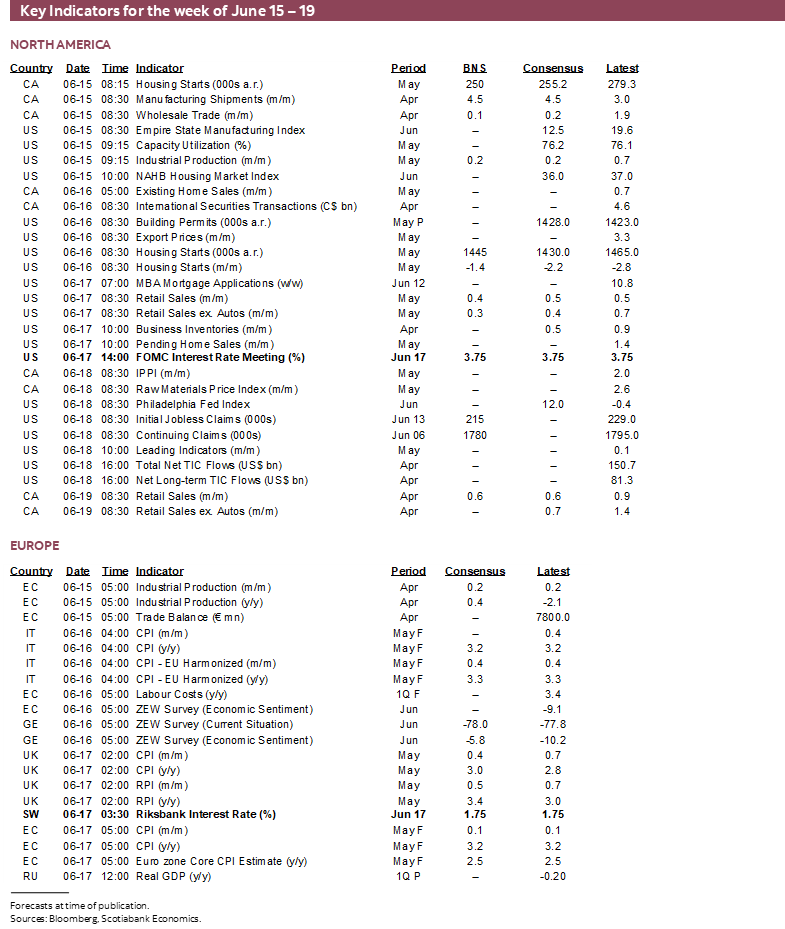

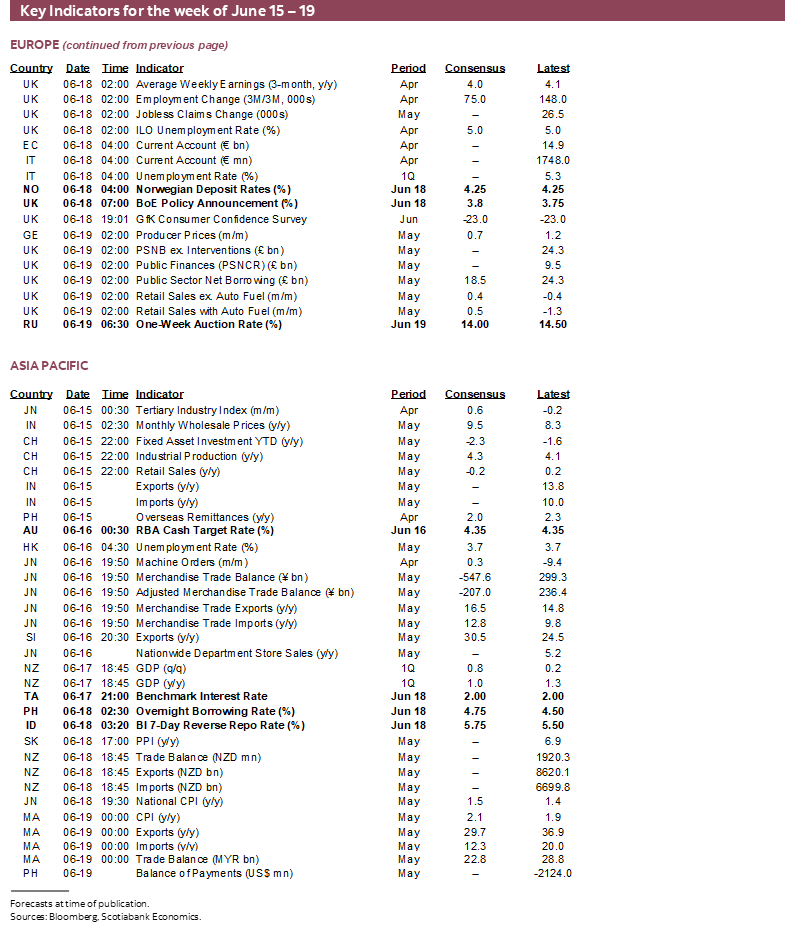

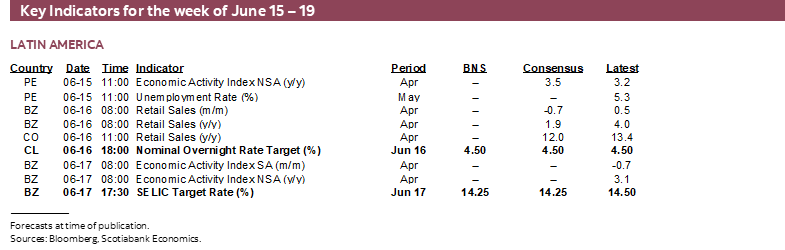

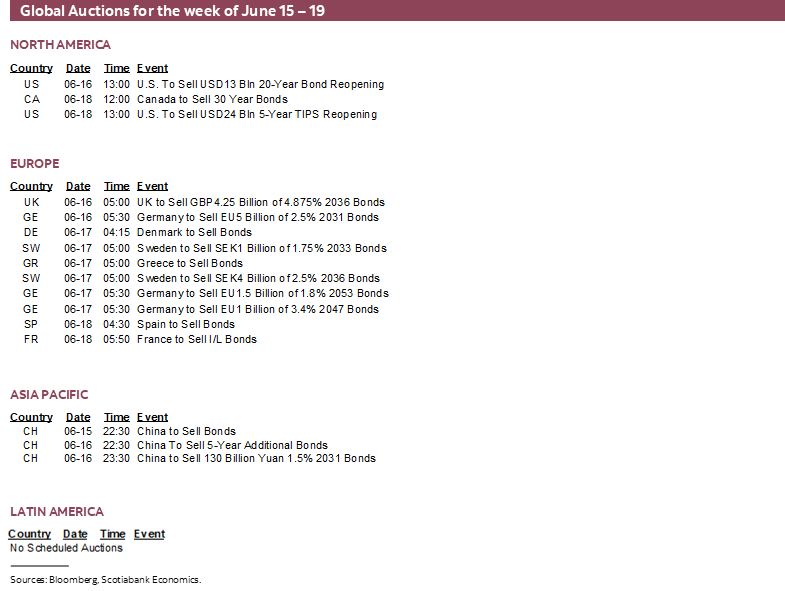

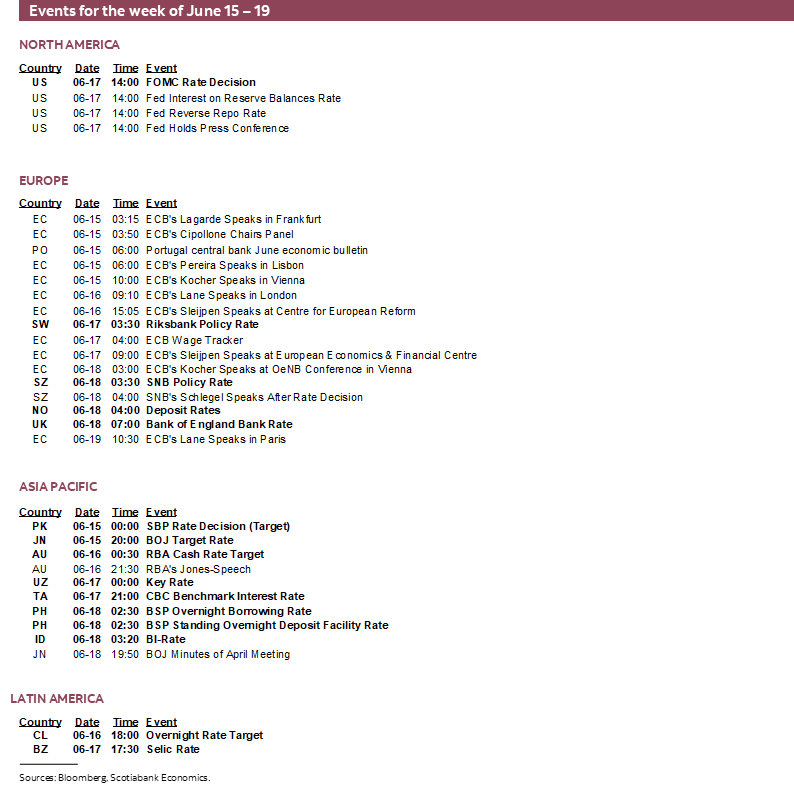

Next Week's Risk Dashboard

- Thirteen central banks to weigh in this week

- A possible MOU still questions what war achieved

- FOMC preview — Warsh puts his stamp on the Fed

- A high bar for Fed hikes, future cut more likely

- BoJ — The show must go on

- BoE — a high bar to hike

- RBA — Might have done enough

- Riksbank — still more patient than markets?

- Norges Bank — that’s all ya got?

- SNB — Stuck at the bottom

- BCCh — Likely to hold

- BI — A continued emergency

- BSP — Soaring inflation begets more tightening

- BCB — The war interrupted cut plans

- CBCT — No urgency

- Russian central bank — Another cut

- Global macro

- Juneteenth US holiday Friday

Chart of the Week

The week’s prime focus will be the baker’s dozen of central bank decisions that are on the docket even after trimming a few tiny ones. There could be more flips and flops across the cacophony of calls than you’d expect from a World Cup soccer match. I’ll focus mainly upon the Federal Reserve which could be a turning point in multiple respects. The reprieve for US market participants will be Friday’s ‘Juneteenth’ market closures.

A secondary focus will be whether a deal of some sort emerges between the US and Iran as soon as this weekend or into the otherwise fractured G7 meetings from Monday to Wednesday in the French Alps town of Évian-les-Bains by the Swiss border. An MOU to enter fuller negotiations accompanied by limited commitments appears to be more likely than any actual peace agreement but it awaits the Supreme Leader Khamenei and there have been countless false dawns to date.

