Next Week's Risk Dashboard

- June FOMC is still ‘live’

- The BoC needs to hike…

- …as its conditions have been violated

- Canadian jobs, wages and productivity

- Treasury to replenish cash account

- RBA decision resembles the BoC’s

- RBI to hold, forward guidance key

- BCRP likely to extend hold

- Global inflation updates

- China’s nonexistent inflation

- Other global indicators

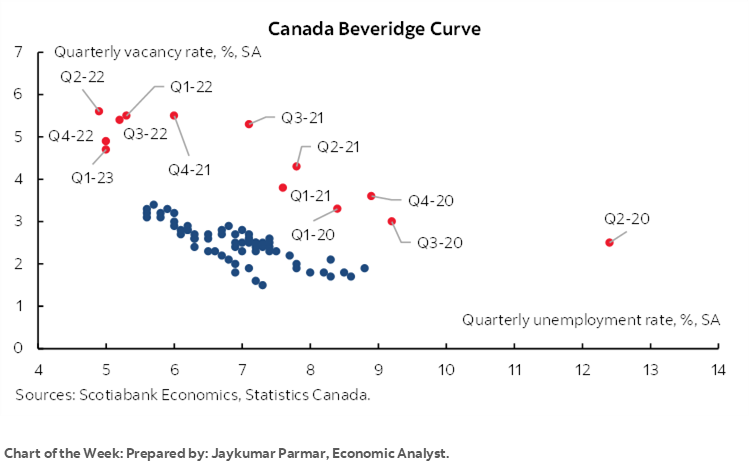

Chart of the Week

A key issue overhanging global financial markets is whether the Federal Reserve is done hiking the fed funds policy rate. As the FOMC goes into communications blackout, we are unlikely to receive any further guidance from key Federal Reserve officials on what to expect into the June 14th decision unless they do so via preferred media outlets during blackout which they have done in the past. The likely silence will keep markets in limbo after a strong payrolls report that keeps the door open to further tightening. The next test may be US CPI on day 1 of the two-day June FOMC meeting.

The core case for the Fed to be done hangs on interpretations of Fed-speak starting with Chair Powell’s May 19th remarks and culminating in this past week’s comments by other officials. Some have taken the suite of those remarks—and particularly the Chair’s—as a clear sign they will pause in June. That may be applying too much literary licence to what they actually said.

Recall that on the 19th, Powell said the following:

“Having come this far, we can afford to look at the data and the evolving outlook to make careful assessments.”

He also noted that no decision had been made about the June meeting’s outcome and that they will take decisions one at a time depending upon the evolution of data and events like the debt ceiling agreement’s passage since those remarks were offered. What I heard the Fed chair say is quite literally that they will “look at the data” which to me sounds more like a shift away from providing explicit advance guidance that they will definitely hike toward taking it one meeting at a time. After getting another very strong payrolls report (here), it’s now onto core CPI.

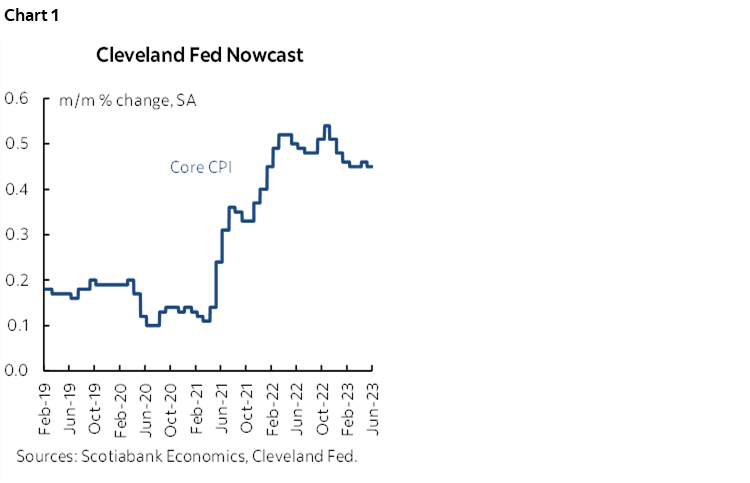

On that note, the Cleveland Fed’s core CPI ‘nowcast’ is leaning toward another hot print for May of about 0.5% m/m SA (chart 1). Should core CPI turn in a hot performance then it may be difficult for the FOMC to resist another hike. Also bear in mind that when Chair Powell spoke he was concerned about political developments around the debt ceiling and the risk of market dysfunction that has now been swept aside by the highly predictable passage of the agreement in both chambers of Congress.

Markets also took comments from Governor—soon to be Vice Chair—Jefferson as supportive of a June pause. Funny, but here too what I heard him say doesn’t match the market narrative. Jefferson said:

“A decision to hold our policy rate constant at a coming meeting should not be interpreted to mean that we have reached the peak rate for this cycle.”

Note the difference between signalling a potential pause “at a coming meeting” versus, say, “at the next meeting” or “soon” which would have been a June pause signal consistent with language they’ve tended to use to communicate a greater sense of urgency.

