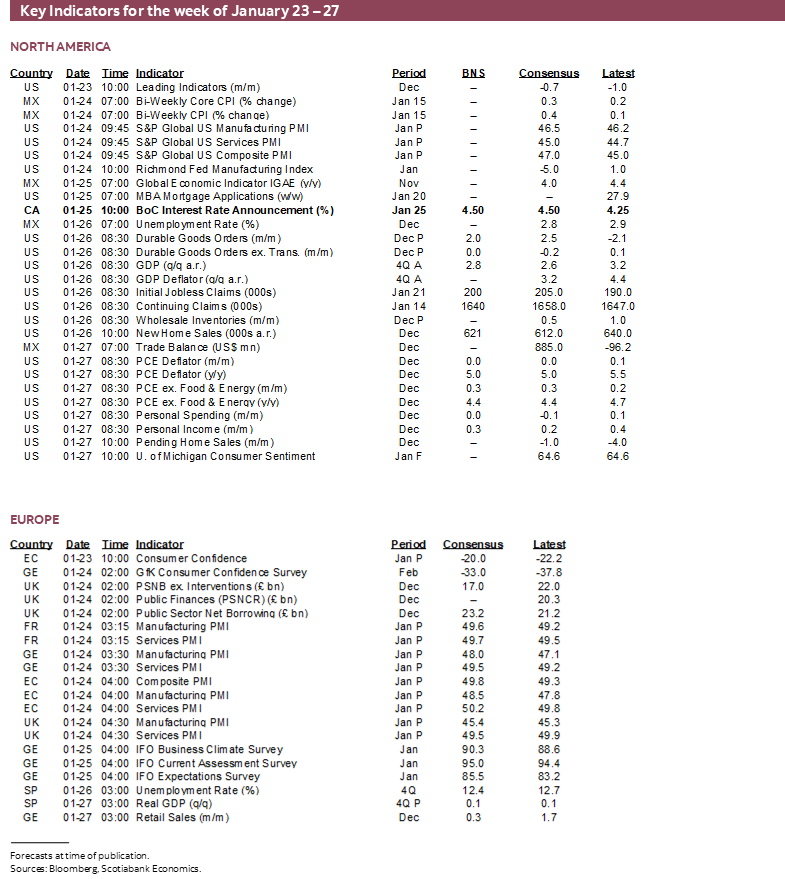

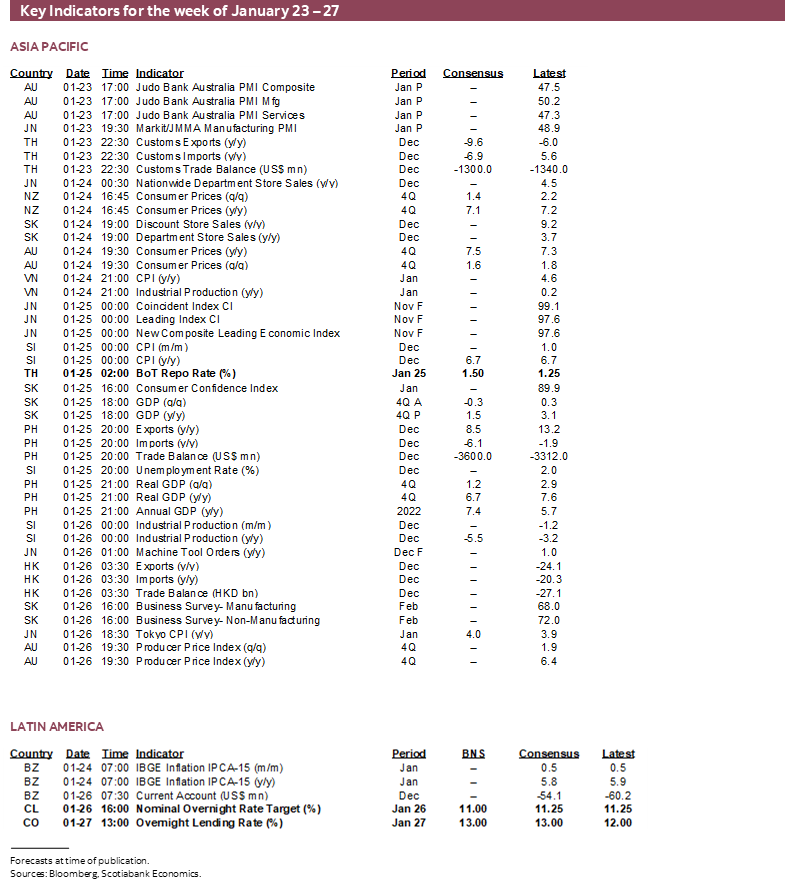

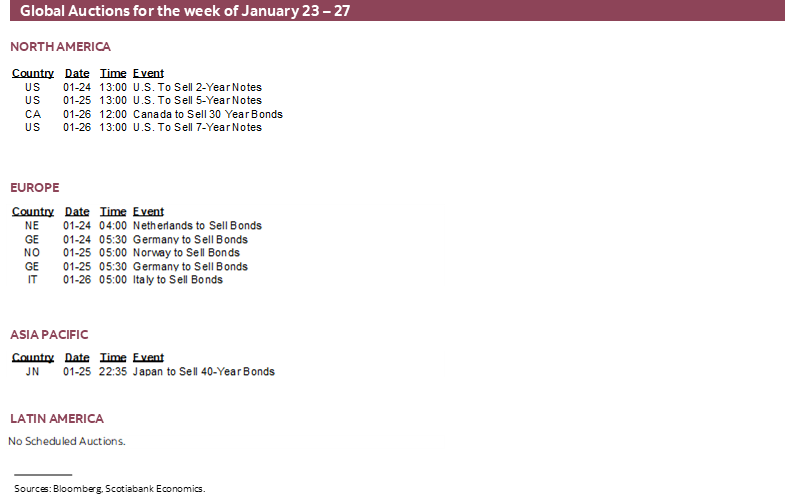

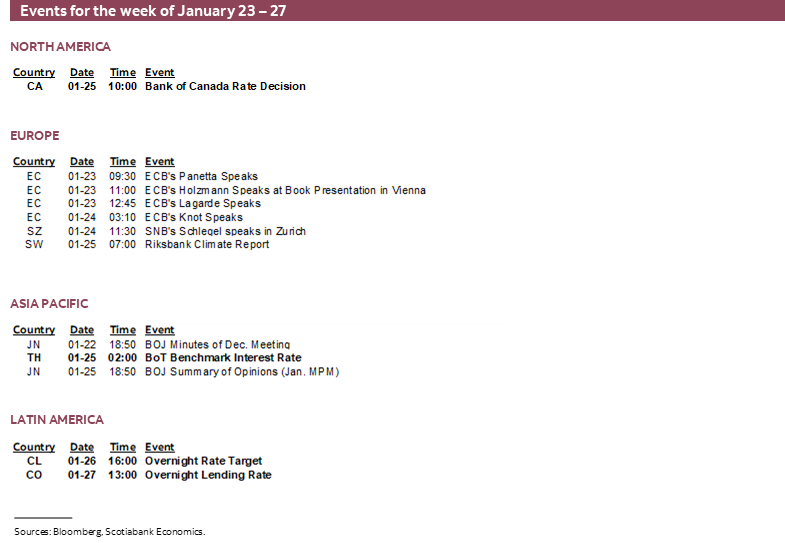

Next Week's Risk Dashboard

- How markets and the economy behave around US debt disputes

- Consensus has been too bearish on US growth

- The US consumer is more resilient this time

- BoC: Risk versus reward around hike expectations

- BanRep expected to deliver another mega-hike

- BCCh like to extend policy hold

- BoT to hike as tourism recovers

- SARB to cool the pace of hikes?

- US PCE to follow CPI

- Aussie inflation expected to accelerate

- NZ picks a new leader while hoping inflation eases

- Global PMIs to inform Q1 GDP growth tracking

- earnings season intensifies

- Other global releases focused on the US

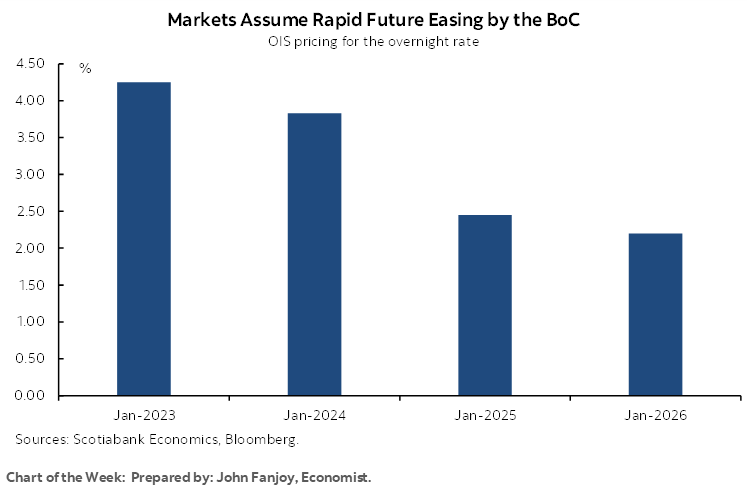

Chart of the Week

While consensus has been too bearish toward the prospects facing the US economy and faces another reminder of such this week, Congress has decided to play games again and with uncertain ramifications for global financial markets. The US Treasury will