as high as into the 7–8% range.

Russia’s Central Bank—You Made Your Bed

Friday’s decision by the Central Bank of the Russian Federation could be another step down in pace, this time to a halt. The bank has cut 50bps on three occasions this year before downshifting to a quarter point cut in June. Now they may entirely halt easing as inflationary pressures begin to rise once again. Total CPI was up over 6% y/y again in June with core CPI crossing back above 5%. The war direct effects and indirect effects on energy prices—including Ukrainian strikes on Russian refineries—have put upward pressure on the cost of living that may tilt the balance of policy risks toward managing inflation risk and a little away from addressing stumbling economic growth. The Russian economy was flat in Q1 (-0.2% y/y) and growth had been sharply decelerating throughout 2025. The Putin regime made its bed. The public has to suffer the consequences.

GLOBAL MACRO—BEYOND N.A.

The first week of this two-week issue brings out a number of other potentially high-impact readings from across the global economy but you’ll have to look beyond North America for most of them except for updated tracking of Canadian and Mexican consumers.

Canadian Retail Sales and Producer Prices

Canada refreshes retail sales for May and offers preliminary guidance for June on Thursday July 23rd. Statcan guided on June 19th that May’s nominal sales were tracking a 1% m/m SA gain. Some of that gain was probably due to higher prices as evidenced by the 0.5% m/m SA rise in CPI and 0.3% gain in CPI ex-food and energy. Watch volumes that strip out price effects.

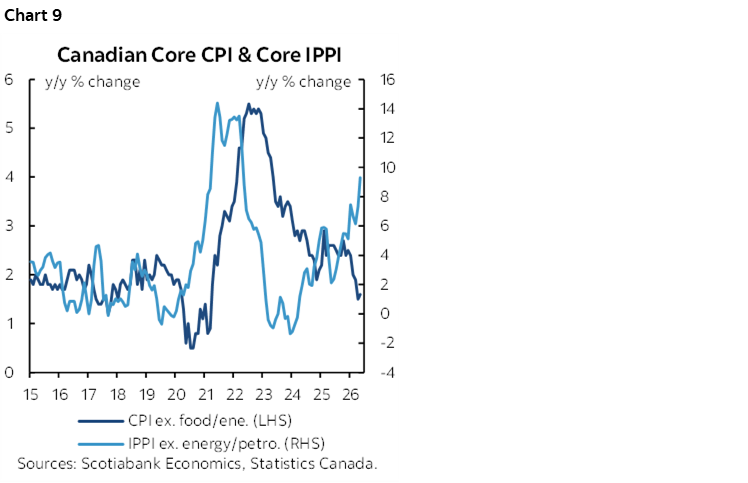

Canada also updates producer prices for June on Friday July 24th. Key will be industrial prices ex-food and energy given the role that core producer prices play as a leading indicator of consumer price inflation (chart 9).

Relatively Quiet in the Rest of N.A.

US markets will primarily focus upon the continuation of the Q2 earnings season in the first week. New home sales during June (July 24th) are likely to rebound.

Mexico refreshes retail sales for May on Tuesday. Sales have been growing at about a 4 ½% y/y nominal pace so far this year but growth is expected to slow.

Global Readings Focus on PMIs, Jobs and Inflation

A batch of global purchasing managers indices will be refreshed with July readings over Thursday July 23rd – Friday the 24th. Japan and Australia kick it off followed by India, the Eurozone, the UK and then the US.

