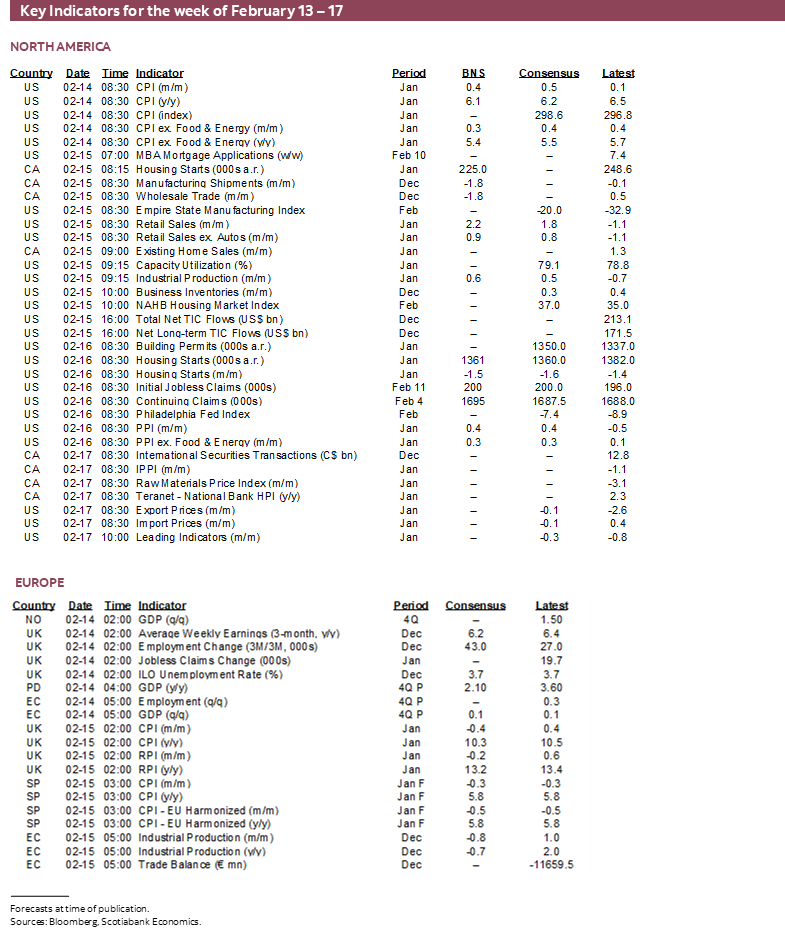

Next Week's Risk Dashboard

- US consumer bounces back

- US CPI set to rebound with firm core

- BoJ: We have a name, but now what?

- PBoC restrained by resurfacing yuan pressures

- BSP likely to hike again

- BI probably done

- Eyes on UK wage growth

- Australian jobs may inform RBA’s next step

- Soft UK inflation and retail sales

Chart of the Week

Fed-fighters haven’t been faring so well of late and they might not find much love in this week’s developments either. US headline CPI inflation is likely to spring higher, core inflation is expected to remain resilient and markets may have to reassess how they prematurely wrote-off the US consumer at the start of the year as we brace for a strong retail sales print. Toss in uncertainty around the BoJ as a formal nomination lands, how yuan weakness may be returning to confront the PBoC and key updates on the state of UK and Australian job markets plus UK inflation and heightened market volatility is sure to persist.

US CPI—LOVES TREASURIES, LOVES THEM NOT

The path to the FOMC’s next data dependent decision on March 22nd that will include fresh forecasts and potential changes to the Committee’s prior 5¼% estimate of the terminal rate will bring out two more rounds of CPI inflation readings, one more set of the Fed’s preferred PCE inflation figures and another nonfarm payrolls report alongside a slew of other releases. One such round of CPI figures lands on Valentine’s Day, no less. Given recent movements, Treasury yields and fed funds pricing may be more vulnerable to a downside miss on inflation expectations than a bigger upside surprise.

I have estimated that headline CPI increased by 0.4% m/m SA (0.5% NSA) which would lower the year-over-year rate to 6.1% from 6.5%. The month-over-month rate is what should receive the attention in terms of evidence of inflationary pressures at the margin and clean of year-ago base effects. Core inflation excluding food and energy is estimated at 0.3% m/m SA and 5.4% y/y (from 5.7%).

