Next Week's Risk Dashboard

- Powell et al get a chance at a redo

- More revision risk, this time to US CPI

- Delayed German inflation could influence ECB thinking

- China’s inflation might have picked up on reopening

- The odds may favour another Canadian job gain

- BoC’s Macklem front-runs new minutes

- Banxico to hike again

- Peru’s central bank still hiking

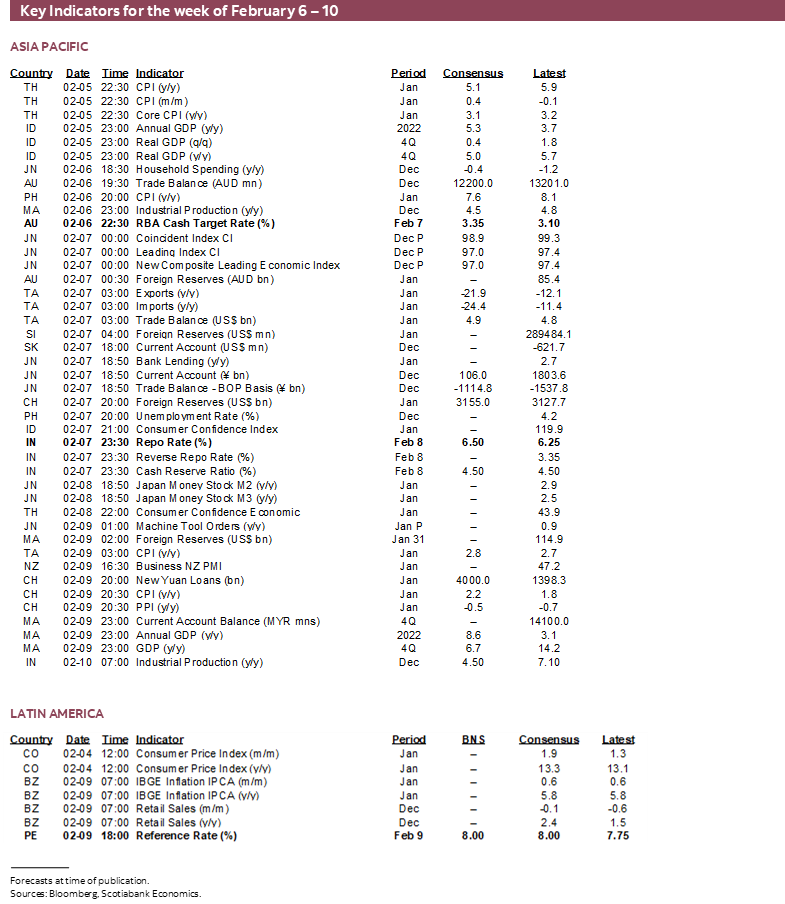

- RBA to hike, perhaps signal pause

- RBI might strike a finer balance

- Riksbank’s refreshed forward guidance

- UK economy likely ended 2022 on a sour note

- Other macro

Chart of the Week

After a blow-out US jobs report that rocked global markets the key this coming week could be the extent to which downside risks to the US economy have been reduced enough to influence global central banks. It’s just one report, but after Chair Powell’s recent press conference resulted in temporarily easier financial conditions, he and other FOMC officials might seek to use payrolls as grounds for a more confidently hawkish stance this week.

Communications from the Bank of Canada that precede another report on jobs and wages may play a similar role.

Delayed German inflation could inform market perspectives toward ECB President Lagarde’s recently lackluster appearance when she waffled somewhat on the next move and sounded more balanced toward inflation risk. That is despite the possibilities that less downside risk to the euro area economy and the global economy plus more purchasing power amid weaker than expected energy prices could fan upside risk to Eurozone core inflation.

Fresh decisions by the RBA, RBI, Banxico and Peru’s BCRP will also have to weigh the evidence with further hikes being favoured. Inflation updates will dominate global indicators.

