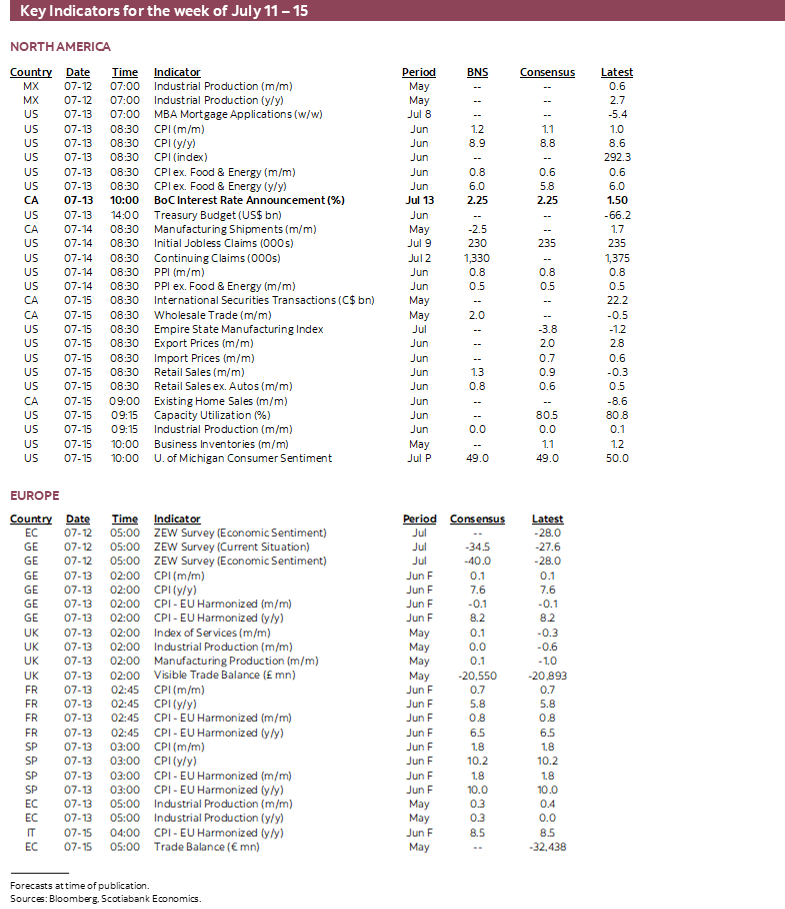

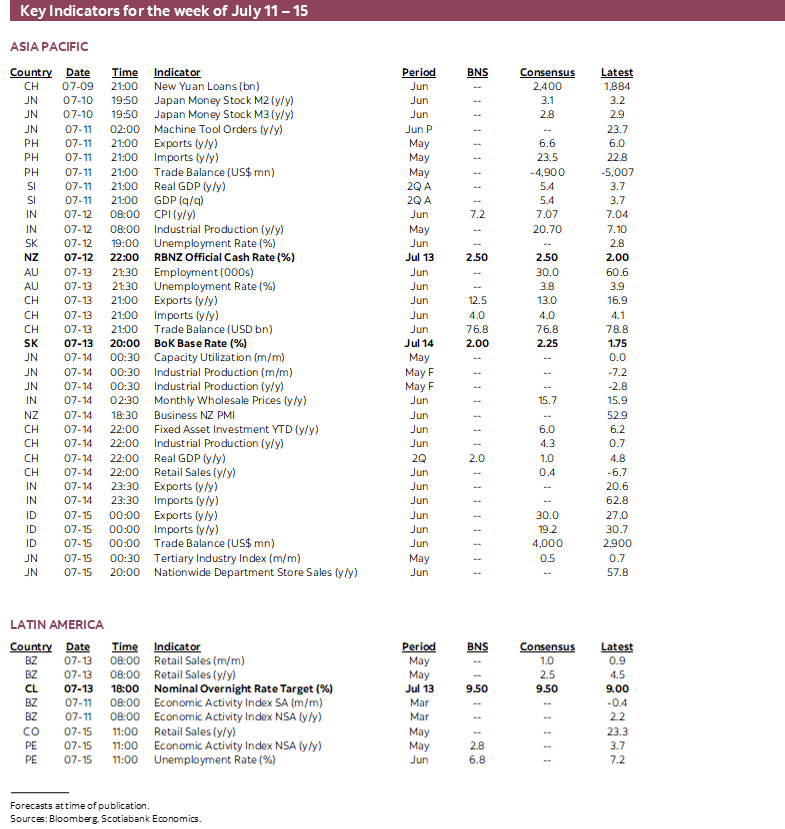

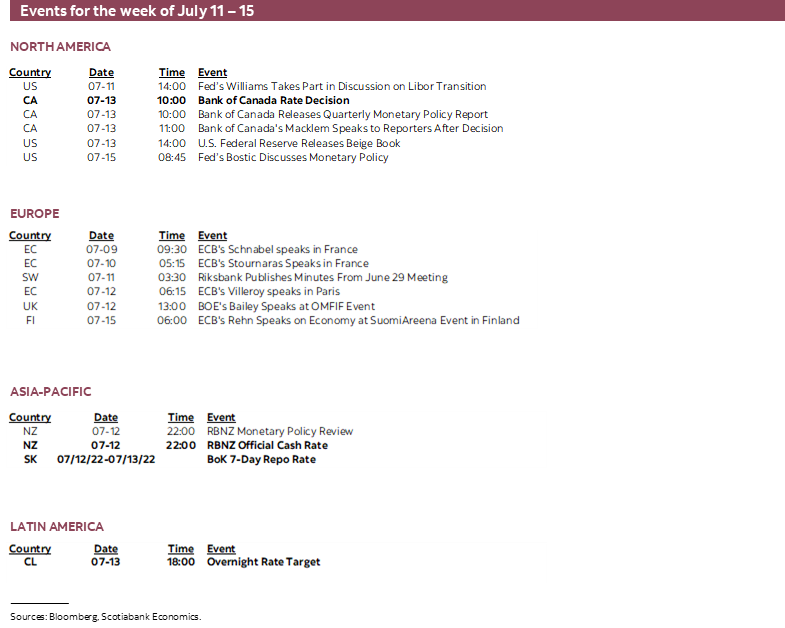

Next Week's Risk Dashboard

- US CPI is still running hot

- BoC to up-size its hikes

- The Q2 US earnings season

- RBNZ, BoK, BCCh to continue to lead

- Australian jobs

- China’s economy

- Global macro readings

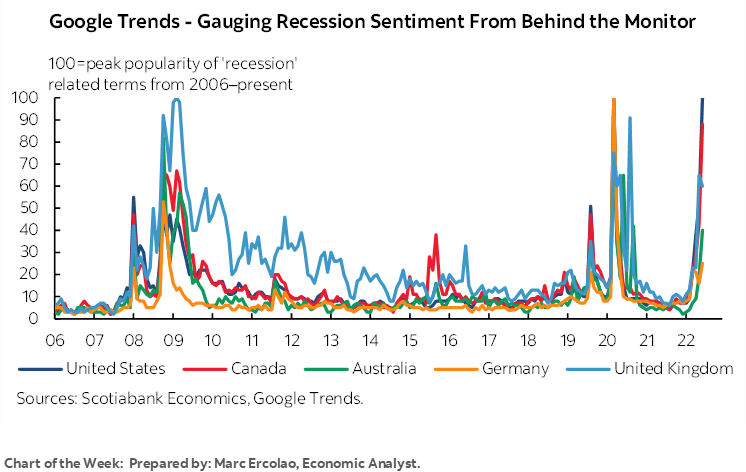

Chart of the Week

Since some readers of this publication likely care about US inflation and the Bank of Canada my advice would be not to take Wednesday off! In fact, most of the week’s main events including the Q2 US earnings season unfold over the back half of the week.

