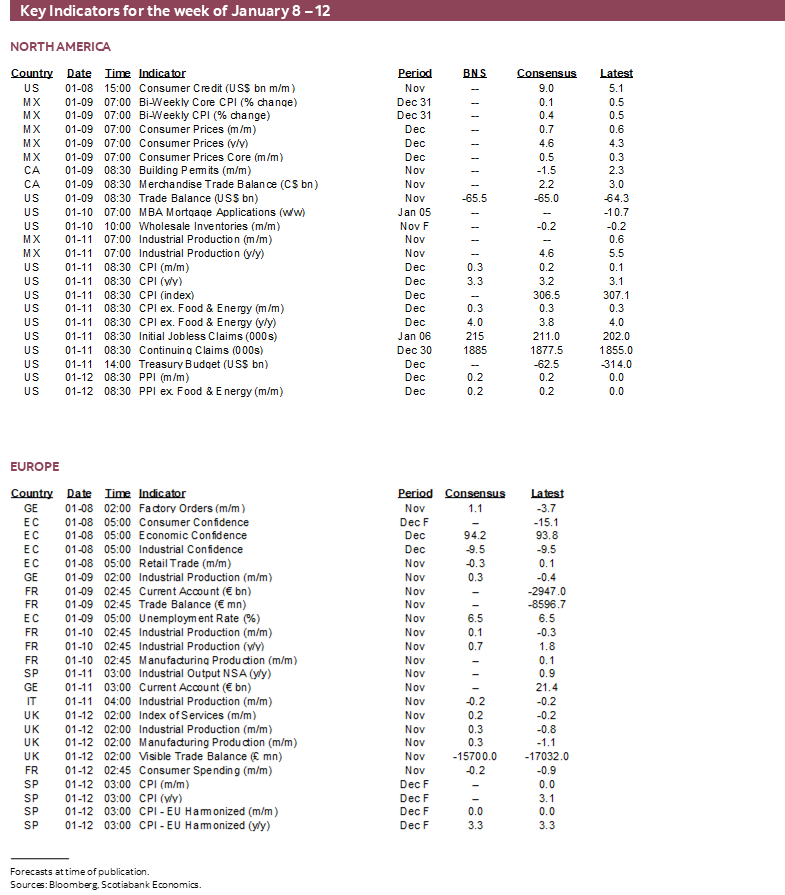

Next Week's Risk Dashboard

- Markets push out and reduce rate cuts

- Is the US core CPI inflation trend still too warm?

- Tracking and updating global progress on inflation relative to central bank pricing