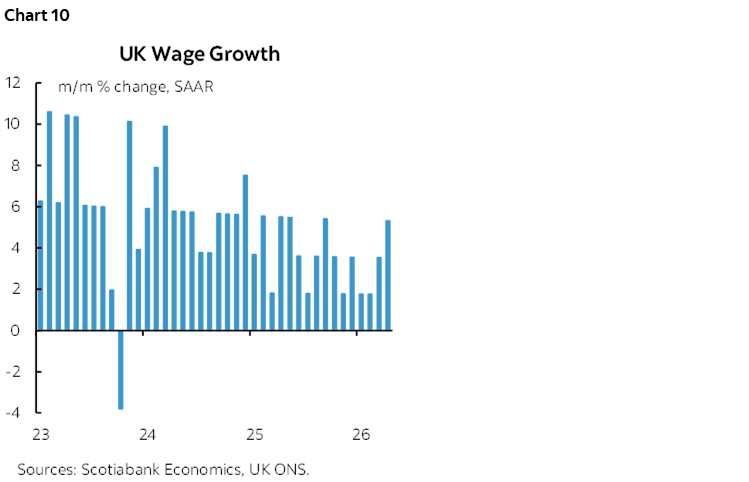

The UK refreshes two key sets of readings this week, one on jobs and wages (Tuesday) and the next on CPI (Wednesday). It also refreshes retail sales during June on Friday. Nothing is priced for the following week’s Bank of England decision, but markets are clinging to pricing 1–2 hikes thereafter. Key will be second-round effects of higher commodities amid a pick-up in wage growth (chart 10) but so far there are MPC members who remain highly sceptical that such pressures will be material. Bank of England Deputy Governor Breeden recently sounded against hiking as she downplayed second-round effects of oil on inflation by flagging a soft economy and labour market slack: “Those two things mean that that shock is less likely to become embedded and lead to inflationary dynamics that we might need to lean against.”

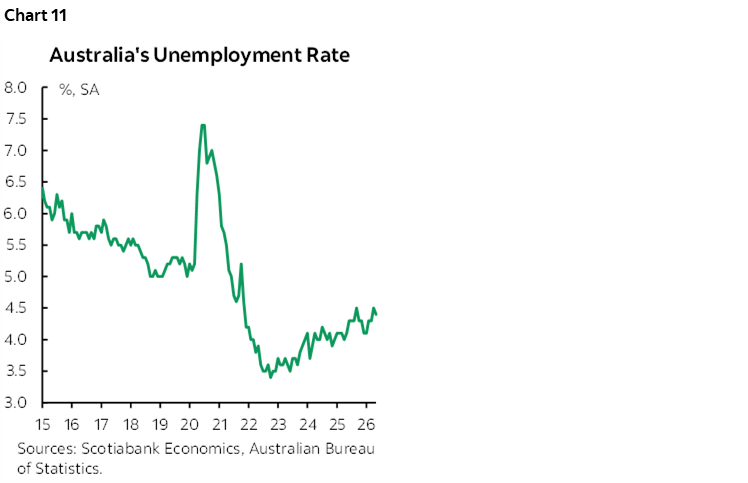

Australia’s jobs juggernaut has been on first for some time. Can it keep it up with June’s numbers on Wednesday? With the exception of April’s 41k drop, every month has seen gains this year although there has been a tilt more toward part-time job creation. Still, while it is off the bottom (chart 11), the unemployment rate remains low at 4.4% but that’s partly because the pool of available workers seeking employment has been softening as evidenced by the decline in the labour force participation rate since early 2025.

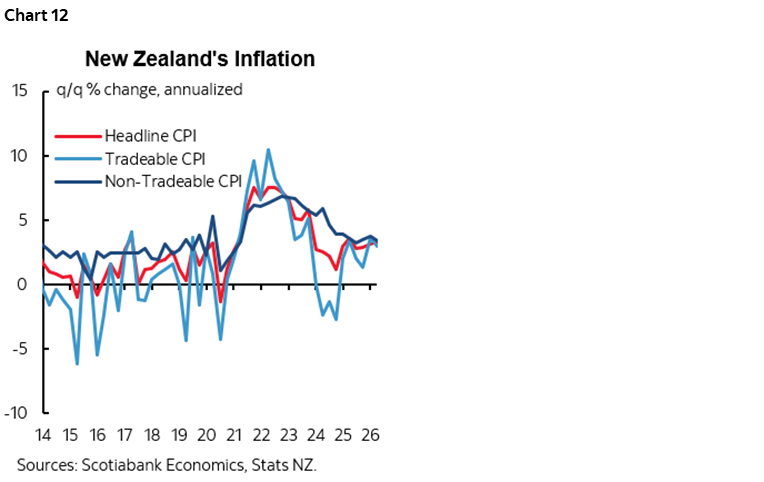

RBNZ watchers will have a keen eye on Q2 CPI (Monday). Markets are priced for another hike at the next meeting on September 2nd and about a percentage point of hikes through to the middle of next year. A hotter reading compared to the warm trend (chart 12) is very likely given that CPI figures are pushing into the initial effects of the surge in commodity prices due to the Iran war. A nonannualized reading that could be the highest in years would provide ample cover for further tightening.

Japanese CPI inflation on Thursday is likely to closely follow the Tokyo gauge that climbed by three-tenths to 1.7% y/y in June. The BoJ delivers an updated decision the following week (see below).

