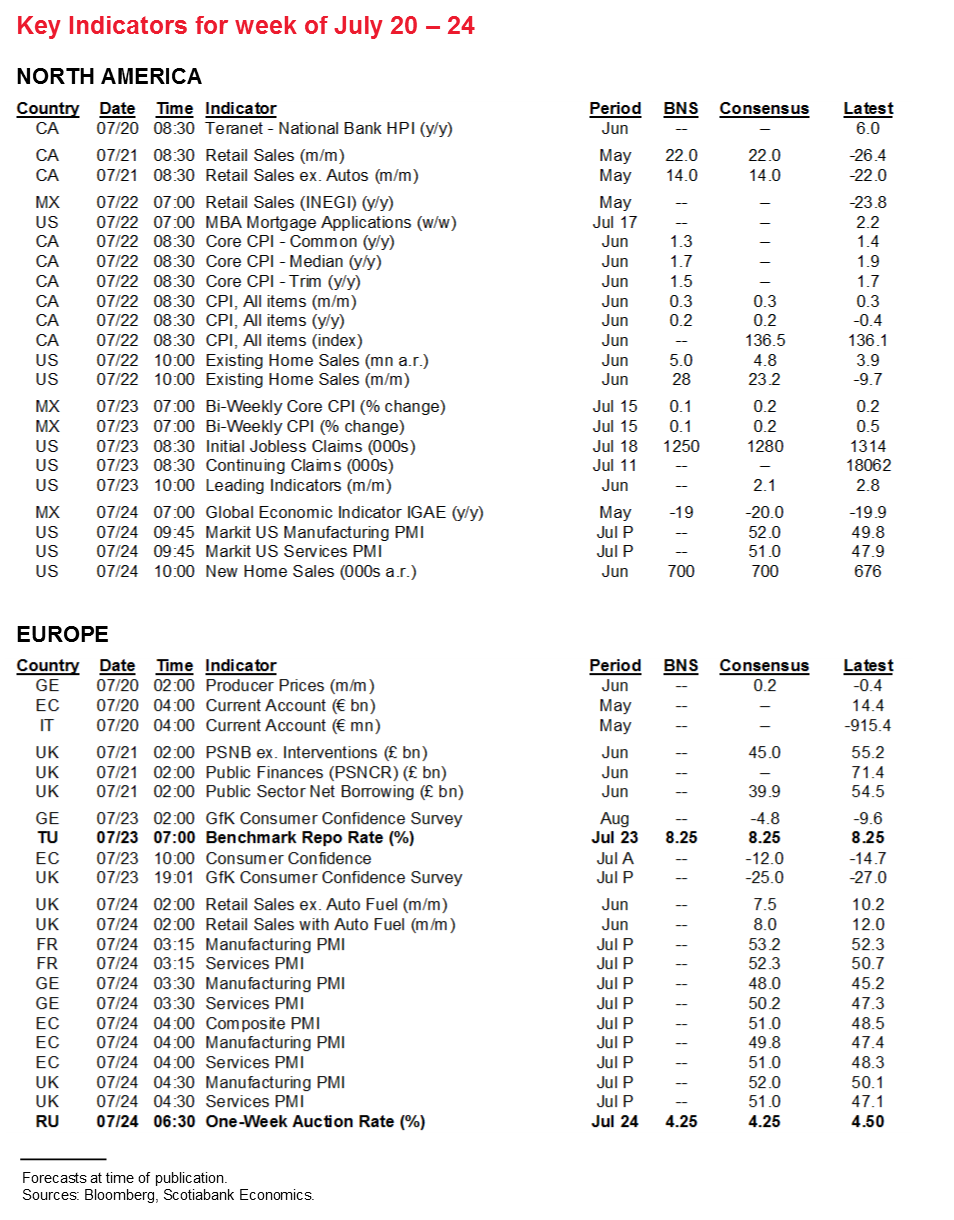

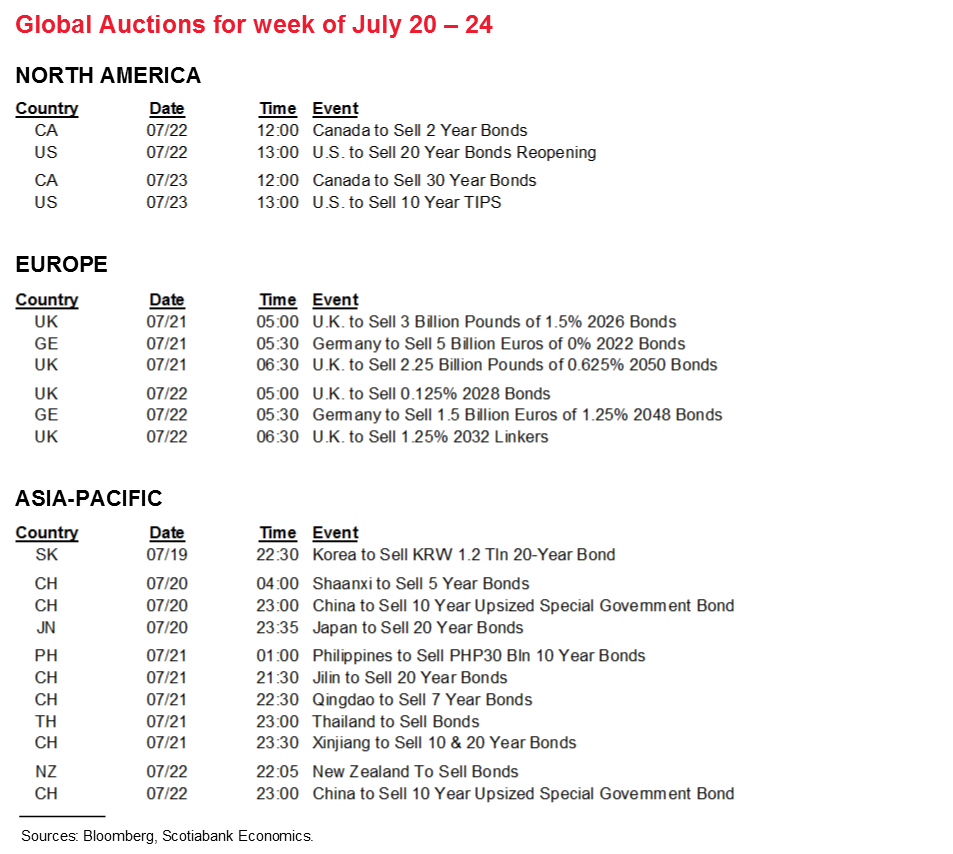

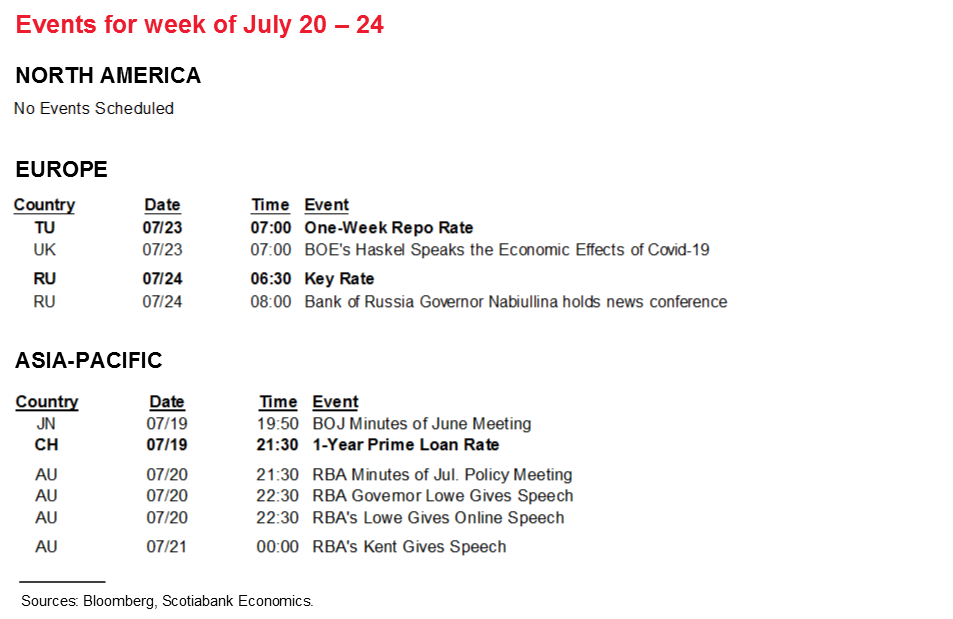

Next Week's Risk Dashboard

• EU Summit

• PMIs: EZ, US, UK, Japan

• CDN CPI, retail sales

• Fed expectations

• Earnings

• US housing

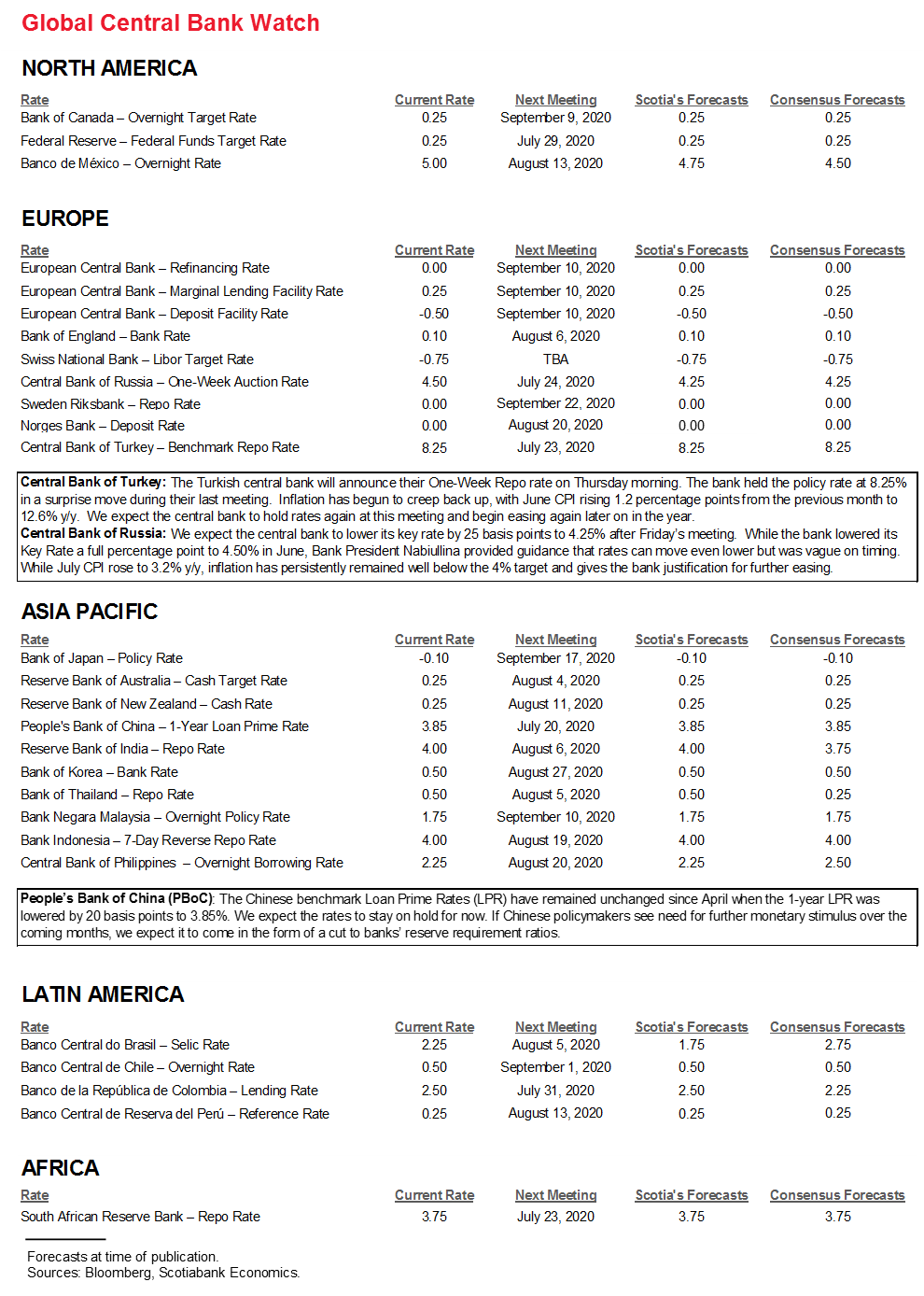

• CBs: PBOC, Russia, Turkey