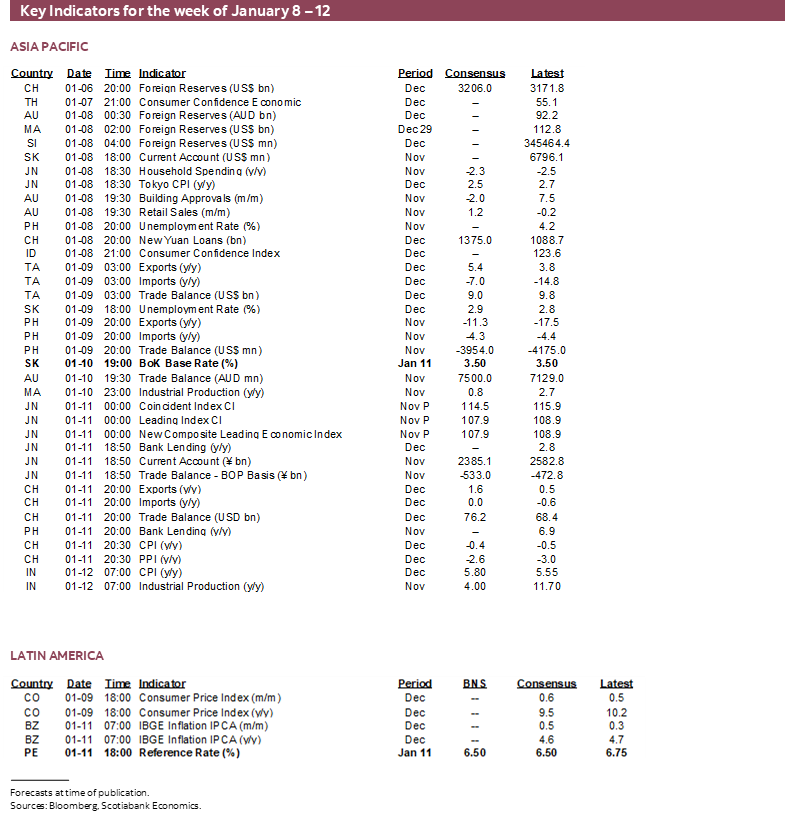

- CPI: LatAm, Tokyo, China, India, Switzerland, Australia, Norway

- US banks to kick off another earnings season

- Peru’s central bank expected to cut again

- Bank of Korea will likely extend hold

- Global macro readings focus on Germany, UK

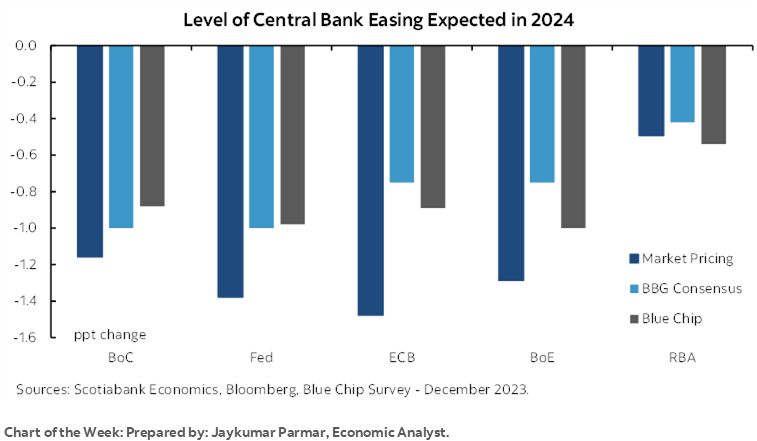

Chart of the Week

If the first week of the new year offers any guide in terms of what to expect, then this is going to be a wild year in the markets and one that makes it unwise to be too confident that full-year projections that typically flood inboxes at this time of year will prove to be correct. As sometimes quipped, the purpose of a forecast is to have something to revise especially during exceptionally uncertain times.

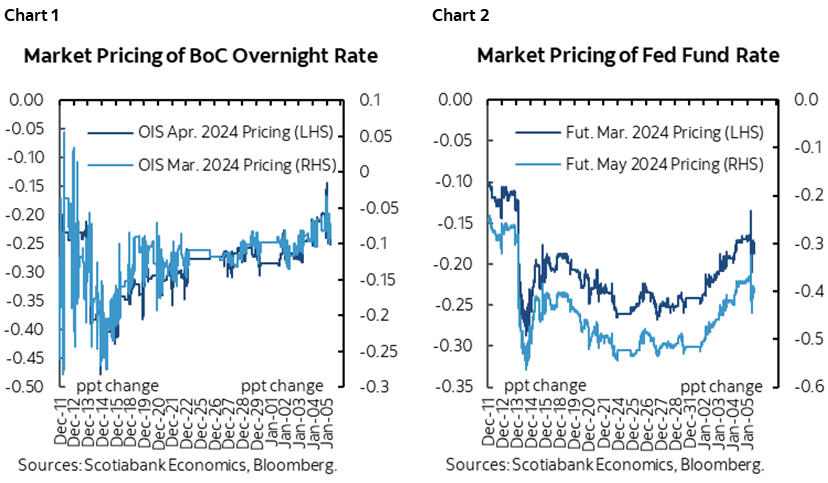

Bonds spent the week selling off while the USD strengthened across most major currencies. A big part of the reason is that markets scaled back bets for the start of a rate cut cycle as shown in charts 1 and 2. This fits my view that markets had gotten too carried away pricing cuts over the final weeks of 2023. Data helped to drive this reassessment given strong job growth and wage growth in the US (recap here) and very strong wage growth in Canada as job growth took a third breather in what was an incredibly strong year marked by 430k jobs created (recap here). Added catalysts for the market reassessment could stem from the ability to start a new year freed from the pressures of blowing performance into year-end and with a fresh start for portfolio managers after the holiday period.