South Korea’s economy and markets are stumbling to say the least. The first high level take on how much so will come with Q2 GDP on Wednesday. Most estimates range from ¼% to ½% q/q nonannualized growth and with probably further weakening ahead as monetary policy tightens and financial conditions tighten. The Kospi has lost one-quarter of its value since late June.

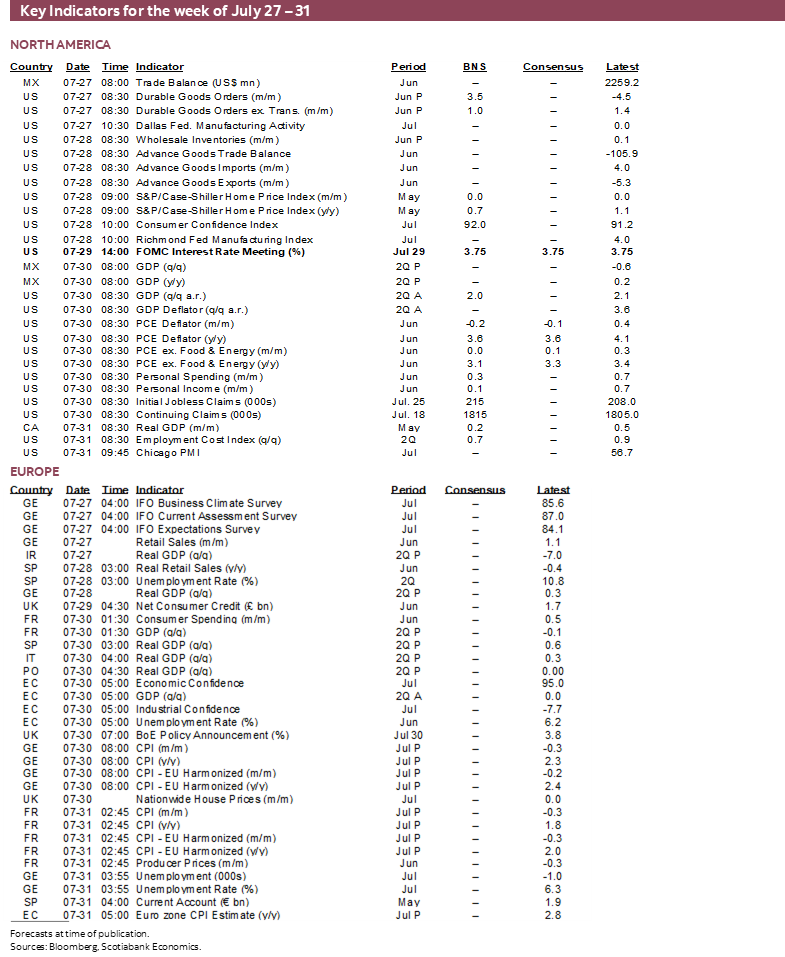

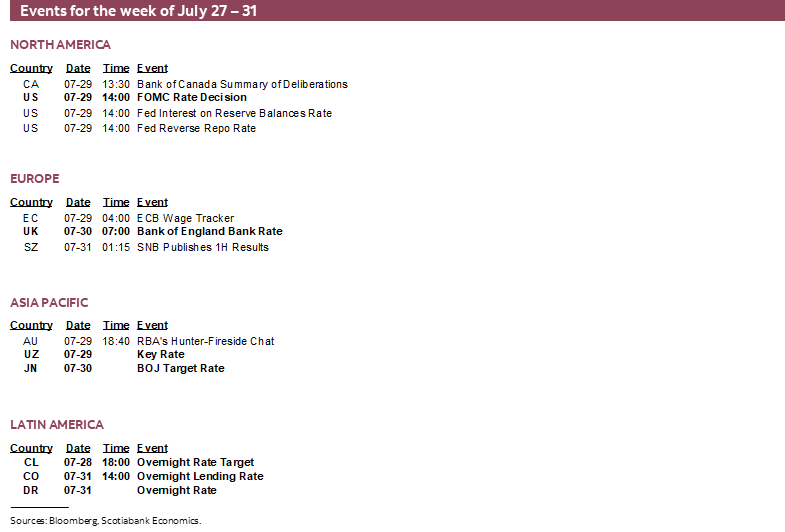

Week of July 27th – 31st 2026

The second week covered by this publication will bring out more of the heavy hitters among global central banks (Fed, BoJ, ECB, BoE) and a pair of LatAm central banks (Chile, Colombia) alongside a wave of global PMIs, GDP reports and inflation updates.