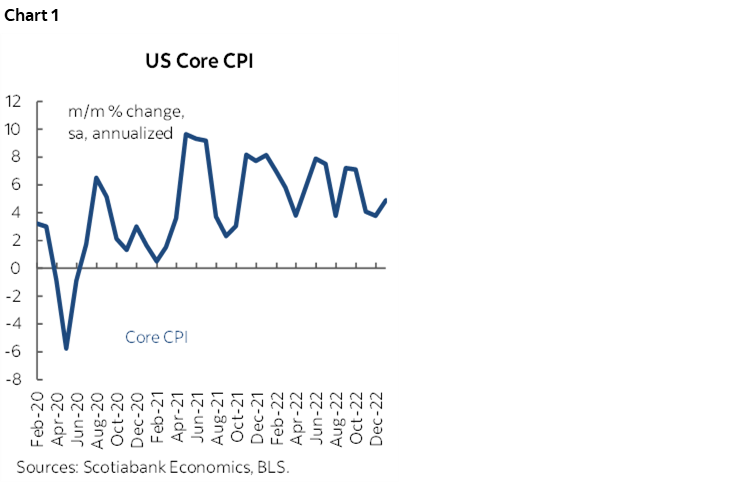

Core inflation is already hotter going into this report than previously understood because of revisions that were made as part of annual seasonality updates. Those updates added to estimates of core inflation (chart 1) by raising the estimates for November and December by 0.1% m/m SA in each case to now post year-end core inflation of nearly 5% m/m SAAR.

We know that gasoline prices were up by about 4% m/m NSA in January which translates into about a 3½% SA rise at a roughly 4% weight which would make for a weighted contribution to CPI of about 0.15% m/m.

Industry gauges also indicate that vehicle prices were little changed in January and shouldn’t move the dial. New vehicle prices appear to have been up 0.1% m/m NSA and down a smidge in seasonally adjusted terms at about a 4% weight while used vehicle prices were up by about 0.4% m/m NSA and 0.3% m/m SA that at a 3.7% basket weight translates into little by way of vehicle contributions to inflation.

Owners’ equivalent rent is expected to remain hot with a continued gain in the vicinity of ¾% m/m SA along with a similar rise in rent as housing gauges continue to face lagging disinflationary pressures later this year into next.

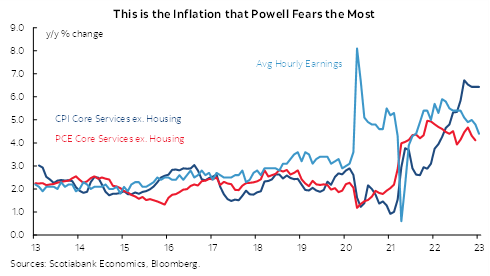

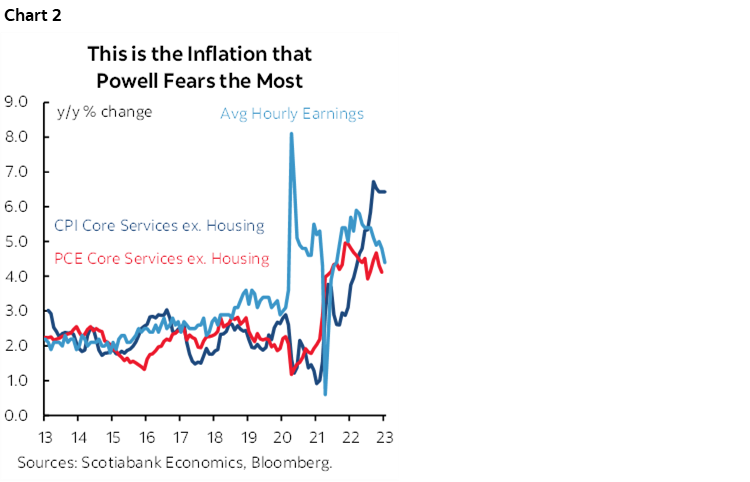

Core services inflation is likely to remain key. Job gains of the magnitude witnessed of late add to the Fed’s concerns around the connection between services inflation and job growth. The extent to which such gains fan further tightening of the job market and along with it wage gains is a worry to the Fed because, as Powell explained in his speech on inflation in late November (here), there is a rough connection between wage gains and core-services inflation ex-housing (chart 2).

A further complicating factor may be updated basket weights applied to CPI in this round of figures. Starting this year, the BLS will apply updated weights each year using the annual break down of consumer expenditures for 2021 versus the prior practice of updating weights biennially.