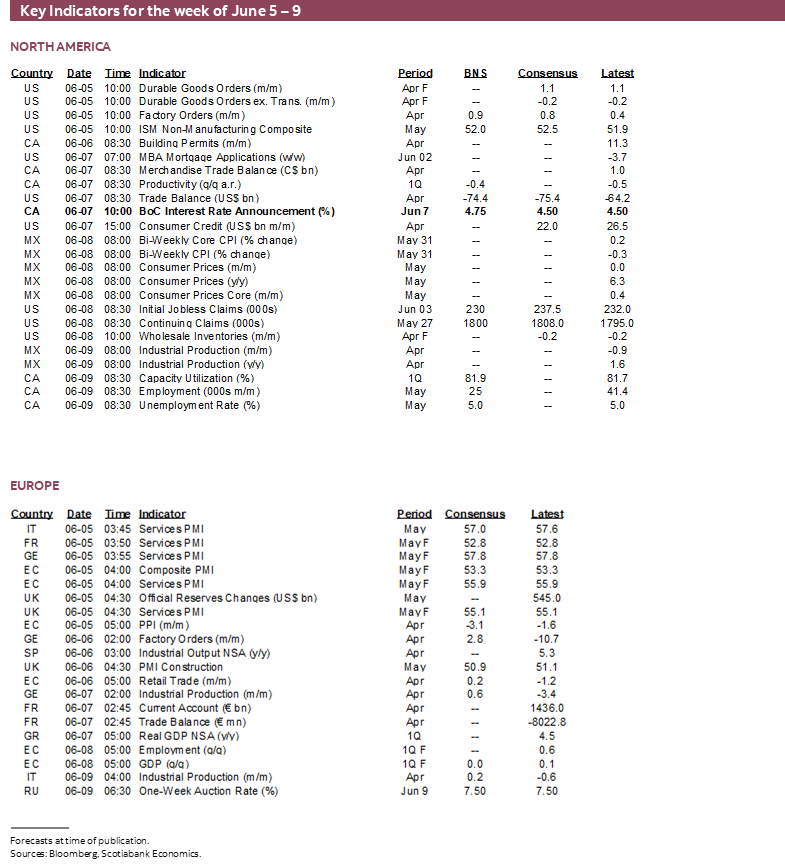

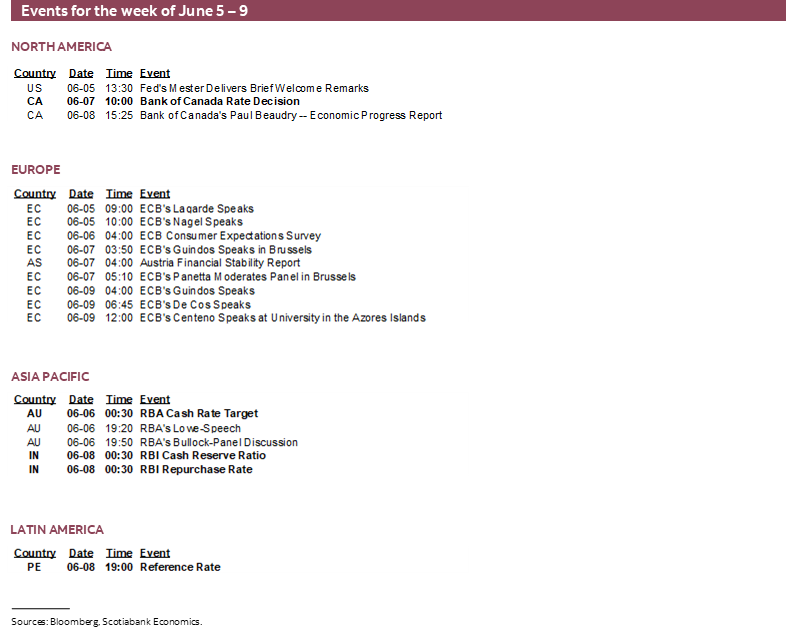

This coming week will offer plenty of time for markets to consider these matters absent much by way of US calendar-based developments. For that matter, we can say the same about much of the world with the exception of the week’s strong focus upon Canada.

BANK OF CANADA—THE CONDITIONS HAVE BEEN VIOLATED

The Bank of Canada delivers a policy rate decision on Wednesday that will be delivered via a statement sans either forecasts or press conference. This will be followed the next day by outgoing Deputy Governor Beaudry’s turn to deliver the customary economic progress report that usually follows non-MPR meetings. Beaudry will leave the BoC at the end of July and so this will be his second last policy round of involvement in the decision-making process.

Scotia Economics expects a 25bps rate hike at this meeting accompanied by continued guidance that leaves the door open to further tightening by largely retaining something either identical or very similar to the final paragraph’s guidance in recent statements that has said:

“Governing Council continues to assess whether monetary policy is sufficiently restrictive to relieve price pressures and remains prepared to raise the policy rate further if needed to return inflation to the 2% target.”

If the BoC does not hike this week, then the effect of hawkish guidance on the front-end of the Canada rates curve is likely to be tantamount to a hike as an imperfect substitute toward buying time into July.