Media reports as this publication is being finalized indicate that the scope of the MOU is limited but both sides spent Friday conflicting on the details if not the spirit. It may include a 60-day ceasefire extension including in Lebanon but lacking clarity on whether Israel agrees, an agreement to enter into negotiations on Iran’s enriched uranium stocks and nuclear program, and a vague Scout’s honour pledge by Iran to never acquire a nuclear weapon although with no apparent teeth. There are conflicting accounts of how open the Strait of Hormuz would become, with the US side claiming it would be fully open without tolls and a lifting of the US blockade, while Iran’s foreign ministry rejects restoring the Strait to pre-war levels while nevertheless claiming that an agreement has never been closer which may be a low bar. Details like unfreezing some Iranian assets, compensation to Iran, and the scope of sanctions relief to allow Iran to sell its burgeoning supply of oil in storage are unclear. All the while Israel’s Defence Minister threatened unilateral action to curb Iran’s nuclear program.

In short, we need to see the full scope of any MOU and that only restarts the clock on fuller negotiations that have failed many times to date. In my opinion, Iran would be getting more out of any such MOU than the US would get and this reflects the US administration’s desire to stand down. It’s unclear what the US may have achieved if the Iranian regime stays in place, hard guarantees around the nuclear program are not achieved, enriched uranium stockpiles are not removed, and risks surrounding transit through the Strait remain while relations across countries throughout the Middle East are in tatters.