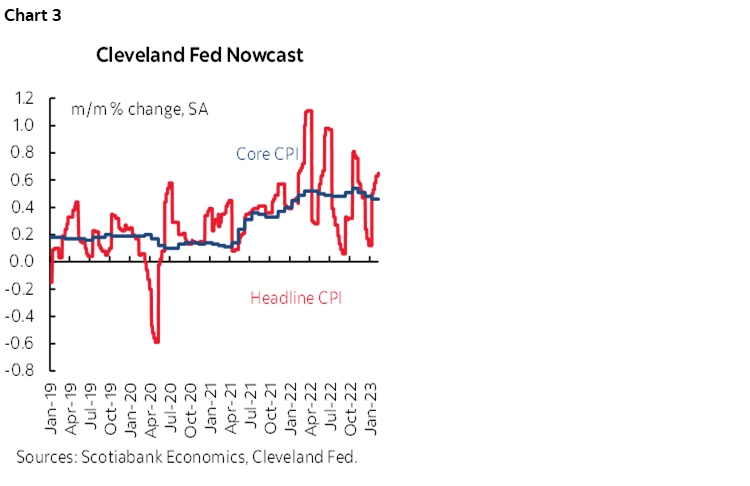

Finally, while they have overestimated inflationary pressures somewhat of late, the Cleveland Fed’s ‘nowcast’ measures for headline and core inflation point to significant upside risk to estimates (chart 3).

US CONSUMERS PREMATURELY WRITTEN OFF?

After the drop in retail sales during December, markets seemed to believe that US consumers were on their way out. A strong rebound this week could drive everyone to the other side of the ship. We’ll find out on Wednesday when US retail sales for January give a first glimpse at the new year.

I’ve estimated a sharp rise of 2.2% m/m for total retail sales and 0.9% m/m for sales excluding autos.

We know that auto sales volumes were up by 18% m/m SA in January and that could single-handedly add over 2½ percentage points to total retail sales growth.

Gas prices were up by about 3½% m/m SA which should add another few tenths to sales growth, given that the US reports retail sales in nominal terms. Expectations cited above for core inflationary pressures could add a bit more when translated into categories aligned with retail sales.

The key will nevertheless be sales ex-autos and gasoline. Those sales fell by 0.7% m/m in December and that weak hand-off into January could prompt a rebound. So could evidence drawn from spending on payments cards. Deferred use of gift cards could be another driver. Another could be that holiday shopping for goods was brought forward to earlier in the season in late summer and October given earlier and deeper discounting plus earlier shopping out of concern about product shortages. Furthermore, it could be that services consumption benefited more from holiday festivities this time than goods consumption.