To a degree it has been mission accomplished with my view on Canadian shorter-term borrowing costs over recent months. The two-year Government of Canada bond yield had sunk to about 3.4% in March when aggressive rate cuts were being priced for this year starting by now but has since risen to about 4.3% now. Guidance against policy easing in favour of a hike bias throughout this period has driven excess returns if adhered to. Guidance in favour of pricing significant probability of a rate hike(s) by June/July has also generally worked out; June OIS pricing has swung from pricing a large cut by this coming meeting back in March to a decent shot at a hike while July OIS pricing has swung from large cumulative cuts priced in March toward about a full quarter point hike priced now. All of the rest of consensus throughout this period of time was in disbelief toward the prospects of renewed rate hikes until very recently and starting around mid-May.

The BoC has been fairly clear that its conditional hold since January relied upon developments conforming to its expectations. That clearly has not been the case.

GDP growth: The 3.1% surprise in Q1 exceeded the BoC’s 2.3% forecast (here) and the early read on the Scotia Economics ‘nowcast’ for Q2 GDP growth is pointing toward 2 ½% versus the BoC’s forecast for 1% Q2 growth. This indicates that the economy continues to push further into excess demand conditions in contrast to the BoC’s forecast for a return toward potential growth over H1 or lower. What’s more is that the details to the growth figures continue to point toward robust growth in consumer spending—including the most interest-sensitive types—and against fears that higher rates would take down spending. The BoC may have to revise its growth forecasts higher for the full year.

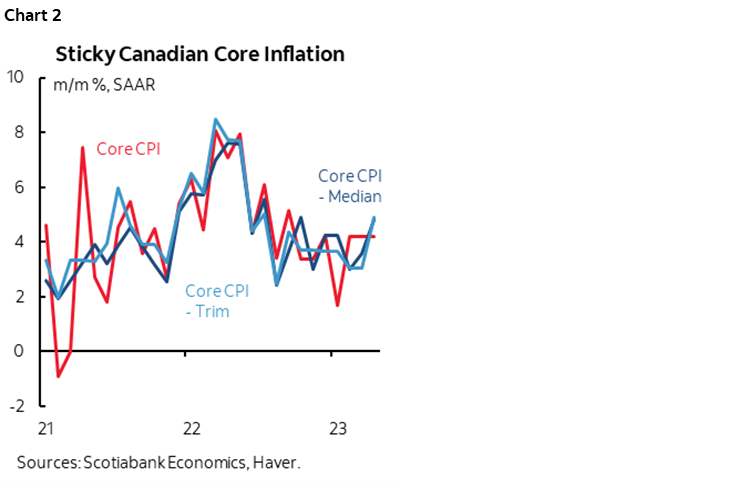

Inflation: Strong H1 growth will only amplify Governor Macklem’s concerns about the next leg toward the 2% inflation target being harder to achieve than the first moves. As chart 2 demonstrates, the correct way to look at core inflation as the operational guide to achieving 2% headline inflation is on a month-over-month annualized and seasonally adjusted basis. All of the main measures are running at 4%+ as they jumped higher in April which is not something the BoC can afford to ignore. The only period of marked improvement was over 2022H1 and since then these measures have been moving sideways at remarkably sticky rates notwithstanding the fact it has already been ~20 months since bond market tightening began in earnest and in anticipation of policy rate hikes.