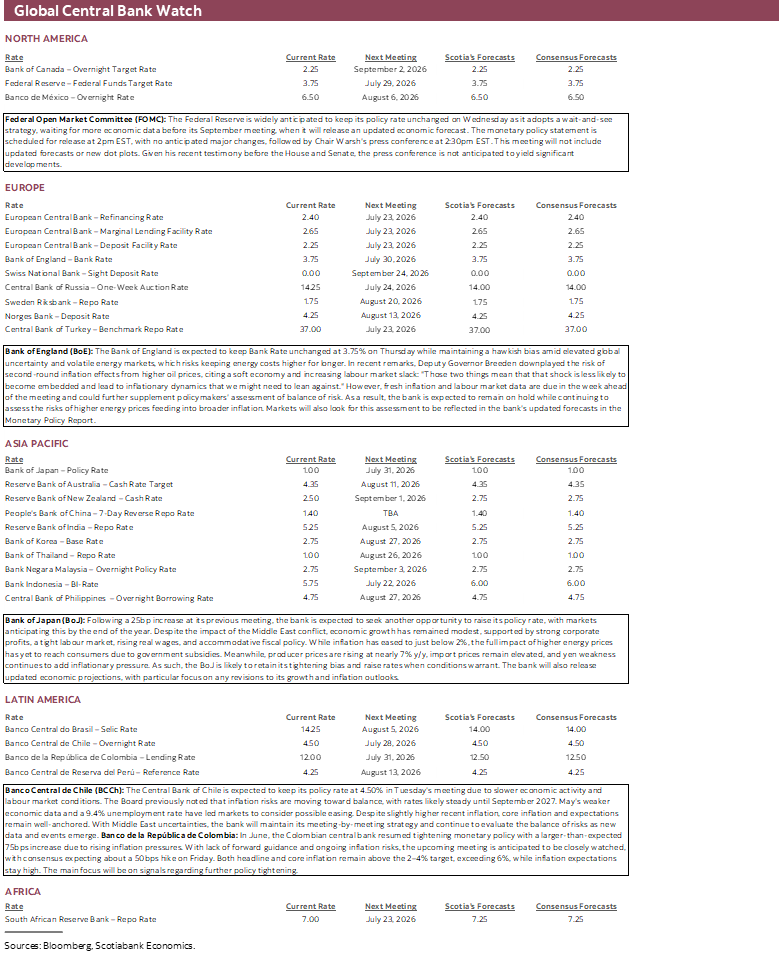

CENTRAL BANKS—WHAT’S THE BIGGER RISK OF POLICY ERROR?

Several central banks will offer policy decisions during the week of July 27th – 31st. The majors are expected to hold but a LatAm bank could hike.

FOMC—Cliff Diving

Notwithstanding the possibility of dissenters, no one really expects much out of Wednesday’s communications from the Federal Reserve’s Open Market Committee. This one will only offer a statement at 2pmET sans forecasts and dots, followed by a press conference thirty minutes later. The next Summary of Economic Projections including a revised dot plot will be delivered at the September 15th–16th meeting. Chair Waller is no fan of explicit forward guidance so we won’t hear clear messaging on the next move which will be informed by data, taskforces, geopolitical developments etc.

Consensus unanimously expects a hold and markets are priced for a hold at an upper bound target rate of 3.75%. Markets had been pricing about half of a hike at this meeting at stages throughout the latter half of June and first half of July when we were advising clients to receive OIS pricing. A hike at this meeting never made sense. Why?

Chair Warsh warned that the FOMC will take price stability seriously after years of blowing the 2% target, but also told markets to be patient as the work of his five task forces gradually begins to arrive over the Fall into year-end. Impatiently hiking felt incongruent to guidance to be patient! Markets chose to hear hike and soon and have been back pedalling ever since.

The Committee appears to be divided on whether to move toward any further hikes but particularly this soon. As near as we can tell, the only clear voice in favour of possibly hiking at this meeting was Governor Waller when he spoke the day before weaker than expected US CPI and made his view conditional upon the outcome which likely weakened his case. Other voting members have either argued that policy is well positioned (Governor Jefferson, NY Fed President Williams), or guided that the rate may have to go up depending upon further rounds of data (Governor Cook, Dallas President Logan), or circumspect by flagging a stable but not good job market and how June CPI was encouraging but not enough evidence (Chicago’s Goolsbee). Cleveland President Hammack has perhaps been the most strident voice expressing a near-certain opinion that tighter policy is needed to address inflation that she claims is driving “a growing sense of despair.”

