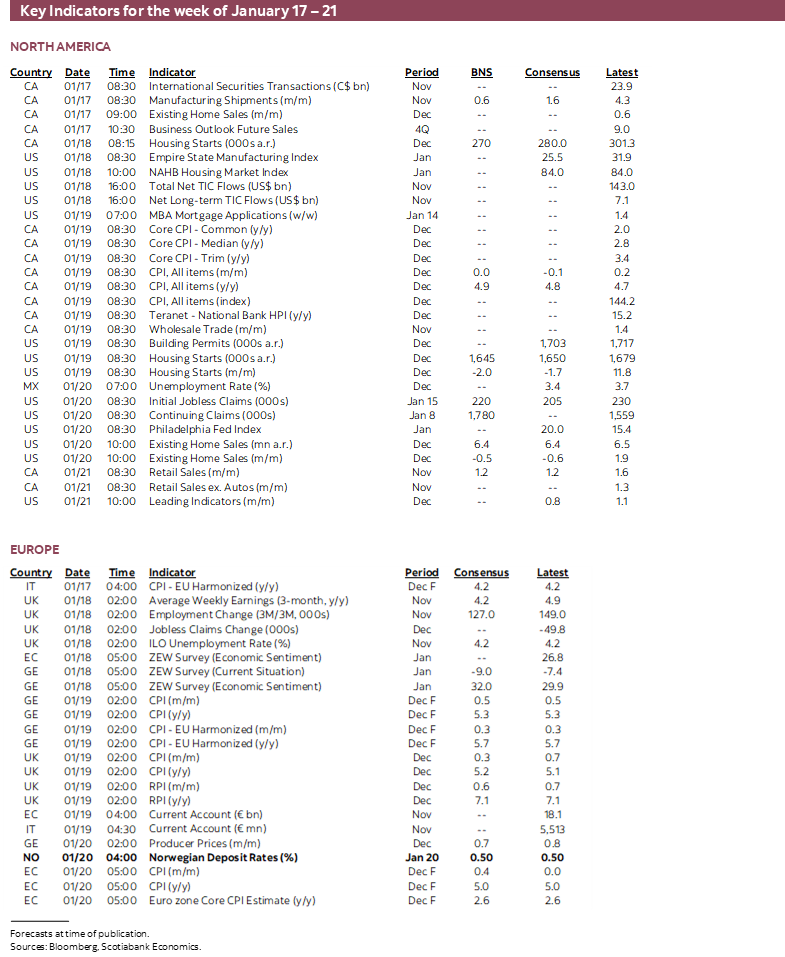

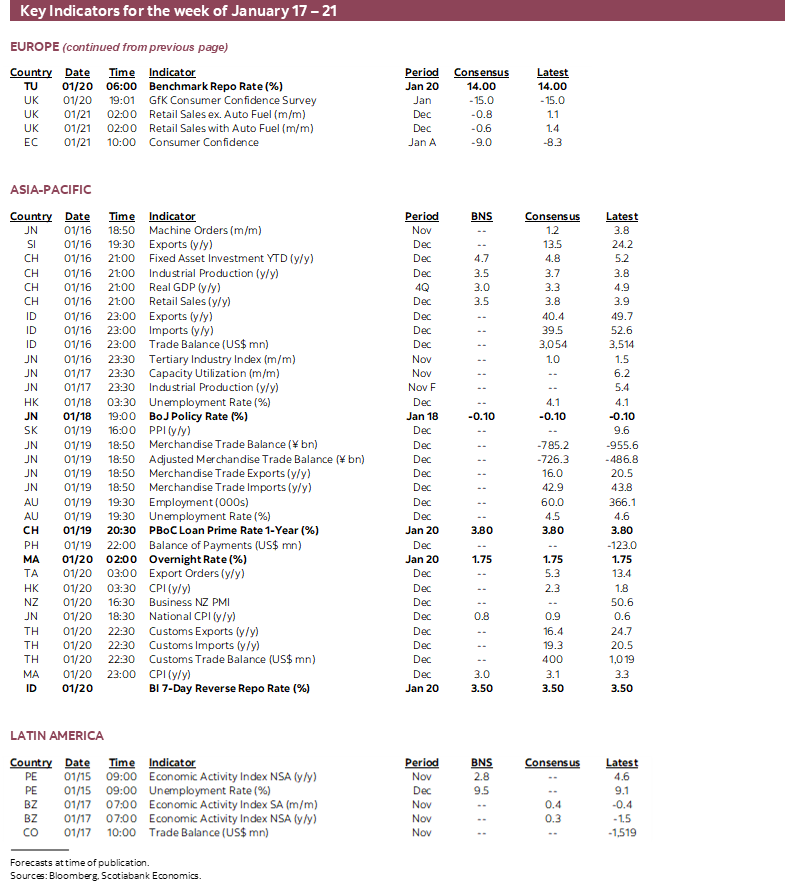

Next Week's Risk Dashboard

• Fed balance sheet roll-off scenarios & term premia

• Canadian inflation: stale and fishy

• BoC’s surveys: Are expectations becoming unmoored?

• Did you hear the one about the BoJ hiking?

• PBOC cuts, further easing likely

• China’s flagging economy

• Other CBs: Norges, Negara, BI

• BoE watching inflation, jobs

• Aussie jobs

• US earnings season

Chart of the Week

FEDERAL RESERVE RUN-OFF SCENARIOS

Market uncertainty around central bank actions over 2022 will continue to be a focal point especially as it applies to the Federal Reserve’s actions and their spillover effects. Raising the policy rate is going to be the first and most significant tool used by the Federal Reserve to lessen the massive amount of stimulus still coursing through the economy’s veins. Still, the Federal Reserve is counting upon its ability to avoid inverting the US Treasury curve—indeed steepen it—if it is intent upon raising the policy rate toward a neutral or restrictive stance by adjusting balance sheet policies as needed in order to raise longer-term bond yields by enough to counteract other possible forces in the bond market. Several FOMC speakers have