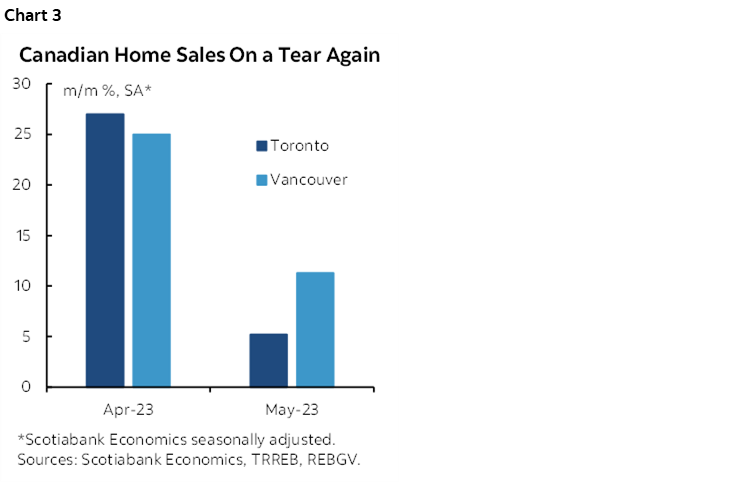

Housing: The BoC would not hike for housing alone and is principally focused upon its 2% inflation target. That doesn’t mean that it wouldn’t consider a stronger case for hiking due to housing market developments. Macklem guided in April that the BoC expected a rebound in housing in the second half of the year, yet, as chart 3 vividly depicts, that is already happening. Housing matters in that if it were to feed stronger housing investment with spillover effects upon consumption then it could drive a more resilient economy and further thwart the desired push toward opening up disinflationary slack in the economy. Housing also matters from the standpoint of driving stability concerns. With commercial and industrial real estate conditions on robust terms, a pressured office market is a relatively small consideration against the emerging rebound of residential real estate. The stability risks of allowing this to get out of hand once more outweigh the downside risks that an over-leveraged minority tail of households pose to the outlook. In my opinion, the BoC has played a role in past bouts of runaway gains in house prices with rates that were too low for too long and it is very much within its scope of influence to do something about it in the context of its overall inflation forecasting framework. It cannot count upon other policy levers to do so since, to be totally candid, the country’s policymakers get an ‘F’ for consistently applying excess stimulus to housing demand while paying short shrift to the supply side of the picture. Any further delay in raising the policy rate would only fan housing imbalances to a greater degree and the BoC would be allowing one of the most interest-sensitive sectors that used to be a drag on growth return as a significant driver of growth and with that inflationary pressures.

What is clear is that the BoC faces no need to have to set up a hike this week. It has already done so in spades while making it clear that if its conditions are violated then it stands prepared to return with additional hikes. Macklem has warned that they considered a hike in April and we’ve since taken down more hawkish developments at home and abroad (eg. debt ceiling, regional banks). He has warned that they are concerned about the next leg down to 2% being a tougher battle. He has warned they are more concerned about upside risks to inflation than downside risks. He has delivered such messages on multiple occasions including his April press conference, his IMF media roundtable, his two rounds of testimony to parliamentary committees with SDG Rogers and in various media appearances. If markets haven’t gotten the memo by now, then another month spent hammering away at the same themes won’t matter. This is also why the decision does not need to be delivered by the Governor himself since he has basically already primed the path in advance.

Nevertheless, time is very much of the essence here. With each passing month that households, businesses and governments bear witness to out of control inflation, strong job markets, strong housing markets and a robust economy, faith in the BoC’s ability to control inflation expectations will suffer and they may never be able to get inflation under control. Decisive action should have already been delivered, but further delay until July only to disappear for August holidays would lose precious time to send a concrete message.

In my view, the greatest risk to the economy, to inflation, and to the stability of the financial system would be a BoC that turned a blind eye to these developments instead of hiking this week and teeing up a bias toward another.

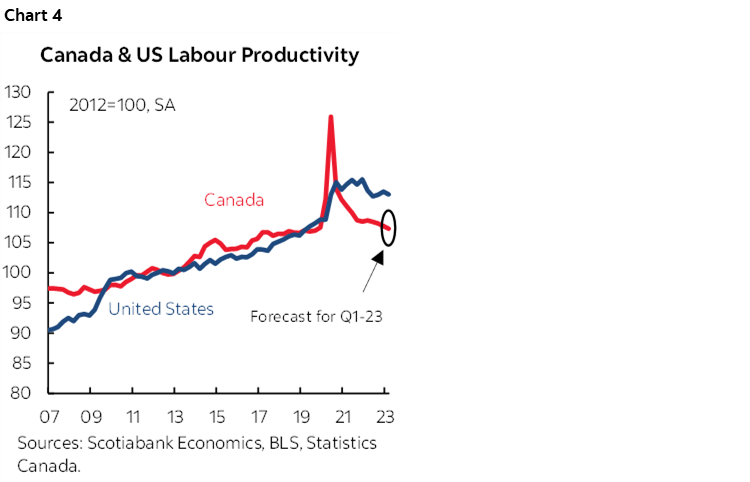

CANADIAN JOBS—MORE BODIES & HOURS, LESS PRODUCTIVITY

Canada updates jobs and wages for May on Friday and productivity figures for Q1 two days before. The estimates I’ve gone with imply continued resilience amid labour-driven cost pressures in part owing to poor productivity performance.

None of the releases will impact the Bank of Canada’s decision on Wednesday morning. The statement is ready to send before the official release of the productivity figures and the BoC would have a decent idea of what to expect for a reading that is only a part of the picture, while the jobs figures arrive two days later and the BoC would be agnostic toward the uncertainty around a single print. If anything, this round of job figures and the next one on July 7th could be influential to the July 12th BoC decision and the accompanying updated projections.

Productivity probably fell again in Q1 with an estimated drop of 0.4% q/q, or 1.8% q/q annualized. This decline is expected despite strong GDP growth of 3.1% during the first quarter because hours worked increased by more than GDP. Hours were up by 1.2% q/q SA, or 5% q/q at an annualized rate. To achieve higher output, the Canadian economy relied upon working more hours to counter an ongoing productivity challenge (chart 4).