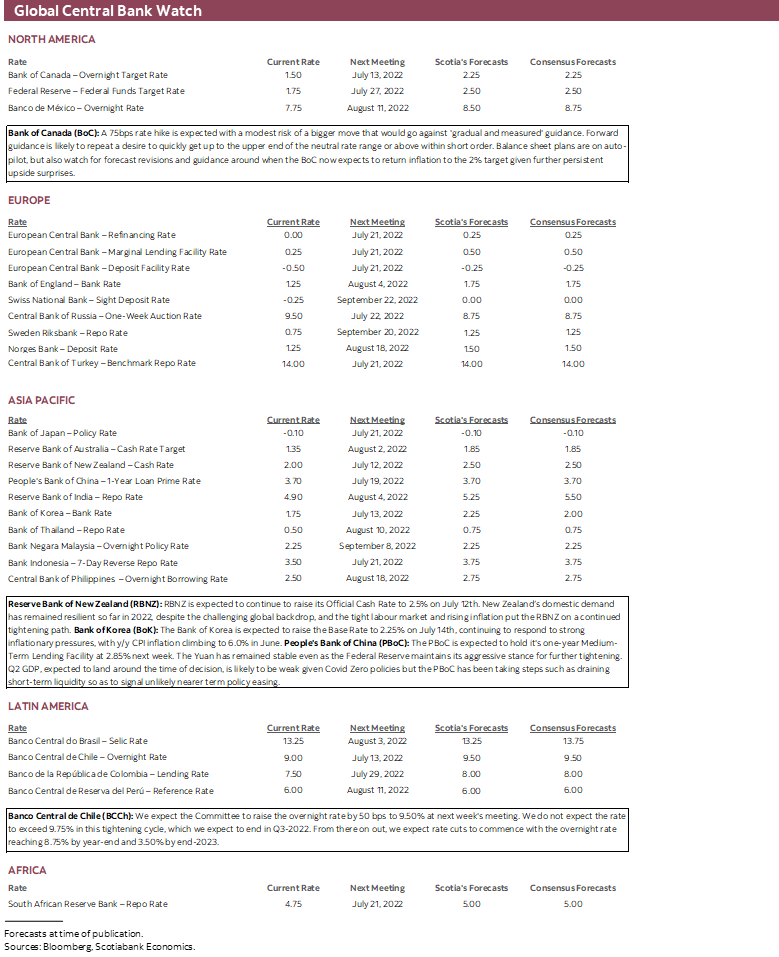

BANK OF CANADA—JUST RIP THE BAND-AID OFF?!

The Bank of Canada delivers its latest policy rate statement on Wednesday (10amET) at the same time as it releases updated forecasts and assessments in its Monetary Policy Report. Governor Macklem and SDG Rogers hold a joint press conference one hour later. The suite of communications unfolds after the release of US CPI that may muddy the waters in terms of pure market reactions to the developments.