intimated that they can achieve such an outcome by adjusting policies around reinvestment of maturing securities within the System Open Market Account. The loose logic is that by reducing its net holdings of securities, the Fed will lessen its role in the broad fixed income market and leave the market to take down issuance on its own absent Fed participation such that the term premium on longer-dated securities may increase.

Maybe, but I’m skeptical that will be enough to do it. The relatively slow speed at which reinvestment policy shifts alone can motivate a reduction in the size of the SOMA portfolio, coupled with the evidence on movements in term premia, probably require the Fed to consider asset sales if it wants to shrink its balance sheet by enough to overcome other forces in bond markets.

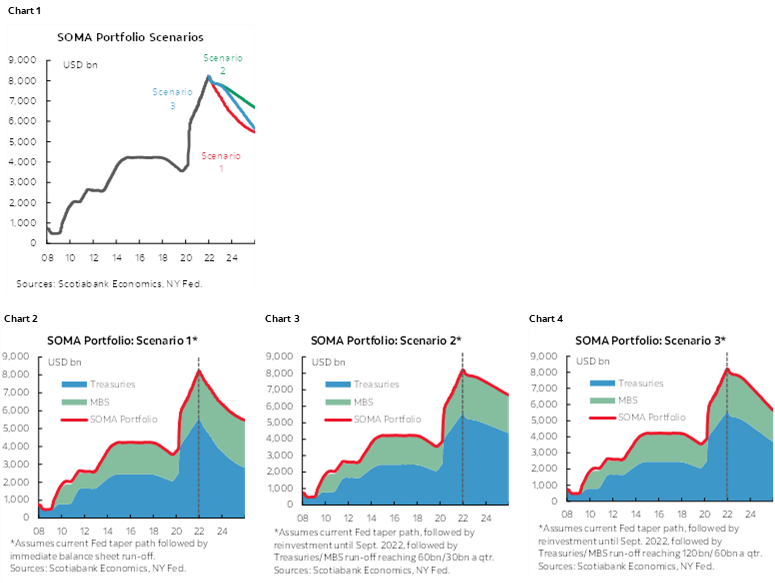

Charts 1–4 offer reinvestment scenarios to help explain why and with research help from Marc Ercolao. The SOMA portfolio is presently sized at about US$8¼ trillion versus about US$3.8 trillion just before the pandemic struck. Chart 1 shows the outcome of three different reinvestment scenarios applied to forecasting the size of the SOMA portfolio, while the other charts break down the changes in Treasury and MBS holdings.