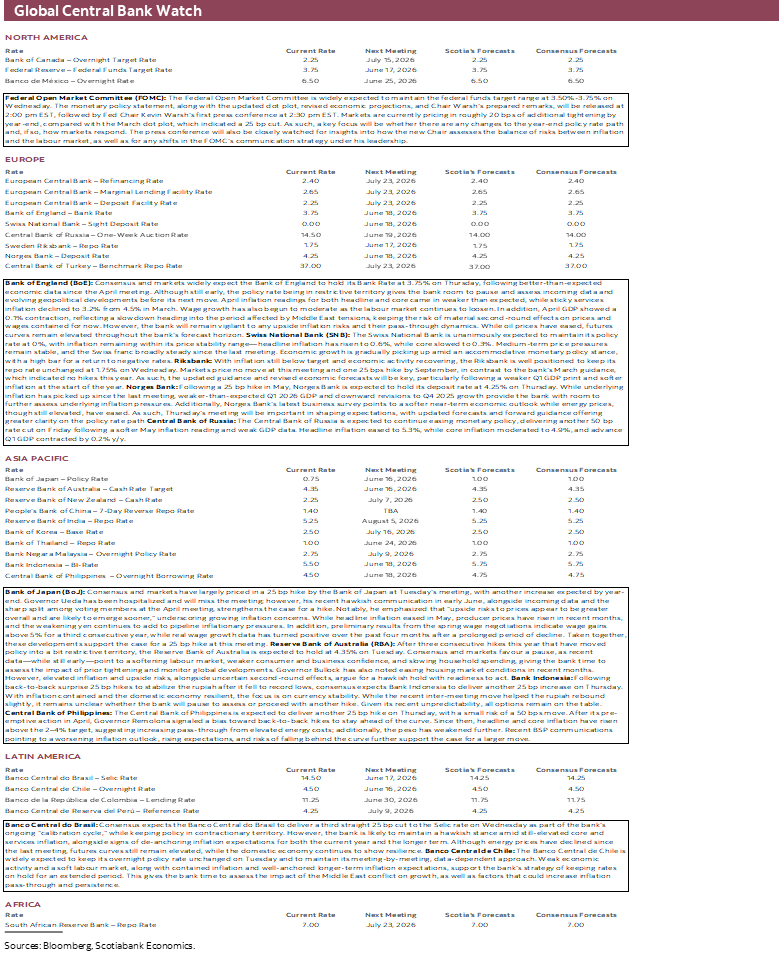

FOMC—WARSH’S GRAND ENTRANCE

Chair Warsh’s first meeting unfolds on Tuesday and Wednesday. Wednesday’s summary statement (2pmET) will be accompanied by the Summary of Economic Projections (SEP) followed by the press conference that starts at 2:30pmET. No policy changes are expected at this meeting but that’s not the same as saying you shouldn’t expect some sparks to fly. In fact, I expect the broad message coming out of this round of communications will be to prepare forecasters and markets to work harder than under the spoon-fed Powell era which is something we should relish more than lamenting what may be lost. A full pivot back to the Greenspan era is unlikely if not impossible, but a relatively more opaque Federal Reserve is likely forthcoming in a way that many market participants and Fed watchers cannot relate to if their experience set is more confined to the Powell and perhaps Yellen and Bernanke eras. With less transparency may come more volatility.

Forward Guidance Will be Gone

I expect the line that references “the extent and timing” of further policy changes will be entirely omitted. This has been alluded to by Fed officials and would be a sensible way of appeasing Warsh’s opposition to providing forward guidance and simultaneously pleasing the Committee’s hawks that are uncomfortable with still signalling a cutting bias at this point. It should not be taken as a tee-up for a hike bias. Instead of telling you what the FOMC is going to do at the next and subsequent meetings, we will all need to do more of our homework.

Other Statement Changes

Is it still fair to note that ‘economic activity has been expanding at a solid pace”? The economy grew by just ½% q/q SAAR in Q4 and 1½% in Q1. I’d say so, when looking at the details behind what drove underlying momentum in both quarters, but peak growth is still behind the US.

Is it still true that the Committee believes “job gains have remained low”? Payrolls grew by 214k in March, 179k in April and 172k in May including the effects of revisions. That’s likely above estimates of breakeven rates of job gains.

They could still cite the fact that the unemployment rate “has been little changed in recent months” as it has stayed at 4.3% for three straight months. Then again, it’s derived from the noisier household survey that has been shedding a very different trend in overall employment year-to-date than nonfarm.

Will Warsh seek to tweak “Inflation is elevated”? The Committee would have to agree, but his argument in favour of trimmed mean PCE could invite a modification.

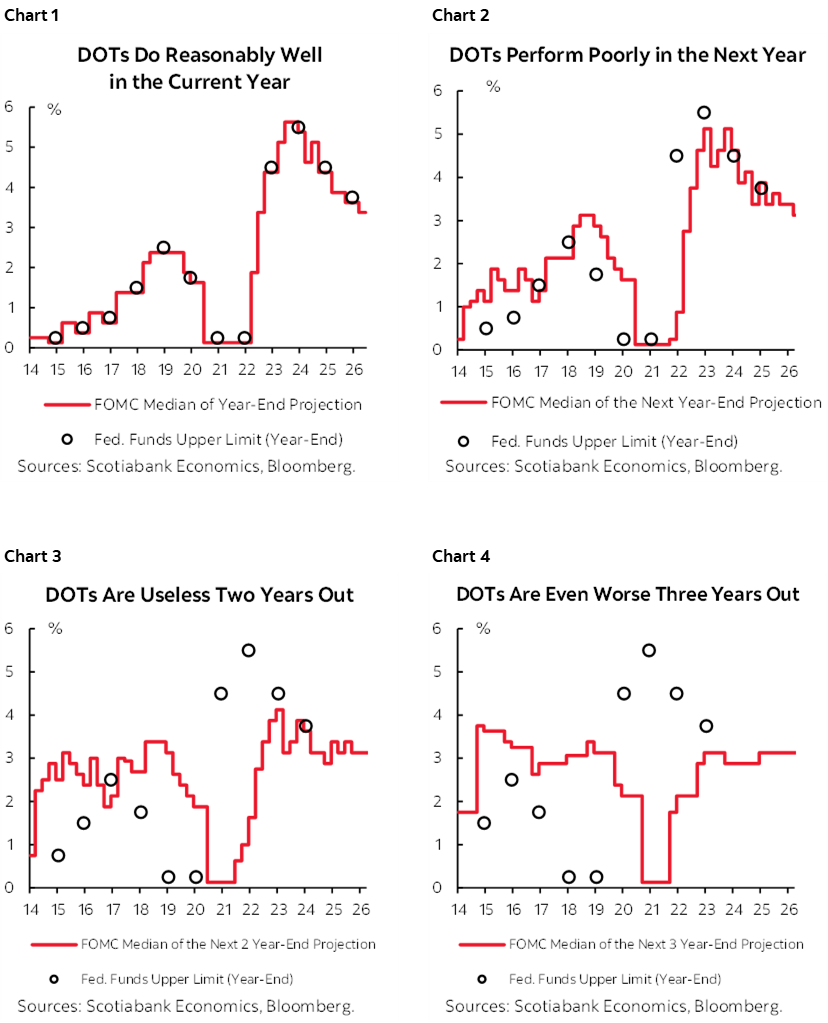

Dot Plot on Life Support?

I’m unsure what to expect for the dot plot at this meeting but watch for signs that it’s on the way out. It’s probably too late to cancel it without preparing markets somewhat in advance. It’s possible that Warsh’s opposition to forward guidance leads him to withhold his own dots and hence expectations for where the policy rate is going. Instead of 19 dots, there could be at least one missing in each dot—a rather vital one at that! The effect could dilute the usefulness of the dots and essentially set it up to be axed.

This makes some commentators nervous that they’ll be missing something important. Not this one. The Fed’s dots are not terribly helpful in any event. Charts 1–4 depict the track record of the median Committee projection for the policy rate relative to what actually happens across different time periods. The dots become more useful in-year and later in the year at that, but are of relatively little use as a guide beyond a very limited horizon. Put simply, the FOMC doesn’t necessarily have any better idea what it may do in future than anyone else. It could be that the reason some oppose abandoning the dot plots is that they give the cottage industry of Fed-watchers more marketing material and something to hide behind in terms of their own forecasts.