Data will inform the path central bankers may embark upon and more key data arrives as this week’s focal points. This will include US CPI and a round of inflation reports from across the world. It will be a light week for central bank decisions, but earnings risk takes over beginning with the US banks.

US INFLATION—PLACEHOLDER AS MARKETS REDUCE RATE CUT PRICING

Thursday brings out the final CPI print before the January 31st FOMC meeting and will inform expectations for the Fed’s preferred PCE measure of inflation on January 26th. Nothing is expected from that statement-only outcome and markets are reducing bets for rate cuts at the March 20th and May 1st meetings. The winning trade through the holiday season into the new year was to pay those contracts.

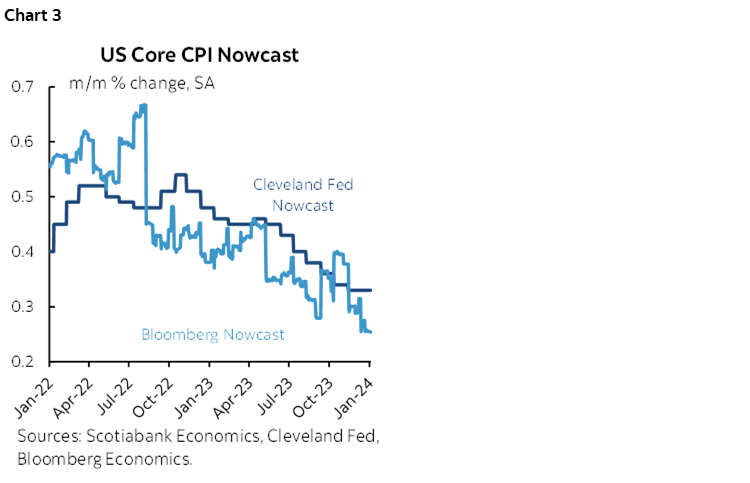

I have estimated the final readings for 2023 at 0.3% m/m SA for both the headline and core CPI. This time the estimates happen to be close to nowcasts with the caveat that nowcasts have tended to overestimate the readings including two examples that are shown in chart 3, though don’t ask me how on earth daily updates of inflation nowcasts are credible.

Among the expected drivers are the following:

- Gasoline prices were down by 5.2% m/m NSA. Since gas prices are normally a bit weaker in December the seasonal adjustments translate this into a nearly flat m/m contribution to headline CPI such that it shouldn’t matter to the difference between headline and core CPI.

- Food prices are not expected to be a material contributor. Therefore, here too there should be little reason to expect a difference between headline and core CPI in m/m terms.

- Owners’ equivalent rent and rent of primary residence are tracking further increases of about ½% m/m SA.

- Core service prices (ex-housing and energy services) are expected to rise by 0.3% m/m SA.

- Seasonally adjusted vehicle prices could contribute a touch to headline and core CPI through a mild rise in new vehicle prices. Used vehicle prices were little changed.

The week ends with December’s producer price index on Friday.

GLOBAL INFLATION—VARIED PROGRESS

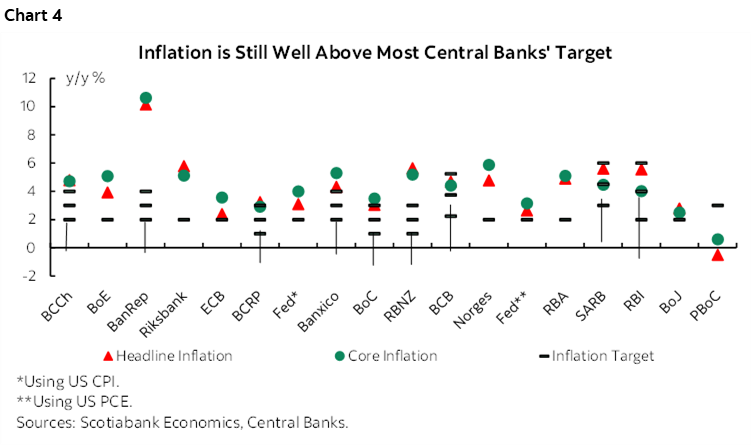

The US won’t be the only country to update inflation readings for the month of December as a slew of reports will arrive throughout the week. Chart 4 shows the highly differentiated degree of progress in brining headline and core inflation toward central bank targets at least in terms of year-over-year measures.