further its use of emergency measures designed to manage the freeze on debt issuance as the debt ceiling has become binding and with that will go gradually rising speculation toward the consequences. The central banks that have to weigh in with decisions this week will need to keep potential market frailties in mind while global data releases offer a fairly heavy calendars for the fundamentals.

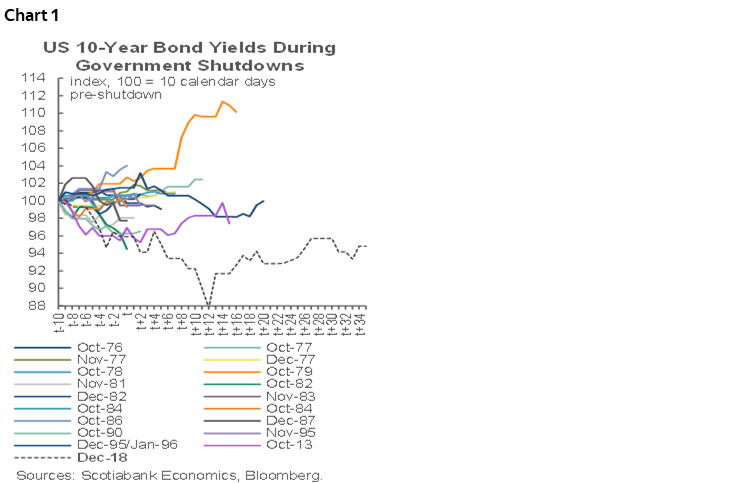

History offers some indication of how markets may respond should developments become more extreme. Key in evaluating the implications is to consider how stocks, bonds and currencies performed when debt ceiling frictions have become acute enough to drive government shutdowns, of which there have been plenty over time. Most shutdowns have been very short and lasted anywhere from just a few hours (1984, 1986) to 1–5 days. More acrimonious disputes resulted in three lengthier shutdowns including the granddaddy of them all under the Trump administration when the government was forced to shut for over a month over border wall funding in late 2018 into early 2019.