Chart of the Week

CANADA—‘V’

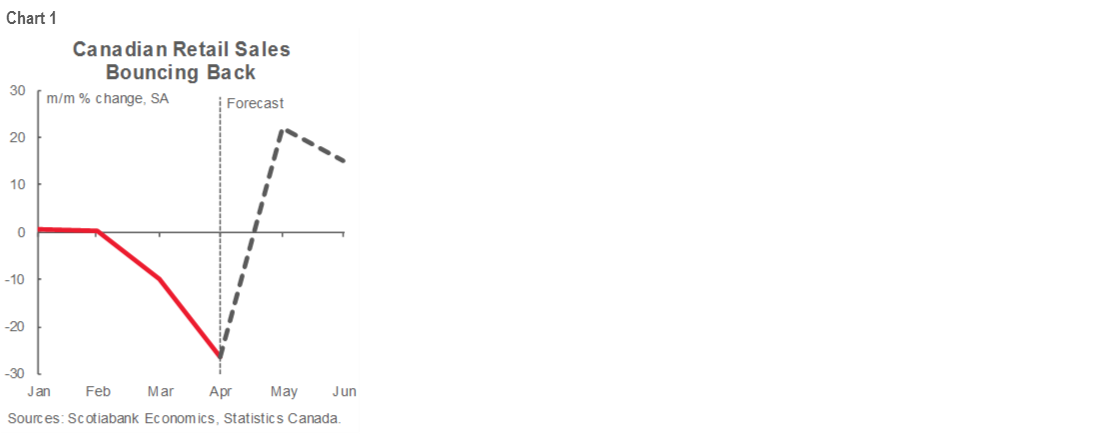

The week’s main event may be evidence that Canadian retail sales are already clawing back much of the COVID-19 related decline (chart 1). Headline inflation may also return to being marginally positive while masking softness beneath. Earnings guidance may also be instructive by way of anecdotes on economic behaviour.

Tuesday’s retail sales report for May will hopefully also include preliminary guidance for June and thus provide a more informed snapshot of the full quarter. StatsCan guided on June 19th that its preliminary estimate for May’s reading was a gain of 19.1% m/m in value terms while cautioning that revisions should be expected. I went with +22%. Auto sales volumes were up by 127% m/m with an 11% weight on the overall new car dealer category. Sales ex-autos are expected to rise by 14%. There is high risk around both estimates, but a strong snapback is likely.