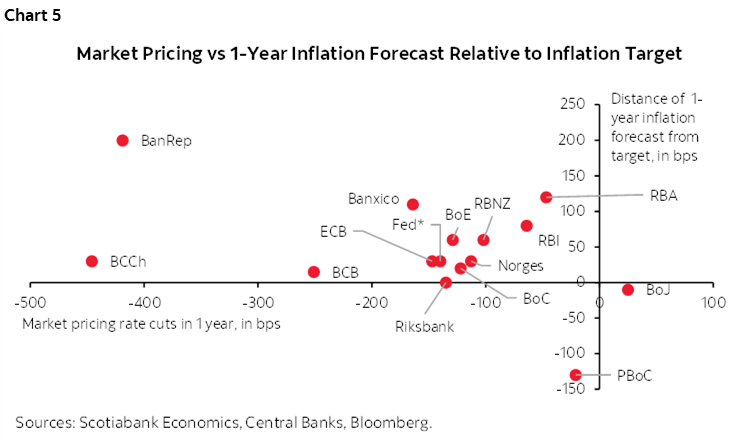

There is at best a loose correlation between what markets are pricing for expected easing and progress to date on inflation relative to inflation targets. The relationship doesn’t improve very much using expected easing and expected inflation progress using consensus forecasts (chart 5).

Here’s a quick rundown of expectations by country in chronological order.

- Chile (Monday): Total CPI inflation has tumbled from a peak of about 14% with inflation ex-food and energy peaking at about 11% y/y in mid-2022 to about 4¾% in both cases in November. December’s reading will likely take them under 4½%. That remains above the central bank’s 3% target for the two-year period for now, but the central bank is forecasting a return to 3% this year. This is why BCCh has been slashing its policy rate by 300bps so far from a peak of 11.25% up to last July.

- Switzerland (Monday): Swiss inflation is already quite low and comfortably within the Swiss National Bank’s 0–2% inflation target range. December’s update is expected to remain around 1½% y/y. This is just a placeholder, however, since the SNB will consider two more inflation reports after this one before its next policy decision on March 21st that it as likely to be influenced by ECB developments as it is likely to be affected by domestic considerations and franc stability given the CHF’s roughly 7 cent appreciation to the USD since early October.

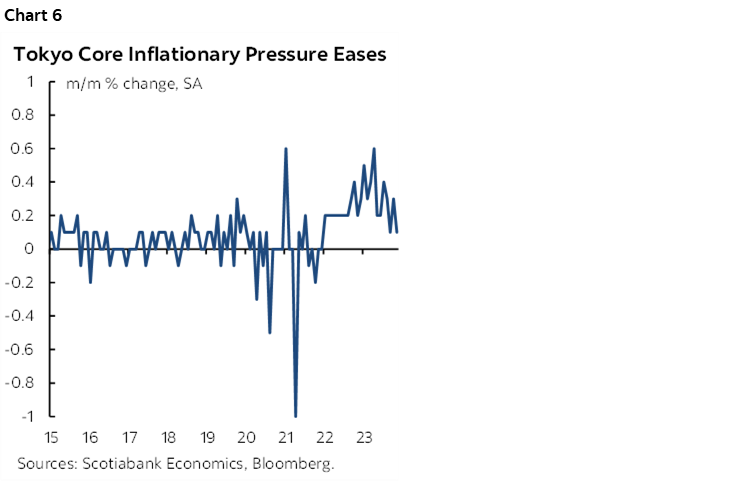

- Japan (Monday): Monday’s Tokyo CPI measure will provide a fairly accurate sense of what to expect when the national CPI figure is updated on the 18th and hence just ahead of the Bank of Japan’s next policy decision on January 23rd. Core Tokyo inflation ex-food and energy has modestly decelerated from a peak of 4% in August to 3.6% y/y in November. More telling, however, is that core inflationary pressures at the margin as measured by m/m SA changes in CPI ex-food and energy have rapidly dissipated (chart 6). The lagging effects of prior yen depreciation and earlier peaks in oil prices on higher underlying inflation may be maturing. That could continue to make the BoJ cautious with respect to moving away from negative rates as it monitors Spring wage negotiations.