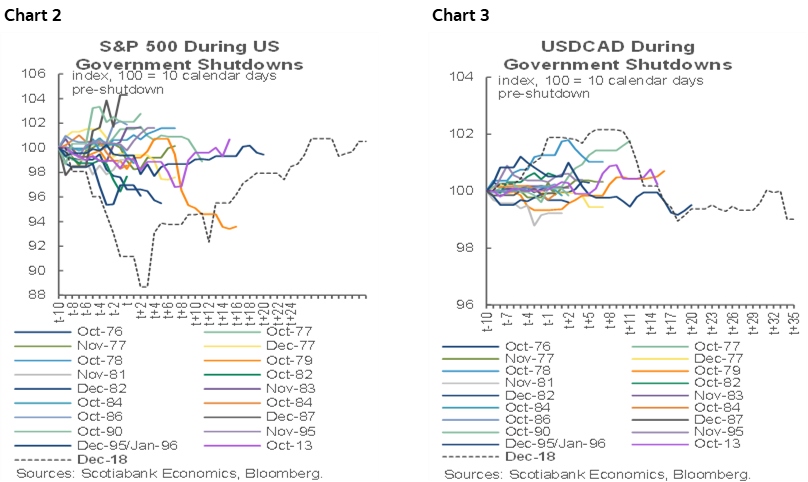

When evaluating charts 1–3, it’s therefore important to focus less on the short-lived squiggles and more on the outlier experiences aligned with the bigger shutdowns in 2018–19, 2013 and 1995–96. Chart 1 plots performance of 10-year US government bonds indexed to equal 100 starting 10 days before each government shutdown at time t=0 when concern intensifies and for varying durations of time thereafter according to each episode’s length of shutdown. A declining trend is a rally in Treasuries (falling yields) and the biggest and longest shutdowns have driven the largest market effects.

Chart 2 does the same thing for the S&P500 and shows that the shutdown in 2018–19 carried a material effect on risk appetite. Chart 3 shows that effects spilled across the border through the USDCAD exchange rate as the Canadian dollar depreciated while the world rewarded US political dysfunction through buying more USD and Treasuries due to, well, no choice given the size and pervasiveness of US government securities in world markets. Owe me a dollar it’s your problem, owe me a few trillion and it’s mine.

Through this period of market volatility that we may well be entering it’s important to emphasize a few base case expectations. One is that defaulting on US Treasuries is likely an extremely remote prospect in the minds of those of us who have seen this movie in various incarnations and with alternating actors many times in the past. McCarthy in ‘Home Alone’ version whatever it is now? Defaulting would be a Lehman event in the markets and the GOP would most assuredly be blamed into the 2024 Presidential election. The US administration spends too much and has rapidly driven debt higher, but Americans are unwilling to cut core government spending programs.

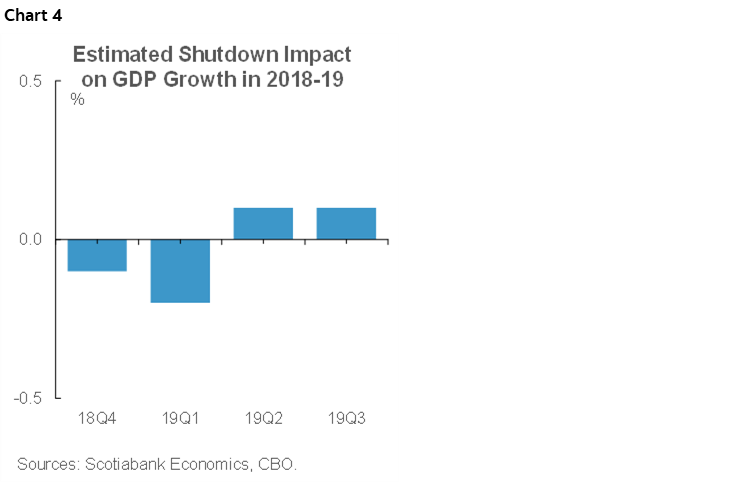

Second is that any impact on the US economy is typically modest and transitory in the absence of a default; witness the few tenths knocked off GDP growth from the 2018–19 shutdown and added back later (chart 4).

Third is that there is opportunity to both investors and parts of the economy amid the potential political turmoil that lies ahead. Maybe the timing could be fortuitous into, say, Canada’s highly seasonal Spring housing market if fixed term borrowing costs decline due to lagging effects of GoC bond yield movements to date and anything further that may be tacked on in the weeks and months ahead. Monitoring swap markets and mortgage pre-approval pipelines may be offshoots of this argument going forward.

US ECONOMY—TOO BEARISH?

The US economy has been defying forecasters’ expectations for an abrupt slowdown for some time now. Key has been the performance of the US consumer despite market reactions to recently softer retail sales.

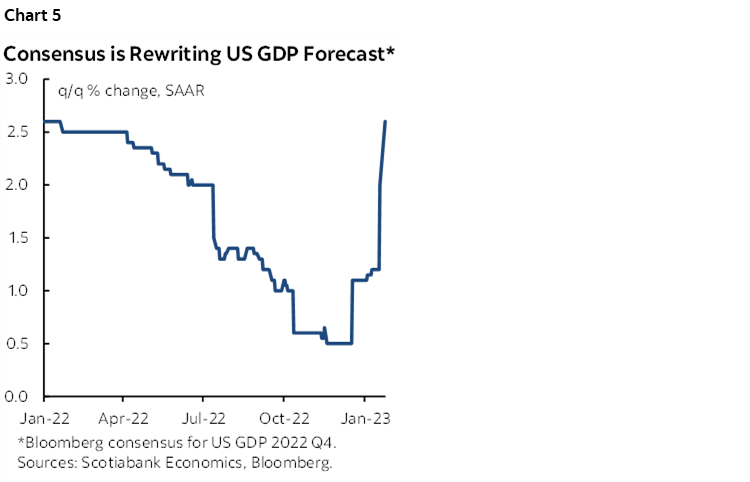

Chart 5 shows the evolution of consensus forecasts for Q4 GDP that arrives on Thursday. Not so long ago—in fact right up to just days before the holiday season—the median consensus forecast across dozens of forecasters was for paltry growth of 0.5% q/q at a seasonally adjusted and annualized pace. That consensus now sits at 2.6% as new information has arrived. I’ve estimated growth to land at 2.8%. At the time of publishing, roughly one-quarter of consensus had 3-handled estimates. If such estimates are even remotely in the correct ballpark, then in just a few short weeks forecasters have seriously upgraded their estimates. This is part of the set of material new information to forecasters across the global economy in recent weeks.

If such upside to earlier estimates is delivered, then this would be the second consecutive quarter in which forecasters have gotten it wrong by being too negative toward the US economy. By the end of Q3, consensus was estimating Q3 US growth to have been about 1.4% q/q SAAR and then steadily revised this estimate higher as actual figures arrived and presently point to growth that is more than doubling such expectations (3.2%).