Scenario 1 is probably unrealistic but provides a starting point by applying the Fed’s current guidance toward reducing net purchases and then ending them by mid-March and then assumes that no reinvestment follows. We use the published schedule of security maturities to time the roll-off of the various debt securities. This approach would reduce the size of the SOMA portfolio by about US$1 trillion by year-end, and ultimately still leave the SOMA portfolio ending 2025 at about US$5½ trillion—still nearly 50% larger than before the pandemic four years from now.

Scenario 2 is a little more realistic in that it assumes the same guidance on net purchases until mid-March, fully reinvests all maturing securities until about September 2022 in keeping with Powell’s guidance that such a step may occur “later in the year” and then reduces reinvestment by allowing the pace of roll-off of maturing securities to proceed at a similar pace to what the Fed did over 2018–19. Under this scenario, the SOMA portfolio ends 2022 at about US$7.8 trillion for a reduction of only about $½ trillion, and then ends 2025 at about $6.7 trillion which would remain 75% larger than before the pandemic.

Scenario 3 does the same things as in Scenario 2 but doubles the quarterly pace of roll-off after this September. This scenario would pay heed to guidance from Chair Powell that roll-off could be not only sooner but also faster than the last time in 2018–19. By the end of this year, the SOMA would be just under US$7.8 trillion and by the end of 2025 it would be US$5.6 trillion and hence still just under US$2 trillion larger than before the pandemic.

We don’t know what reinvestment path the Fed will choose and there are many more possible scenarios than just these three. More information is expected in the FOMC discussion that we have been led to believe will occur at the meeting on January 25th–26th and in subsequent meetings. Scenario 1 is likely too fast, scenario 2 is probably too slow, and so scenario 3 may wind up being closest to the mark.

Enter the term premium connection. When the Fed bought such a massive number of bonds in the pandemic did it really swing the already very low term premium materially lower? Not really. Chart 5 shows that it was already diving into the -50bps to -100bps range according to NY Fed economists before the pandemic struck and bond buying may have pushed it a little lower. That effect has been reversing since last Fall. For all the trillions in bond buying, the impact at the margin was at best rather modest and transitory in relation to other forces guiding the term premia. That’s even truer in terms of the broader forces that caused outright Treasury yields to sharply decline even as the Fed’s SOMA portfolio was still shrinking in 2019 and as yields plummeted when shutdowns first began to hit in 2020Q1.

What makes the Fed so sure that in relation to these many other forces guiding bond yields its reinvestment assumptions under any scenario will be enough to materially swing the term premium higher after its long-term decline and in isolation of other forces operating on bond markets? For that matter, what makes equities so fearful that roll-off will destabilize bond markets with negative effects on equities?

I do think that term yields will rise for a variety of reasons over our forecast horizon and avoid curve inversion as the Fed begins to hike its policy rate if we’re anywhere in the right ballpark on our assumptions for markets, the economy and inflation. If we’re wrong to the downside of our assumptions and the Fed hikes too much, then it’s unclear that the Fed should even attempt to lean against the information in a potentially inverting yield curve. If we’re right on everything else but wrong on the forecast rise in bond yields as the Fed hikes and the Fed wishes to manipulate the bond market in order to maintain a positive upward sloping yield curve, then it may well have to entertain more aggressive options such as outright asset sales. Even that may not be assured of success in part depending upon implementation.

