Next Week's Risk Dashboard

- Politicized attacks on the Fed must stop

- The tangible benefits of independent central banks

- Trump idolizes Andrew Jackson — whose meddling sparked disaster

- What happened when other countries meddled with central banks

- US ‘specialness’ would be severely tested by meddling with the Fed

- US monetary policy is about right — what many models, and judgement say

- 1% you say? Please explain this coming crisis to us.

- Japan’s upper house election likely to further weaken PM Ishiba’s control

- ECB expected to stand pat

- BoC surveys likely to show modest inflation relief

- Powell to kick off a Fed conference on capital during blackout

- Global PMIs to inform risks to growth, inflation, supply chains

- RBA minutes likely to be stale

- Turkey’s erratic central bank might cut

- So might Russia’s

- Global macro readings

Chart of the Week

The coming week’s main developments will focus on earnings, central banks and data. The US earnings season broadens out to include earnings from ‘Magnificent Seven’ tech darlings in a market that has once again become narrowly driven. A few central banks will weigh in with updated decisions (ECB, Turkey, Russia), while the BoC primes the way with surveys ahead of its decision the following week. Chair Powell kicks off a Fed conference on regulatory capital standards. Significant global macro readings will be peppered throughout the week.

Japanese markets will follow the outcome of this weekend’s Upper House elections on Sunday. Just over half of the seats are up for grabs (chart 1). Prime Minister Shigeru Ishiba's minority government may be dealt a further blow partly at the hands of the rising Sanseito party—a right wing, anti-immigrant upstart. Sanseito has garnered support from rising opposition to foreigners. Ishiba’s ability to control the direction of major public policy challenges such as trade with the United States and fiscal policy could be further impaired.

The FOMC goes into communications blackout ahead of the following week’s decision. That affords the opportunity to delve into the dangers of politicized attacks upon the Federal Reserve as this week’s special topic.

POLITICIZED ATTACKS ON THE FED MUST STOP

Attacks against the independence of the Federal Reserve have reached alarming proportions. While likely performative in nature, they are nevertheless MUCH harsher, more direct, and potentially more dangerous than what has been done by other modern US Presidents. I’ll expand on the following points:

- History strongly counsels caution when messing with central bank independence including examples from US economic history long ago, and more recent international episodes.

- There is clear evidence that independent central banks have led to better outcomes than seemingly forgotten prior experiences. This piece from the World Bank is one among many pieces that draw upon empirical evidence that the rise of central bank independence has been associated with generally lower inflation outside of the complex and unfortunate experiences of the pandemic, and smaller, less frequent budget imbalances.

- And the evidence points to Federal Reserve monetary policy as being suitably positioned for now in stark contrast to President Trump’s views and those of several individuals vying to succeed Powell.

All said, I’ll take an error-prone Federal Reserve during highly uncertain times over a politically dominated one that bends to the behest of the administration any day.

US Precedence

There is a long history of US Presidents meddling in the affairs of the Federal Reserve, while generally sticking to playing politics rather than overt interference. The closest example of overt interference with central bank independence was a very long time ago and ended in disaster for the US economy. Ironically, it was due to a decision by a President that current President Trump reveres. Other examples are drawn from much less developed economies.

Long before the Federal Reserve Act of 1913, the closest—and highly imperfect—thing to a central bank around two hundred years ago was the Second Bank of the United States. Students of US economic history and money and banking will recall the history that is neatly summarized by this post from the Richmond Fed. President Andrew Jackson—a protectionist, like the current President—repealed the charter of the Bank which set in motion the undisciplined and politicized expansion of credit on overly favourable terms into property markets and state-sponsored projects. What ensued was the Great Panic of 1837 and the deep recession of 1837–38. Mr. Trump leaves out that part of his admiration of the Jackson era either through omission or lack of awareness.

Other Examples

There are multiple examples of the perils of messing with central bank independence with varying costs and consequences.