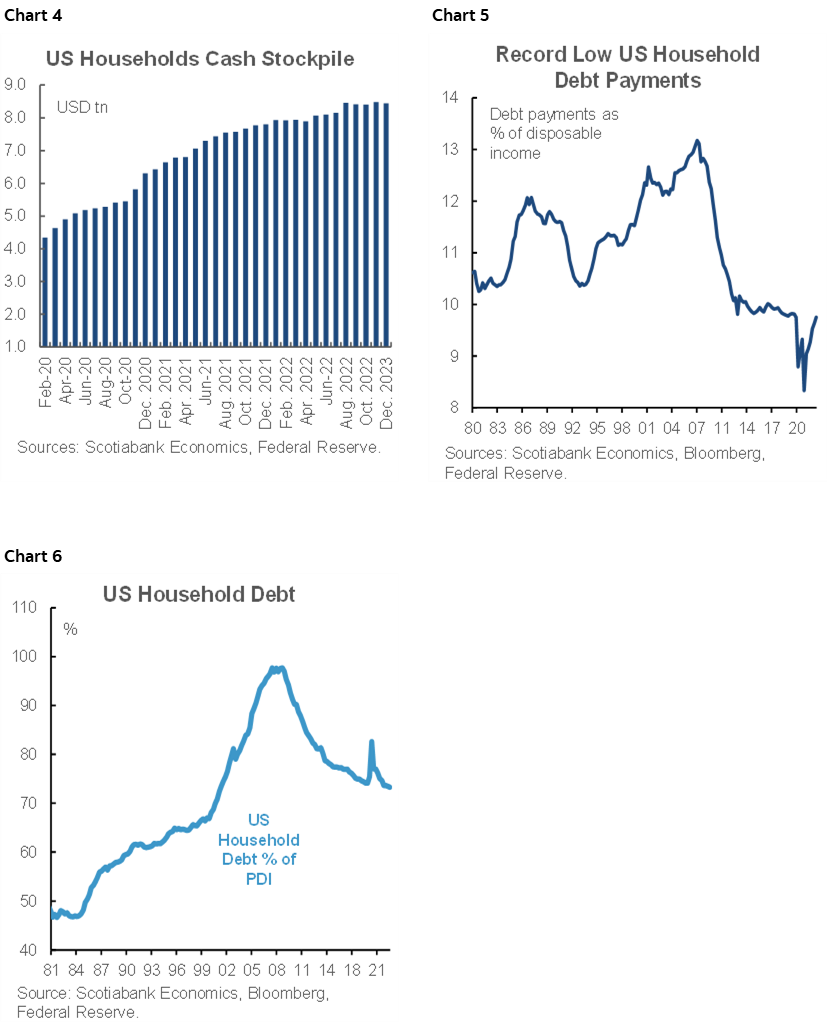

Regardless, the US consumer’s fundamentals remain sound. Job markets are very tight, wage gains are decent, the debt-to-income ratio is at a twenty-two year low, debt payments as a share of incomes are toward record lows, cash balances are very high after socking away pandemic stimulus and Americans have a one-way option to refi in a falling rate environment that locked in pandemic lows for 30-year mortgages. See charts 4–6.

CENTRAL BANKS—THE DUELLING YUAN AND YEN

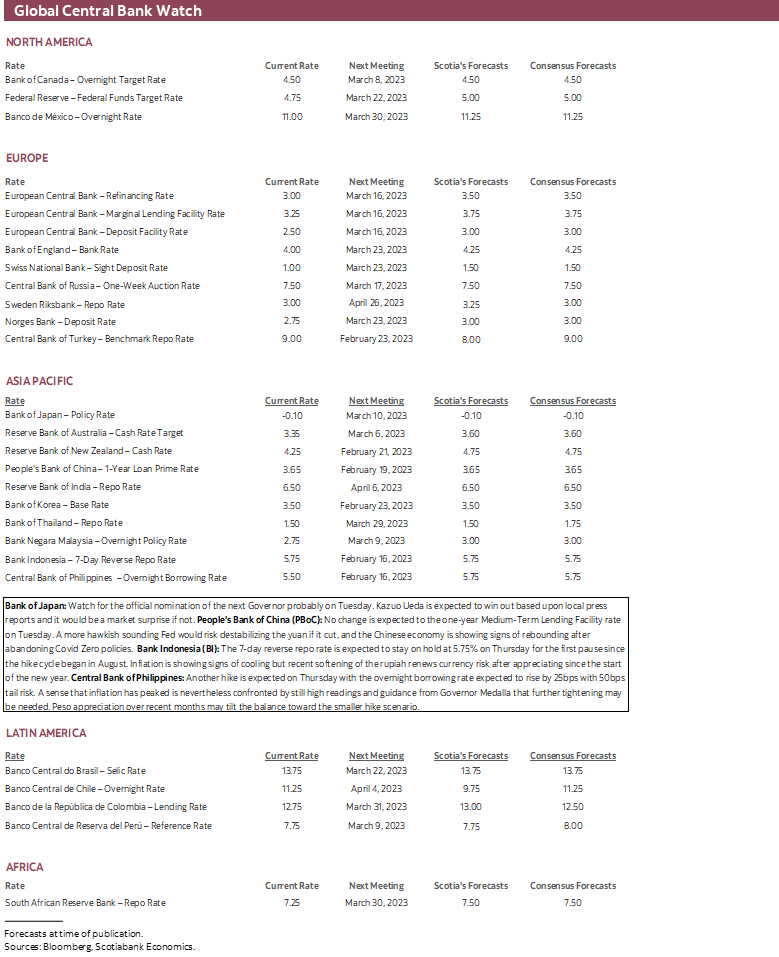

Central bank developments will be focused upon Asia and primarily the Bank of Japan and PBoC.

Bank of Japan—We’ve Got a Name, but Now What?

Watch for PM Kishida’s official nomination of the next Governor to a five year term probably on Tuesday. Kazuo Ueda is expected to win out as Haruhiko’s successor based upon local press reports. After the surprise to markets following those reports, it would be a further surprise if they were to prove wrong which appears to be unlikely. His potential nomination will then have to be approved by Parliament amid reports that the ruling LDP is divided.