Further, I have a lot of sympathy for the argument that being forced to commit to policy rate expectations well off into the unforeseeable future could entrap policy makers into a form of intellectual stasis, rigidly adherent to outdated views and applying confirmation bias.

Fewer Press Conferences?

The focus will quickly shift to the press conference which is still scheduled to occur although it may well be shorter than usual. It will be interesting to see whether it will have more of a dictation style than allowing the press to question him as openly and for as lengthy a time as under Powell. Personally, outside of major developments, I’ve long felt the pressers could easily be considerably shorter with a higher bar set on the press to ask higher quality, relevant and impactful questions. For that matter, you might reduce the number of journalists to include only ones that closely watch the Fed and understand the dos and don’ts of what applies to the scope of questioning.

Warsh has indicated a preference toward less frequent communication which might mean going back to holding press conferences only four times a year instead of Powell’s shift to every meeting. For that matter, a more ad hoc schedule driven by material developments could materialize.

Recall Warsh’s role in the Bank of England’s internal review of communications strategy when he quipped that “It is rare indeed that the economy changes so rapidly that adjustments to monetary policy are needed at four-week intervals” and his speech last year in which he stated “Fed leaders would be well-served to skip opportunities to share their latest musings.”

It may be ironic that the most important aspects of Wednesday’s communications could be delivered in the press conference that Warsh loathes doing so frequently.

Subcommittees?

We will be watching the press conference for signals about research programs and assignments given to subcommittees either soon or by signalling that such movement is afoot. One possibility is the creation of a subcommittee to explore alternative inflation measures. The Fed’s dual mandate is set by Congress, but there is wide latitude in terms of how to operationalize and implement it.

Another possibility is that Warsh may signal the establishment of a working group to explore communications plans. The style of the statement, the content, frequency and perhaps survival of the Summary of Economic Projections and its dot plot are each at stake.

A Different Inflation Measure?

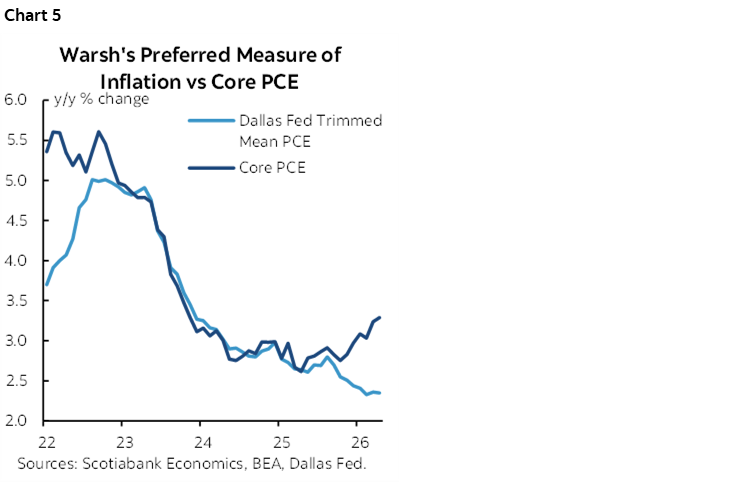

Warsh said during his Senate confirmation hearing in April that “The measures I prefer are looking at things that are called trimmed averages. What I’m most interested in is what’s the underlying inflation rate, not what’s the one-time change in prices because of a change in geopolitics or a change in beef.”

Enter chart 5. He has a point. The departure between the Fed’s traditionally main measure—core PCE inflation that removes only food and energy—versus the Dallas Fed’s trimmed mean PCE gauge is unusual in history. Core PCE inflation is running at 3.3% y/y and trending higher whereas the Dallas measure is at 2.35% y/y and trending lower.

How to square the circle on these competing measures? It’s possible that today’s inflation shock is more of a relative price change than an outburst of generalized inflation. Monetary policy shouldn’t necessarily chase relative price shocks. All prices cannot be controlled at once, but the central tendency of price pressures may be under greater control of monetary policy.

A caveat to this view is whether today’s wedge between the measures is temporary. For instance, while this harkens back to the unusual early days of the pandemic recovery, core PCE inflation turned higher before trimmed mean eventually followed suit back in 2021. In the GFC, core PCE turned lower earlier than trimmed mean.

Still, the notion of focusing upon central tendency price pressures is worth pursuing. Smaller central banks that were at the vanguard of explicit inflation-targeting regimes with quantified targets much earlier than the Fed have been employing such measures for quite a while. They include the Bank of Canada, RBNZ, and RBA. Several other central banks also reference trimmed mean inflation but on a lower frequency basis. A view on the superiority of such measures across these central banks is summarized here.

Warsh’s Views on Inflation—Tran….Temporary?

In addition to possibly arguing that underlying inflation is overstated by the Fed’s traditional PCE and core PCE measures, how is the new Fed Chair likely to view the outlook for inflation? It’s possible that he surprises dovishly.

Before turning to why, there are still some legit reasons to be concerned about US inflation. The economy remains in excess aggregate demand which tends to raise pricing power in a more capacity-constrained economy. Pass through of surging commodity prices may be at a nascent stage of development. Fiscal policy is in competition against inflation control. Supply chain turmoil may remain at an early stage, possibly passing on the first-round effects of tariffs but with protectionist policies spawning years of negative supply-side effects and less contestability to US producers. AI is inflationary in the short-term through the positive equity wealth effect on spending relative to its absence, through the investment surge, and through associated increases in prices for electricity, various electronic components, and in some cases commercial real estate prices.

That’s now. But monetary policy needs to be crafted for expected future conditions given its long and variable lagging effects on the economy.

Today’s inflation spurt in the US economy could be more tra….nope….let’s say temporary this time. I didn’t buy that in the pandemic but have more time for it today. The scope of damage to global supply chains is less severe than in the pandemic. Back then, demand had to be shrunk toward damaged supply but today’s supply side effects play the war’s effects against potential productivity surge partly driven by heavy tech investment. The overkill on stimulus measures is less acute, notwithstanding heavy surge-spending on defence and infrastructure in major economies. Fed policy is starting from a mildly restrictive point than coming out of the pandemic at the lower bound and by contrast to the ECB, BoC etc.

The surge across commodity prices may face limited pass through of a shorter-duration nature. A major reason for this view is how incomes and behaviour adjust.