Turkey is a serial offender of central bank independence, having fired three central bankers over the 2019–2023 period. Chart 2 shows that the lira suffered during the attacks in the lead up to their firings and subsequently. Turkish President Erdogan’s unorthodox belief was that easier monetary policy would drive lower inflation partly due to lower interest costs. History and basic economics defied such a view as Turkish inflation soared and the lira has been collapsing throughout the whole period of central bank interference; it traded at about five to the dollar into the first firing in 2019 and sold off more aggressively after the second one in 2021 and particularly after the 2023 firing to now cost over 40 lira to buy one US$. Turks have suffered an enormous erosion of their purchasing power.

Argentina offers a further illustration of the perils to meddling with central banks. Former President Cristina Fernandez de Kirchner fired central bank head Martin Redrado in January 2010. Redrado opposed her plan to use foreign currency reserves to pay down Argentina’s debt, thereby monetizing foreign savings and depleting a defence against speculative attacks. He was accused of “misconduct and dereliction of duty by a public servant” which may sound familiar in today’s US context. Argentina was long a pariah in international markets, but this episode in particular didn’t help.

Venezuelan President Maduro fired his country’s central bank head, Nelson Merentes, in January 2017. One alleged reason was the messy handling of the release of large denomination banknotes. Mr. Merentes had a poor track record at containing inflation that soared to over 800% the prior year while the economy collapsed, although he had a lot of help from other policymakers. The bolivar was officially pegged to the dollar until January 2018 and a vibrant black market with alternative exchange rates thrived. Inflation soared in several bouts, the currency was revalued in 2018 and 2021. Policy mismanagement cost Venezuelans dearly.

Nigerian President Bola Tinubu fired central bank head Godwin Emefiele in June 2023. Few lamented the decision given what happened to Nigeria’s economy, inflation and markets under his watch and different administrations, yet his firing led to the collapse of the Nigerian naira from about 470 to the dollar to requiring more than three times as many naira to buy one US dollar (chart 3).

More limited examples of toying with central banks have included erratic changes to the Reserve Bank of New Zealand’s inflation mandate as governments have changed over the years. This sowed confusion in local markets and among forecasters.

Former RBI Governor Raghuram Rajan—a rock star in central banking and academia who spotted conditions in the lead up to the Global Financial Crisis—offers another example for consideration when his openness to accept another term in office was not extended by the government and so his term ended in September 2016. A theory is that his candidness concerning India’s relative economic performance and challenges the country faced put him at odds with government notwithstanding his reputation as beyond reproach. He also conflicted with government in adopting CPI-based inflation targeting and fought to preserve the RBI’s reserves against political meddling that subsequently became a larger conflict.

Another example could even be in Canada where the 2021 five-year review of the Bank of Canada’s mandate tweaked language to include more direct references to maximum employment while restating price stability as the “primary” goal.

US Specialness

Now, to be sure, 200 years ago in US monetary history and the examples above may not be entirely pertinent to the US today (though shouldn’t be ignored). The sheer size and pervasiveness of US debt markets and the reserve currency status of the US dollar connote certain advantages, such as safe haven appeal. This shouldn’t be taken for granted at a mitigating factor for two reasons.

One is that we’ve seen violations of this specialness such as following so-called ‘liberation day’ on April 2nd when Trump announced massive tariffs, and this past week when there was temporary fear that Trump was moving toward firing Chair Powell.

Second is that because firing a Fed Chair is without precedence, we would be entering uncharted waters in terms of the sequence of events that could then follow. A lawsuit in federal court, a potential challenge in an appeals court, and perhaps movement all the way to the Supreme Court would invoke lengthy delays and highly uncertain outcomes in terms of what constitutes firing for cause and whether the current allegations surrounding renovations would tick the box.