Key has been the US consumer. I figure that consumer spending will contribute about 2½ percentage points to Q4 GDP growth in weighted contribution terms given what we know thus far about how total consumer spending evolved and the 71% weight on the consumer in US GDP.

You wouldn’t know it from the reaction by markets to soft December retail sales yet there are two caveats to those results. US retail sales exclude many services beyond restaurants and bars (Canada excludes even that) which means that things like travel by all modes of transportation and lodging are not captured. Another reason for this is that consumers may have pulled forward their holiday retail spending to earlier in the season due to ongoing supply chain warnings and the fact that Black Friday and Cyber Monday discounting no longer has as much to do with Black Friday and Cyber Monday given discounting that arrived weeks to months earlier.

At present, consensus is forecasting 2023Q1 GDP growth to be non-existent. Trust us, they said. This time we got it, they said. Yeah yeah, wanna watch? Got one of those for ya too. Yeah yeah. If the serial pattern to date persists, then perhaps that constantly pushed-out narrative that keeps waiting for the other shoe to drop may not drop as much as feared.

Why? There remains an ongoing quest to get on with making up for lost time in terms of activities that were shelved earlier in the pandemic which speaks to many services, while recently softer goods consumption will eventually shake off its earlier excesses and the ensuing correction. These developments are backed by robust household finances. Huh? Come again? We’re talking profligate US consumers here? Yep, them.

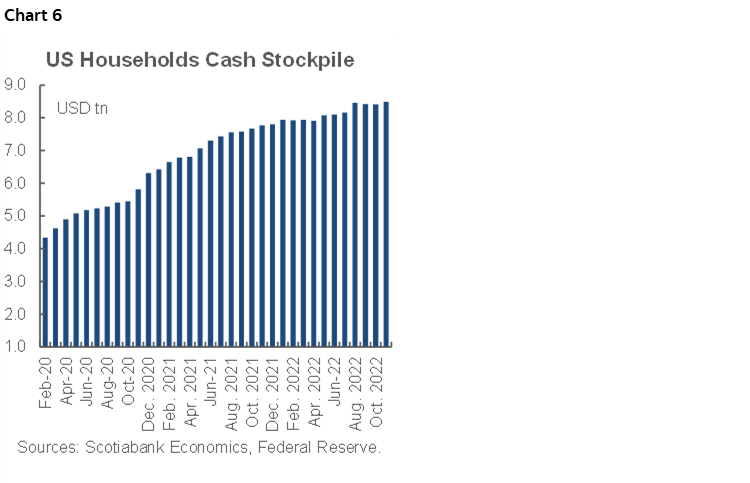

The US consumer’s finances are better prepared for this recession-in-waiting possibility than at any other point in decades. Witness the ever-growing mountain of cash, deposits and retail money market balances (chart 6). Governments kept throwing money at households who said thanks very much, but we can’t spend it as fast as you are giving it to us.

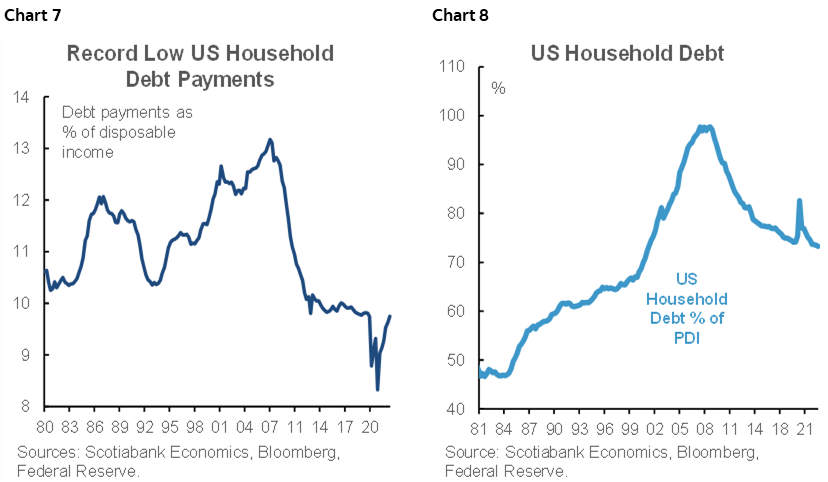

Or how about still very low debt payments as a share of household income (chart 7). A driver of this is that the US consumers’ debt load has been wound back to levels that we have not seen in twenty-two years (chart 8). Twenty-two years folks! A combination of working off the excesses leading into the GFC and regulatory changes have driven improved health of household balance sheets not to fully skirt the tightening of monetary policy, but to adapt to it perhaps in healthier ways than expected. And let’s not forget that existing mortgage debt has overwhelmingly been financed at the 30-year mortgage rate in a very different mortgage market than many other parts of the world where households have a one-way option to refi only when rates are falling and only at a glacial speed when rates are rising which the 30-year mortgage rate stopped doing over two months ago as it fell back by nearly a percentage point from the peak.

All of which is to say that the US household sector is arguably less vulnerable to the 425bps of rate hikes to date than the 425bps of rate hikes leading into the GFC without even getting into other arguments on the shady practices that collapsed at the time in such fashion as to reverse leverage much more aggressively than anything that is likely today.

The flipside to these arguments is that the Fed’s job at sustainably controlling inflation may be harder than markets think as they price a terminal rate that foresees another 50bps of rate hikes when multiple Fed-speakers are guiding just over that threshold and while markets price 150bps of rate cuts starting later this year and into the end of 2024. Markets often think they know better than anyone else, but they’re not listening to the Fed either in terms of terminal rate guidance or cautions against prematurely easing. Since the Fed can control shorter-dated instruments better than rate pricing further up the curve, it may be that the FOMC needs to jolt markets with a bigger rate hike now in order to bring them onside.