A 75bps rate hike is expected alongside a continued pledge to be data dependent on a quest to return the 1.5% overnight rate toward the upper end of the 2–3% neutral rate range or above which is probably the guidance they will repeat. I think a policy rate at 3% by September and 50–75bps higher than that into year-end is a reasonable view. Consensus is unanimous in expecting 75bps this week and OIS markets are pricing half of another quarter point and hence straddling the line between 75 and 100bps.

For the sake of the Bank of Canada’s remaining credibility it would be better advised for them to go 75bps now and then go another 75bps in September to get up to 3% and hence push above the neutral rate range into suitably more restrictive territory than to more aggressively rip the band-aid off with a move of 100bps now—or more. I would like to see the latter and think there is a strong case for 100+ because policy remains excessively stimulative with a policy rate 100bps below the mid-point of the neutral rate range and the balance sheet remains bloated even with no roll-off caps on maturing Government of Canada bond holdings. Yet inflation is four times the target rate and the BoC keeps chasing it higher with its forecasts. The problem is that after having guided ‘gradual and measured’ all along and after missing opportunities to hike earlier even when it was priced in January, for the BoC to now swing to the other side with a 100+ move now would only add to the sense it is behaving very erratically if not panicking. An extra 25 now would accomplish little over leaving the door open to another large move at the next meeting. Still, I can’t resist noting that the same folks who mocked my view some time ago that the BoC would be increasing the size of its rate hikes now suddenly seem to think it’s obvious they should do so.

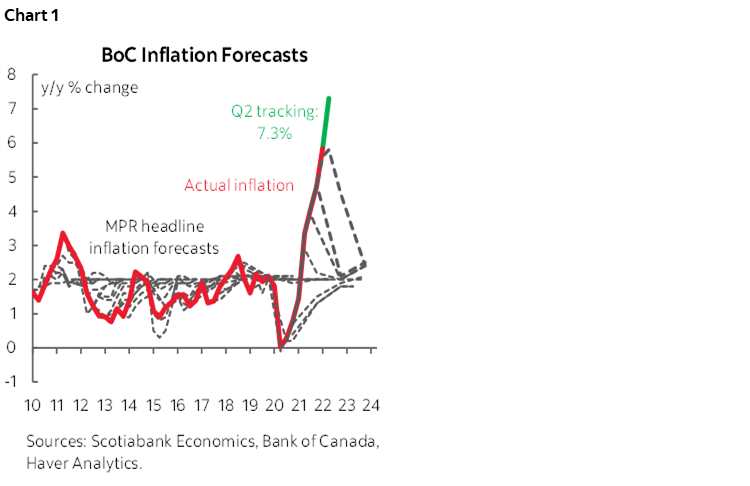

To support such expectations, start with tracking inflation. The BoC continues to play catch up to inflationary pressures. The last reading landed above consensus with headline CPI inflation rising to its highest since 1983 and with average core inflation hitting the highest on record (recap here). Chart 1 shows that Q2 inflation is sharply exceeding the BoC’s 5.8% y/y forecast with tracking at about 7¼% and this continues the weak track record at forecast inflation.

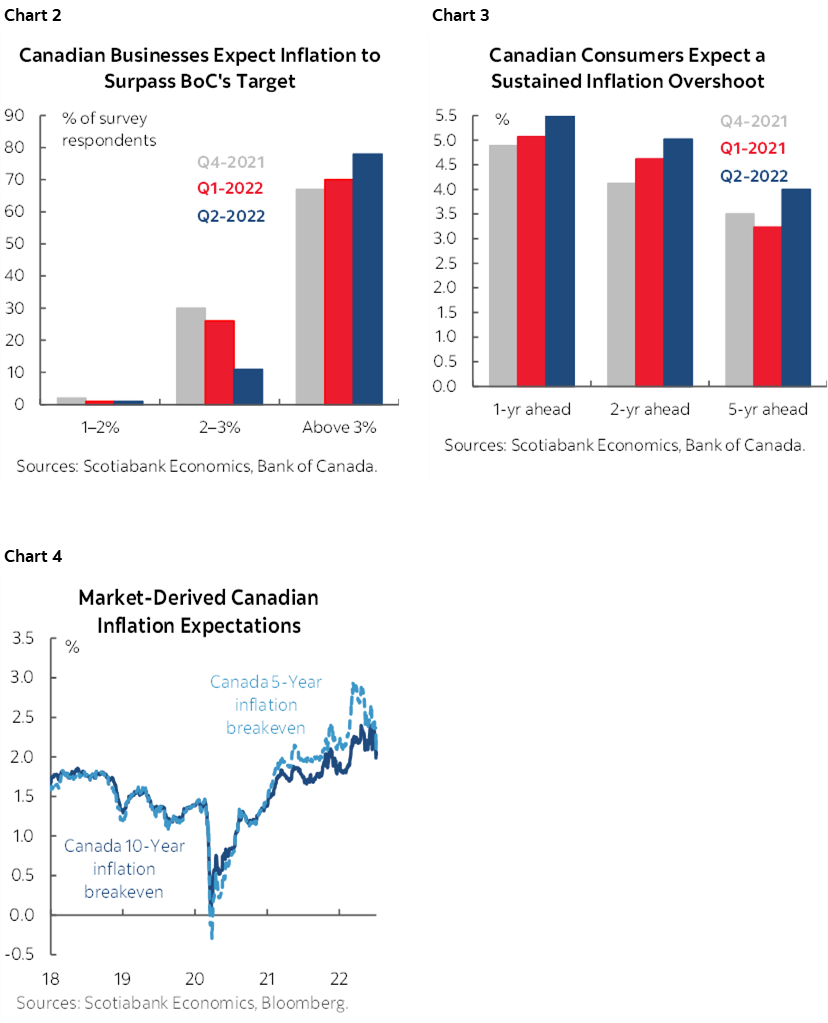

Inflation expectations continue to move higher according to survey-based evidence across businesses (chart 2) and consumers (chart 3). Market-based implied measures have waned coincidental to the sell-off in base yields (chart 4). The BoC is likely to remain concerned about the risks around unmoored inflation expectations and determined to try to steer them lower.