We also don’t know how the rest of the FOMC would react. Would it revert to separating the Board Chair from the FOMC Chair role and appoint their own FOMC Chair? Would there be significant resignations or threats to resign? How would credit rating agencies respond to such turmoil and what would be the potential knock-on effects on other industry ratings? What impact would such turmoil have upon already damaged consumer, business and market confidence? Would financial market turmoil and a potential liquidity crisis be followed by curtailment of foreign investment in real assets in the US? Would the Federal Reserve be in a position to respond effectively to any financial market turmoil that would probably make the regional banking crisis of 2023 pale by comparison and draw greater parallels to more extreme crises?

US Monetary Policy is About Right

Of course, the most important issue at hand is whether Federal Reserve policy is appropriate, or whether there is a case for President Trump’s view that the fed funds policy rate should be slashed down to 1% from 4½% at present.

Most economists would argue that 1% is crisis territory for the policy rate. It would be a policy rate far below the range of estimates of a neutral rate setting that hovers somewhere around 3%. And yet the administration and its supporters have argued that inflation-adjusted US economic growth can be propelled to 3%+ thanks to the ‘big, beautiful bill’ that just passed. That’s not a crisis. It’s not a recession. This is a profound internal inconsistency to their views and sound enough reason for them to keep quiet on monetary policy.

Now, since the President is privy to information that may not be publicly available, he should perhaps be called upon to explain the coming crisis facing the US economy and markets that could merit such dramatic easing of monetary policy.

More reasonable aspects of the debate are presented by voices like Governor Waller who leans toward the July 30th decision being a live one to consider a cut. It sounds like he will dissent in favour of a cut, with his view (and perhaps Governor Bowman’s) being in the clear minority on the FOMC. Waller is an inflation dove and worried about the job market. Waller’s view that tariffs are merely a temporary price level adjustment remains to be tested after such a large inflation shock in recent years that made the economy and markets potentially more vulnerable to a repeat. His concern about private sector job growth of late ignores the fact that weather adjustments to payrolls add back about 122k jobs in the past couple of months and would likely influence private jobs. Mr. Waller should perhaps explain how rate cuts would fix the weather.

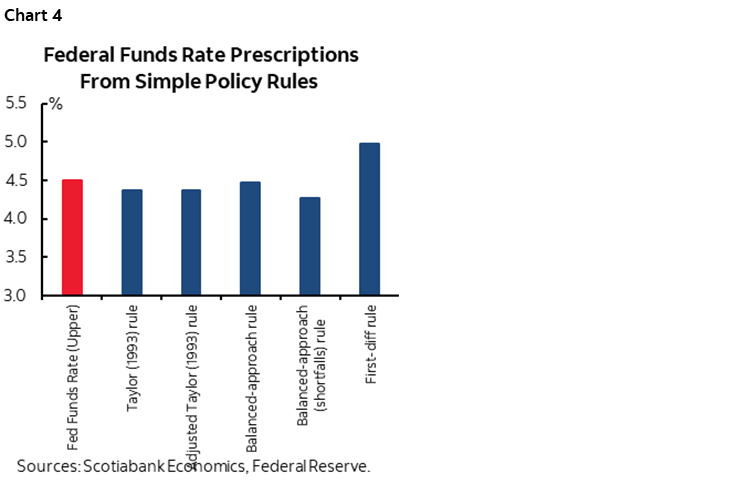

A variety of analytical models tend to show that US monetary policy is about right. As Chair Powell emphasizes, multiple variations of the popularized ‘Taylor Rule’ show policy to be about right and one would support a higher rate path than at present. These are summarized in Box 4 of the Fed’s latest Monetary Policy Report here and in chart 4.

If that’s not enough, then the Cleveland Fed offers even more approaches to evaluating the appropriateness of current monetary policy (here). Of the twenty-one different approaches (yes, 21!), fifteen show that as at the end of 2025Q2, the fed funds rate should have had a number 4 at the beginning, one starts with a 5, another a six, and four start with a 3. None come remotely close to Mr. Trump’s desired level.