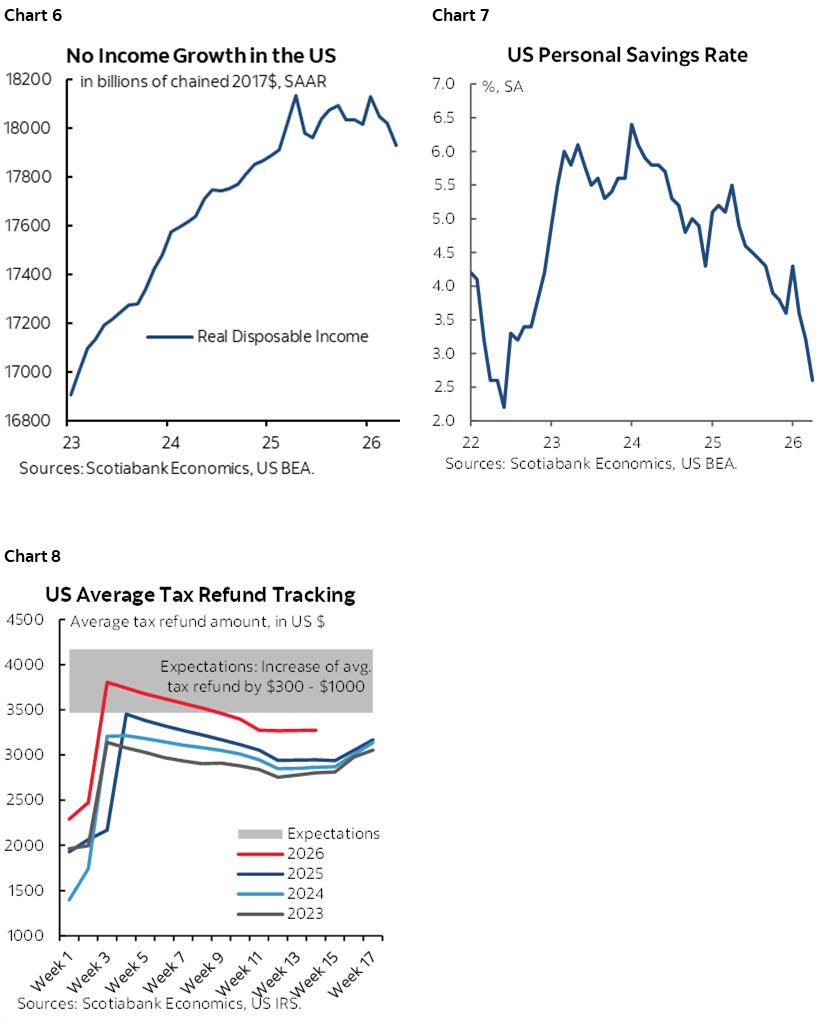

The US household sector has had basically no growth in inflation-adjusted incomes over about the past year-and-a-half (chart 6). That precedes the recent commodity shock. With nominal wage growth at only about 3½% y/y, real wages are likely to be squeezed further. This makes second-round effects on inflation less likely as consumers spent more upon what they must with limited offsets—groceries and energy—and less on other things. They are smoothing the effects by saving less but there is a limit to this (chart 7). It is part of our slowing growth narrative along with fiscal policy contributions to growth peaking this year albeit with lower than expected tax refunds (chart 8) and with investment ex-AI still falling. The US economy only grew by ½% q/q SAAR in Q4 and about 1½% in Q1 such that US economic resilience is an overstated narrative into a negative shock.

How behaviour adjusts is another US distinction relative to, say, Europe and even Canada. Only about 10% of US workers are unionized. Collective bargaining does not play the same role in wage setting exercises as those other regions where unionization is dominant in parts of Europe and where about one-third of Canadian workers are unionized. US labour markets clear more rapidly and what is closer to real time without as many knock-on effects of prices on wages.

Furthermore, US businesses routinely respond to cost shocks by doubling down on efficiency gains, offsetting cost reductions and productivity gains more so than elsewhere, thereby also limiting sustained inflation shocks.

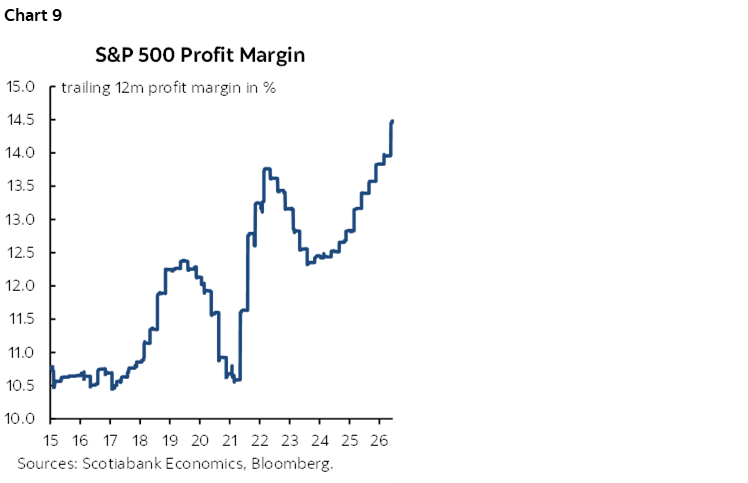

With profit margins still at elevated levels (chart 9), US companies could absorb some of the input price surge, but not all. It’s easier to pass on some of it—and hence crimp real wages—in the context of capacity pressures.

Warsh’s Views on Jobs—Likely More Cautious than Other Members

Key may be the FOMC’s views and Chair Warsh’s narrative on the outlook for the job market as well as their take on recent trends. Several Committee members have sounded encouraged by recent numbers.

In my opinion there is reason to be more guarded and I’ll closely watch Warsh’s views to see if they line up.

- If economic growth slows as we expect, then there should be correlated slowing in employment growth. This is an ‘Okun’s Law’ approach that is no law but argues the two should be correlated over time;

- recent numbers have been overstated by FIFA World Cup hiring in May and probably again in June before this effect reverses in August. I argued this point several weeks ago as part of the reason for going high in consensus on May payrolls.

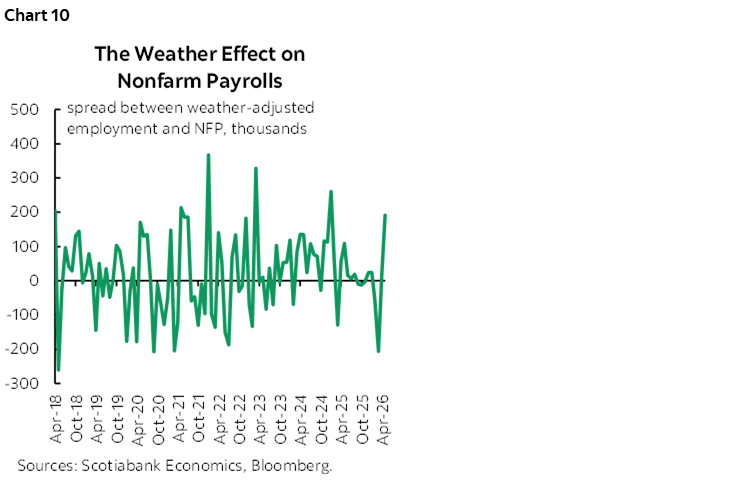

- Weather has been wreaking havoc with payrolls this year (chart 10). More evidence on the trend is needed.