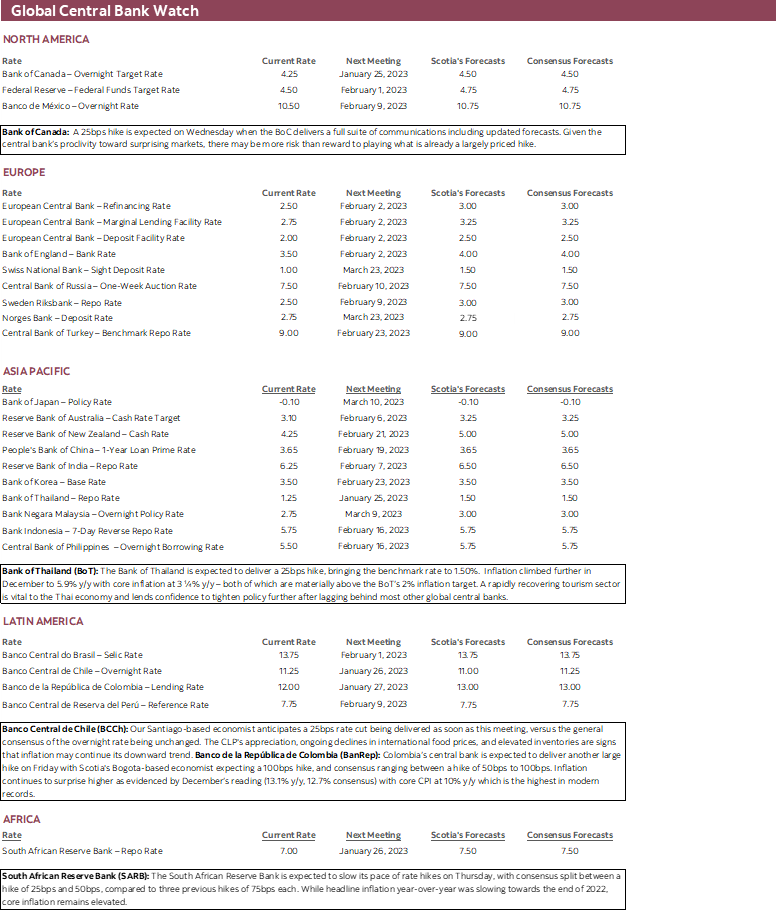

BANK OF CANADA—RISK VERSUS REWARD

The Bank of Canada weighs in with a full suite of communications this Wednesday including an updated policy statement and Monetary Policy Report with fresh forecasts (10amET) followed by the 11amET press conference hosted by Governor Macklem and SDG Rogers. This will also be the first time that the BoC releases meeting minutes two weeks later on February 8th and a day after Macklem speaks in Quebec City. The timing puts the minutes between the BoE’s release on the same day and the Fed’s release three weeks after meetings.

Markets are almost fully priced for a 25bps rate hike. All of the big domestic banks’ economics shops expect a 25bps hike including the Scotia Economics house view.

It is with modest conviction that we expect a 25bps hike. I don’t really have much more to say about expectations than what I’ve recently written on the topic in a number of notes as rolled into this one. I would assign 55% odds to a 25bps hike, 35–40% odds to a pause and we can’t fully shut the door to a hawkish surprise as a low probability but high impact tail risk. Part of the reason for that is that the BoC surprises in both directions when it (often) chooses to surprise. Deputy Governor Kozicki said on December 8th that “We are still prepared to be forceful” which is code language for a larger than normal rate hike “If there were to be a very large shock.” What has happened since probably doesn’t qualify, but it was after she spoke that over 100k jobs were created in a single month and forecasts for US GDP growth began to be revised sharply higher with implications for spillover effects into Canada’s economy.

The fundamentals support continued hiking including upside tracking to the BoC’s Q4 GDP forecast, ripping job growth in very tight labour markets, lessened downside risk to the world economy given recent developments and easier financial conditions especially via bond markets. The biggest argument for a hike, however, may be the reverse logic point; don’t hike, and markets will have their ‘gotcha’ moment in that Macklem will be perceived to be getting weak kneed. This could drive a further pile on into the shorter-term rates complex that pushes rate cut pricing to be even more generous than at present (see cover chart).

Still, my bias is that the risk-reward calculus points to more risk of a hold than a hike relative to what is already priced. The added key will be the general policy bias if they deliver one.

I doubt the BoC will pre-commit to further hikes and would prefer that they keep the door open to doing more if necessary. The combination of a hold and clear signal that they are done hiking would probably further amplify an easing of financial conditions compared to the roughly 200bps of easing that is already priced into markets starting later this year and mostly next year. This would seem to be the most counter-intuitive to efforts to durably contain inflationary pressures and dampen interest sensitives like housing. A hold and open bias might lessen this reaction, but markets have a tough time believing anything central bankers are saying about the future as it stands now and so here too markets might heap on cut bets.

FOUR MORE CENTRAL BANKS

Four other central banks will deliver policy decisions this week including two that land squarely within the core footprint markets of my employer and many of its clients.

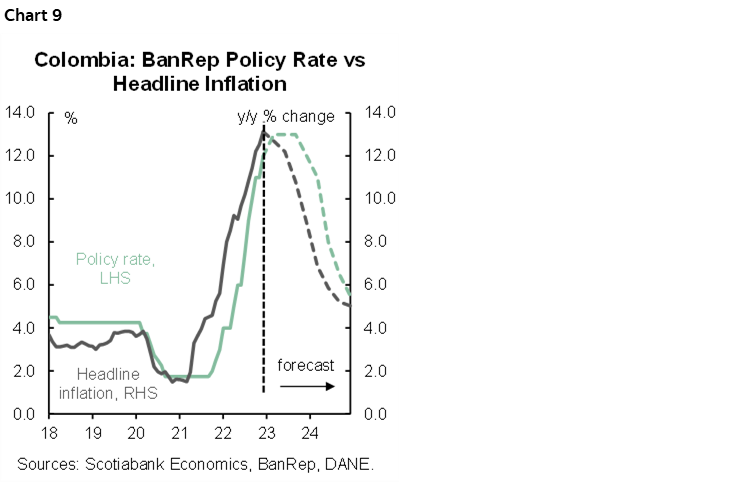

- BanRep: Another mega-hike is expected to be delivered when Colombia’s central bank weighs in on Friday. Consensus is somewhat divided on the call with eleven voices expecting +100 including Scotia’s Bogota-based economist, five forecasters expecting 75bps and a couple expecting a 50bps hike. Inflation continues to surprise higher as evidenced by December’s reading (13.1% y/y, 12.7% consensus) with core CPI at 10% y/y which is the highest in modern records. Rapid easing is expected later (chart 9).