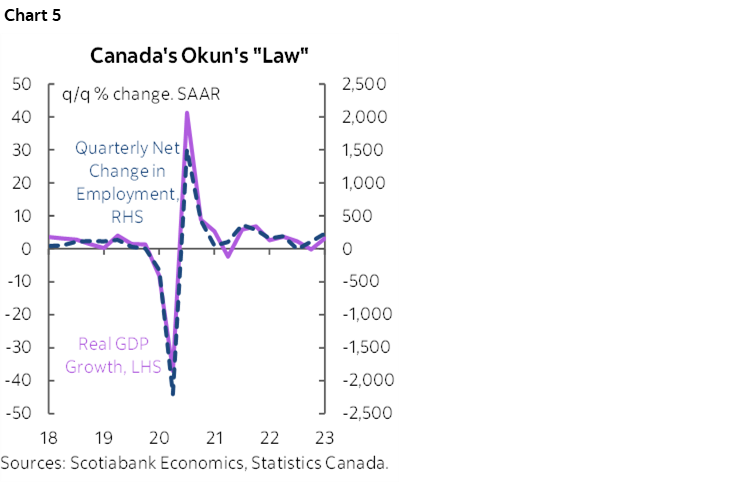

In fact, that Canadian employers routinely rely upon hiring more workers to achieve higher output versus more emphasis upon productivity is illustrated in chart 5. Okun’s ‘law’ is no law per se but this shows the correlations between employment growth and GDP growth.

I’ve guesstimated ongoing resilience in the job market with another 25k employment gain and a fairly stable unemployment rate of 5% as labour force expansion offsets job growth. Using US measurement principles that would equate to about a 4.2% unemployment rate versus the 3.7% US rate. Given confidence bands around the noise it’s feasible that the unemployment rates are virtually identical in the two countries, yet Canada’s natural rate of unemployment is commonly estimated to be higher than the US. As such, there is a tighter labour market north of the border than to the south at least as measured by unemployment rate spreads to OECD natural rate estimates.

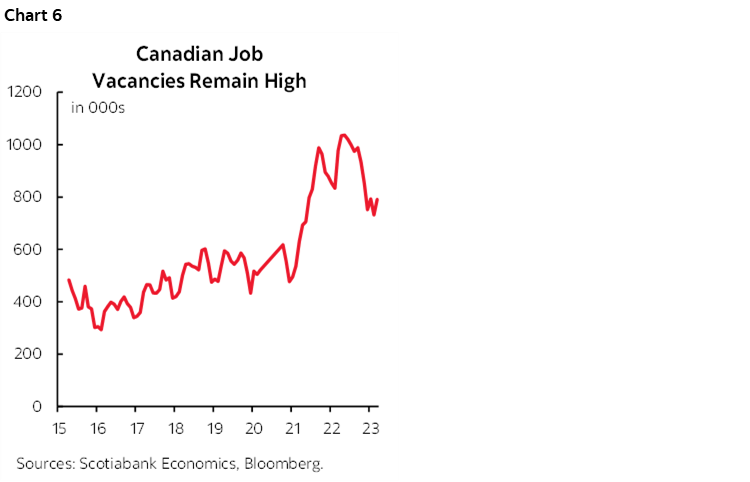

One reason for expecting continued resilience is that job vacancies remain very high at about 800,000 (chart 6). That’s off the peak of over 1 million about a year ago, but it is still hundreds of thousands higher than pre-pandemic levels. Another reason is that May can bring out increased hiring for youths in the summer job market that seems weaker than last year’s but still vastly stronger than pre-pandemic levels (here).

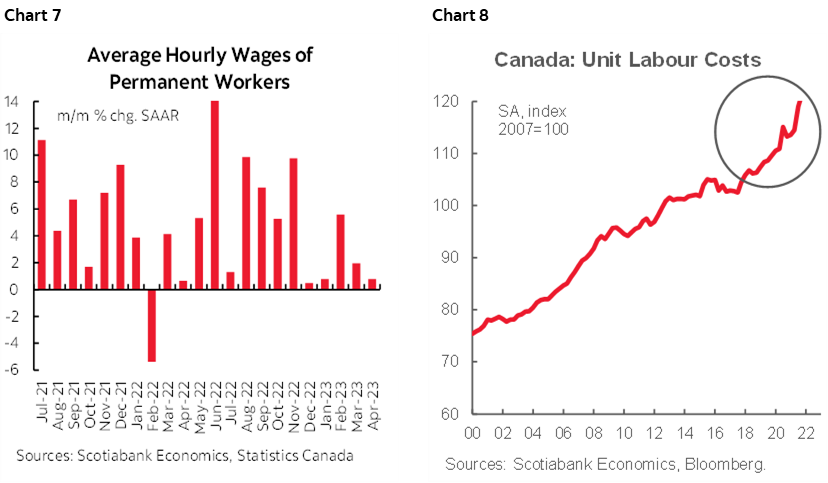

Given some evidence of cooling wage growth, this week’s fresh evidence could further inform a trend, or reset the narrative a touch. Year-over-year wage gains have been steady at around 5%, but the month-over-month gains have stalled out of late after applying standard seasonal adjustments (chart 7). Wage growth after taking account of weak productivity is probably continuing to put upward pressure upon unit labour costs that began to accelerate before the pandemic and then picked up even more over the past couple of years (chart 8). Inflation connections to the job market need to consider both the wage and productivity trends.