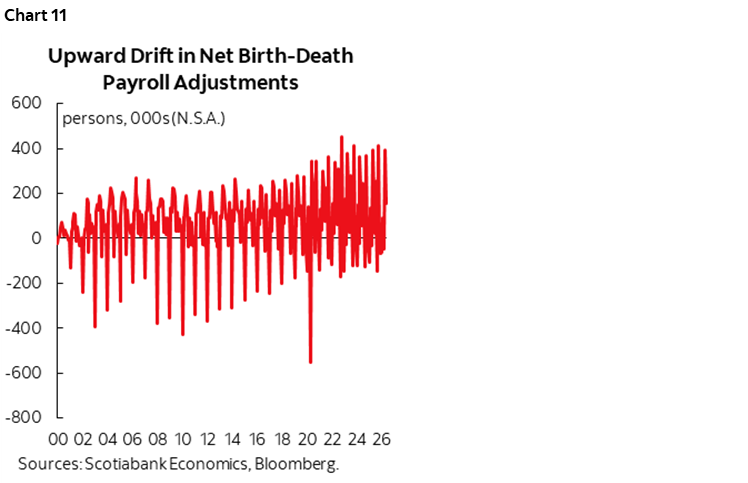

- annual benchmarking revisions in September—about one-week before that month’s FOMC meeting—should be approached with care. There have been harsh downward revisions to March payroll levels and on a monthly basis over the prior year in each of the past two years partly because of birth-death model overcounting of job creation. The persistent upward drift in birth-death model additions to nonfarm payrolls makes us concerned that this model-based component of the change in nonfarm payrolls could be overcounting payrolls again (chart 11).

And then there is the next elephant in the room.

AI’s Influences

As the father of a teenaged boy who excels in academics and other pursuits I’m nevertheless concerned about the formative years of his generation’s years in the workplace.

I’m no Luddite and believe that innovation waves can impact both supply and demand over time, but the key uncertainty is relative magnitudes and timing on both sides of the balance.

Whole swaths of employability are at risk. At risk are both so-called blue- and white-collar jobs that merely take information, apply routine procedures and rules, and then establish routinized output. Many such forms of employment are early stage in one’s career.

Software programmers are now up against massive efficiency improvements in terms of AI’s ability to generate code which could dampen the longstanding pattern by which Silicon Valley employers scoop up swaths of recent graduates of computer science, engineering and math programs from the leading schools. Investment banking associates that work punitively long hours may be ripe for automation. I can use ChatGPT to develop a fully detailed travel itinerary for a family vacation with no help from a travel agent that will be forced to elevate service and target niches. Insurance adjusters, call centre employees, administrators, basic accounting services, radiologists, back office operations at finance companies etc are among the jobs that make up large shares of the workforce that are likely to be vulnerable.

Against this will be jobs created around new products and technologies that could lead to better outcomes. My bias is this arrives at a slower pace.

AI’s uncertainties require FOMC members to be circumspect, careful and open-minded toward the consequences. Don’t judge the future of employment using last month’s nonfarm report. Be careful not to wait too long for the perfect evidence. Be nimble. A neutral bias that is open to potential front-loading of easing into such a shock may have merit. A nasty employment shock could create sharply disinflationary pressures that merit a lower policy rate with monetary policy incapable of offsetting the effects but instead focused upon mitigating them.

At a minimum, set an extraordinarily high bar against further tightening and a lower bar in favour of potential insurance cuts. If the job market’s risks unfold the way I fear, then the Fed wouldn’t wish to react too late.

Forecasts

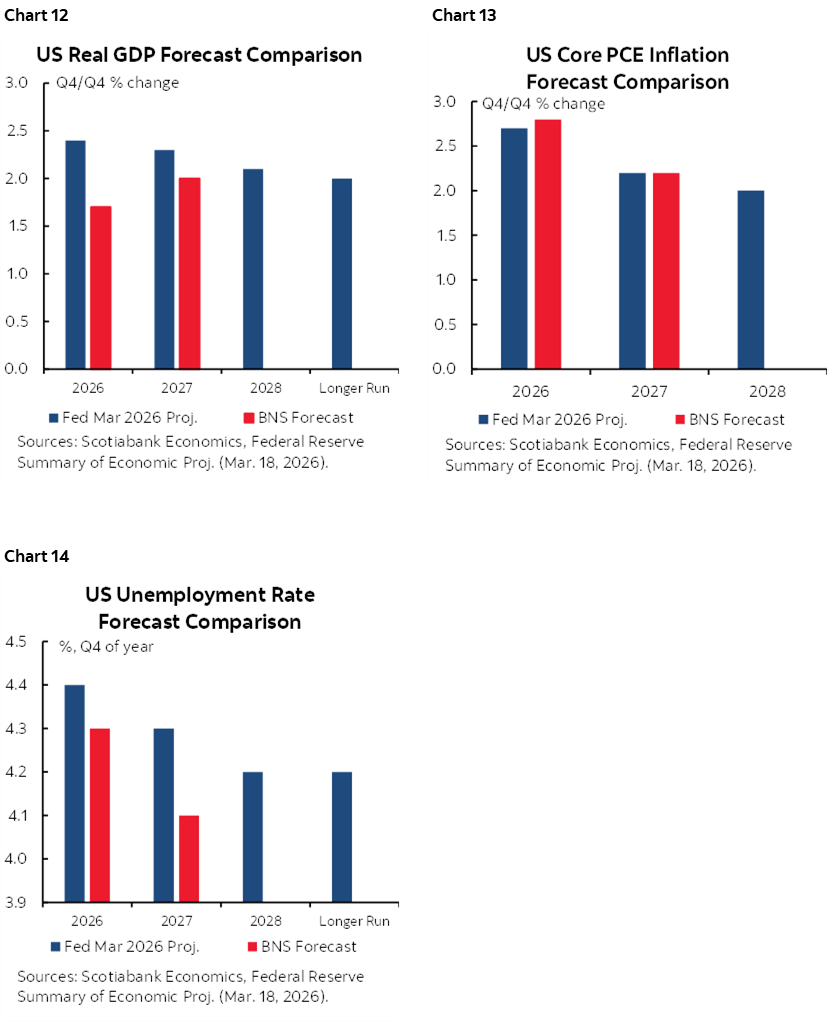

All of which boils down to how the FOMC’s forecasts may change. Charts 12–14 provide an idea of where we currently stand on projections relative to the Committee’s last attempt back in March. Growth may be revised down, inflation could remain at least as high, while the unemployment rate could be revised lower.

The Balance Sheet

Markets will also have a close eye on how Warsh views balance sheet policy. He has previously expressed opposition to serial QE, and openness to shrinking the balance sheet. His rationale is not just rooted in a desire to shrink the Fed’s role in capital markets.