What is therefore left is to try to translate this into expectations for action by the BoJ. Markets think they know, since the yen appreciated and a reassessment of global carry across bond markets drove correlated movements toward high bond yields in the wake of the stories.

Never trust the initial market reaction to central bank appointments. It’s usually blind speculation and with several observed instances to support as much. For one thing, it’s a bit puzzling that much of the narrative in advance of the news had painted the likely victor—Deputy Governor Masayashi Amamiya—as being relatively more hawkish and yet Kazuo Ueda—a former Prof and BoJ Board Member—is now viewed this way. Kuroda’s two deputies have been sacked as well and so perhaps the old guard’s out.

From what I’ve read about Ueda’s background that seems to be a stretch. Ueda has a history of cautiously supporting Kuroda’s measures. We still need to get through Spring wage negotiations and cement faster wage growth as the missing ingredient to durably achieving the BoJ’s long-elusive 2% inflation goal versus just temporarily doing so due to lagging yen and oil price effects and it’s the latter narrative that dominates within the BoJ. We still need to have a potential policy review being called and then the conclusions to said policy review and whether they will embrace change or, say, go through this largely useless exercise like the BoC does every five years only to say no change is needed after all.

Personally, I remember when droves of UK market participants were requesting calls and visiting Canada to ask me about Mark Carney and how hawkish they thought he was while mindlessly teleporting that bias across the pond to very different circumstances. Yeah, Canada, just like the UK. Then Brexit hit.

Central bank heads have a degree of control over the direction taken by their organizations, but so does the overall hierarchy within these organizations. Circumstances, fresh developments and collective thinking are more likely to dictate BoJ actions than anything else. The ability to adapt is what makes a good central bank head and from what I see Ueda is praised as someone who is likely to be circumspect and evidence-based in his decision making going forward. Time will tell.

PBoC—Yuan Risk Returns

The People’s Bank of China is likely to leave its one-year Medium-Term Lending Facility Rate unchanged at 2.75% on Tuesday. A more hawkish sounding Fed in the wake of several strong growth indicators would contribute to destabilizing the yuan if the PBoC were to ease at this point. Such risk has resurfaced as the yuan has slightly depreciated since the strong nonfarm payrolls report. The Chinese economy is also tentatively along a rebounding path in the wake of relaxing Covid Zero restrictions as evidenced by PMIs. Officials have also relaxed tech sector and property market constraints while loan growth is showing signs of responding to the prior relaxation of required reserve ratios. Furthermore, while the state targets 3% inflation (and rarely hits it!), headline inflation is inching closer at 2.1% y/y while core inflation is slightly picking up but only sits at 1%.

Bangko Sentral ng Pilipinas—Peso Could Limit Hikes

The majority within consensus expect another 25bps hike in the overnight borrowing rate with a minority expecting a 50bps hike on Thursday (ET). Governor Felipe Medalla recently stated that high inflation “points to the need for sustained efforts to combat price pressures” but that inflation “most likely” has peaked. That was in the wake of another upside surprise to 8.7% y/y inflation in January which is nearly three times the mid-point of the 2–4% target range. If anything holds the central bank back from a large hike at this meeting then it could be ongoing currency appreciation as the peso has moved nearly 8% higher since October.

Bank Indonesia—Done Yet?

Most within consensus expect Bank Indonesia to hold its 7-day reverse repo rate unchanged at 5.75% on Thursday (eastern time as always). That would be the first pause in the hike cycle that began in August of last year and that has raised the rate by 225bps. Inflation remains high with headline CPI up 5.3% y/y but cooling somewhat of late, while core inflation is holding steady around 3¼% y/y and hence near the middle of the 2–4% inflation target range. A wild card may be how the central bank views the rupiah and risks to stability, given its appreciation since the end of 2022 but its renewed slight weakening of late.