- Australia (Tuesday): This update will lag the rest of the global reports as it covers November. Headline inflation has only moderately waned to just under 5% y/y with core at just over 5%. Trimmed mean CPI is tracking a little above core at 5.3% y/y. The RBA targets total inflation at between 2–3% and so readings like these continue to be unacceptably high which is one explanation for why market pricing for RBA rate cuts later this year is not as aggressive as it is for other central banks. Markets are only pricing just over a half percentage point cut over 2024H2 and conditional upon a lot further improvement in inflation readings. All that said, the full Q4 estimates on January 30th may be more informative that this week’s monthly figure.

- Mexico (Tuesday): Tuesday’s update is one of two reports before Banxico’s next policy decision on February 8th. Further progress is expected to show core inflation ebbing to just above 5% y/y from a peak of 8 ½% back in November 2022. A better depiction of this progress is offered by chart 7 that shows how rapidly month-over-month core inflation has decelerated toward pre-pandemic and seasonal norms. This is why markets are pricing significant easing over the coming year with the overnight rate priced to decline by almost two percentage points, although the starting point is likely to be significantly affected by what the Fed does and how the peso responds. Broad dollar weakness has contributed to the nearly 8% appreciation by MXN since the end of October.

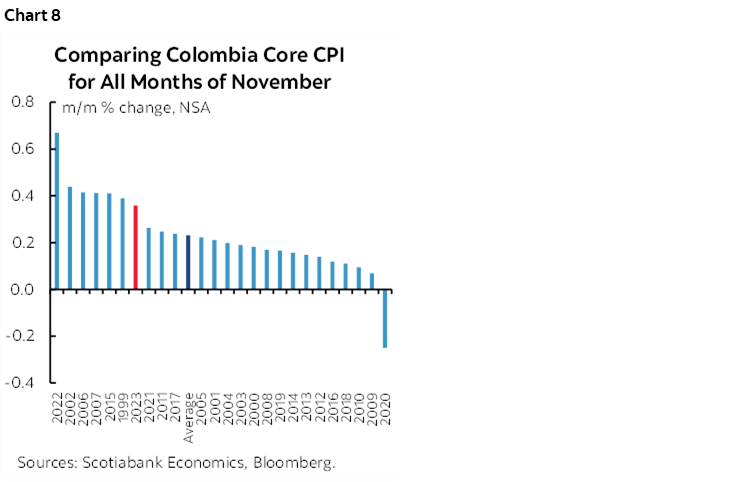

- Colombia (Tuesday): You know all that talk above about progress toward lower inflation? That doesn’t apply as much to Colombia. Inflation is still at a screaming rate of 10.2% y/y which is down from the peak of 13.3% peak in March, but the month-over-month pressures remain acute (chart 8). Headline inflation is likely to fall below 10% y/y next week but core inflation is expected to remain above 10%. Markets are aggressively pricing easing over the coming year that will require rapid progress on inflation as the economy flirts with a recession following a 1% contraction in Q2 and very little growth in Q3 with Q4 pending release in mid-February.

- Norway (Wednesday): Norges Bank has guided that it expects to keep its policy rate at 4½% “for some time ahead” in signalling the end of its hike cycle after raising the policy rate by 25bps in December. Markets are challenging this by fully pricing a 25bps rate cut in May. This contrasts with the central bank’s published explicit guidance in its MPR (here) that said they will keep the policy rate at the current level “until autumn 2024” before reducing it by up to 150bps by the end of 2026. Having said that, they did hedge their bets by speaking to both tails in noting they were prepared to raise again if needed, but the rate “may be lowered earlier than currently envisaged.” Enter inflation, the krone and oil prices as among the determining factors. Inflation is under 5% y/y with core under 6% and December’s updates are likely to show further progress toward the 2% target. The krone has appreciated by about 8% to the USD since early October. The terms of trade remain constructive, but much less so with the Brent oil price benchmark about US$18 off the peak in September.