In addition to data, the Bank of Canada has also provided altered guidance in favour of a faster pace, potentially bigger individual moves and higher terminal rates. For instance, the June BoC statement omitted reference to “timing” to suggest rate hikes were likely to be compressed into a shorter period of time. The same statement added “more” in front of “forcefully” to drive home the point that they wish to move more quickly and/or in bigger increments. Deputy Governor Beaudry’s speech the day after that statement then said:

“We see this aspect of potentially needing to go higher than we thought before and we still have the idea that we want to get there as quickly as possible so that could involve doing more moves in a row or it could involve bigger moves.”

When SDG Rogers spoke a week later at a Globe and Mail event she passed on the opportunity to talk down a bigger 75bps hike.

So to be clear, nothing the BoC has provided explicit guidance about the size of a rate hike beyond leaving the door open to perhaps doing something bigger than 50bps and at a quickened pace.

There may be several considerations that could hold them back from a mega hike. One is that GDP growth is probably undercutting their forecast for 6% in Q2 and is more likely just above half that rate. Still, such growth is well above the economy’s noninflationary speed limit and is pushing the economy further into excess demand conditions best indicated by at least parts of the inflation picture. Second is the recent drop in jobs they might reference, but I don’t find that to be likely as argued here. Third is very nascent evidence that perhaps global supply chain pressures are beginning to ease as one of the drivers of inflation, versus the other which is a persistent move into excess demand. Fourth, interest sensitive sectors—namely housing—are rolling which should give them a perverse form of encouragement in that the transmission channels of tightened policy are working their way through.

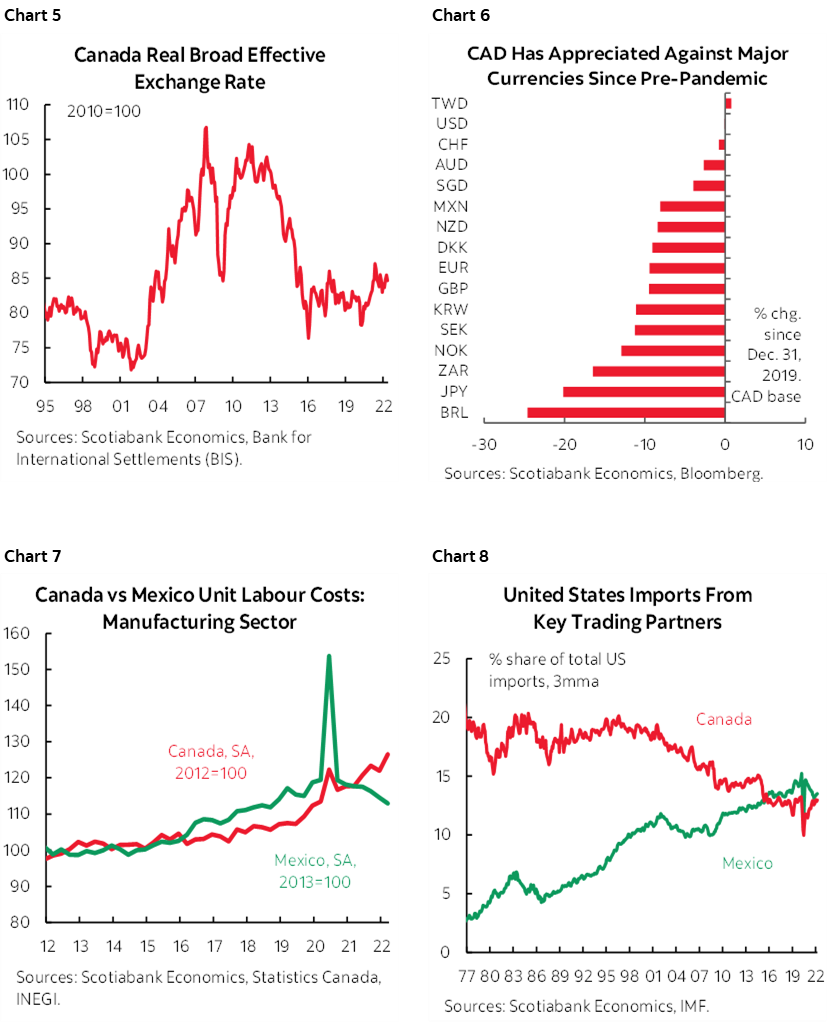

Some will say that the level of the C$ at just under 1.30 (USDCAD, 77 cents CADUSD) suggests it is an undervalued currency that leaves room for the BoC to hike more aggressively. Against this view is that the real effective exchange rate—which is trade weighted and adjusted for relative rates of inflation—has slightly appreciated since just before the pandemic (chart 5) in part because other currencies like the Mexican peso have depreciated against CAD over this time (chart 6). Canada has developed a serious competitiveness challenge partly because of this, partly because of tumbling labour productivity and partly because of relative expensive labour. Chart 7 shows that Canada’s unit labour costs—employment costs per unit of output which essentially combines productivity—have risen throughout the pandemic relative to Mexico’s. As a consequence, guess who is gaining market share in the US and who is not (chart 8). Canada’s high commodity prices may be all it has left going for it in terms of trade drivers of growth while interest-sensitive sectors retreat.