Note that several of the most hawkish voices on the FOMC vote for four more meetings and then shift into backseat driver roles come January (Logan, Hammack, Kashkari). Some members have been rather silent and not just Governor Powell who has shifted out of the limelight.

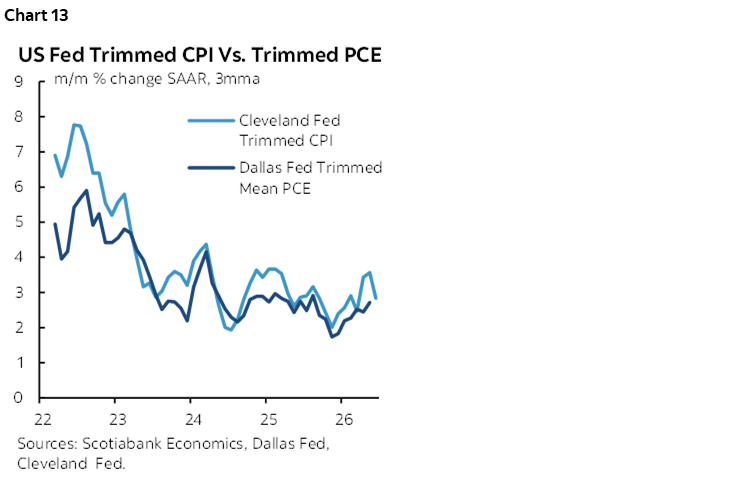

Should the Fed eventually opt to tighten, then my belief is that there is higher risk of policy error being committed. Trimmed mean CPI and PCE readings have been recently cooling but more data is needed (chart 13). Nothing can be done about current inflation—much less inflation over the past five years!—given lags of monetary policy actions.

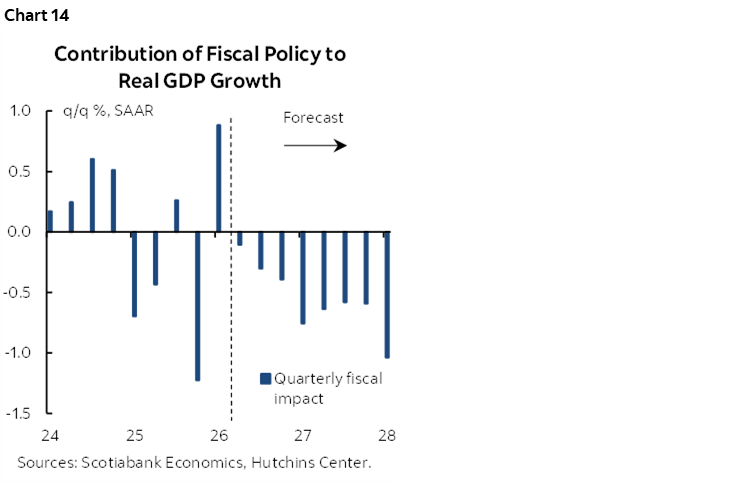

Tightening now could coincide with expected tightening of fiscal policy and its effects on growth (chart 14). If that were to coincide with cooler AI-related spending growth, then the US economy may be vulnerable into next year.

Monetary policy is presently modestly restrictive. Dollar strength mitigates some pass through of import prices.

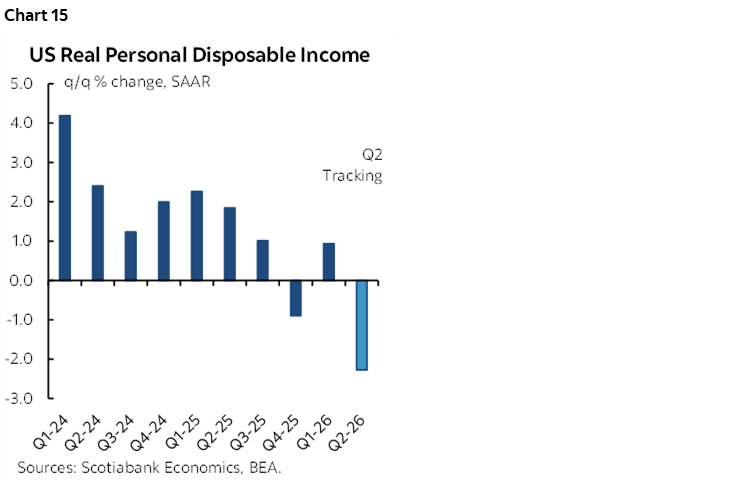

Second-round inflation pressures from the commodity surge could be constrained by real wage compression and multiple quarters of no growth in disposable incomes that impair purchasing power for everything other than gas and groceries (chart 15). Nominal wage growth vaulted higher out of the pandemic even ending 2022 at 5% y/y once base effect distortions had shaken out; today’s wages are up 3.5% y/y.