- Brazil (Thursday): There isn’t much that is going to get in the way of Banco Central do Brasil’s plans for further rate cuts as it delivers among the most aggressive easing campaigns anywhere in the cycle to date. The Selic rate has fallen by 200bps to 11.75% from the peak last summer. December’s inflation reading will likely bring the year-over-year rate under 4½%. That could bring it barely within the BCB’s inflation target range of 3% +/- 150bps amid expectations for further progress that would merit additional easing. Markets are pricing on the order of 250bps of additional easing this year.

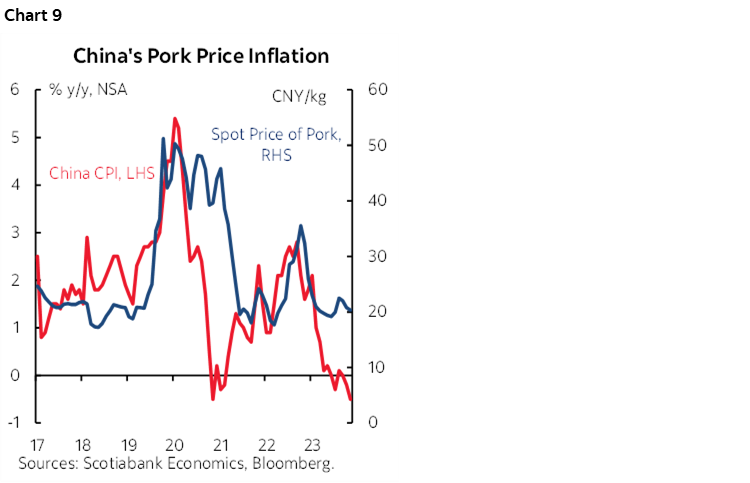

- China (Thursday): Deflation it is not, at least not yet, but I’m sure the sensational median headlines will scream out the word once more when China updates CPI for December. The update could push further below -0.5% y/y in the prior reading given weaker energy prices. Core inflation remains marginally positive and has been bouncing around ½% y/y which fails the deflation test. Breadth also doesn’t support the required definition of deflation to be a sustained, economy-wide decline in prices that is expected to persist and that alters behaviour. Services prices are up by 1% y/y. Falling food prices (-4.2% y/y) are the main driver of weak CPI especially pork prices. As chart 9 shows, the year-over-year effects of waning pork prices should stabilize into 2024 as the year-ago comparison to surging prices in 2022 drops out of the calculations.

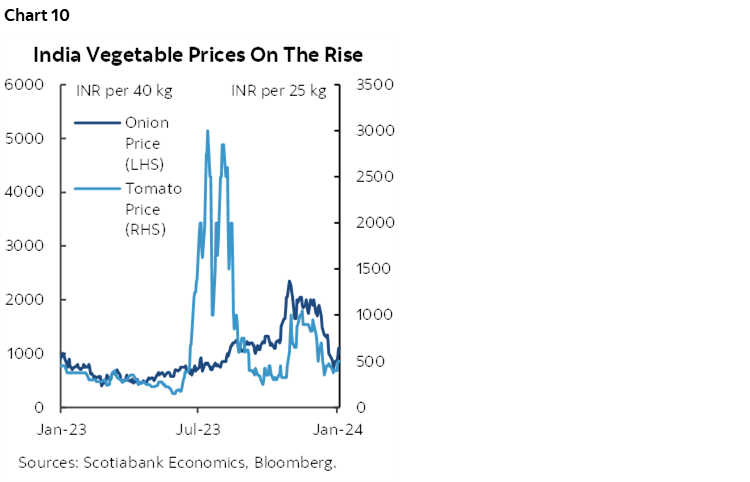

- India (Friday): Inflation should peak in December’s reading at least through the impact of higher food prices. Key staples in the Indian diet—like onions and tomatoes—experienced soaring prices due to unusually wet weather but this has already corrected itself (chart 10). Food prices were up by 8% y/y in November and there could be further upside in December’s reading with vegetables (18% y/y) a key driving force.