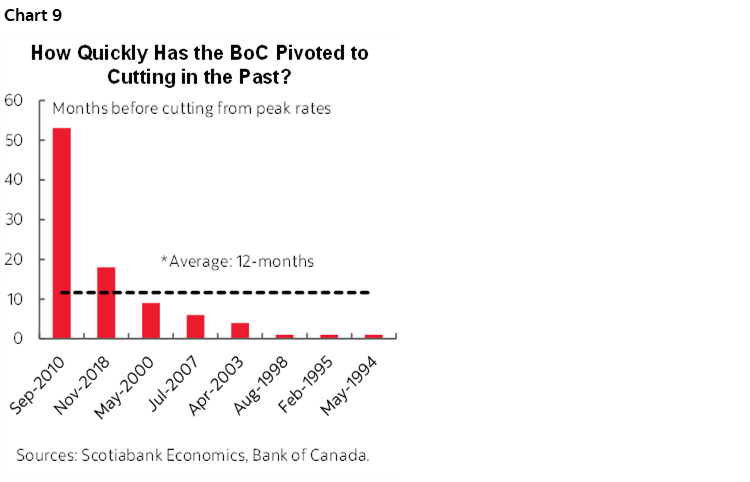

Having said that, would the BoC return to cutting next year as markets have been flirting with of late? As chart 9 shows it isn’t impossible they do so given that the average distance between rate peaks and the first rate cut has been about a year since the GFC and less than that upon removing the one big outlier. The question is whether the experiences over the period between the GFC and now are instructive in terms of present challenges. I don’t think they are. For one thing, the long and variable lags between rate adjustments and the full effects on the economy are somewhere between 6–18 months amid debate over whether the rate responsiveness may be higher this time (given the interest sensitives that drove a lot of growth to date) or lower this time (given various arguments including a nascent services rebound). If so, then the BoC is unlikely to begin easing before the full effects have been felt. Secondly, after having botched inflation management to date, I think they’ll want to be darn sure that inflation has returned toward target and stayed there before easing.

Also watch for important revisions to growth. Q2 GDP growth is coming in well shy of the BoC’s 6% April forecast but is likely still well above potential group such that the economy continues to push into excess demand while inflation is overshooting their forecasts as the more important point. The BoC will also ink their first attempt at forecasting Q3 GDP growth.

US INFLATION—PERSISTENCE

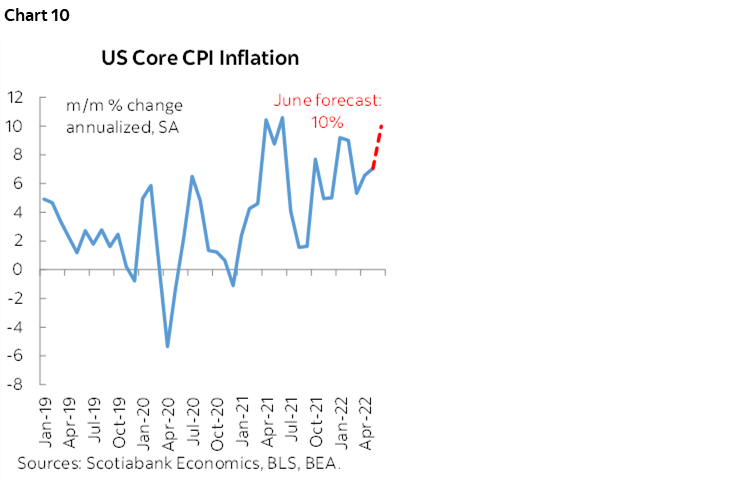

US CPI inflation for June lands on Wednesday (8:30amET). I’ve gone with 1.2% m/m for seasonally adjusted headline inflation and 8.9% y/y while expecting core inflation to hold steady at 6% y/y only because another large month-over-month gain of 0.8% should be enough to offset year-ago base effects that would otherwise put downward pressure on the year-over-year rate.

If I’m right, then headline CPI will be running at a nearly 14% m/m rate in seasonally adjusted and annualized terms, with core CPI inflation running at 10% m/m at a seasonally adjusted and annualized rate. That would be the hottest core reading since June of last year while indicating continued upward pressure upon underlying inflation (chart 10).

Here are the drivers:

- Year-ago base effects on their own would drag the year-over-year rate of inflation down from 8.6% to 7.6%. I’ve said it over and over, but I’ll say it again: so what! If we judge inflationary pressures by looking at year-over-year rates instead of incremental evidence of inflationary pressures through a variety of month-over-month and breadth gauges then central banks and consensus will make the same mistakes they did throughout 2021.