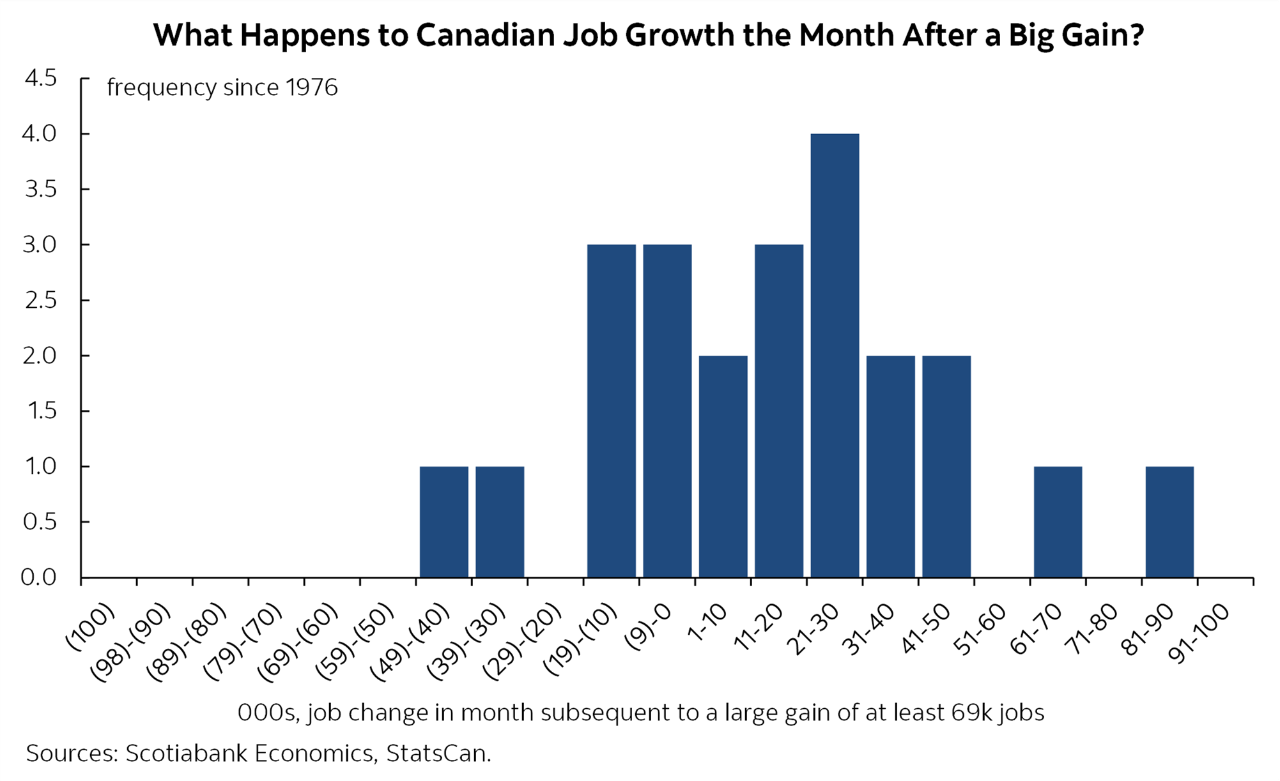

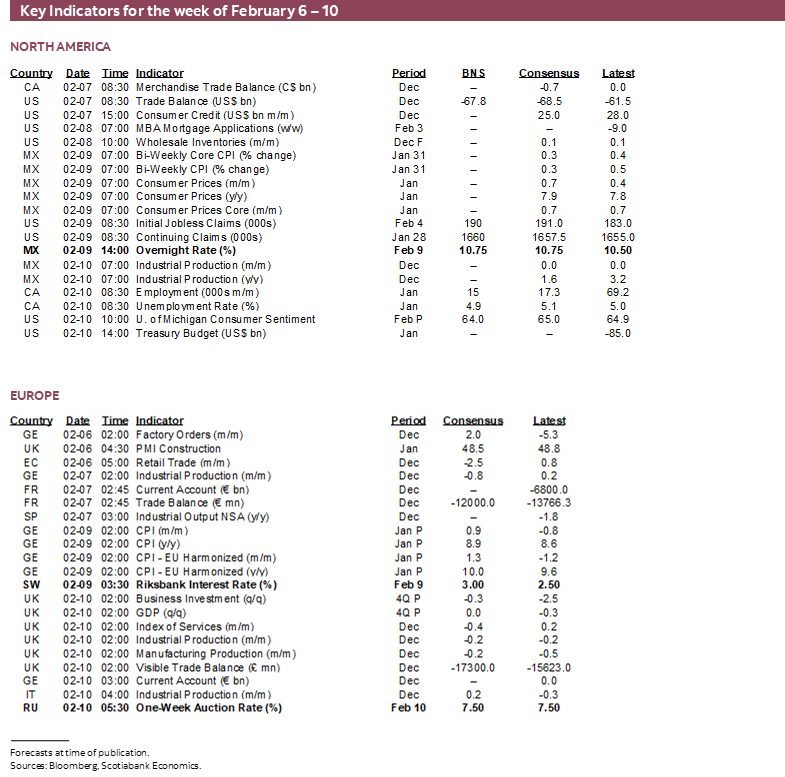

CANADIAN JOBS—THE ODDS MAY FAVOUR ANOTHER GAIN

Canada spins the wheel on the latest estimates for job growth, the unemployment rate and wage growth during January on Friday. I’ve tentatively gone with another gain of 15k, a downtick in the unemployment rate to 4.9% and expect wage growth to be resilient.

What goes up, must come down, right? Maybe not for Canadian jobs. After a revised 69k job gain during December (more here), statistical momentum favours another job gain in January. In all months since the Labour Force Survey’s inception in 1976 when job growth has been equal to or greater than December’s pace, the next month has tended to be another gain. This is shown in chart 1. That’s not always true, but the next month was up in 15 out of 22 times since the LFS’s inception in 1976 when the monthly gain has been 69k or greater.