US BANK EARNINGS—A SOFTER EXPECTED TONE

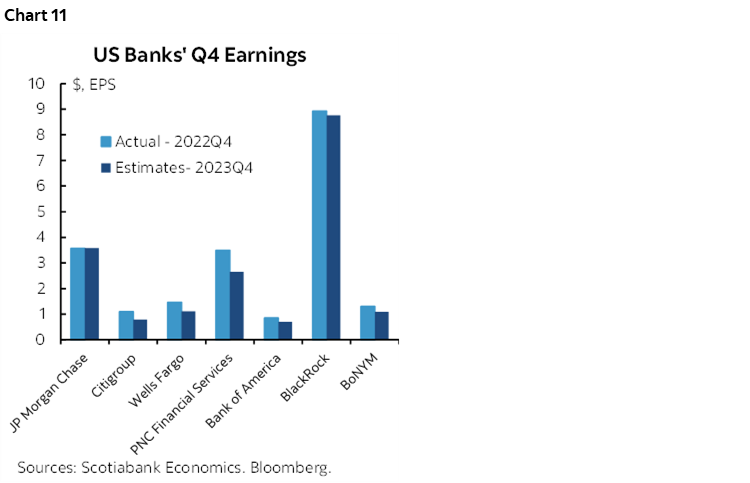

The year-end and Q4 US bank earnings season kicks off on Friday before the onslaught that arrives alongside rising breadth to the reporting season in subsequent weeks.

Among the initial names will be JP Morgan Chase, Citigroup, Bank of America, Wells Fargo, BoNYM and BlackRock. Chart 11 shows expectations for the season with the analyst consensus generally expecting a softer tone for earnings in Q4 than the prior year’s Q4 given it is seasonally unadjusted data.

CENTRAL BANKS—A CUT, A HOLD, AND THE WAITING GAME

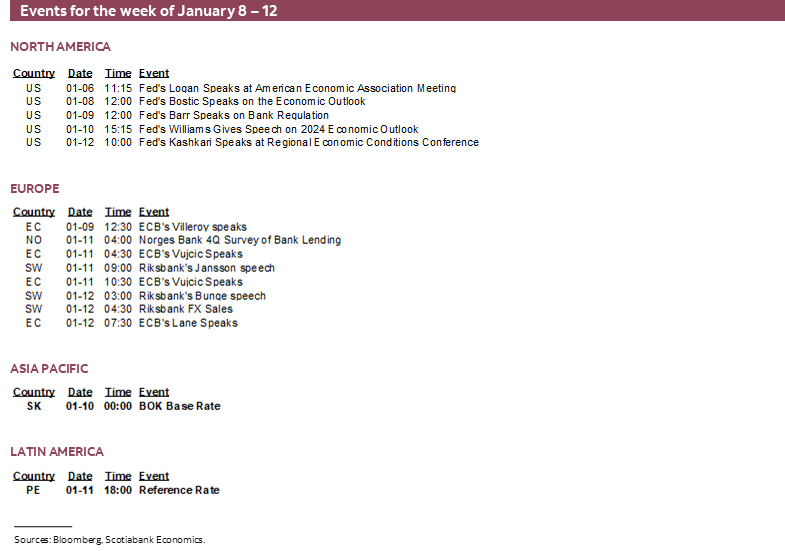

A pair of regional central banks will weigh in with decisions on Thursday. For the most part, global markets are in limbo awaiting the arrival of decisions by the world’s biggest central banks starting with the Bank of Japan but not until January 23rd.

Central Reserve Bank of Peru—Only Just Beginning

BCRP is expected to cut by another 25bps on Thursday. It began easing in September and has delivered a cumulative 100bps of cuts to date. That’s only a partial reversal of the 750bps of hikes that were delivered starting in August 2021 through to early 2023.

The magnitude of BCRP’s tightening campaign and the unique challenges that have affected Peru are among the reasons why we shouldn’t view cuts by LatAm central banks as necessarily indicative of what major global central banks may have in store for markets this year.