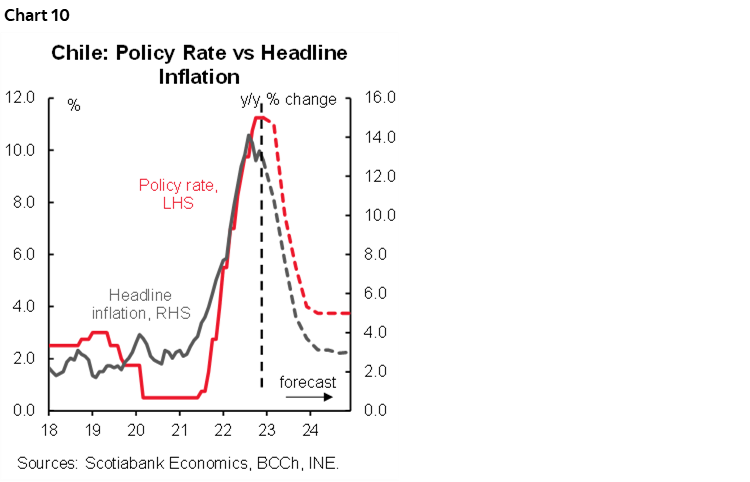

- BCCh: Consensus almost universally expects another policy rate hold at 11.25% on Thursday which maintains the overnight rate at the same unchanged level since October. Our Santiago-based economist boldly thinks there is a chance at a rate cut being delivered as soon as this meeting. Inflation has started to ease in y/y terms to 12.8% y/y from a peak of 14.1%. Easing is expected later (chart 10).

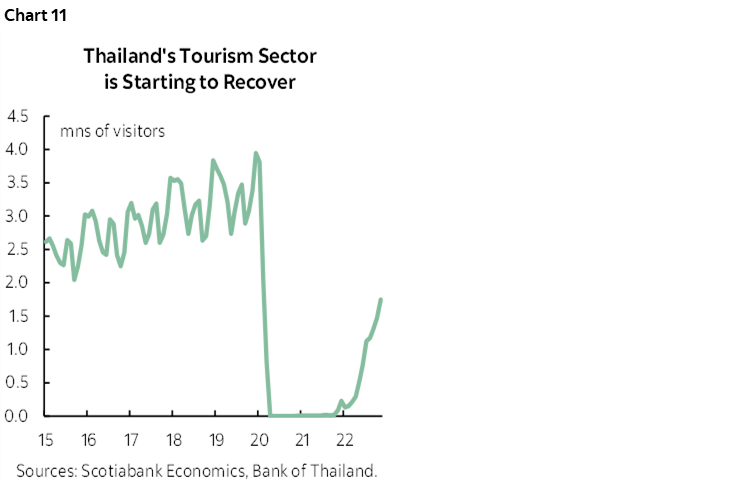

- Bank of Thailand: Wednesday’s decision is expected to deliver a 25bps hike to a new benchmark rate of 1.5%. Inflation climbed further in December to 5.9% y/y with core inflation at 3 ¼% y/y—both of which are materially above the BoT’s 2% inflation target. A rapidly recovering tourism sector (chart 11) is vital to the Thai economy and lends confidence to tighten policy further after lagging behind most other global central banks.

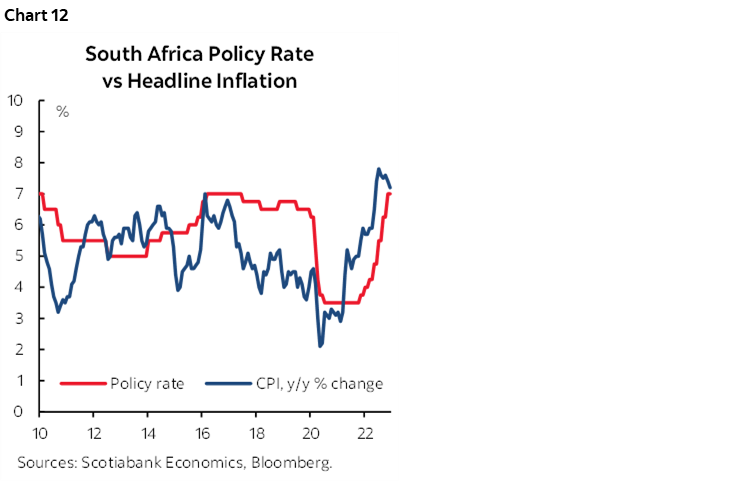

- SARB: The South African Reserve Bank is expected to hike again on Thursday, but consensus is split between +25bps and +50bps with markets leaning closer to the former. The uncertainty is based upon whether the central bank will wish to cool the pace of rate hikes at this meeting given some evidence that inflation is cresting (chart 12).

GLOBAL MACRO

Several global inflation readings, a round of global purchasing managers’ indices and a batch of other US economy readings will combine with a more intense week for US earnings reports to make for a lively week.

US earnings season kicks into higher gear this week with 89 S&P500 firms poised to report across a broadening number of sectors.

Several global inflation readings arrive this week as follows:

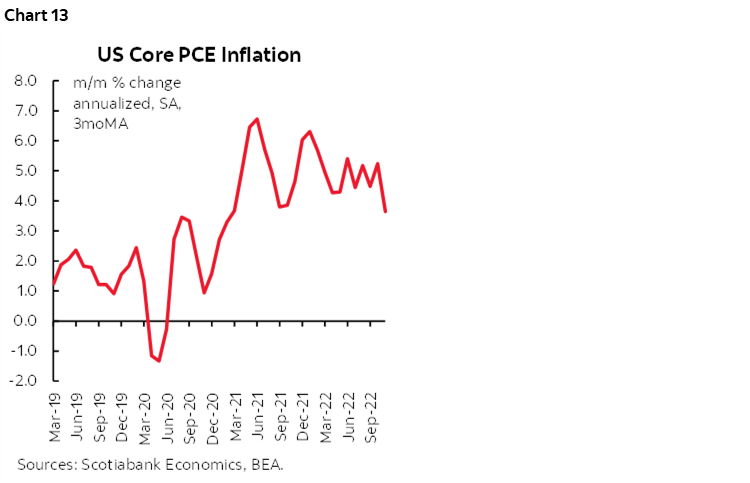

- US PCE: Don’t call it cool just yet (chart 13), but the Fed’s preferred inflation gauge will probably follow CPI with my estimate for headline PCE to be flat (0% m/m SA) while core PCE ex-food and energy rises by 0.3% m/m. The large 0.8% m/m rise in owners’ equivalent rent in CPI gets a much higher weighting than in PCE and so there is perhaps more downside than upside risk to my estimates. That dynamic will reverse later in the year as CPI gets dragged down faster by housing than PCE.