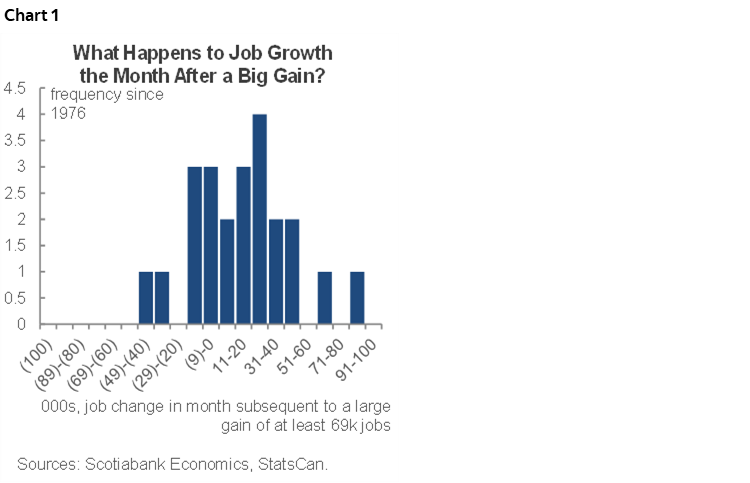

Supporting continued job gains are the facts that job postings remain elevated (chart 2) and so are lagging job vacancies.

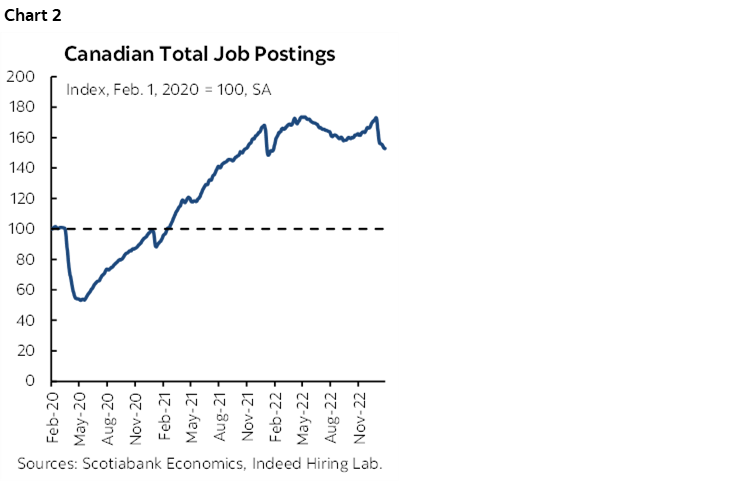

The layoffs issue in Canada appears to be of modest concern but admittedly we’re more reliant upon very soft data to gauge this factor relative to the US that tracks layoffs more closely. Chart 3 uses Google search trends for key words like ‘unemployment benefits’ and ‘laid off’ on the theory that folks searching for such terms may have experienced job loss. As the chart shows, there was a mild increase in such searches into the reference week for the LFS that includes the 15th day of the month and mostly for the ‘laid off’ term, but the larger and more volatile spike was after this week. That seems to conform to anecdotes I’ve observed.