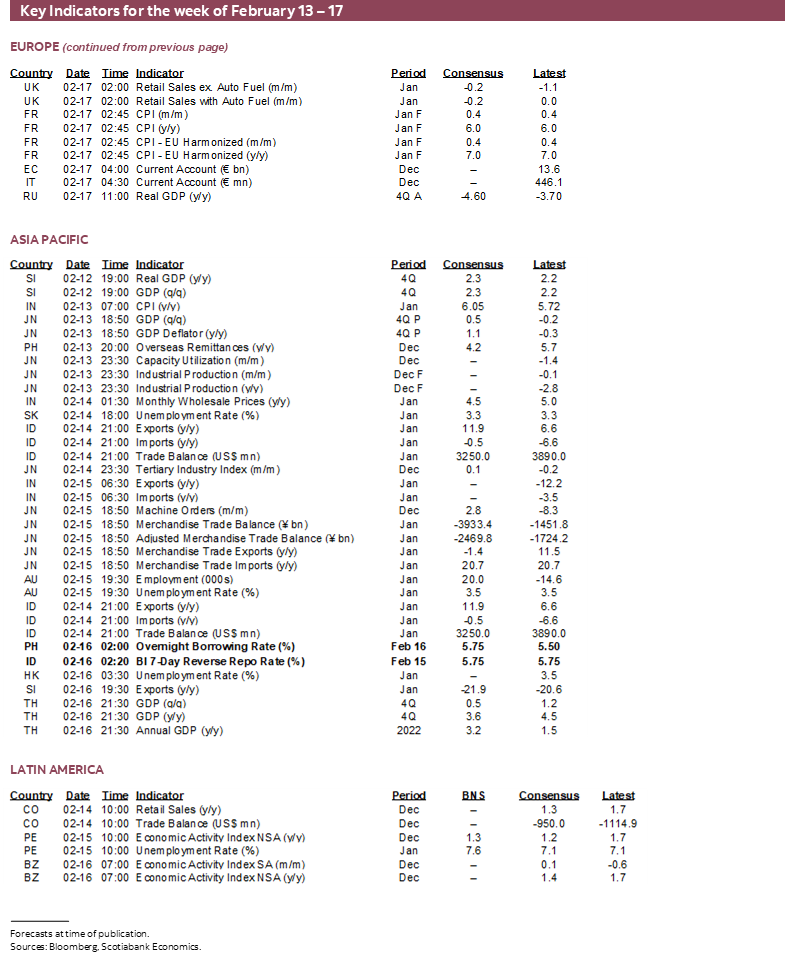

GLOBAL MACRO—BoE, RBA FACE JOB MARKET UPDATES

The rest of the line-up of calendar-based macro risks will primarily focus upon UK jobs and inflation, Australian jobs, RBNZ inflation expectations and a handful of other indicators.

Canada doesn’t face top-shelf macro reports or key calendar-based risks this week but there will be a few macro reports that are due out on Wednesday that could help fill in the blanks after another stunning jobs report that calls into further debate the longevity of the BoC’s conditional pause (here). Housing starts may dip given softening permit volumes and Statcan has already guided that the nominal values of manufacturing shipments and wholesale shipments both fell in December pending information on volumes. Existing home sales for January arrive that same day.

Other US macro reports will include industrial sector readings such as Wednesday’s industrial output and Empire manufacturing gauge and Thursday’s updates for the Philly Fed’s business outlook measure and producer prices in January. Weekly jobless claims and housing starts arrive on Thursday.

Latin American markets only face Colombian GDP during Q4 that is expected to register a mild contraction on Wednesday, plus Peru’s unemployment rate for January on Wednesday.