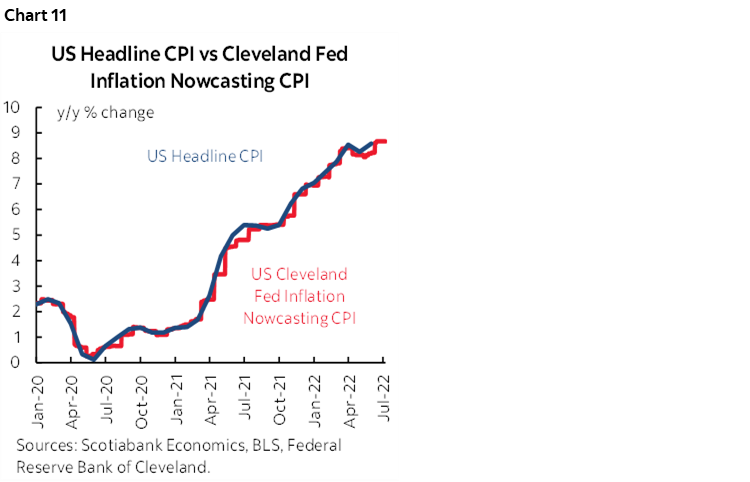

- The Cleveland Fed’s ‘nowcast’ of US inflation points toward a rise of about 8.7% y/y for headline CPI during June and is so far indicating sustained pressures into July despite year-ago base effects that should be lessening the pressures upon this reading (chart 11). This measure has nevertheless been recently underestimating inflation and so there are the other following considerations.

- Gasoline prices moved higher again. A 9% m/m rise at a 4½% weight in the basket should add about 0.4 percentage points to the m/m rate of CPI inflation.

- Natural gas prices moved higher on a Henry Hub spot basis, but not enough to contribute to piped utility fuel prices in the basket given a 0.9% weight.

- Used vehicle prices moved up by about 4 ½% m/m according to a proxy of the input source used by the BLS. At about a 4% basket weight this should add 0.2 ppts.

- New vehicle prices were slightly higher but not enough to matter in weighted terms.

- I’ve assumed another 1% rise in food prices split between groceries and at-home contributions.

- And lastly I’ve assumed that reengagement effects particularly through high-contact service prices like airfare, lodging, car rentals, etc contribute to an extra three-tenths rise in inflationary pressures from a bottom-up standpoint.

Amid all of the data noise are impetuous markets. The tone of much of the commentary around inflationary pressures is too skewed toward what might happen in the short-term versus addressing longer-run drivers of inflationary pressures, in addition to focusing too heavily upon year-over-year rates instead of higher frequency gauges.

AND THE CENTRAL BANK OF THE YEAR AWARD GOES TO….

Three of the leading candidates for central bank of the year awards are poised to deliver fresh policy decisions this week. They are in this boat together for their relatively early tightening stances as global inflationary pressures began to escalate and with considerable distance from the initial emergency conditions of the pandemic.

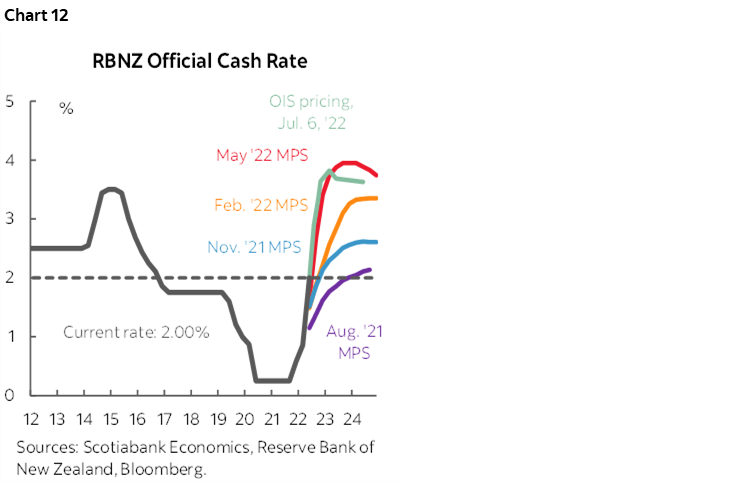

The Reserve Bank of New Zealand will be first out of the gates on Tuesday and it is expected to hike by another 50bps with consensus and Overnight Index Swap (OIS) market measures aligned. The RBNZ was among the early hikers as it raised its official cash rate by 25bps last August and would have raised it in July if not for the fact that a sudden burst of COVID cases prompted a shorter-lived government shutdown on the eve of that decision. Since then, the RBNZ has hiked by 175bps and a 2 ½% policy rate this week would make the RBNZ the first among the relatively mature market central banks to get its policy rate into restrictive territory. Its intent to overshoot the neutral rate was conveyed in the May statement that ended by noting “Once aggregate supply and demand are more in balance, the OCR can then return to a lower, more neutral, level.” Markets have generally come on side (chart 12). There may also be questioning or guidance around the start of the RBNZ’s legislated 5-year framework review that began on June 1st with a public consultation period until July 15th on the path toward recommendations to the Finance Minister next year on issues like the 2% inflation target.