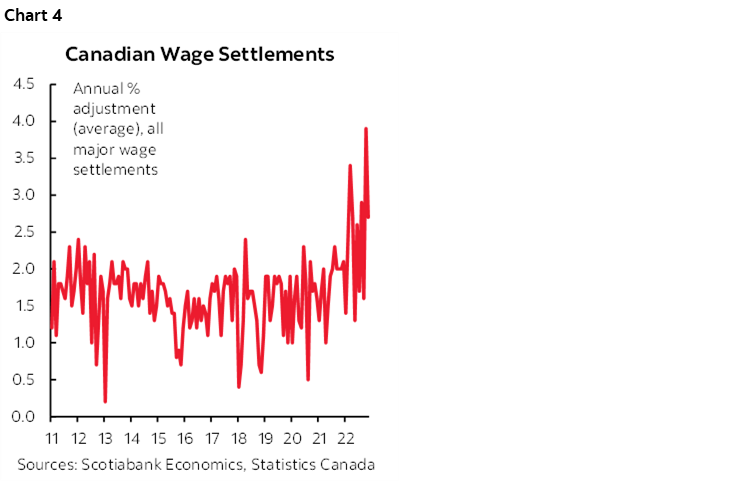

Also watch the wage figures. The prior month’s annualized gain decelerated but the three-month moving average trend remained hot and lagging figures for major contract wage settlements has continued to accelerate (chart 4).

A secondary matter involves addressing StatCan’s recent annual revisions to the LFS. Barring extreme circumstances like errors and unlike the US, the agency does not revise the figures each month. They did revise December’s gain down from 104k m/m to a still-hot +69k, but in the process also revised up the gain for 2022 as a whole from 394k to 409k which makes for an incredibly strong year. Due to cumulative revisions the overall level of employment at the end of 2022 is now 112k higher.

The revisions did not affect the overall rate of unemployment that was left unchanged at 5% to end 2022 which indicates no material change in estimates of tightness. Modest changes to overall employment in a country with 19.9 million employed people were offset by modest changes to the labour force.

Revisions to cumulative wage growth now point to being slightly lower to end 2022 because it was raised to be slightly higher previously. From a previously reported 5.1% y/y growth in average hourly wages in December 2022 we’re now at 4.8% whereas the growth rate one year ago was revised up to 3.3% instead of 2.7%.

CENTRAL BANKS—EVERYBODY NOW, WHO WANTS A FED REDO??!

The titans of North American monetary policy all weigh in this coming week alongside several other regional central banks.

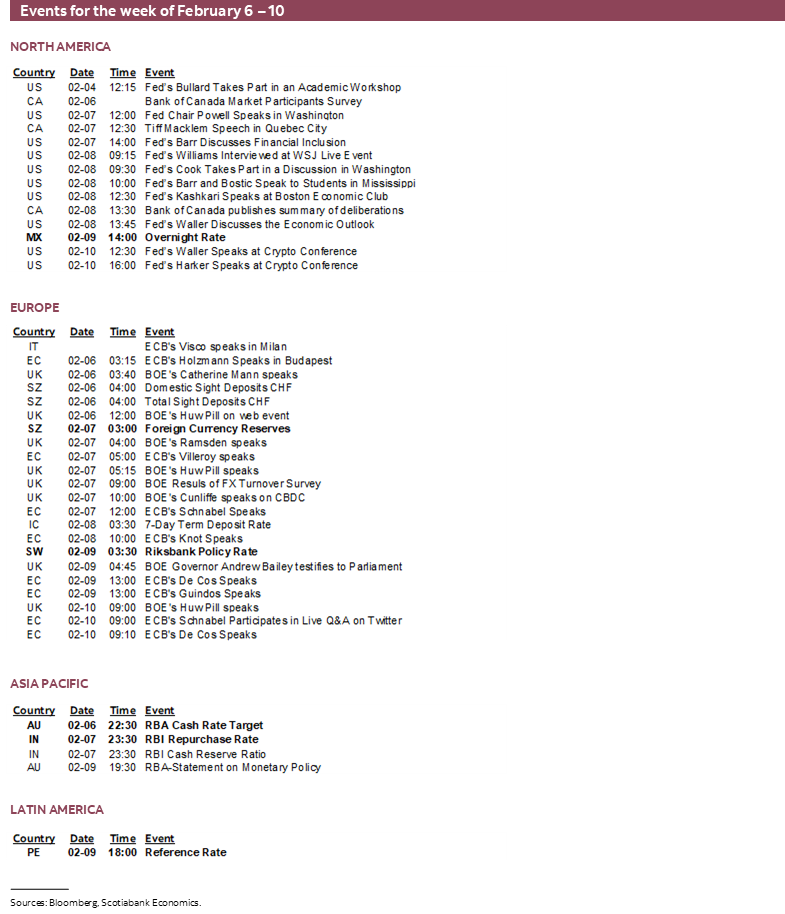

Fed Chair Powell Take 2?