More intuitively, there are two main concerns around easing prematurely. One is that the US economy remains resilient with tracking of Q2 GDP ‘nowcasts’ around 2½% q/q SAAR and including resilient nonfarm payrolls that could weaken materially further and not cause undue alarm over the unemployment rate as tighter immigration policy and forced removals shrink the labour pool. Two is that we simply don’t know if tariffs will present a one-off price level adjustment or material inflation, for how long, and whether tariffs present more risk to jobs or inflation. Until there is more clarity—which in turn requires greater confidence in the evolution of US trade and other policies that have been volatile to date—then the appropriate steps for policy cannot be judged. This makes it an empirical question to be informed patiently by data and time.

In my opinion, Chair Powell gets top marks for efforts applied to explaining such complexities and deserves the street’s full support.

Data and time may be the Trump administration’s greatest fears in this debate. Peak pressure is being applied on Powell now because of the concern that tariffs will pass through inflation in more material fashion over coming months and quarters and make it increasingly difficult to ease monetary policy. Relatively tight monetary policy along high tariffs and other Trump administration policies could present serious challenges to the fragile majorities held by the GOP in both chambers of Congress on November 7th 2026.

Which brings the conclusion that candidates for the top job should turn down the heat and turn up the substance. Currying favour with Mr. Trump against the empirical considerations surrounding the suitability of current monetary policy is a damaging pursuit by some of the most pointed critics. It helps no one over time while creating the impression that these candidates would be too close to the administration’s whims.

CENTRAL BANKS—BUSY CALENDAR ABSENT SPICE

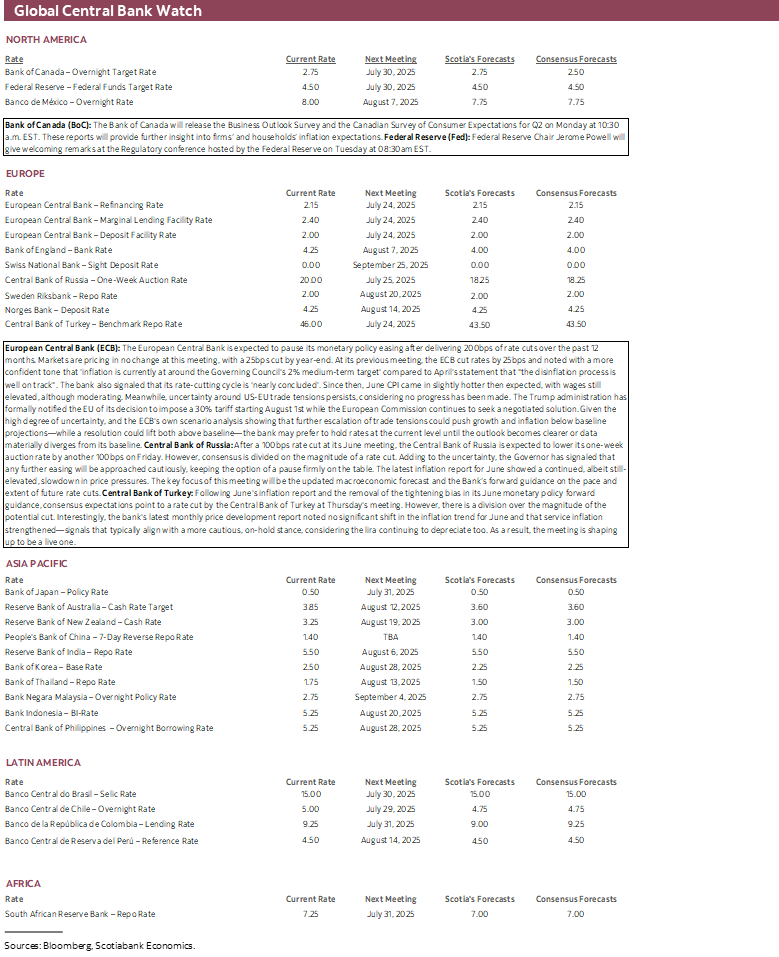

While the central bank calendar has several entries on it for the coming week, none of them are likely to be earth shattering in terms of market consequences. In fact, they could come and go with relatively little fanfare. The ECB, Central bank of Turkey and Central Bank of Russia deliver policy decisions to accompany a Federal Reserve conference on bank capital, RBA minutes and BoC surveys ahead of the following week’s decision.