When asked about this during his recent confirmation hearing, Chair Powell ducked the issue and left it to be discussed over coming FOMC meetings. Few would blame him given there is no playbook for how to get out of an $8¼ trillion portfolio while hiking and all the while hoping that the pandemic may be on its eventual way out and without sparking a dumpster fire in the process. This issue could be the elephant in the room for the bond market over said coming meetings and (more likely) beyond. Unfortunately, the FOMC goes into blackout this coming week ahead of the following week’s meeting and so markets will be on tenterhooks waiting for some potentially cleared guidance on balance sheet plans.

ARE CANADIAN EXPECTATIONS BECOMING UNMOORED?

This will be a big week for Canada watchers and Canadians in general. Several pieces of new information will be considered as the Bank of Canada goes into communications blackout after Tuesday ahead of the policy communications and forecasts on January 26th. At the same time, the kids go back to school after a two week online interval in several parts of the country; this deck that reviews the science behind returning to school is likely to be useful to parents.

The fun starts with a pair of Bank of Canada surveys on Monday. A rich array of measures is revealed by the consumer (October edition here) and business (October edition here) surveys including information on capacity pressures, sales growth expectations, labour shortages, hiring and investment plans and consumer spending plans.

What will matter most to the BoC will probably be the forward-looking measures of expectations for inflation, wage growth and house price growth. One reason for that is because Governor Macklem said so just before the holidays when he stated that “we are closely watching inflation expectations and wage costs.” That was part of a broad set of narrative-shifting remarks that he made with the prime emphasis upon “We are not comfortable with where we are on inflation” (speech recap here). Another reason is that the rest of the surveys’ responses may be marred by the fact that the survey periods pre-dated omicron with responses gathered over November into early December. The BoC takes a very long time to turn around these results! Having said that, if several measures of expectations were shifting in such fashion as to build upon wage and price signals before omicron introduced further shocks to supply chains, then the BoC may be inclined to treat those gauges as fresher indicators.

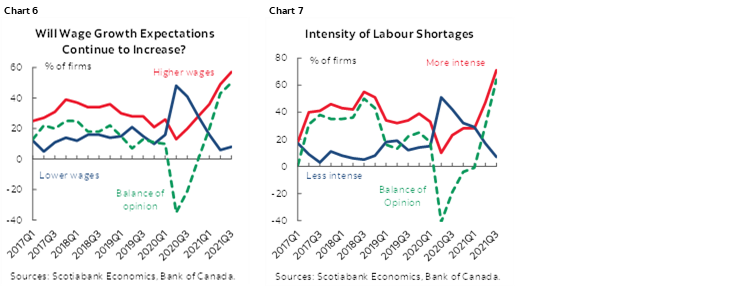

Chart 6 shows that businesses had been ramping up their wage growth expectations as labour market conditions tightened through 2021; further upward pressure would add to the inflation narrative. Chart 7 shows that more businesses have been indicating tightening labour market conditions.

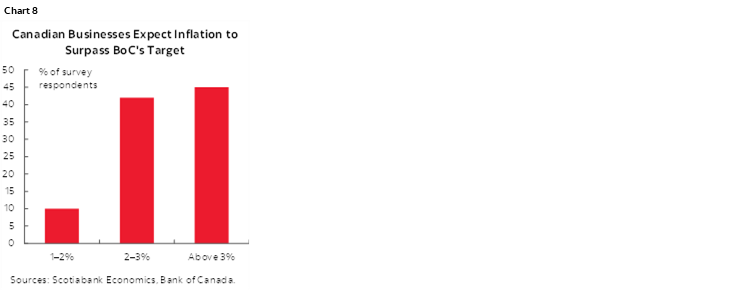

Chart 8 shows that businesses were also sharply raising their inflation expectations over recent surveys to the point to which almost half of firms thought inflation would be over 3% in the coming year and over 87% of respondents thought inflation would be over 2% which is the mid-point of the BoC’s inflation target. Further upward pressure on inflation expectations would risk spooking the BoC into believing they are becoming unmoored.