A negative housing wealth effect and how businesses and wage setting exercises respond may also mitigate pricing power. Cost shocks to US businesses often prompt rationalization of costs including weaker hiring and higher productivity as offsets. It’s not like second-round pressures in Europe’s economy or even Canada’s where unionization rates and collective bargaining are far more pervasive than in the US.

Tightening to counter AI-driven inflation won’t work given that tax subsidies swamp the effects of borrowing costs. Some effects on inflation may be maturing such as tariffs but with caution around erratic policies. Profit margins are very high and offer the ability to absorb considerable price pressures. We can’t judge the duration of the war but think the incremental effects on commodity price pressures should wane once a new level is established. Today’s supply shocks are not like five years ago, nor is a demand surge occurring.

How AI may influence jobs, growth and inflation in future remains highly uncertain but I’m of the view it will damage jobs before stabilizing. Also note that annual benchmarking revisions to nonfarm payrolls arrive before the September FOMC.

In short, I’m of the belief that the Fed needs to be very careful with data dependency that amounts to walking forward while looking backward. They’re at high risk of walking off a cliff.

BoJ—He’s Back!

Governor Ueda is expected to return from his hospitalization and chair this Friday’s press conference after the Bank of Japan’s latest decision. Welcome back!

No change is expected and guidance may remain hawkish but noncommittal on timing future possible tightening. Markets begin to price material risk of another hike by the October 30th meeting and then have almost a full hike priced by December.

This will be a forecast meeting, however, which means that forward guidance could be informed by revised paths for GDP growth and inflation. Anonymous sources have told newswires that growth may be revised up partly on evidence of resilience but also tech influences, while more positively reassessing guidance about downside risks. Renewed intensification of the US war with Iran may prompt the central bank to revise up inflation forecasts.

BoE—Round Two!

The Bank of England is widely expected to stay on hold on July 30th. Markets are pricing material chance of a hike in Bank Rate by the September 17th meeting and over a hike by the November meeting.

MPC members have been deeply divided toward tightening prospects with the main message being one of patience as further information is gathered. Growth has been weak and a soft labour market points to some slack. Updates on CPI, jobs and wages before the meeting may further inform the bias. Bank of England Deputy Governor Breeden recently sounded against hiking as she downplayed second-round effects of oil on inflation by flagging a soft economy and labour market slack: “Those two things mean that that shock is less likely to become embedded and lead to inflationary dynamics that we might need to lean against.”