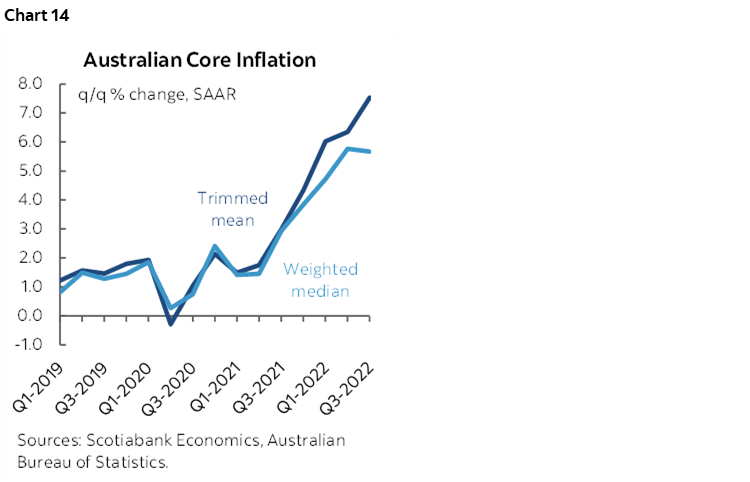

- Australian inflation: The addition of monthly CPI inflation readings since October has sharply improved the freshness of readings that were previously largely reliant upon lagging quarterly estimates. Australia updates both for Q4 and December on Tuesday evening (eastern time as always). Markets trimmed RBA bets a bit after a small part-time driven drop in employment during December and may be more vulnerable to upside surprise to inflation relative to what is priced. Headline CPI is expected to accelerate toward 7 ½% y/y in Q4 and 7.7% y/y in December with trimmed mean CPI expected to approach almost 6% y/y. Quarter-over-quarter momentum will be key given the pattern to date (chart 14).

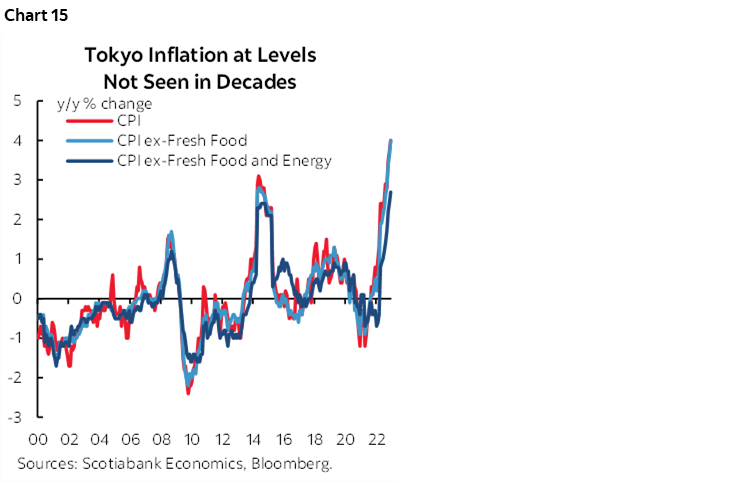

- Tokyo: CPI for the city during January (Thursday) is the freshest monthly gauge ahead of national figures. Core Tokyo CPI ex-fresh food and energy is expected to rise again and inch toward 3% (chart 15). Such a reading—especially if surprised higher—could further fan expectations for a BoJ pivot. I think those expectations are overdone in some corners of the markets, but new information is focused upon Spring wage negotiations with the unions and the transition of power from Governor Kuroda to his successor in April.

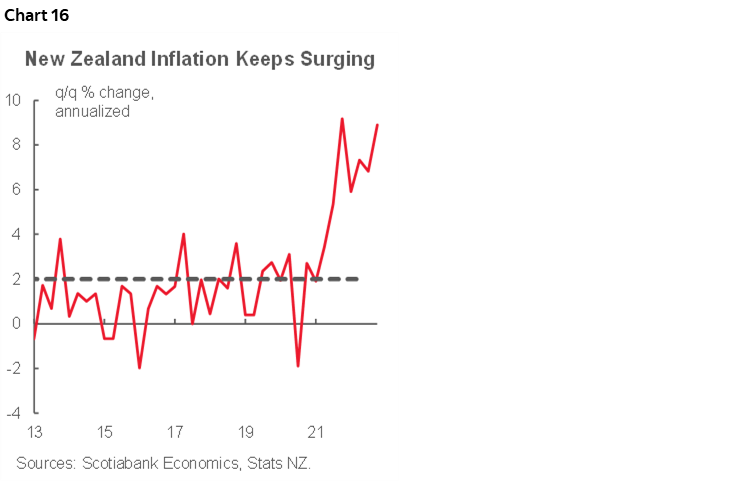

- New Zealand CPI: Not only will the Labor Party pick a new leader this week in the wake of the surprise resignation of PM Jacinda Ardern, local markets will also have to weigh the implications of fresh CPI figures for Q4 on Tuesday (eastern time). A somewhat cooler but not cool pace of inflation is expected compared to the recently explosive pattern (chart 16).