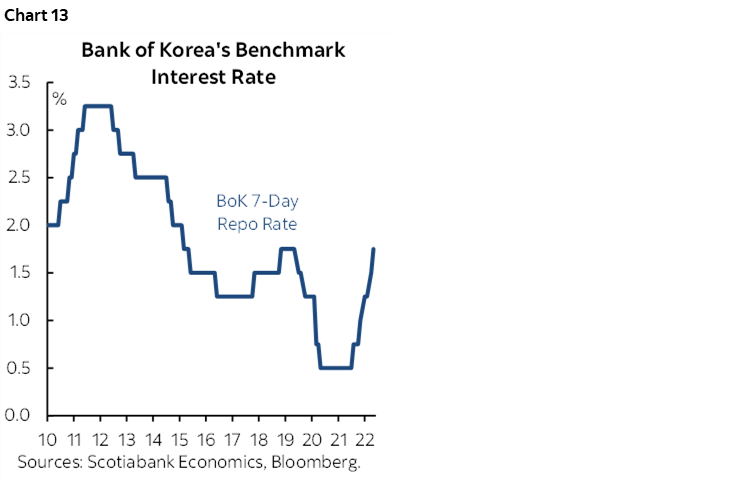

The Bank of Korea could give the RBNZ a run for its money as the poster child for prudent monetary policy. The BoK is also expected to hike by another 50bps on Thursday which would bring the 7-day repo rate up to 2 ¼%. The BoK first hiked last August and has raised its policy rate by 125bps to date (chart 13). At issue is how much further room for tightening there may be. The BoK has a 2% inflation target and estimates of its real neutral policy rate tend to be negative (here). If so, then market pricing for the nominal policy rate to roughly double within the next year imply a shift into significantly restrictive territory. Watch forward guidance on this matter.

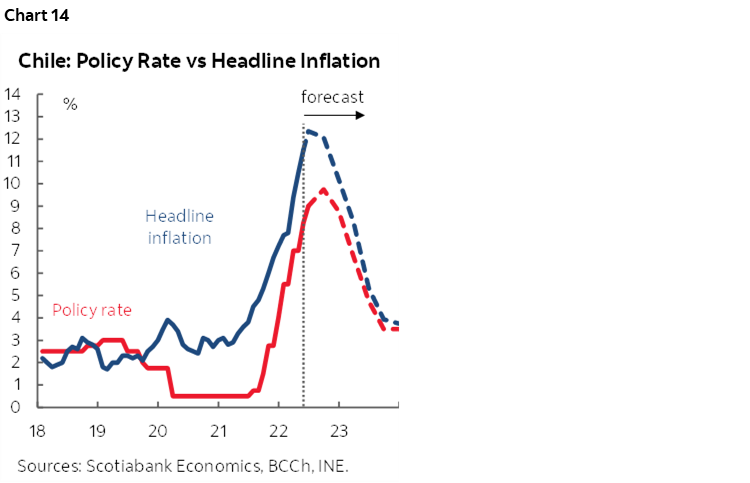

At Wednesday’s Banco Central de Chile (BCCh) meeting, we expect the committee to deliver a 50bps hike of the overnight rate to 9.50%, the highest rate since 1998. Like many of its LatAm peers, Chile is nearing the end of its tightening cycle, having hiked the policy rate a cumulative 850 bps since July 2021. However, with both headline and core inflation remaining stubbornly high, well in excess of the central bank’s 3 +/– 1% target (chart 14), most are calling for hikes into Q3-2022, where a likely pause followed by rate cuts should commence thereafter. Tighter financial conditions and removal of stimulus measures are weighing on Chile’s growth outlook, so future policy decisions will need to balance this with the hopes that price pressures will alleviate.

THE Q2 US EARNINGS SEASON

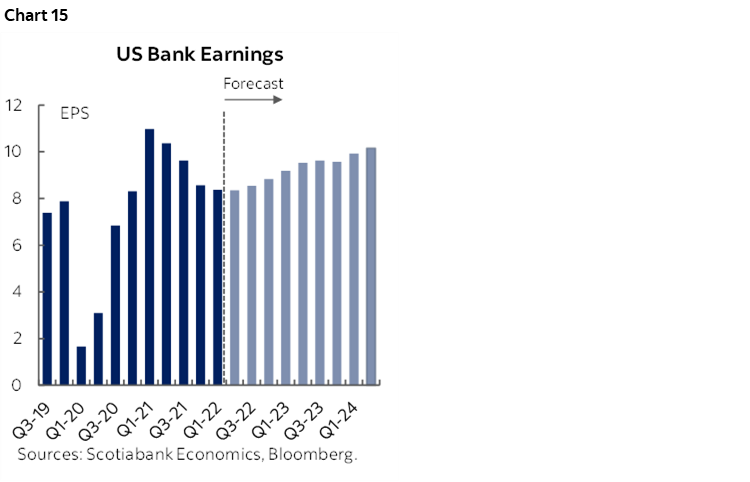

The Q2 US earnings season kicks off with the usual early focus upon key financials toward the end of the week. JP Morgan Chase and Morgan Stanley release on Thursday followed by Citigroup, BlackRock, Wells Fargo and BoNYM on Friday. Other financials will be mixed into the fray along with Delta Air Lines that releases on Tuesday. Chart 15 shows the earnings expectations for the banks on the S&P500.

OTHER GLOBAL MACRO REPORTS

Major releases on the docket are due out from China, the US, Australia, South Korea and the UK.

US retail sales will pale by comparison to CPI in terms of market significance but Friday’s estimates for June should offer up a healthy gain at least in nominal terms. Vehicle sales volumes were up by 2.5% m/m in June and prices also edged higher which should add to higher gasoline prices that were up by about 9% to drive the dollar value of total retail sales up by an estimated 1.3% m/m. Sales ex-autos and gas are expected to post a minor gain. After stripping out the effects of higher prices there may be little to no gain in sales volumes.