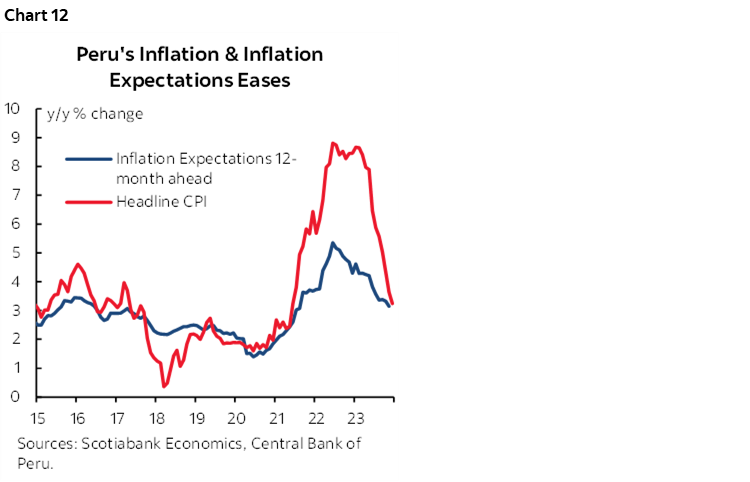

With this in mind, what BCRP has an eye on is the speed by which inflation expectations are coming down. One-year ahead inflation expectations surveyed by the central bank act as a modest leading indicator of inflation and give the central bank some comfort to continue its easing campaign (chart 12).

Bank of Korea—More Reason to Hold

Thursday’s BoK decision is expected to keep the 3.5% base rate on hold. It decided to remain on hold at its last meeting on November 29th and since then a pair of inflation readings have both been weaker than expected. November CPI fell -0.5% m/m, or about double the decline expected by consensus, with core inflation ebbing to 3% y/y. December CPI was flat (0.2% consensus) and core CPI fell again to 2.8% y/y. In its prior statement, the BoK struck out reference to possible further tightening but guided that it would remain restrictive “for a sufficiently long period of time until the Board is confident that inflation will converge on the target level.”

GLOBAL MACRO—GERMANY AND THE UK IN FOCUS

Apart from inflation readings, the rest of the global macro line-up will be pretty light next week with coverage provided in daily notes.

The UK will update readings for November on Friday that will cover monthly GDP, industrial output, services activity, construction activity and international trade. A mildly constructive tone is expected across the suite of data.

Germany will update November readings for factory orders, exports and imports (Monday), and industrial production (Tuesday). Norway (Monday), France (Wednesday) and Italy (Thursday) will also update industrial output readings. The state of the European consumer will be revealed by Eurozone retail sales during November (Monday), Italian retail sales (Wednesday) and then total French consumer spending (Friday).

Outside of inflation, Asia-Pacific releases will be focused upon Chinese exports in December (Friday) and Aussie retail sales during November (Monday). China might also update aggregate financing figures either this week or early the following week.

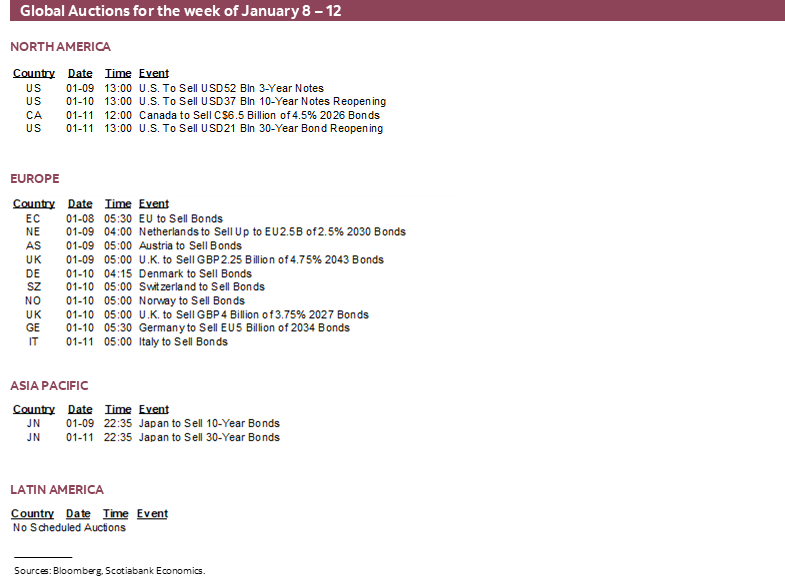

Canada updates trade figures for November on Tuesday.

The main US focus will be CPI, as the rest of the week only contains a probable small widening of the US trade deficit (Tuesday), probably still low initial jobless claims (Thursday) and light Fed-speak.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.