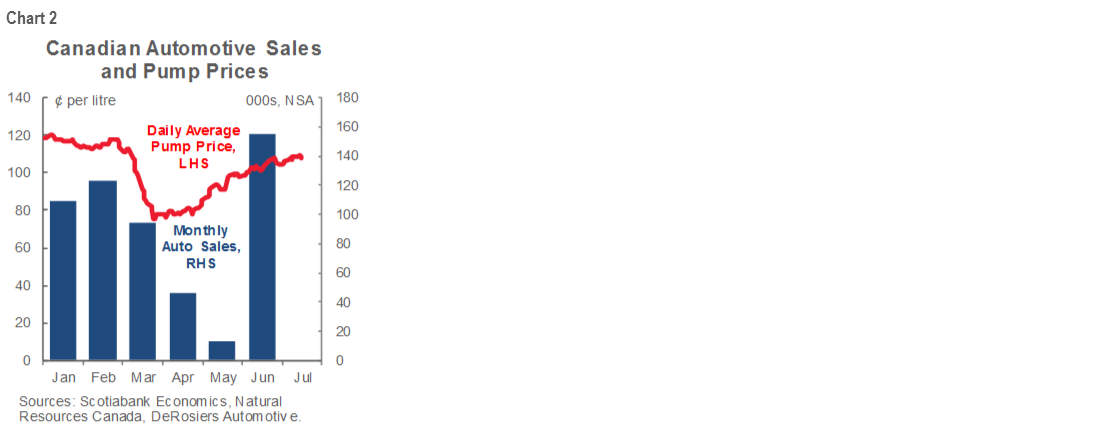

As for a preliminary June reading, expect it to further the recovery evidence with very possibly another double-digit percentage gain. Auto sales were estimated to have risen by nearly 50% m/m seasonally adjusted last month. Gasoline prices also climbed. The rise in both measures is shown in chart 2. More important—at least to sales ex-autos and gasoline—may be that provincial economies furthered their reopening plans for nonessential retailers. I found this to be a handy summary of reopening timelines by province. Supplementing the main drivers of the call is evidence that some forms of payments transactions have sharply picked up (here).

CPI inflation for June will be updated on Wednesday. Headline inflation should go positive again in year-over-year terms for the first time in three months. Don’t get too excited by this, however, in that the drivers are unlikely to cause much of a thrill at the Bank of Canada. A combination of favourable year-ago base effects, muted seasonal influences at this time of year, higher gas prices that alone should add about ½% to the year-ago rate, and soft pricing power across the rest of the basket will net out to a firmer headline but probably softer core readings. Watch for 0.3% m/m CPI and 0.2% y/y plus slight downticks in the common component, weighted median and trimmed mean ‘core’ gauges.

Canada’s earnings season usually lags the US season, but 18 TSX-listed firms will report next week including names like CN, Rogers, CP and Loblaw. Guidance on pandemic-related spending, streaming activity and rail transport can help to supplement data with anecdotes on the recovery.

UNITED STATES—THE RECOVERY ROAD TO MORE STIMULUS?

As the Federal Reserve slips into communications blackout this Saturday through to the day after the July 29th FOMC announcements, macro reports and earnings will further inform recovery progress.

Speculation toward further Fed policy options on the path to the next meeting intensified somewhat after former Fed Chairs Bernanke and Yellen testified to Congress on Friday. Their joint written remarks are available here. They indicated the possibility that the Fed will adopt condition-based forward guidance (not time or hybrid) dependent upon the state of the economy and that they might implement yield curve control at the 2-year part of the Treasury curve. That such options are possible is not surprising. That Yellen and Bernanke delivered the message combined with guidance it may arrive “in coming months” is useful information.

Recall that the Fed’s strategic review to date has tended to dismiss longer-term yield targeting given the potential difficulty between credibly balancing a very long-term yield target with the possibility that at some point the Fed’s policy rate may begin to drift back upward again. That said, Chair Powell has sounded less than enthused even toward yield curve targeting in general given how low yields are now and mixed evidence on its efficacy. That might make a policy shift as soon as July 29th unlikely, with subsequent meetings scheduled for September 16th, November 5th and December 16th. Note, however, that they have proven they do not need formally scheduled meetings to act, if needed.

It may, however, turn out to be the case that further initiatives get packaged together upon presentation of the Fed’s completed strategic review that NY Fed President Williams recently indicated may be completed before the end of 2020. If so, then the Fed may find it more powerful to communicate a broader set of tools simultaneously, like a formal shift toward symmetric average inflation targeting that implies a catch-up period from years of undershooting its 2% inflation target, alongside yield curve targeting and strengthened forward guidance. The net effect might allow the Fed to ease up on actual Treasury purchases in favour of daring the market to challenge its intent, while simultaneously reaffirming its intent to keep rates low for possibly many years. If the Fed were to adopt strengthened forward guidance soon, it would follow central banks like the Bank of Canada, but could lead along with the RBA toward targeting shorter term yields.