Global markets may be sensitive to any tone shift coming from Fed Chair Powell when he will be interviewed before the Economic Club of Washington on Tuesday between about 12–1:30pmET (here). Here is what to watch:

- I felt that the Chair’s performance during his post-FOMC meeting press conference was lackluster (recap here) and that this may have contributed to the strong rally in Treasuries before they got thumped by payrolls. Was Powell satisfied by the market reaction to his presser?

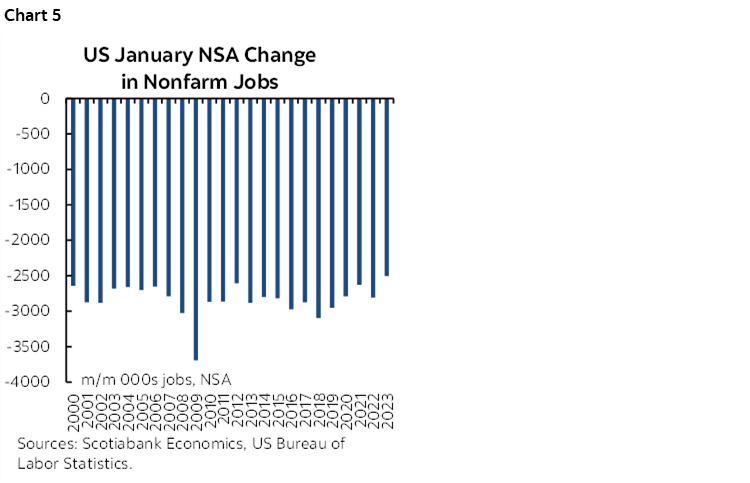

- Did the incredibly robust nonfarm payrolls report including revisions affect his thinking in the aftermath of the FOMC meeting? A recap is here. Some have dismissed the report as a seasonality distortion which is patently false; seasonally unadjusted payrolls typically fall in January but this year’s decline was among the softest for a month of January which indicates some combination of less post-holiday layoffs and more hiring than usual (chart 5). Applying seasonality factors to this drove some of the upside along with the powerful effects of large positive revisions for a genuinely very strong report. Powell might be inclined to say it’s one report and they need more information such as two more inflation readings before the next decision, but it would be surprising if he did not sound more enthusiastic toward the state of the US job market. He will probably follow the general tone of San Fran Fed President Daly (voting 2024)—a labour economist by background—who remarked post-payrolls that it was a “wow number” that indicates the labour market is really strong.

- Will he reveal the tone of the discussion at this meeting? Recall he said “wait for the minutes” and that “The sense of the discussion was talking quite a bit about the path forward.”

Other Fed-speakers will include several hawks. Bullard appears over the weekend. Governor Waller appears twice later in the week. Philly’s Harker speaks on Friday. Governor Cook (Wednesday), Vice Chair Barr (Tuesday, Wednesday), Atlanta’s Bostic (Wednesday), Minneapolis President Kashkari (Wednesday) and perhaps others will all scramble for the mic in the wake of payrolls and the market reaction to the FOMC’s recent communications.

Bank of Canada Governor Macklem Front-Runs Minutes

I’ll be at the Governor’s speech on Tuesday in gorgeous Quebec City. His topic is ‘how monetary policy works’ with the speech landing at 12:30pmET followed by his press conference at about 2pmET. It’s doubtful that he will offer materially new information of concern to nearer term market expectations given the pause signal that was sent on January 25th meeting (recap here). Since then there really hasn’t been much of anything new on the domestic scene other than GDP estimates for November and December (recap here) that are roughly tracking in line with the BoC’s revised forecasts in the January MPR.

The BoC will release minutes to its most recent meeting for the first time ever the very next day (1:30pmET). This is happening partly at the behest of the IMF. I wouldn’t say we should expect a quantum leap forward in terms of revealing inner disagreement and public discourse of the sort that occurs at the Fed, the ECB, the BoE etc. The BoC has a relatively more insular culture, but there could be a nugget or two in the formally titled Summary of Deliberations. Perhaps Macklem will speak to the minutes during his appearance the day before.