Households have slightly raised their expectations for house price gains going forward and further upward pressure would probably concern the BoC. That’s especially so in the context of the BoC’s increased concern toward the role of extrapolative house price expectations and investor interest in the real estate market that it fears could foment instability (here).

Chart 9 shows what consumers think (as opposed to the earlier evidence from businesses) will happen to inflation going forward. Consumers are saying that they expect inflation to be above 3% in each of the 1-year, 2-year and 5-year horizons. Again, if expectations rise further then the BoC would be concerned, and it is likely to do so in my view because of the adaptive expectation component and recent history.

CANADIAN INFLATION—STALE AND FISHY

I know, ewww! But it got your attention and with some validity to it. The inflation readings we get for the month of December on Wednesday will be an incomplete picture of true inflationary pressure and a potentially stale one at that in light of the sundry pressures brought on by omicron’s rise.

I’ll start with the guesstimates. I went with 0% m/m for top line CPI inflation in seasonally unadjusted (NSA) terms and 4.9% y/y from 4.7% y/y previously. On the m/m effects, the 0% NSA translates into about about a 0.2% m/m SA gain. December is usually a seasonal down-month for prices. Gasoline prices were also down a bit as a part of that. I'm figuring on a net effect of +0.2% m/m NSA to capture other influences beyond those factors which is kind of in-line with the recent experiences. Base effects add a couple of tenths to the y/y inflation rate.

As for the average of the central tendency core measures, I think they could tick up again from 2.7% y/y. All 3 measures are either on-target (common component at 2%) or well above (trimmed mean at 3.4%). Whatever your preferred measure of core, a deeply negative real policy rate has no place under current Canadian circumstances. Real rates have pushed more deeply negative over the months as an easing offset to omicron's transitory (bad, but transitory) effects. It might also not be surprising to see traditional core CPI (ex-food and energy) at 3.1% jump higher and ditto for CPIX at 3.6% that could jump toward 4%.

I sense that some clients still think the BoC places greatest emphasis on common component CPI. Not so. They dissed that in the April MPR last year by explaining a) it only reflects slack conditions when spending patterns don't materially change, but when they do as in the pandemic it is thrown off, and b) CPI-common is more susceptible to base year effects than the other central tendency gauges. That's because common takes a literal y/y measure, whereas the trimmed mean and weighted median gauges take m/m rolling compounded changes that are weighted and annualized (ie: not a simple y/y). All of which is to say this is why the BoC now appears to talk about 7 measures of core inflation. Yep, 7. Throw it all at the wall and see what sticks. That’s ok since they’re pretty much all sticking with all but one (possibly distorted) core measure above target and some are way above.

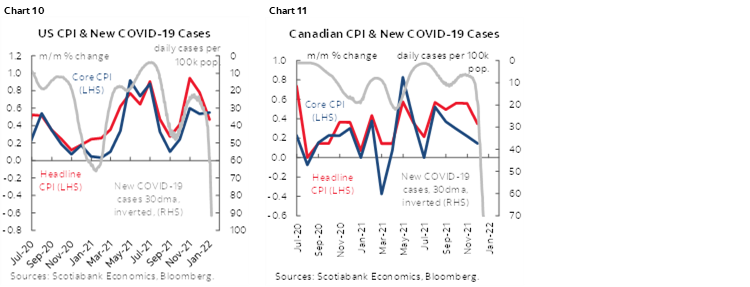

Let’s start with why December CPI is stale, why that matters and then leave the delectable little fishy bits until afterward. Given that the figures will be for the month of December they probably won’t capture significant effects from omicron. Unlike the evidence for the US that shows an inverse relationship over a fair stretch of time between pandemic cases and m/m price changes (chart 10) such that as cases rise monthly price changes tend to ebb, the evidence is less convincing in Canada (chart 11). It’s possible that this Canada-US difference that confronts relative inflation-traders and central bank watchers is because of different policy responses to rising cases in the two countries. For instance, when cases climbed in Canada this prompted tightened restrictions and lockdowns from last March to May in large parts of the country. In several key parts of the country like Ontario the schools remained offline through to the end of the school year. When all of that happened, it drove prices higher because of the damaging effect upon supply chains in Canada. It’s possible that as Canada does this again we may well see inflation light-up once more in Canada but less so in the US.