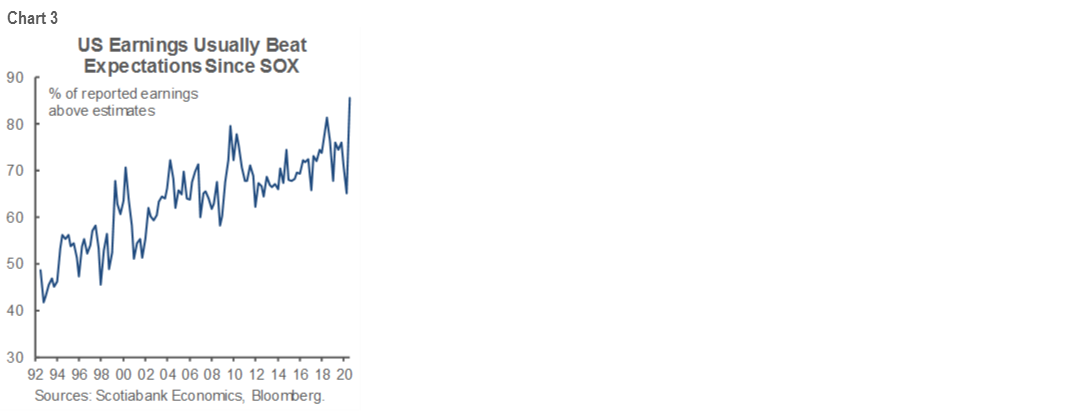

Eighty-six S&P500 firms will release earnings next week including names like Twitter, Microsoft and Intel. Chart 3 shows how well this earnings season is going– relative to expectations, that is. In absolute terms it’s a mess, but just not as big a one as anticipated. 85% of the ten percent of S&P500 firms that have released so far have beaten analysts’ expectations.

Macro reports should further recovery evidence on a relatively light schedule focused upon housing and purchasing managers’ indices.

Existing home sales during June (Wednesday): There was a massive 44% rise in pending home sales during May (June arrives at month end) and most of that should show up within two months when the paperwork settles and keys exchange to show up as completed resales. June’s completed sales are pencilled in at +28% m/m.

Jobless claims (Thursday): Did the latest week’s reading reveal stalled progress toward declining numbers because they were pushed higher from the prior week’s holiday interruption? If so, then they should resume a downward march over the next couple of weeks. Another possibility remains that an interruption in reopening plans across some states—while others like New York expedite plans starting on Monday—could further stall progress.

Markit July PMIs (Friday): We could see the traction of further recovery push PMIs across the 50 line for composite, manufacturing and services and into expansion territory.

New home sales during June (Friday): This is arguably more important as a housing indicator than resales because the sales get recorded in timelier fashion. Thus, as a sentiment gauge toward appetite for home buying it will be more informative. Revision risk is always substantial, but a milder gain than the prior month’s 17% rise would seem to follow the tone of other readings like mortgage applications.

EUROPE—RECOVERY SANS FUND?

Recovery evidence into the third quarter and the aftermath of the European Union Summit could dominate developments into next week.

How is the recovery proceeding into the third quarter within the Eurozone and UK? Friday’s purchasing managers’ indices will reveal useful new information. In both cases—and like the aforementioned US Markit gauges—we could see the first returns to the right side of 50 that signal outright economic expansion that is mirroring reopening plans. Both regions have gone V-shaped with their PMIs to date but have yet to cross back above 50 (see front cover chart).