RBA—You Got Another Hike Coming

Most of consensus expects another 25bps hike into Wednesday. Markets are mostly priced for a quarter point. The central bank had suggested that a pause was considered at the prior meeting in December which makes this call less than a slam dunk.

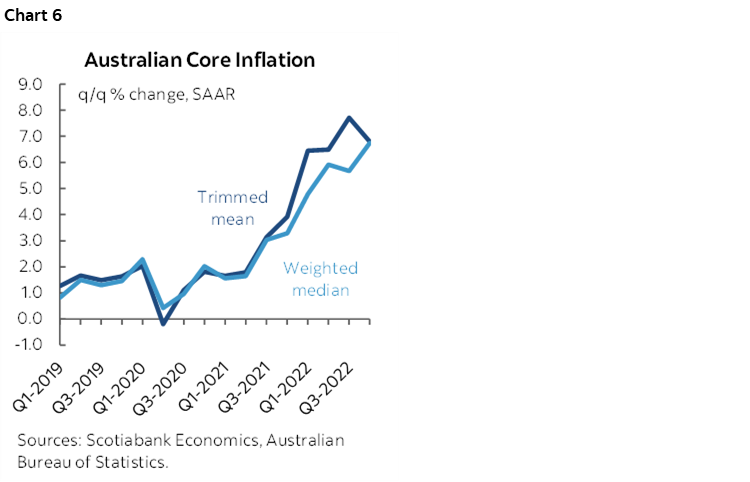

Still, what tilts the balance of opinion toward another hike was the strong upside surprise to Australian inflation not only in Q4 but also for the final month of the year, given that Australia started to release monthly CPI estimates in October. Annualized changes in central tendency gauges including trimmed mean CPI and weighted median shot higher in Q4 (chart 6). There may be pause guidance at this meeting but the hot inflation figures and China rebound narrative challenge whether the RBA should instead keep its options open.

RBI—Resilient Core Inflation

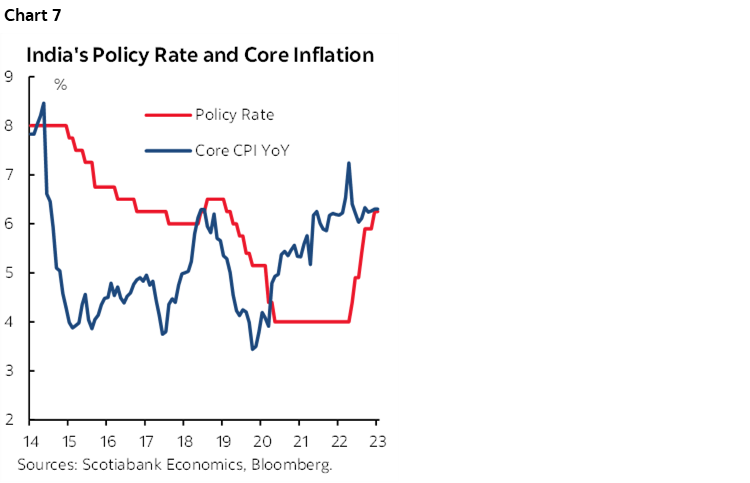

Most economists expect another 25bps hike from the RBI into Thursday. That would take the repo rate up to 6 ½% for a cumulative increase of 225bps since policy tightening began last April. OIS markets are priced for most of a quarter-point hike. Key is whether the Monetary Policy Committee will continue to vote in favour of further withdrawal of policy accommodation after a 4–2 vote in favour of doing so in December, or whether it may signal a hard pause. While headline inflation subsequently ebbed, core inflation remains resilient (chart 7).