He has argued that an expanding balance sheet has disproportionately benefited well-heeled investors and that shrinking it while reducing the policy rate could allow monetary policy to seep through the cracks in the plumbing with greater efficacy toward more households and businesses on mainstreet. The implied view is in favour of steepeners. Here is a direct quote of his:

“The Fed’s bloated balance sheet…can be reduced significantly. That largesse can be redeployed in the form of lower interest rates to support households and small and medium-size businesses.”

There is some merit to this in my opinion, but it may be overridden by the discipline that markets may apply. Reducing the balance sheet would likely drive lower reserves in the banking system as the Fed puts net supply of Treasuries back into markets with a concomitant liquidity reversal via the interplay between the Fed’s balance sheet and the banking system’s balance sheet. The Fed’s ample reserves framework has leaned toward padding banking system liquidity and not pushing it to such a low point as to ignite funding market strains. An abrupt pivot toward shrinking the balance sheet could reignite such funding strains, cause market instability, and backfire on the Fed through propelling measures like SOFR and other short-term relative rate spreads higher. A funding and liquidity crisis should not be entertained by the Fed.

It’s possible that Warsh courts a discussion on the interplay between changes in several of the Fed’s policy tools. He could argue that lower short-term rates can allay funding market strains stemming from shrinking the balance sheets; spreads could widen, but all-in yields may not. This is highly uncertain, but there may be limited room for initial experimentation.

Other Matters

Whatever the outcomes, preserving Fed independence is job #1 for Warsh. The FOMC is well situated to withstand attacks from the administration but needs its leader to be the source of the rallying cry. The 5-year extensions given to regional Presidents and no current vacancies put it in good position to conduct appropriate policy.

Moral hazard should not dominate FOMC thinking, nor should they be oblivious to it. Many of the Trump administration’s policies carry pernicious effects that have slowed economic growth. I’ve argued this for a long time and The Economist’s recent piece took up the argument. Monetary easing that counters negative effects of foolish trade policies, overly restrictive immigration policies, the deeply incorrect logic behind the ‘maga’ victim hypothesis behind what drives the twin fiscal and current account deficits, and persistent instability and uncertainty could invite more such conduct. It could be that the Fed needs to be the adult in the room.

There is also the question of former Chair and now Governor Powell’s future. We’re unlikely to learn more about it this week, but I still think it makes sense for Powell to stay on the Board at least until the new Congress convenes in January. That way if the Democrats take the Senate, there may be a more balanced replacement put forth than if Powell were to leave beforehand only for President Trump to reappoint Stephen Miran. While Powell has said he intends to play a backseat role, his vote and voice could be an important moderating presence. He is also perfectly correct to stay for as long as the administration continues to undermine Fed independence through trumped up charges.

BOJ—THE SHOW MUST GO ON

Consensus unanimously expects the Bank of Japan to raise its unsecured overnight call rate by 25bps on Tuesday. Markets are priced for such an outcome. Governor Ueda is hospitalized and will skip this meeting which could impair or limit the overall tone of any guidance that is provided. Furthermore, the BoJ is between forecast rounds in May and July which puts more of the focus upon Ueda’s expected return alongside fresh forecasts at the July 31st meeting. Markets are presently pricing a hold at that meeting and one more hike by year-end.

BANK OF ENGLAND—A HIGH BAR TO HIKE

Like the Federal Reserve, the Bank of England is judged to be in restrictive territory but unlike, say, the ECB or the Bank of Canada. It can take some time to evaluate second round effects, having halted its easing campaign after last December’s cut. Consensus unanimously expects a hold and markets are priced for one. Markets are pricing a modest chance at a hike in late July, more of a chance in September and a full hike by November.

The BoE is between forecast rounds in April and July. MPC members are not indicating an immediate appetite for policy tightening, while views on forward risks are mixed.

Governor Bailey has described inflation as driven “pretty much entirely” by the war and has stated the following:

“Given the context of softness in the real economy and uncertainty around the scale and duration of the shock, tolerating temporarily above target inflation to provide some support for the real economy is an appropriate way to approach the trade-off.”

Others, like Alan Taylor, go further: “Interest rates don’t need to go higher because they’re quite restrictive at the moment.” Still, there are members who are more uncertain, preferring instead to evaluate inflation risk as a function of how long the conflict and its effects persist.

In short, no action for now, but stay tuned over H2.

RBA—MIGHT HAVE DONE ENOUGH

Tuesday’s decision is priced to hold the cash target rate at 4.35% and consensus is basically unanimous. Markets only have just over half of one more quarter-point hike priced over the 2026–27 horizon, anchored around early next year. There is a general sense that policy fine tuning may have done enough via 75bps of hikes this year. Governor Bullock has noted the softening tone in the housing market “that partly reflects tighter monetary policy.”

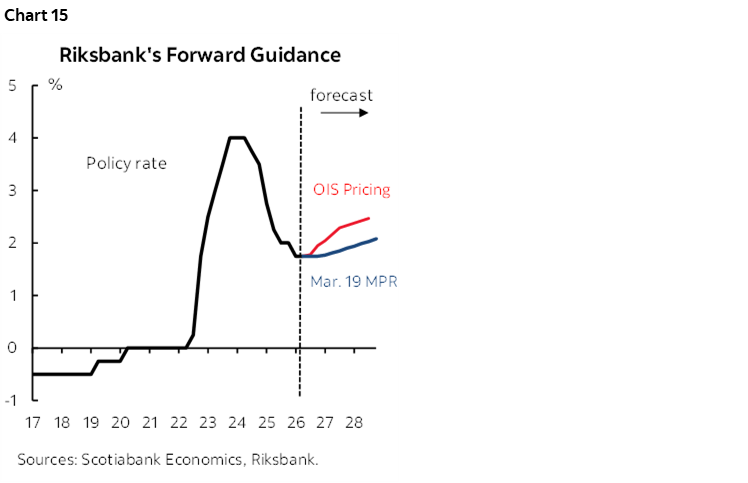

RIKSBANK—REFRESHED GUIDANCE

Consensus unanimously expects Sweden’s central bank to leave its policy rate unchanged at 1.75% again on Wednesday. It has been on hold since last September. Markets are fully priced for a hold. Key will be whether updated explicit forward guidance continues to point toward greater patience than priced into markets (chart 15).