European Central Bank—We’ve Done Enough

Markets are priced for the ECB to hold the deposit rate on Thursday at an unchanged 2%. Consensus also expects a hold. President Lagarde said on June 5th after cutting by 25bps that “We are getting to the end of a monetary-policy cycle that was responding to compounded shocks—including Covid, the illegitimate war in Ukraine and the energy crisis. At the current level of interest rates, we believe that we are in a good position to navigate the uncertain conditions that will be coming up.”

Since then, GDP growth exceeded expectations at 0.6% q/q SA nonannualized (0.4% consensus) and core inflation has held firm at 2.3% y/y. The policy rate lies within the ECB’s estimated 1.75–2.25% neutral rate range. As defence spending plans across Europe ramp up and trade tensions with the US pose uncertain risks to inflation, the ECB’s best course of action for now is to hold.

Federal Reserve Capital Conference

Federal Reserve Chair Powell delivers opening remarks on Tuesday at a Fed conference on the regulatory capital framework (here). Otherwise, the FOMC is in blackout until one day after the July 30th decision.

Bank of Canada Surveys

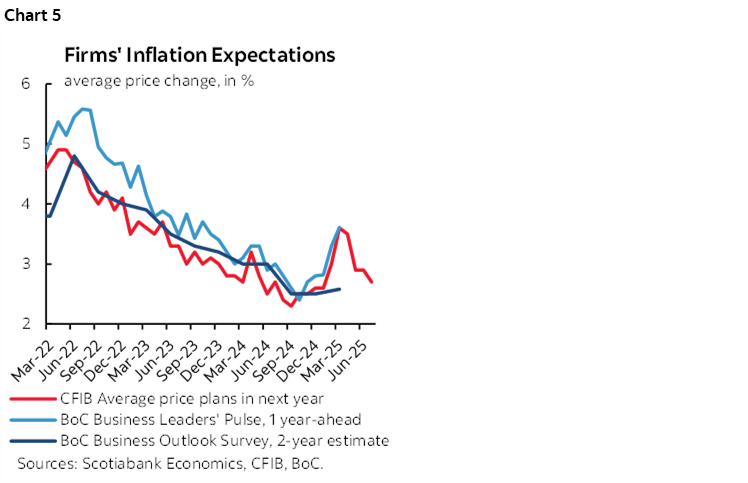

The Bank of Canada releases its quarterly pre-MPR surveys of businesses and consumers on Monday. One of the key sets of measures concerns expected price pressures. An advance indicator of small business price expectations serves as a leading indicator for the BoC’s surveys and suggests they will show less concern (chart 5). A caveat is that the BoC surveys are more skewed toward larger businesses. Of course, a risk is that these are merely sentiment-driven gauges that could be stale now since Trump has been escalating tariff risks all over again.

RBA Minutes May be Stale

RBA minutes to the meeting that resulted in the surprise hold on July 8th might further inform the bias going forward. Key could be defining “a little more information” on inflation progress that may come on July 29th when Q2 readings are provided. Developments since the decision have made the minutes a little less relevant given back-to-back weakness in jobs reports.