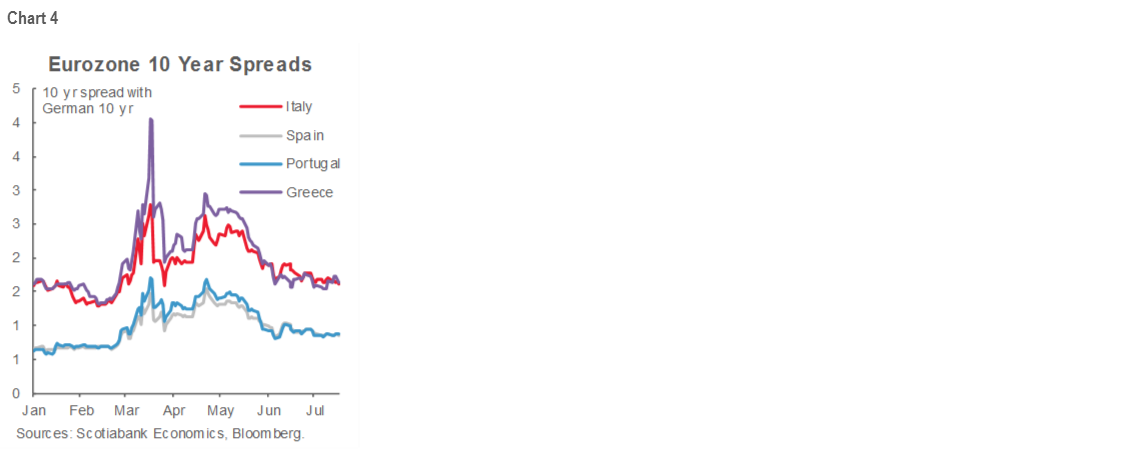

The Asian market open on Monday may be sensitive to developments upon the conclusion of the EU Summit on Saturday. At issue is ideally sudden swift agreement on contentious matters surrounding the €750B recovery fund or—much more likely—agreement to return to the negotiating table to complete the dialogue sometime soon. If achieved, then movement toward a form of transfer system, common debt issuance and a common long-term budget would be major steps forward toward stronger overall integration and unity. Indeed, it would be a substantially new framework that delivers on important steps to complement monetary union; the absence of fiscal union has been a longstanding missing ingredient. The substantial tightening of Eurozone debt spreads over German bunds has been driven by ECB actions as well as the announcement on April 23rd that EU leaders would work toward a recovery fund concept (chart 4).

Turkey’s central bank is expected to hold its policy rate unchanged at 8.25% again on Thursday amidst a pick-up in core inflation from a trough of 6.7% y/y in October 2019 to 11.6% last month. Most economists expect Russia’s central bank to cut by 25–50bps on Friday.