One issue is whether collective bargaining agreements could soon begin to show up in the wage figures, albeit the reliance upon self-reporting given that the Labour Force Survey is a consumer survey. The month of May saw faster wage gains for about 150k Federal civil servants after a strike. Airlines have also contributed to this picture including a 15.5% hourly pay hike for WestJet pilots retroactive to January 1st as well as a decision by Air Canada’s pilots to withdraw from their agreement by September and pursue more aggressive wage demands over the summer as a reflection of a global shortage of pilots and planes. Universities have been among other unionized sectors seeking wage gains (examples here).

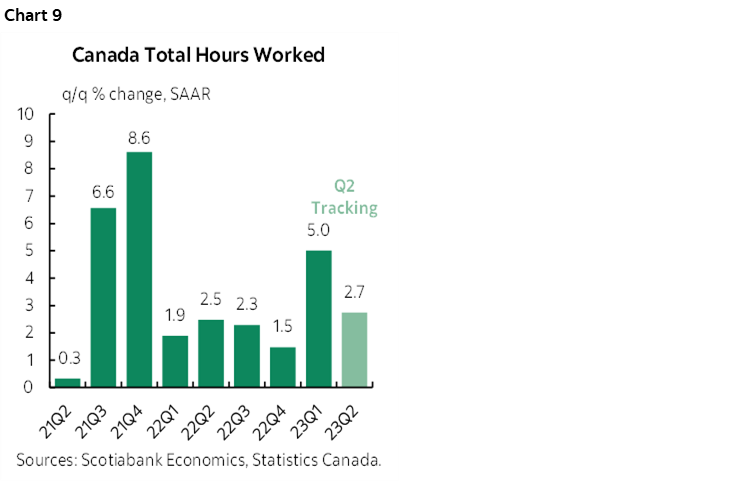

Finally, we also need to have a close look at hours worked. Current tracking is pointing toward a Q2 gain of over 2½% on a q/q SAAR basis (chart 9). May data will further inform this tracking. This matters as a guide to tracking GDP growth in Q2 since GDP is an identity defined as hours times labour productivity. If hours worked post significant growth, then this could support resilient economic growth in Q2 after Q1 GDP beat expectations with a 3.1% q/q SAAR surge—as long as productivity doesn’t go pear-shaped in Q2.

Further on this count is that Patrick Perrier’s nowcast model of Canadian GDP growth is tracking an early gain of about 2½% in Q2. After Q1 growth of 3.1% that beat the BoC’s 2.3% April MPR forecast by a significant margin, it may be that the BoC has to upgrade its Q2 projection for 1% growth.

OTHER CENTRAL BANKS—THE THREE RS

Three other central bank decisions could spice things up a bit albeit potentially in difference directions to one another in some of their cases.

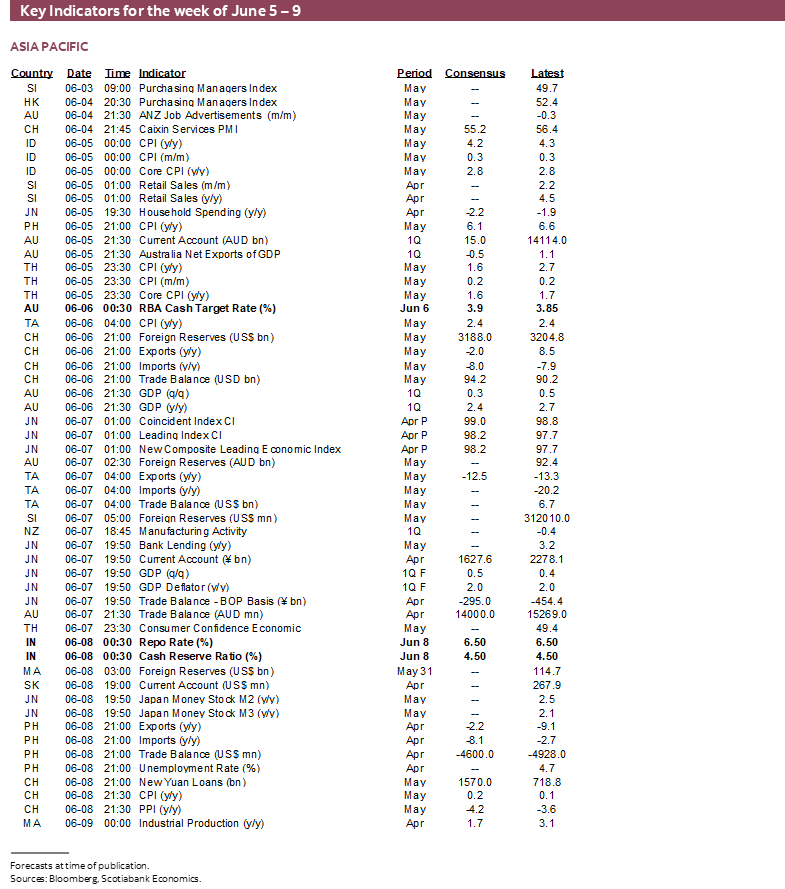

RBA—Sounds Familiar!