Turkey’s Central Bank Likely to Ease

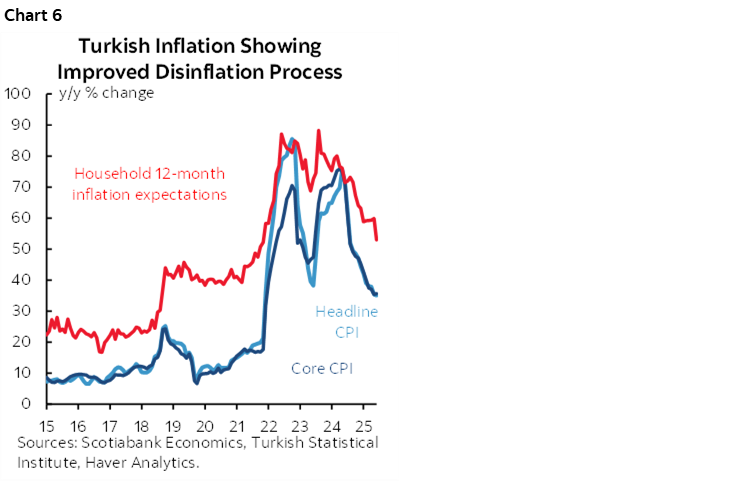

Forecasting Turkey’s central bank is only for the bravest among us. While the magnitude is often a wildcard, some forecasters expect the Central Bank of Turkey to restart monetary easing on Thursday. The 1-week repo rate had been reduced from 50% in December to 42.5% by March before a 350bps hike the next month. Erratic you might say. Inflation has ebbed, but remains elevated at 35% y/y (chart 6) and ongoing weakness of the lira that poses consistent upward pressure on import prices could well motivate additional tightening if it were not for the fact that the tightening bias was removed from the last statement.

Central Bank of Russia—Pause with Cut Risk

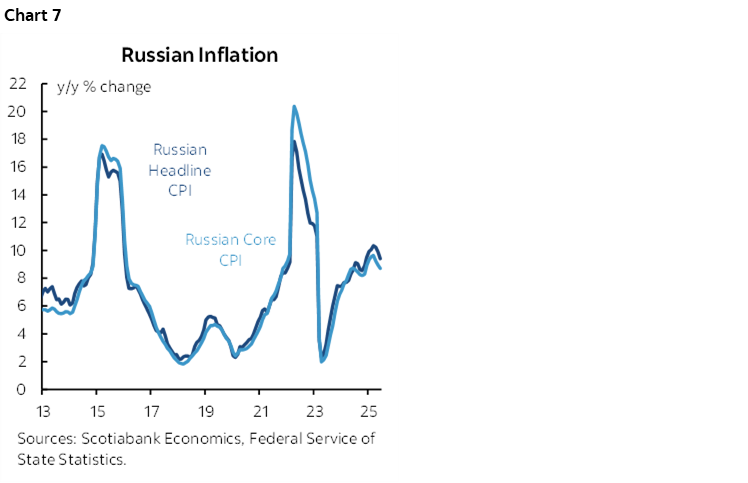

After cutting by 100bps on June 6th, Governor Nabiullina advised that further easing was to be approached with caution and that pauses with hike risks could pepper the path forward. She also noted that a hold was also considered which indicates that there may not be confidence to follow up easing with another cut. Most of consensus nevertheless anticipates a sizeable cut as inflation may be cresting (chart 7).

GLOBAL MACRO—PMIS THE FOCAL POINT

Earnings and PMIs will be the main focal points beyond central banks, along with a smattering of other global indicators.

A main focus on the data calendar will be purchasing managers indices that reveal global evidence on growth momentum, supply chain pressures, hiring appetite and inflation risk. Australia and Japan will kick off the readings on Wednesday evening (ET) followed through the overnight into the N.A. session when readings arrive for France, Germany, the Eurozone tally, the UK, US and India. Composite PMIs for every one of these regions is signalling modest growth except for India that is still signalling fairly rapid growth.