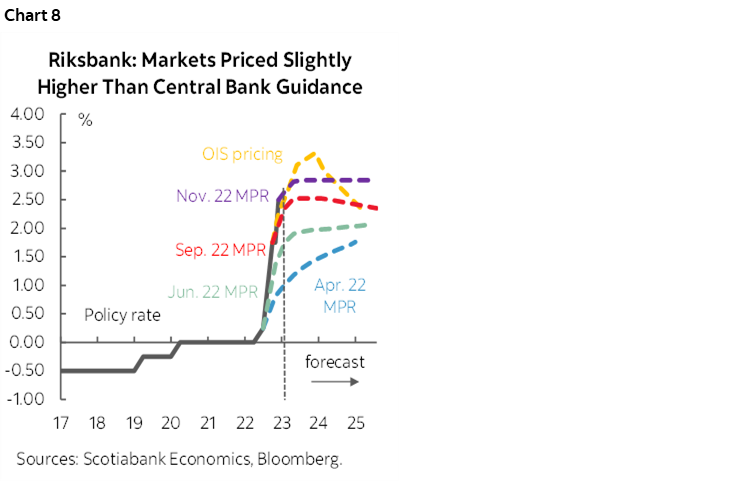

Riksbank—Forward Guidance is Key

Sweden’s central bank is likely to follow the ECB’s 50bps hike with one of its own on Thursday. Markets are priced for it and most of consensus is onside. Key will be forward guidance offered in the fresh Monetary Policy Report’s published forward rate path. The last forecast way back in November has reset the forward rate path to a higher level, yet markets continue to overshoot in the near-term while pricing a quicker return to rate cuts than the central bank has guided (chart 8). Given the central bank’s prior experience with premature easing it may be setting a high bar against such expectations.

Banxico—Stuck to the Fed

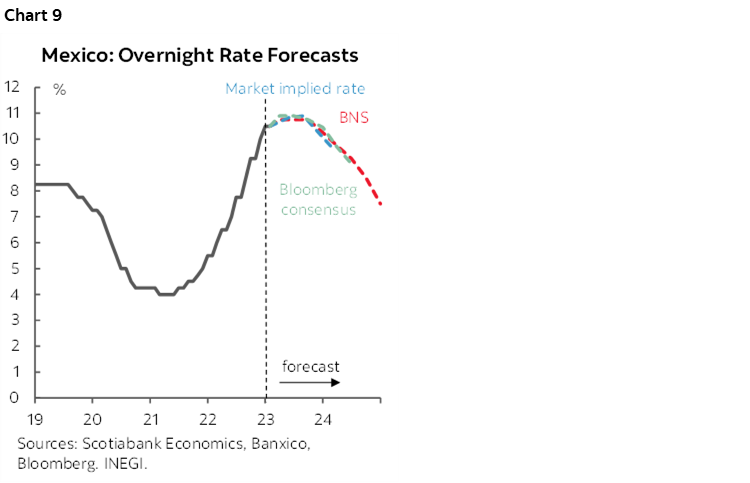

Mexico’s central bank is expected to hike its overnight rate by 25bps on Thursday and therefore continue to match the Fed’s moves. Another inflation report for January and a bi-weekly reading for the back half of the month will arrive on the morning of the decision. Renewed upward pressure on bi-weekly core inflation into mid-January is likely to further reinforce the rationale for the hike and postpone any consideration of diverging from the Fed with rate expectations shown in chart 9. A very strong US jobs report and other strong data like ISM-services and vehicle sales could also be taken as signals of a strong set of external conditions to merit additional policy tightening.

Peru—Protests Complicate the Outlook

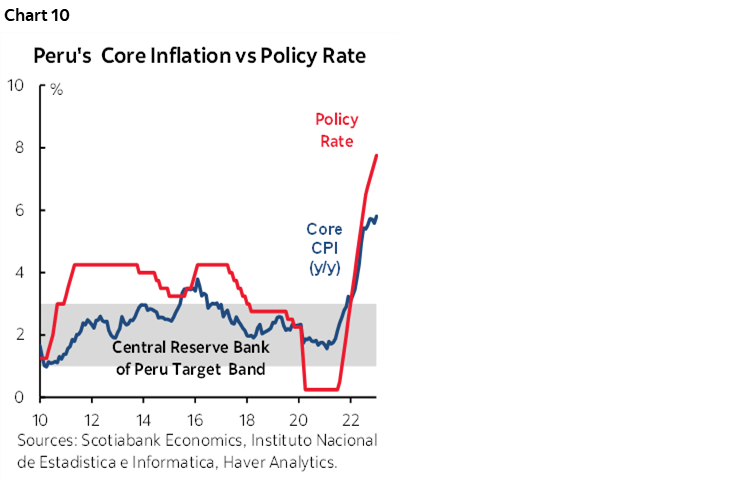

Consensus generally expects BCRP to hike by another 25bps on Thursday evening (eastern time). The pick-up in January’s inflation reading was less than expected, but it still accelerated to 8.7% y/y with the core rate of inflation rising to 5.8% y/y (chart 10). Protests in the southern part of the country where key resource riches lie complicate the outlook for the economy and inflation including bottleneck pressures. The sol has depreciated a touch further since the last policy decision on January 12th which may keep alive concern about import-price passthrough effects.