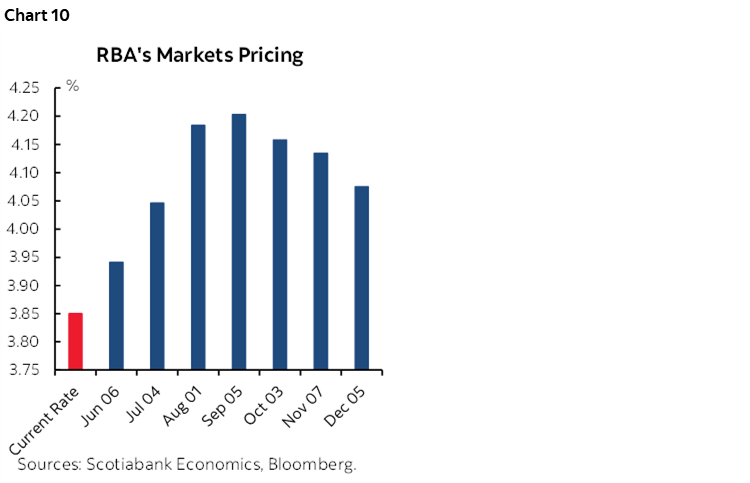

The Reserve Bank of Australia faces a similar set of market and consensus expectations as the Bank of Canada faces. There is a significant market probability attached to a hike on Tuesday with about one-third of consensus expecting a 25bps move. Minutes to the prior meeting indicated that the pause in April could have driven currency weakness and higher home prices and sounded hawkish toward the possibility of further rate hikes. Then CPI surprised higher with a rise of 6.8% y/y in April from 6.3% (consensus 6.4%) and yet underlying inflation was a bit softer while jobs were flat in April (-4.3k). Q1 GDP arrives not long after the decision. See chart 10 for future market pricing of the RBA policy rate.

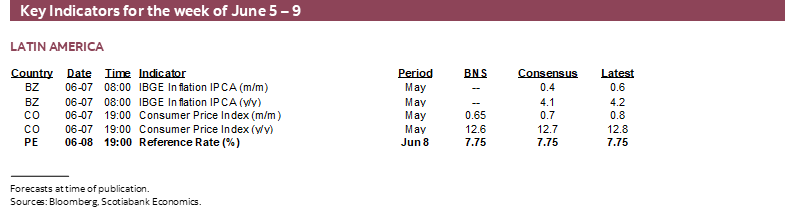

RBI—Watch Guidance

Notwithstanding the Reserve Bank of India’s pattern of offering surprises in the past, consensus expects India’s central bank to stand pat with an unchanged repurchase rate of 6.5% on Thursday. Whether it wipes out hawkish guidance with something more balanced and neutral may inform future policy rate pricing.

Peru—Soft Core CPI Should Extend the Pause

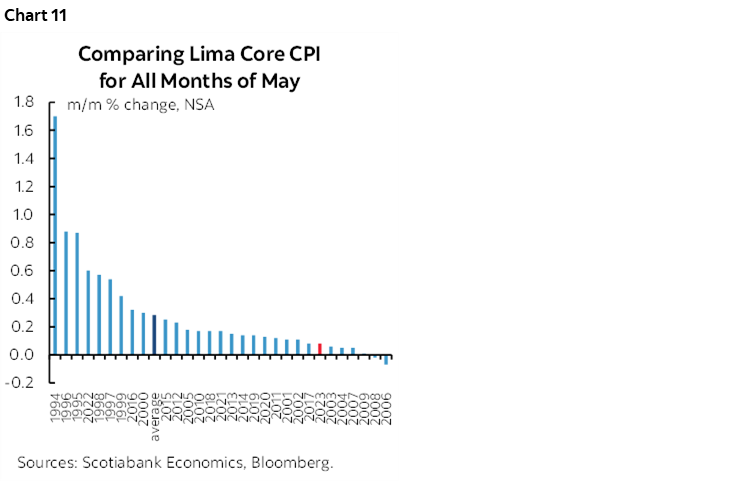

Banco Central de Reserva del Peru is expected to hold its reference rate unchanged at 7.75% again on Thursday evening (ET). As elsewhere, the focus may be upon forward guidance particularly as CPI landed on the screws at 0.3% m/m and 7.9% y/y but with core inflation dropping a half percentage point to 5.1% y/y in May and with the month-over-month seasonally unadjusted core CPI measure abnormally soft for a month of May (chart 11).