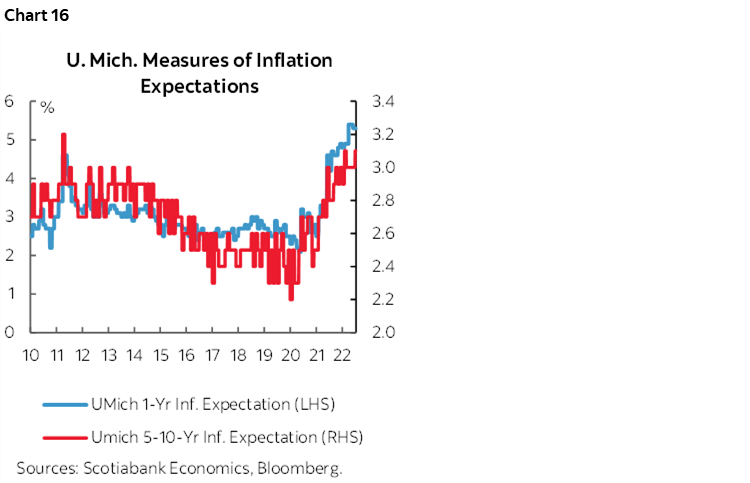

Other US releases will include the University of Michigan’s consumer sentiment survey for July (Friday). Watch the measures of inflation expectations after Fed Chair Powell cited the prior month’s run-up as a reason alongside the upside surprise in May CPI for shifting to a 75bps hike instead of 50bps (chart 16). Industrial output during June (Friday), the producer price index during June (Thursday), the Empire manufacturing gauge’s kick-off to another round of regional surveys (Friday) and the Fed’s Beige Book of regional conditions (Wednesday) will round out the calendar.

China releases will also vie for attention. Chinese CPI inflation during June is expected to edge up again toward 2 ½% y/y when it gets released on Saturday, Beijing time. At some point during the week China will update aggregate financing figures for June that are expected to accelerate in the wake of prior easing. The People’s Bank of China is expected to leave its 1-year Medium-Term Lending Facility Rate unchanged at 2.85% one day this week. Chinese export and import growth during June will be updated by mid-week. Then the main release for Q2 GDP arrives on Thursday alongside June estimates for retail sales and industrial output that will help to inform hand-off effects for growth into Q3. China’s economy is expected to post a Q2 contraction in no small part due to Covid Zero restrictions, but also due to pressures upon its key export markets.

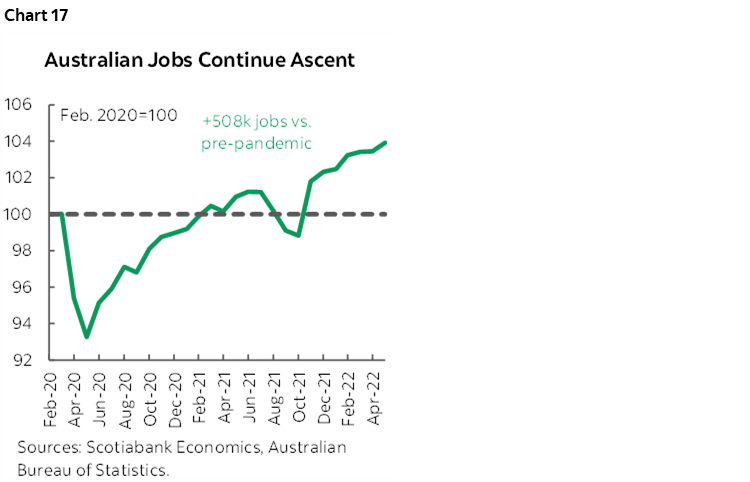

Australia’s job market continues to push deeper into full employment, with another +60k jobs added in May alongside a participation rate that nudged up to a record 66.7% and an unemployment rate that sits at a historic low of 3.9%. Another modest gain is expected for June (consensus +30k), which would mark the eighth straight month of job gains and would put the total level of employment +508k above pre-pandemic levels (chart 17). Labour market strength has given the green light for the RBA to continue aggressively tightening, delivering a 50bps hike on July 5, with continuing hawkish guidance for further hikes.

The South Korean labour market has been resilient in the face of the central bank’s tightening cycle which has been underway for the better part of the last 12 months. The slight uptick in unemployment rate in May, up a tenth of a percent to 2.8%, still sits in record low territory and was mainly driven by a healthy rise in the participation rate, up to 64.2%, that outpaced an equally as impressive +140k jobs added (chart 18). On wages, the Bank of Korea is prioritizing inflation containment during their normalization cycle; current levels of inflation are keeping real wages suppressed.

UK macro reports are likely to fly beneath the radar given the backdrop of political turmoil. Industrial output probably contracted in May and Wednesday will also reveal the same month’s readings for a services index, trade and monthly GDP with the latter expected to post a third consecutive retreat.

Other Asian reports will include Indian CPI inflation for June (Tuesday) that is expected to hold at about 7% y/y. European releases will also include the ZEW investor sentiment reading for July (Tuesday) as well as inflation prints from Norway and Switzerland. LatAm readings will only add retail sales from Brazil (Wednesday) and Colombia (May) plus industrial output in Colombia (Friday) and Mexico (Tuesday).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.