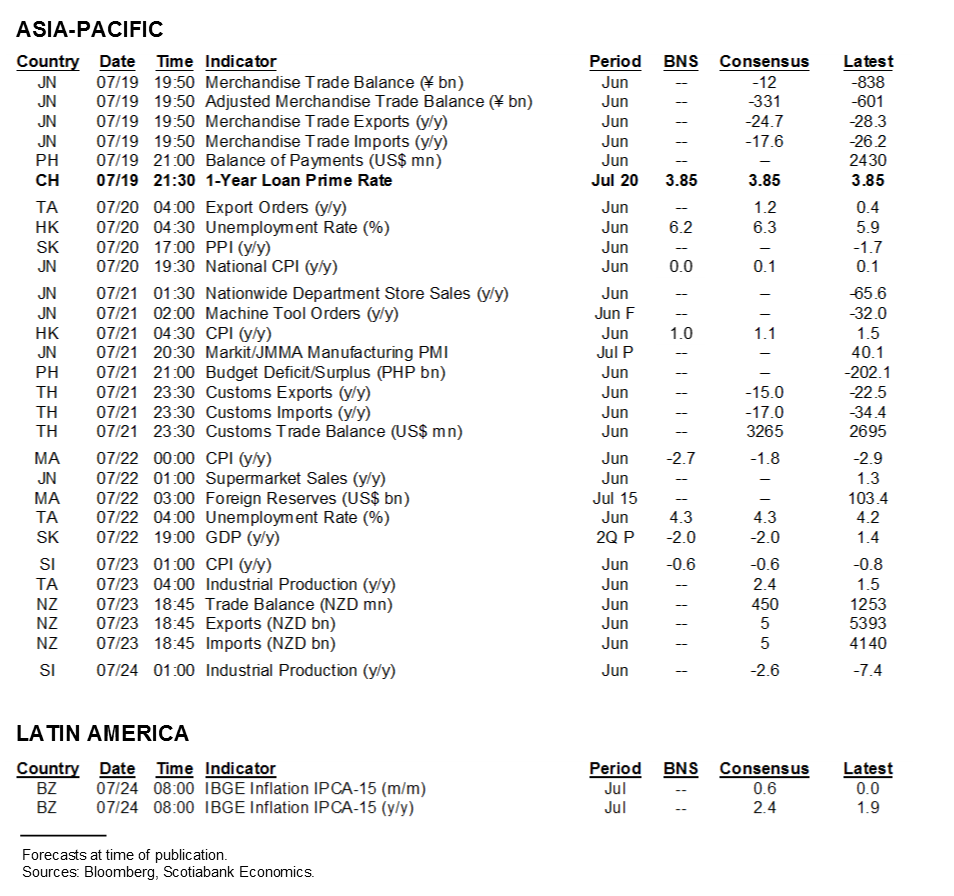

ASIA-PACIFIC—JAPAN’S RECOVERY LAGS

Asian calendar-based risk should be light and largely inconsequential to global markets over the coming week.

The People’s Bank of China is expected to keep its one and five year Loan Prime Rates on hold at 3.85% and 4.65%, respectively, on Sunday night into the Asian Monday market open. The PBOC has guided that it is leaning more toward a pick-up in credit growth plans this year rather than adjusting the policy rate that has held steady over the past couple of months.

Japan will update its Jibun purchasing managers’ indices for June on Tuesday night. They have generally lagged progress elsewhere across PMIs in the Eurozone, UK, US and China. July’s readings may close some of the gap and indicate further progress toward an economic rebound (chart 5).

LATIN AMERICA—LIGHT CALENDAR RISK

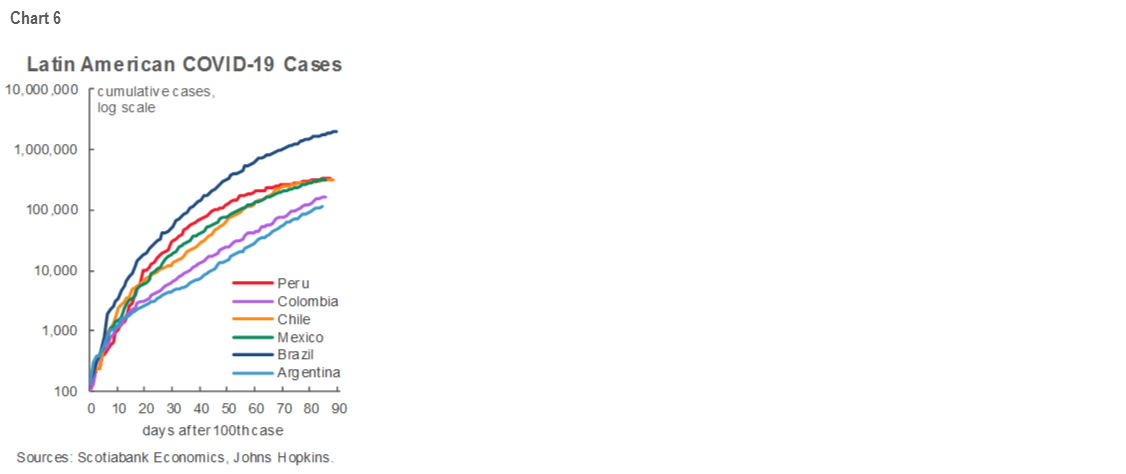

Endless debt restructuring talks in Argentina are making progress and a mid-month inflation reading out of Brazil will offer light regional market risk compared to what remains the dominant issue of tracking COVID-19 cases and ramifications for the local economies. Chart 6 offers an updated depiction of the magnitude of the challenge.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.