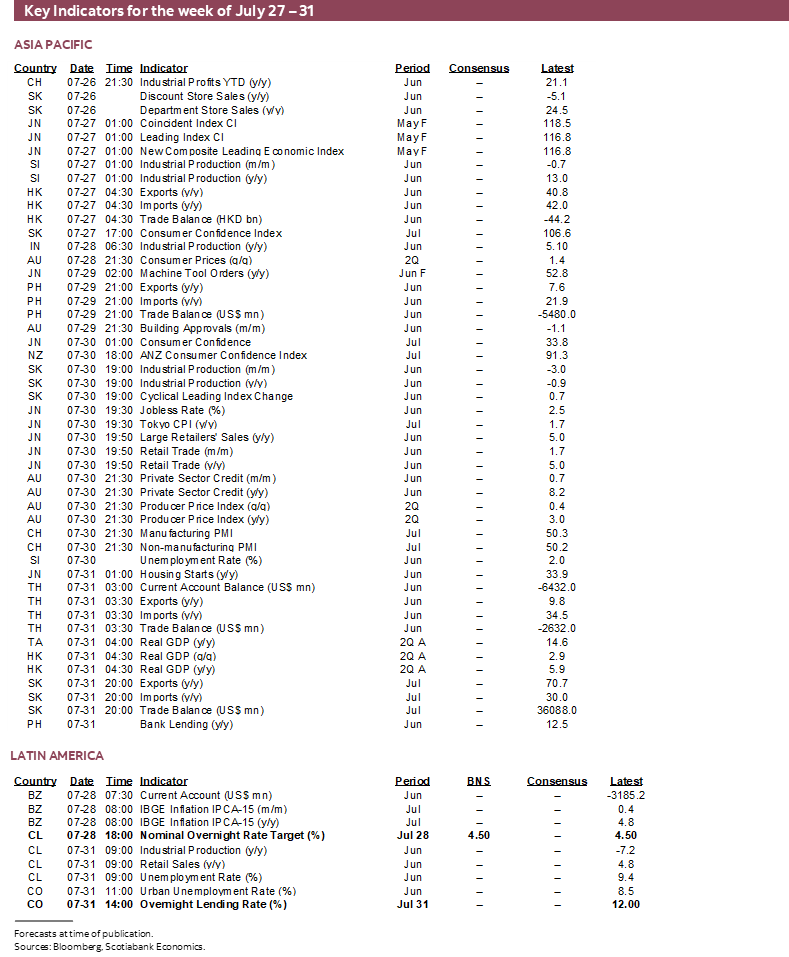

BCCh—Slack Versus Oil

Banco Central de Chile is widely expected to stay on hold at an overnight rate of 4.5% on July 28th. Guidance from the prior meeting on June 16th when a moderately dovish tone was struck may be stale by now given the reescalation of risks in the Middle East and commodity markets. Since that meeting, inflation accelerated to 4.3% y/y but mostly on headline influences as core CPI and inflation expectations are generally anchored. A weak economy that contracted by 0.3% q/q SA in Q1 and remains soft in Q2 alongside a high and rising unemployment rate of 9.4% are likely to continue to dominate neutral/dovish guidance.

BanRep—No Buyer’s Remorse

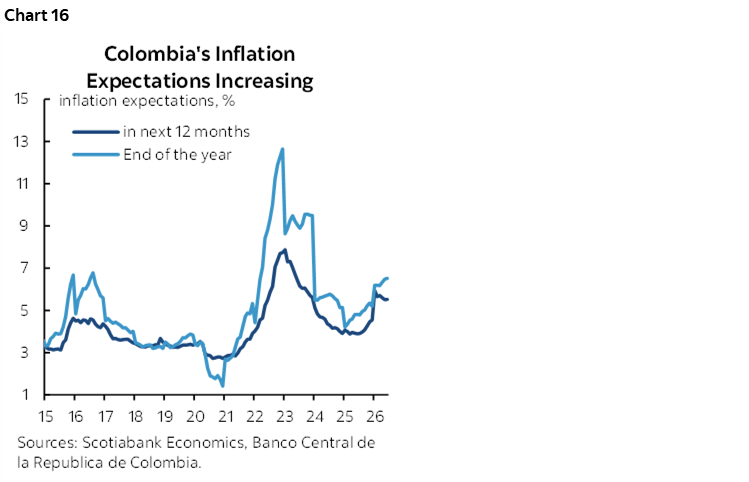

Colombia’s central bank is unlikely to have buyer’s remorse after hiking its policy rate by more than expected on June 30th when it raised the overnight rate by 75bps to 12%. The decision on Friday July 31st is likely to add more to policy tightening and could be another up-sized move. Headline and core inflation remain above the 2–4% target, exceeding 6%, while inflation expectations stay high (chart 16). The main focus will be on signals regarding further policy tightening.

CANADIAN GDP—TRACKING THE REBOUND

GDP growth for May with preliminary guidance for GDP arrives on July 31st. Like inflation, there won’t be a whole lot riding on this set of numbers in terms of policy implications.

Statcan had previously guided back on June 30th that GDP growth was tracking 0.1% m/m SA in May. A simple linear regression that I run against high frequency readings points to a little firmer growth of about 0.2%. Hours worked were up by a whopping 0.6% m/m SA. Housing starts slipped after a massive prior gain such that construction GDP may grow with lagging spending, and there were other positive signs on balance across other traditional readings. Less traditional readings for the services sector were rather strong including flights (chart 17) and restaurant bookings that temporarily surged in the two biggest cities (chart 18).

As for June, there is precious little to go by, such as a 0.2% m/m rise in hours worked that would indicate further growth given GDP is hours times labour productivity. Services remained buoyant.

For the overall quarter, Canada’s economy could be tracking at around 2¼% q/q SAAR using monthly production-side GDP accounts.

Canada also reports SEPH payrolls for May on July 30th. It lags well behind the more widely followed Labour Force Survey, is frequently revised in a major way and by definition excludes off-payroll firms that are a big source of employment in Canada.

GLOBAL MACRO—GLOBAL GROWTH AND INFLATION IN FOCUS

A wave of global macro reports not already covered will include Q2 GDP growth from the US, Eurozone and Mexico, China’s PMIs, inflation reports from the US, Eurozone, Japan and Australia. My colleague Jay Parmar and I put our noggins together on what follows.