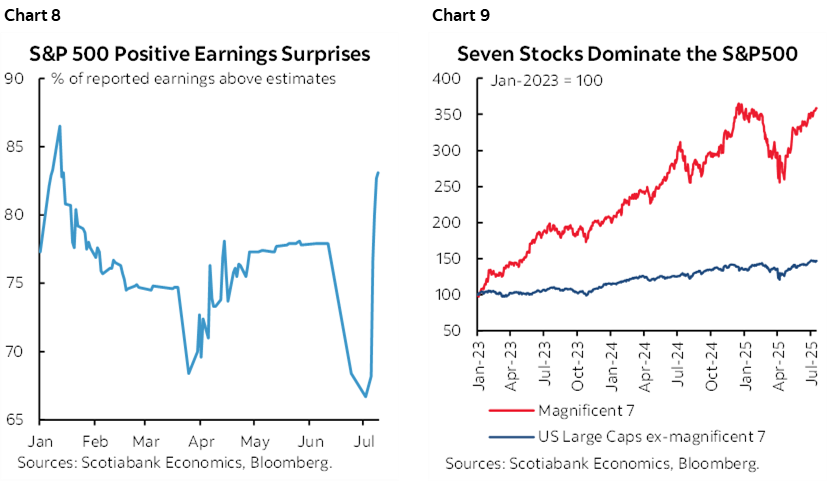

The Q2 US earnings season broadens out and intensifies this week. 104 S&P500 firms release over the coming week and the names diversify beyond the usual early focus upon financials. Positive surprises are encouraging so far (chart 8). Some of the ‘magnificent 7’will lead the way with earnings reports including Tesla, Alphabet, and Intel, although some are recently more magnificent than others. As a group, they’re back to outperforming the broader market that has returned toward performance being highly concentrated in a handful of names (chart 9).

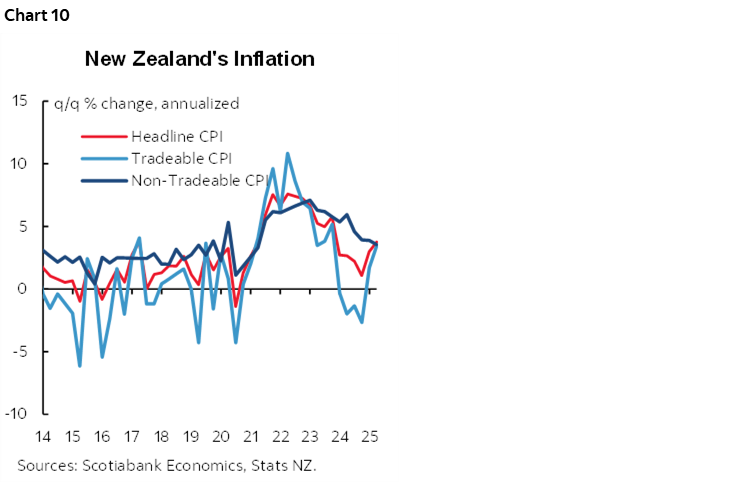

RBNZ watchers will keenly follow Sunday’s Q2 CPI readings for New Zealand which is the last set of readings before the August 20th decision for which markets presently assign about 60% odds of a rate cut. The prior report showed accelerating inflation (chart 10). When the RBNZ paused at its last decision, it noted “the benefits of waiting until August in light of near-term inflation risks. Some members emphasized that waiting would allow the Committee to assess whether weakness in the domestic economy persists, and how inflation and inflation expectations evolve. It would also allow more time to observe developments in the global economy."

More minor readings will focus on retail sales out of the UK (expected to rebound) and Canada (expected to dip) on Friday. The US calendar will focus upon mixed housing readings including resales (Wednesday, slip expected) and new home sales (Thursday, rebound expected) plus big-ticket durable goods orders (Friday) that are likely to reverse some of the prior month’s surge that was driven by airline orders. BoJ watchers will also be interested in Thursday’s July reading for Tokyo core inflation.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.