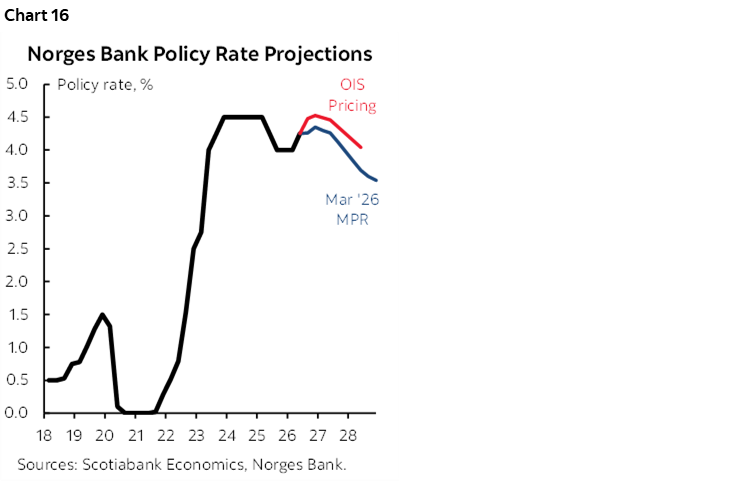

NORGES BANK—ARE WE DONE?

Norway’s central bank hiked at the May meeting but is expected to hold at a deposit rate of 4.25% on Thursday. Markets are mostly priced for a hold and don’t foresee a further hike until later this year. Whether updated explicit forward guidance continues to suggest low odds of material further tightening will be key, alongside more dubious longer-run forward guidance that points to future easing (chart 16).

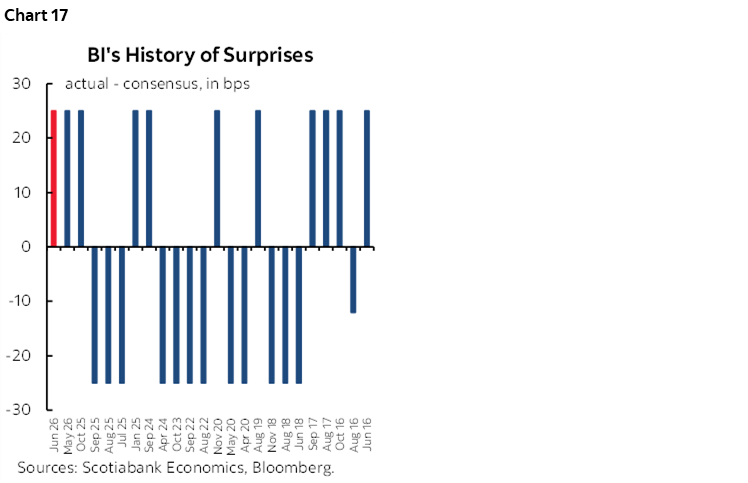

BANK INDONESIA—CHICKEN AND EGG

Why deliver an unscheduled emergency rate hike as Bank Indonesia did on June 9th if you’re not planning on following up with another one this Thursday? Good question! It’s probably why fourteen within consensus expect another 25bps hike, another two think BI could upside with a 50bps hike and two others say nah, they’ll skip this time.

This is the wild west of central banking, only in the east. BI has a strong proclivity toward surprising everyone (chart 17). It may be more encouraged by the stabilization of the rupiah since its emergency hike which allays some concern about stability matters. Then again, rupiah stability is probably conditioned upon a follow-up hike being delivered which means BI may not wish to court the risk of a setback by pausing.

BSP—JUST ONE WON’T CUT IT

Here’s another case of whether you can just take one chip out of the bag. The central bank of the Philippines hiked by 25bps back on April 23rd and is widely expected to hike again on Thursday. Since having hiked, the peso has depreciated by a further 2% against the dollar but has recently stabilized. A question is whether 25 is enough this time, as a fair portion of consensus expects the hike to be upsized.

Key is that while CPI inflation for May landed materially softer than expected, it is still running at well over twice the 3% inflation target and well up from the 1.8% rate at the end of last year. Central bank language signalled a tightening bias after the numbers when it said it “will take necessary actions to ensure inflation returns to its 3% target.”

BCCH—THE CORE OF THE MATTER

Banco Central de Chile is widely expected to hold its policy overnight rate at 4.5% on Tuesday. Inflation at 3.9% y/y is mostly driven by commodities thus far, as core inflation is tamer at about 2.3%.

BRAZILIAN CENTRAL BANK—PLANS INTERRUPTED

Brazil’s central bank is widely expected to cut its Selic rate by another 25bps to 14.25% on Wednesday afternoon following the Federal Reserve. This would be the third cut since March after a prolonged period of restrictiveness. Expect guidance to be measured and data dependent as the effects of the inflation shock work through. Headline CPI climbed to 4.7% y/y in May with trimmed inflation performing identically. This is why markets foresee only a modest additional chance at easing thereafter.

CBCT—NO URGENCY

Most economists expect Taiwan’s central bank to hold its benchmark discount rate at 2% on Thursday with a minority thinking that a hike could be in the cards. Inflation has moved up a bit, but remains low at 2.2% y/y with core inflation performing similarly. The Taiwan dollar has been holding reasonably steady this year under a managed peg regime to the USD.

SNB—STUCK AT THE BOTTOM

The Swiss National Bank will very likely leave its policy rate unchanged at 0% on Thursday. The Swiss franc’s relative stability, low inflation of 0.6% y/y with core CPI at 0.3% and high reticence to return to negative territory give it no sense of urgency to change.

RUSSIAN CENTRAL BANK—ANOTHER CUT

Most forecasters expect Russia’s central bank to cut by 50bps to 14% on Friday and that’s about as much space as we’d ever give to Putin’s central bank here.

GLOBAL MACRO

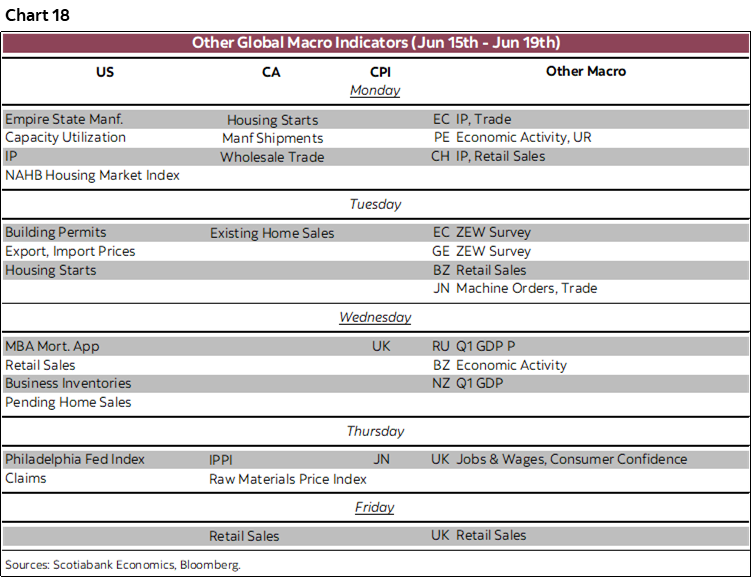

The week’s focus will be upon central banks so I’ll leave discussion of economic indicators to daily notes over the coming week. Chart 18 summarizes the measures by country and day.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.