OTHER MACRO—INFLATION WATCH CENTERS ON THE US, GERMANY & CHINA

The main remaining factors that could impact global markets will likely focus upon German and Chinese CPI as well as US CPI revisions.

The US macro calendar will be relatively light beyond Powell’s appearance. Friday’s CPI revisions to the past five years that incorporates possibly refreshed seasonal adjustment factors may be the main event. Tuesday’s trade deficit is expected to widen given we already know the advance goods balance. Weekly jobless claims (Thursday) have been running at very low levels despite layoffs because so far the job market has been strong enough to absorb them. UofM consumer sentiment (Friday) may follow the recently softer Conference Board estimates of consumer confidence given higher gas prices into the new year but job creation may be offsetting.

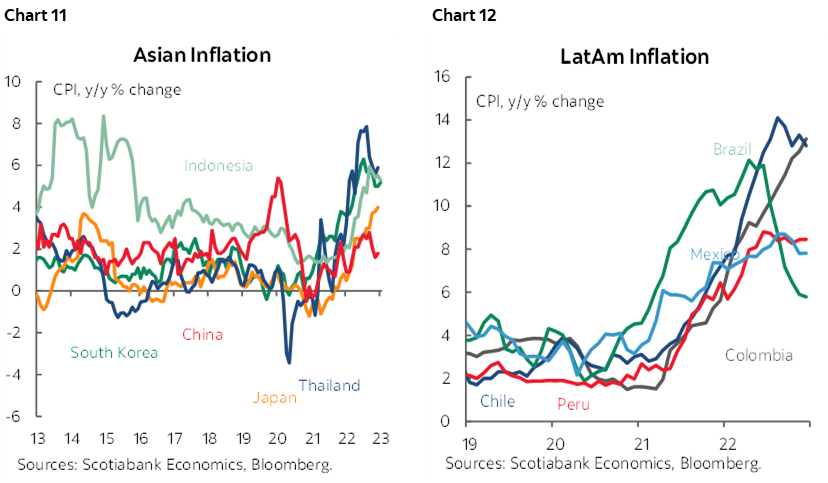

A round of CPI updates arrives primarily from across Asian and Latin American economies. Charts 11–12 highlight the general patterns for many of them.

- German inflation for January is the main one with the potential to disrupt world markets. Recall that the estimates were delayed due to technical difficulties and so Eurozone inflation had to guess at the German component. The January readings on Thursday are expected to jump by over 1% m/m and could drive revision risk to the initially reported EZ estimates.

- Colombia kicks it off on Saturday. Firmer pressure is expected.

- Chile is expected to post a firm m/m headline inflation reading as the year-over-year rate ebbs, but expectations for a rise in core inflation will be more closely monitored (Tuesday).

- Mexico updates CPI on Thursday ahead of Banxico as already noted.

- Brazil’s inflation rate is expected to hold firm at about 5.8% y/y.

- With relaxed restrictions and initial signs of an economic rebound, China’s CPI update for January (Thursday) is likely to come under upward pressure and possibly with more ahead. Thailand (Sunday), Philippines (Monday) and Taiwan (Thursday) also report.

- Norway gets the last word with January CPI on Friday but there will be one more inflation report after this one and before Norges Bank’s next decision on March 23rd.

The UK economy will be a key focal point mainly on Friday when Q4 GDP and December GDP arrive alongside industrial production, the services index and trade figures arrive for December. No growth is expected for Q4 alongside a weaker end to the year.

Canada’s calendar will be fixated upon the previously noted BoC communications and jobs report with the only other consideration being trade figures for December (Tuesday). They will help to inform Q4 GDP growth estimates.

German industrial figures including factory orders (Monday) and industrial production (Tuesday) are expected to offer mixed results with a firmer order book but softer production.

Watch Australian retail sales in Q4 (Sunday) as they are expected to decline given that we already know that December fell by 3.9% m/m.

French wages and Q4 jobs (Wed/Friday), Eurozone retail sales (Monday) and Q4 GDP from Indonesia and Malaysia round out the highlights.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.