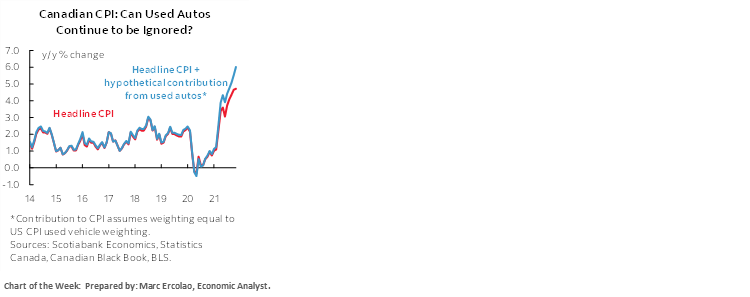

As for the promised fishy bits, the main emphasis here is upon used vehicles. I’ve had the odd fishy one in my younger years, but the point here is that Statistics Canada has whined for years about how it cannot possibly overcome the uncertainties around measuring used vehicle prices that its counterparts in the US, UK and elsewhere have somehow managed to address. Because used vehicles are omitted from CPI (using only inferences from new vehicles) they are excluding pretty much the hottest source of inflation in North America today.

How to address this is a question of sources. We don’t feel comfortable using Canadian Autotrader data on used vehicle prices to inform potential CPI contributions because a) they switched from reporting median to mean prices into 2021 so the series lost comparability, and b) it’s not as fresh, with the latest readings up to September 2021. Instead, we used Black Book’s used vehicle price index (chart 12). It has its own drawbacks like the fact it’s an average drawn from wholesale auctions, it is skewed toward 2–6 year old vehicles and it covers vehicles in average condition, though it does adjust for weighted composition of prices, vehicle age, mileage and condition.

Now for the punchline. If used vehicles were included in Canadian CPI using this measure that was up by about another ~4% m/m and 42% y/y in December and at a similar weight to US CPI (~4%) then it would mean true inflation would be higher by 0.1% m/m and 1.4% y/y than whatever StatsCan will say it is on Wednesday. See the front cover chart for one estimate of how the freshest used vehicle price figures would add to Canadian inflation. Maybe, just maybe they’ll finally weigh in with something to say on the topic??

A HALF DOZEN CENTRAL BANKS

Several central banks will weigh in with updated policy decisions this week. Four out of the six main ones that are on tap are not expected to change their policy stances. Neither is the Bank of Japan but updated forecasts and possibly addressing what ‘sources’ have said of late could be focal points. The main emphasis may be upon China’s central bank.