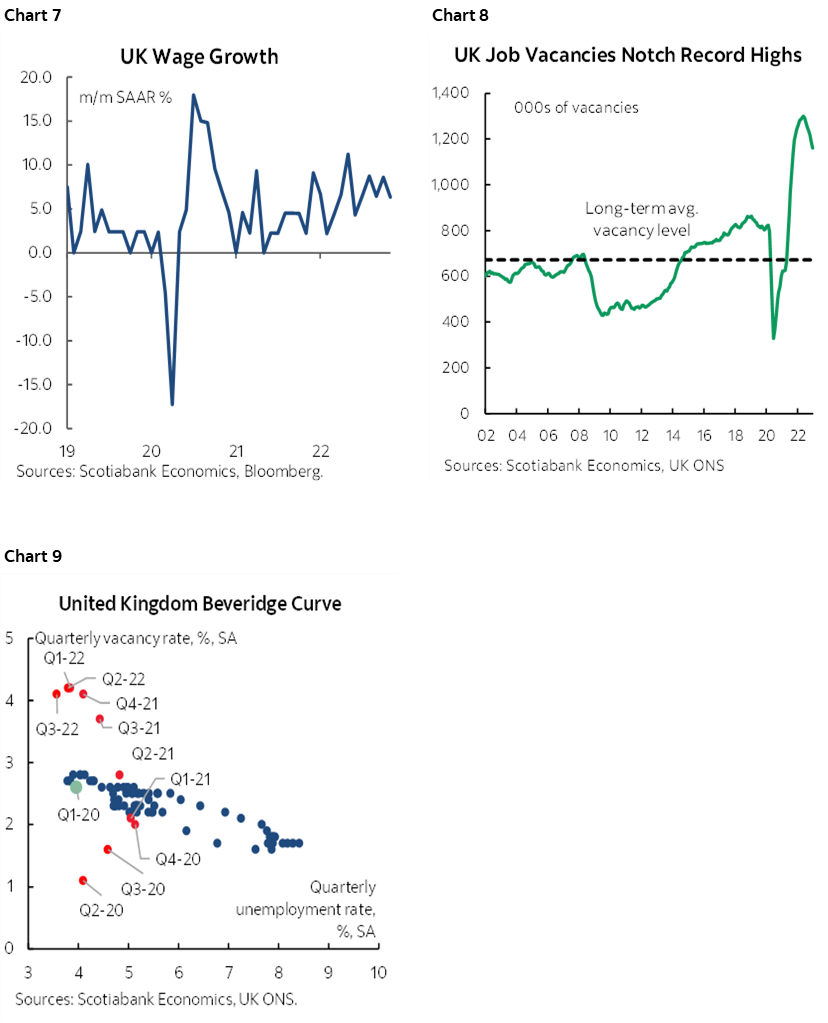

UK job market conditions face updates for January (payrolls) and December (wages and total employment) on Tuesday followed by CPI the next day. Total employment has been moving sideways over recent months and remains short of pre-pandemic levels while growth in average weekly earnings has been accelerating (chart 7). Job vacancies remain very high (chart 8) and have a long way to move lower before there is a material rise in the unemployment rate given the inverse connections between the two measures (chart 9). Softer energy prices should drag down headline CPI that is expected to drop by around -0.4% m/m but the greater focus will be upon whether core CPI begins easing off evidence that the year-over-year rate is plateauing around 6 ¼%. The week ends with retail sales for January that are expected to dip again.

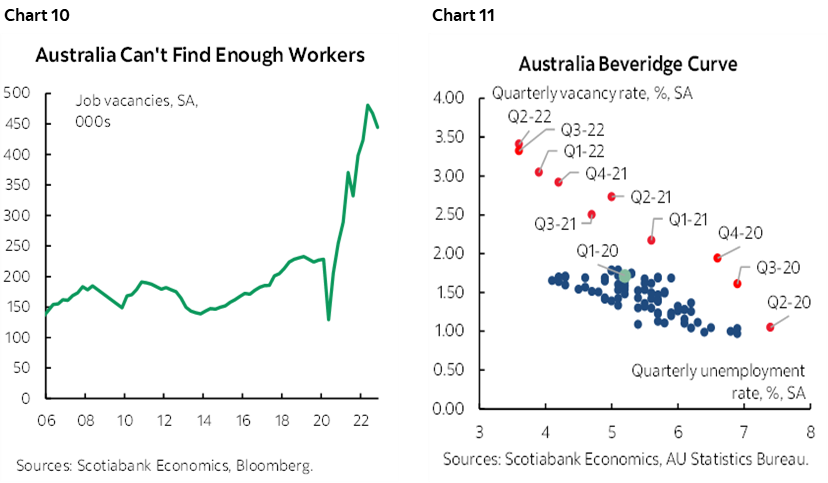

Australia updates job market conditions during January on Wednesday. Consensus has pencilled in a rebound from the drop of 15k in December that was all due to lower part-time employment. Like the UK, job vacancies remain very high relative to unemployment (chart 10, 11).

Also keep an eye on Japanese GDP growth for Q4 (Tuesday) that is expected to return to the plus side with non-annualized growth of 0.5% q/q that would end the year with two ups and two downs.

India’s inflation rate is expected to rise back over 6% y/y on Monday when January’s reading arrives and that would reverse a declining pattern since September.

Finally, for RBNZ watchers, Monday’s Q1 estimate of 2-year ahead inflation expectations may face further upside risk along a rising trend as markets price another full percentage point of rate hikes ahead and then some.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.