GLOBAL MACRO—AN OTHERWISE LIGHT WEEK

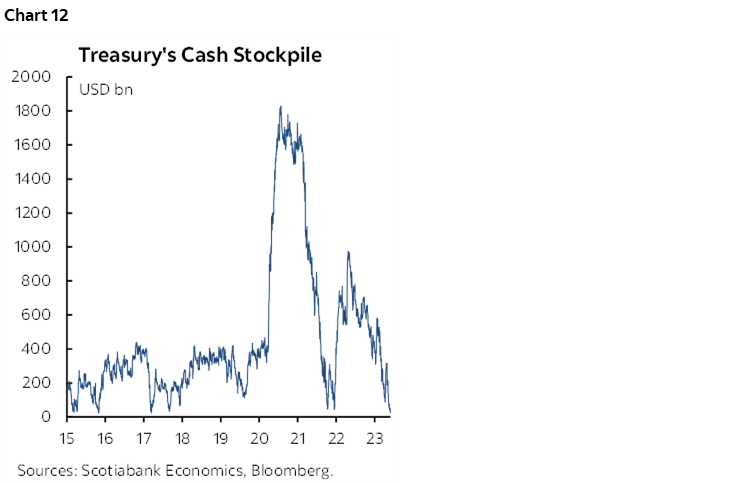

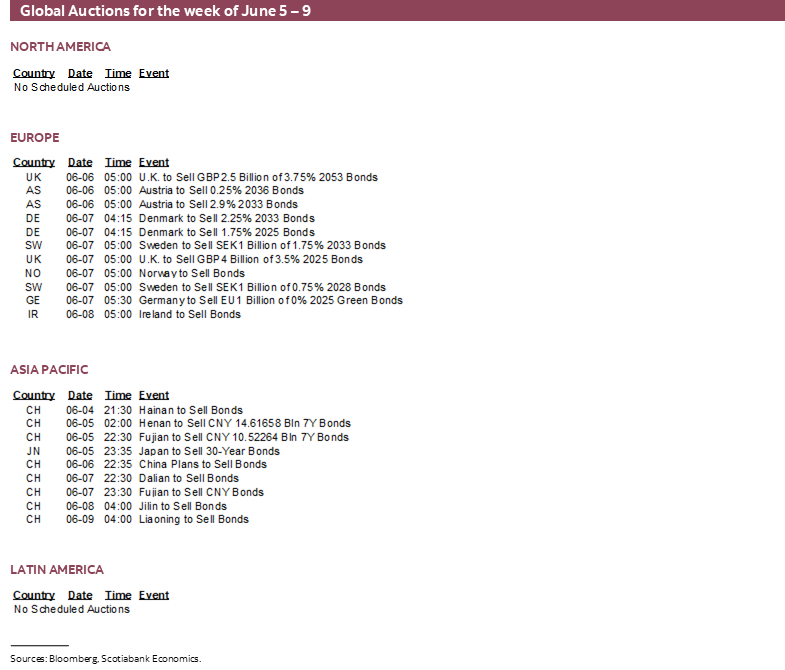

The rest of the global line-up should make for a relatively light line-up of calendar-based risks just as most of the off-calendar risk has dissipated, such as the passage of the debt ceiling agreement in the US and the stabilization of regional banking challenges. The focus now turns to the aftermath in terms of replenishing the Treasury General Account at the Federal Reserve that during the debt freeze sank toward the lowest points in years (chart 12). The effects of shorter-term debt issuance to replenish these cash balances will likely drain banking system reserves in the US and pressure nearer-term liquidity on a transitory basis as on past such occasions.

Canada has enough to focus upon with the BoC, jobs, wages and productivity as already written. Fortunately, the rest of the domestic calendar will be very lightly populated by just trade figures for April (Wednesday) that may further inform Q2 GDP tracking, plus the Ivey PMI for May (Tuesday) that could inform supply chain pressures but is difficult to read because it combines all public and private purchasing managers into one composite.

The US line-up of releases will only include factory orders that should follow the 1.1% jump in durable goods higher (Monday). ISM-services will be the main release for the week (Monday), but what it says about hiring activity is less significant now in the wake of payrolls. The overall trade deficit will probably widen on Wednesday given that we already know this happened to the merchandise component in April. Initial jobless claims have been trending around the 230k range that remains constructive to ongoing job growth and Thursday’s estimates falls outside of the nonfarm reference period anyway. The Fed’s flow of funds accounts for the US economy in Q1 will include updates to various measures of household and business finances on Friday.

A wave of global inflation reports will be unleashed over the coming week. One may be impactful to global markets while the rest could impact local markets. Headline Chinese CPI inflation (Thursday night ET) is expected to remain near 0% y/y while core CPI is likely to continue to hover around ¾% y/y. Switzerland, Indonesia, Thailand and Philippines update on Monday followed by Taiwan on Tuesday, Colombia and Brazil on Wednesday, Mexico and Chile on Thursday and then Norway gets the final say on Friday.

Australian Q1 GDP is expected to post a sixth straight quarter of growth on Tuesday with trade figures for April out the next day.

China’s private Caixin composite PMI arrives into the Monday morning Asian open and since it is more skewed toward smaller producers than the state’s PMIs that are dominated by SOEs it may not necessarily follow the already known 1.5 drop in the state’s composite PMI. China also updates trade figures for May around mid-week and may update credit and money supply figures this week or next.

BoJ watchers should keep an eye on real wages during April (Monday night ET) that may begin to reflect the effects of annual Spring wage negotiations that have been coming off the bottom from earlier in the year.

Europe’s calendar will be mainly focused upon German trade (Monday), factory orders (Tuesday) and industrial output (Wednesday). French Q2 payrolls (Thursday) will strive to make it 10 in a row for quarterly job gains.

Brazilian PMIs (Monday), Mexican industrial output (Friday) and India’s updated PMIs (Monday) round things out.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.