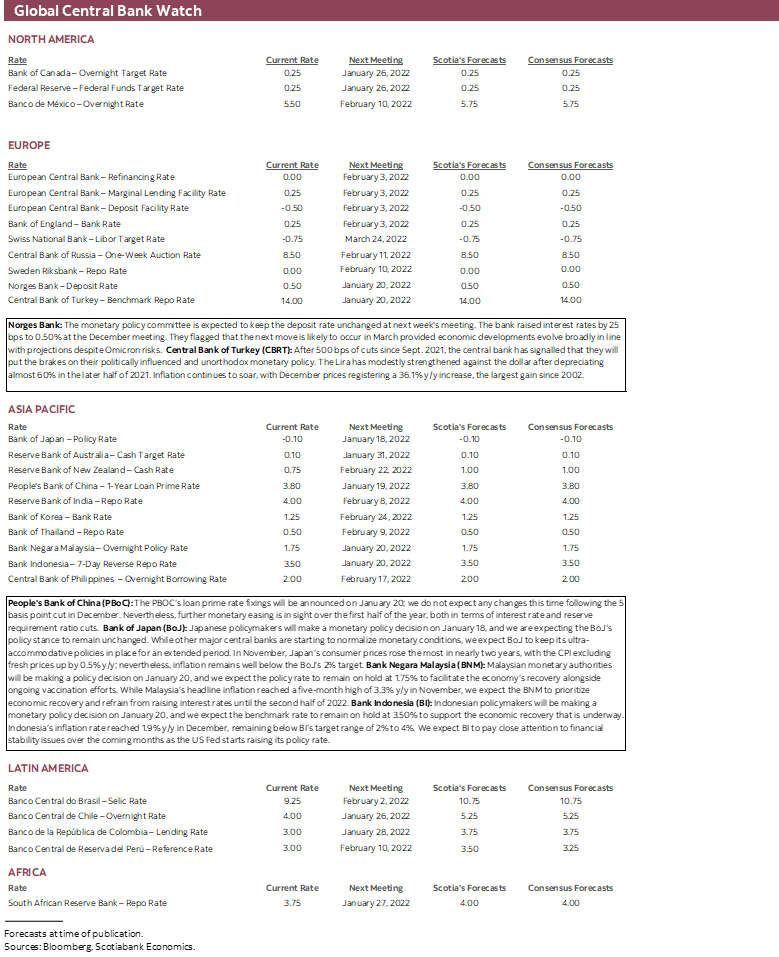

- Bank of Japan (Tuesday): Did you hear the one about the Bank of Japan getting ready to hike because of high inflation? Absent a rumour, start one I suppose (here). “Sources” are saying the Bank of Japan is thinking of a rate hike at some point beyond this year and debating how to manage the messaging. The rationale? Inflation is picking up, or so we’re told. Right. Inflation was 0.6% y/y in November and next week’s expectation for December is 0.9%. Ex-food & energy, prices are lower at -0.6% y/y and falling (chart 13). December’s update arrives on Thursday. Maybe these ‘sources’ would care to step forward?

- PBOC (Wednesday): The People’s Bank of China cut its 1-year Medium-Term Lending Facility and 7-day repo rates to start the week. Watch for at least the 5-year Loan Prime Rate and possibly the 1-year LPR to be cut on Wednesday as the earlier 1-year LPR cut in December was half of the PBOC’s MLF cut. Additional reductions to required reserve ratios are also likely as a lagging policy easing cycle responds to mounting downside risks to China’s economy and absent inflationary pressures.

- Norges Bank (Thursday): After hiking its deposit rate by 25bps to 0.5% back on December 16th, Norges Bank guided that it was planning a further hike likely at the March meeting when another round of forecasts and freshened rate guidance arrives. That naturally implies they will stay on hold this time.

- Bank Indonesia (Thursday): Consensus unanimously expects BI to hold its 7-day reverse repo rate at 3.5%. Inflation remains low with CPI at 1.9% y/y and core CPI at 1.6% y/y. Growth is also largely absent with Q4 GDP expected to be little changed and 2022Q1 GDP forecast to dip. As the Fed moves toward hiking, however, the capital account implications for the rupiah and concomitant implications for inflation and stability will present fresh challenges to the central bank.

- Bank Negara (Thursday): Malaysia’s central bank is expected to hold its overnight policy rate at 1.75%. With inflation running at just over 3% y/y the central bank’s communications will be monitored for indications it is getting closer to starting the withdrawal of policy stimulus.

- Turkey (Thursday): Governor Erdogan Kavcioğlu is expected to hold the one-week repo rate unchanged at 14% after guiding that the 100bps cut in December may be the end of the easing cycle.

US EARNINGS SEASON

Against a relatively quiet US macro calendar, the main focus in US markets will be upon the Q4 and full year earnings season after its checkered start via mixed results for individual banks at the end of this past week.

Thirty-five S&P500 firms will update earnings including names like Goldman Sachs (Tuesday), BofA, and Morgan Stanley (Wednesday), Netflix (Thursday), United Airlines (Wednesday) and American Airlines (Thursday). Analysts have set fairly modest expectations for how the season is expected to evolve (chart 14).