US—Q2 GDP and PCE the Focal Points

US markets start the week with Monday's durable goods orders report, expected to bounce back after last month's drop due to transportation orders. Airplane orders from Boeing surged. Core durable and capital goods orders should stay strong, backed by robust US business investment. Total equipment spending tax write-offs under the BBB are subsidizing capital goods orders to the moon (chart 19) with the questions being a) is activity being brought forward, and b) what happens when the subsidies wane?

Tuesday brings June's advance goods trade report and the May house price index update, followed by the consumer confidence report on Wednesday, which is expected to show a modest improvement in July.

On Thursday, the BEA will provide a first early look at the US's Q2 economic growth performance with the key focus on the household consumption, investments and international trade considering that fiscal policy is expected to lose its positive effect on growth. Growth of around 2% q/q SAAR is expected. The personal consumption expenditure report will be the key amid no real income growth as higher prices reduce the purchasing power.

Also on Thursday will be the release of June PCE inflation data. Total prices are expected to fall by -0.2 % m/m SA given what we know about core CPI, methodological differences, and core producer prices. Core prices are expected to be flat (0% m/m SA) also given similar information. June’s CPI report was much softer than expected (recap here).

China PMIs—Slow Growth

In China, attention will turn to the release of the official July Purchasing Managers' Indices (PMIs) on Thursday. Since March, the headline PMI readings have shown signs of very slight improvement, generally stabilizing just above the 50-point threshold that separates expansion from contraction and hence in slow growth territory. However, the underlying details remain less encouraging. Manufacturing activity has been supported primarily by gains in production and new orders, with strength concentrated in export-oriented and AI-related industries. Meanwhile, expansion in the services sector has relied heavily on elevated business activity expectations rather than broad-based demand. As a result, the July report-providing the first snapshot of economic conditions in Q3-will likely see investors focus more on the underlying components than on the headline figures themselves.

Inflation Updates—Australia, Eurozone, Japan

In Australia, the focus will be on the Q2 inflation report due on Tuesday, which will provide policymakers with an important update on price pressures following recent oil price volatility. Prior quarters have been warm but had temporarily depicted a bit of progress (chart 20). Monthly trimmed mean inflation data through May suggest core inflation is running at around 3.6% y/y, above the 2–3% target range. While the Reserve Bank of Australia expects inflation to remain elevated in the near term, the key question is the extent to which higher commodity and energy costs are being passed through to consumers. The RBA has previously noted that "there are signs that some firms experiencing cost pressures are increasing the prices of their goods and services and others are looking to do so," highlighting concerns about broader inflation pass-through. As a result, policymakers will remain alert to any renewed acceleration in underlying inflation.

Additionally, Tokyo's July inflation report is scheduled for release on Thursday, followed by the Eurozone inflation report on Friday that could reverse the prior month’s improvement given rising energy prices amid renewed conflict in the Middle East. Given that both reports will be released after their respective central bank decisions, their immediate impact is expected to be limited. The next monetary policy meetings are in September, by which time another inflation update will be available.

GDP Round-Up

Finally, attention will turn to the advance Q2 GDP releases from the Eurozone and Mexico on Thursday, which will provide an early assessment of the economic impact of the global oil price shock and the resulting supply disruptions stemming from the Middle East conflict.

Following flat growth in Q1, Eurozone GDP is expected to expand modestly by 0.2% q/q SA in Q2. The conflict in the Middle East has weighed on growth momentum, reducing purchasing power and consumer confidence. Soft survey data suggest the economy remains in contraction territory, driven primarily by weakness in the services sector, while manufacturing activity has remained in expansionary territory, supported by stock building. Why is Spain the target of Trump’s envy? It’s not just football (aka soccer), as Spain’s economy have been red hot and outperforming rivalling the US on growth (chart 21).

In terms of the growth composition, the Eurozone economy is once again expected to be anchored by Spain's relative strength among the four largest economies, although growth is projected to slow to 0.4% q/q. France is expected to grow by 0.1%, while Germany and Italy are anticipated to remain broadly flat.

Meanwhile, Mexico's economy is expected to rebound by 0.6% q/q SA in Q2, following a 0.6% contraction in Q1. Given that the Q1 decline was broad-based across major sectors and, according to Banxico, "notably greater than anticipated," the focus will be on the pace of the recovery as previous rate cuts begin to support activity. However, uncertainty surrounding U.S. trade policy is expected to continue weighing on manufacturing activity and business confidence.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.