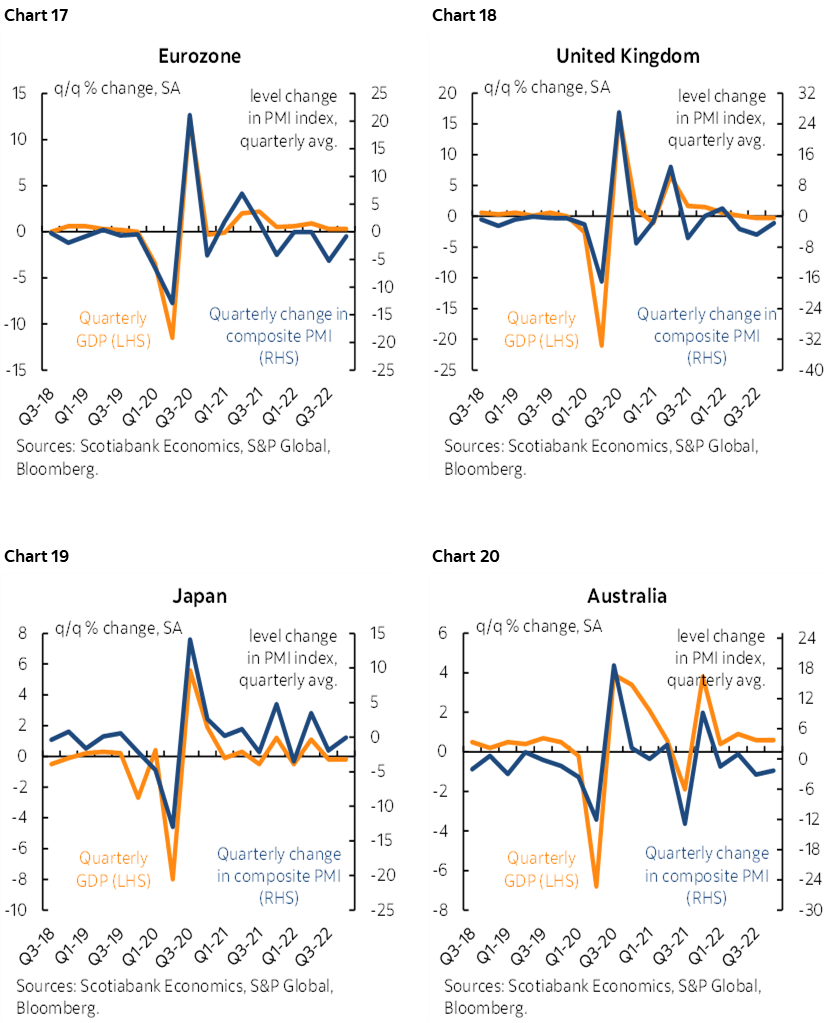

Another batch of global purchasing managers’ indices will be delivered early in the week. If the first of the European survey-based “soft” data readings is any indication, then an improved outlook among German investors in the ZEW survey could portend improved PMIs and German IFO confidence this week as perceived downside risk to the global economy has lessened into this year. The PMIs will further inform tracking of Q1 GDP growth across numerous major regions of the world economy given correlations between the measures as shown in charts 17–20. The measures will offer estimates for January across everything from new orders to order backlogs, inventories, hiring appetite, prices paid and prices received. Australia and Japan kick it off on Monday. The Eurozone and UK follow the next day. The US S&P gauges arrive later Tuesday morning and reflect global operations of US companies, versus the ISM PMIs that the Fed watches more closely as they are more closely aligned to the domestic operations of US companies.

US GDP will dominate, but we’ll also get Q4 GDP growth estimates from South Korea and the Philippines on Wednesday and then Spain on Friday ahead of the following week’s Eurozone-wide estimates.

Since US Q4 GDP including total quarterly consumer spending arrives on Thursday, there will be little fanfare left over for estimates of consumer spending in the month of December when that gets updated on Friday. The greater focus will be upon the accompanying income estimates and I’ve figured that compensation will drive a 0.3% m/m SA gain in incomes. Other US indicators will include the following:

Durable goods orders during December (Thursday) probably grew significantly given a surge of orders for planes from US airline, but core orders ex-defence and aircraft will be watched more carefully as an indication of cap-ex activity that has posted significant gains this year.

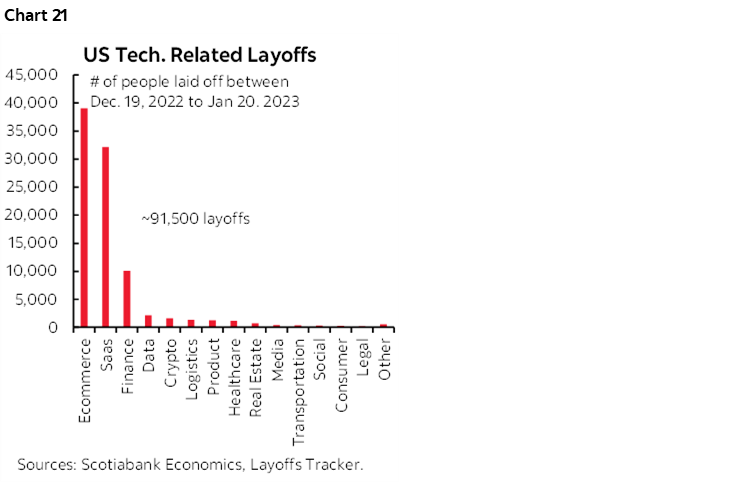

Initial jobless claims are not exactly cooperating with all of the layoff announcements. Chart 21 shows that a proxy for the nonfarm reference period in January over December saw over 90k tech sector layoff announcements, yet initial jobless claims have fall below 200k and have been on a downward trend since November when layoffs began to mount. Why this divergence? One caution is that layoff announcements can involve lags before the final date of unemployment and then making the trek to filing offices. Another caution is that some large states, like California, have been estimating their claims numbers instead of providing hard numbers and one possible reason is due to disruptive effects of flooding that followed heavy rains in parts of the state. Another possibility is that seasonal adjustments have been questionable at various points in the pandemic and may still be. Or, maybe, just maybe, the layoffs are being absorbed into what are still over ten million job vacancies in the US economy.

Housing data will include new home sales during December (Thursday) and pending home sales for the same month (Friday) that serve as a leading indicator of completed resale transactions.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.