OTHER MACRO—CHINA, UK AND AUSTRALIA IN FOCUS

A wave of global indicators of varying degrees of freshness also lies in store. Key emphasis will be upon China, the UK and Australia.

China updated Q4 GDP and December gauges on Monday but the readings were arguably stale as China’s zero Covid policy became more binding and the impact of omicron on key export markets likely intensified into ’22Q1. Q4 GDP grew by just 1.6% q/q SA non-annualized (1.2% consensus), retail sales grew by less than half of what was expected (1.7% y/y, consensus 3.8%) and industrial output was up by 4.3% (consensus 3.7%)

UK inflation arrives for the month of December on Wednesday. Headline CPI is expected to remain just over 5% y/y with core inflation ~4% y/y. The month-over-month price increases have exceeded consensus expectations for five of the past seven months if that’s any guide. The inflation reading may be less stale than elsewhere because omicron was taking off first in Europe (after Africa) and then made its way elsewhere. Higher prices via damaged supply chains could be one consideration behind expectations for retail sales to decline in Friday’s December reading. Other key readings on the UK job market will also matter.

A pair of employment reports land next week with the UK leading on Tuesday, followed by the Aussies on Wednesday. The jobs print for UK jobs in October (+74k, revised down from +160k) revealed that the ending of the government furlough scheme had little impact on the state of the job market. Flash estimates for November point to another strong gain of +257k jobs (chart 15), further reinforcing the tightness in the UK labour market. The reading will further inform whether the BoE will continue their tightening cycle after a +15 bps surprise hike in December–markets are currently pricing a hike for the February meeting.

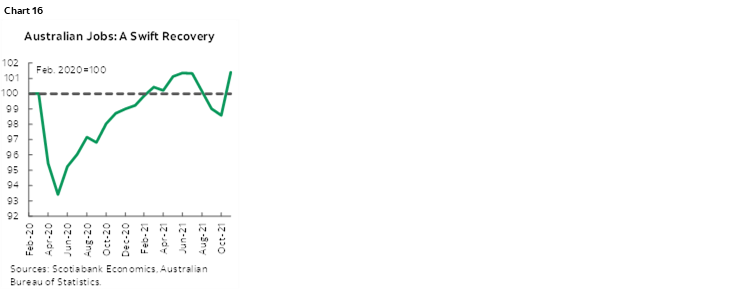

Australian jobs smashed consensus estimates last month with a gain of +366k jobs, swiftly recapturing the almost identical number of jobs lost during the three-month lockdown from Aug.–Oct. (chart 16). The job gain was not from newly created jobs but rather primarily a function of workers re-entering the workforce after being separated from their employment. There still exists a hefty pool of job-attached workers who are either unemployed or not in the labour force that should slowly reintegrate into work over coming months, which will subsequently drive employment and participation rates up.

Other Canadian indicators are likely to fade behind inflation and BoC surveys ahead of the following week’s policy decision. Monday brings out manufacturing sales but they’ll be stale for November and we already have advance guidance that sales were up by 0.6% m/m. Existing home sales during December land the same day and have been on a three-month winning streak. Housing starts during December (Tuesday) probably face downside risk following the larger 26% m/m spike in November. Finally, Friday’s retail sales for November will also be stale and here too we have advance guidance that sales were up by 1.2%; having said that, watch for advance guidance on December’s sales as the key.

This will be a light week for US economy watchers as most of the attention will focus upon earnings reports. Bond and equity markets will be shut on Monday for Martin Luther King Jr Day (this is still one of the most powerful speeches ever made). Minor gauges will include housing indicators such as starts during December (-2% m/m, Wednesday) and home resales for December (-0.5% m/m, Thursday). Industrial readings will include the Empire and Philly Fed regional manufacturing gauges on Tuesday and Thursday, respectively.

Core Eurozone markets only face the ZEW measure of investor expectations that is among the key, fresh survey-based forms of evidence to inform GDP growth expectations. January’s readings for Germany and the Eurozone aggregate arrive on Tuesday.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.