Next Week's Risk Dashboard

- Global central banks to clear the decks before the holidays

- Patience now could offer more handsome rewards later

- FOMC probably won’t deliver on market expectations

- How low could US core CPI go?

- BoC’s Macklem will probably say it’s much too soon

- ECB—Uncle! Now what?

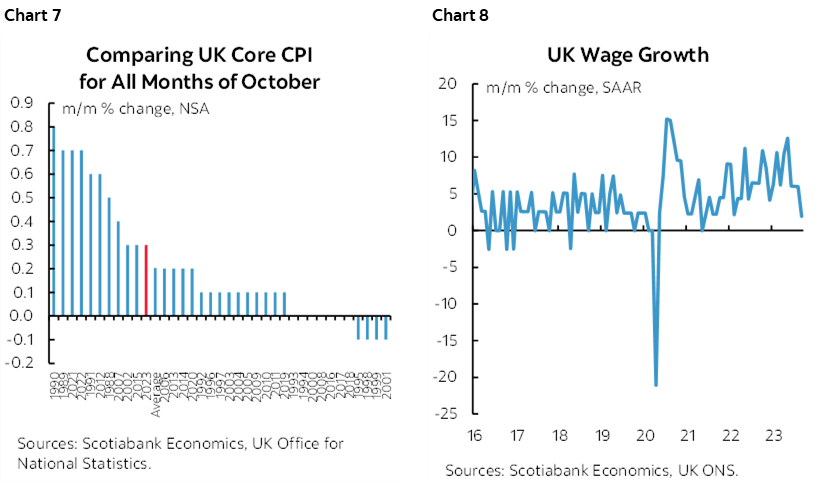

- The BoE’s exercise in futility

- The PBOC may defer to other policy levers

- SNB likely to hold

- Banxico only partly waiting for the Fed

- Peru’s central bank expected to cut again

- Norges Bank’s decision could hinge upon CPI

- Brazil’s central bank expected to continue -50bps pace

- Philippines’ central bank has a cagey definition of hawkish

- CBCT likely to stay on hold

- Russian central bank—it serves you right!

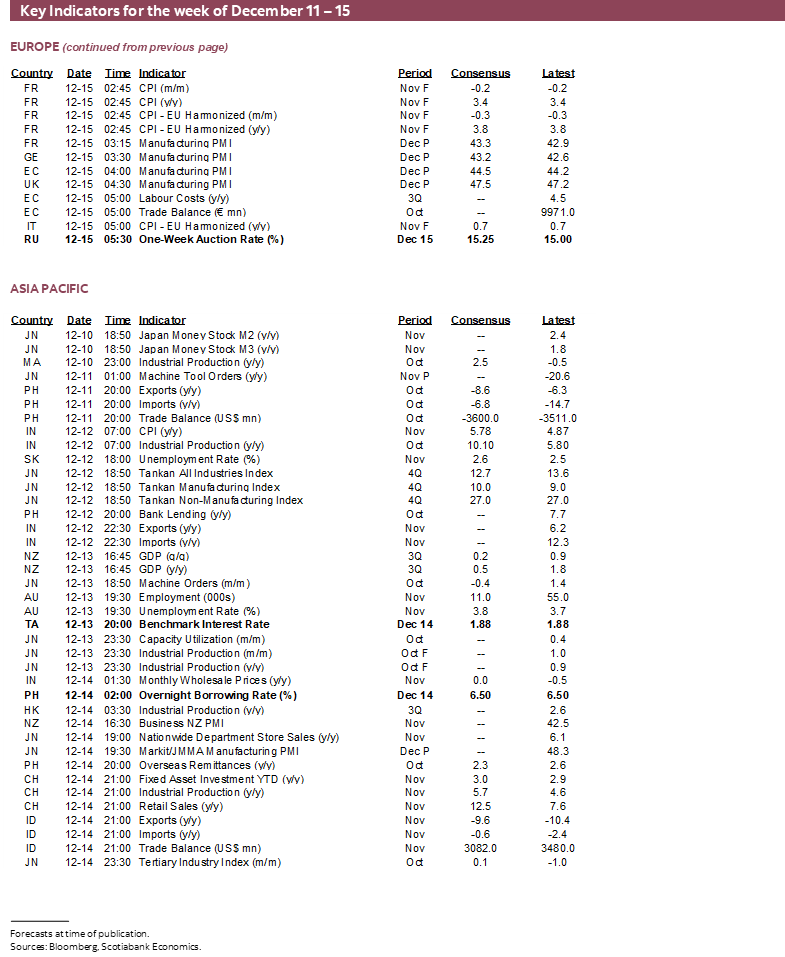

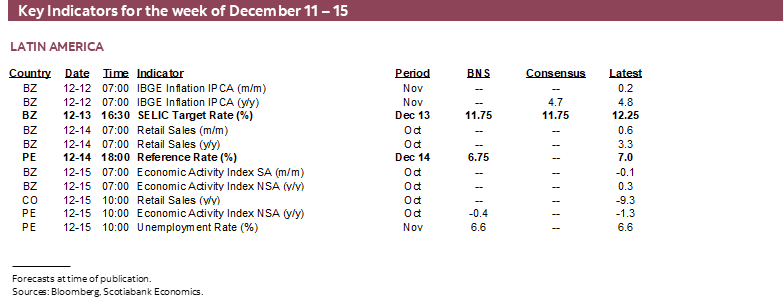

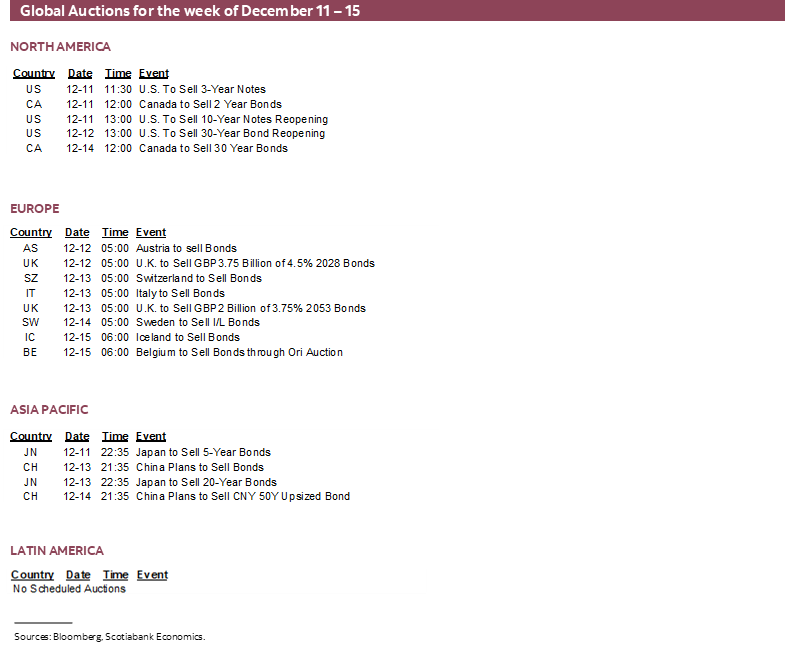

- Global macro indicators

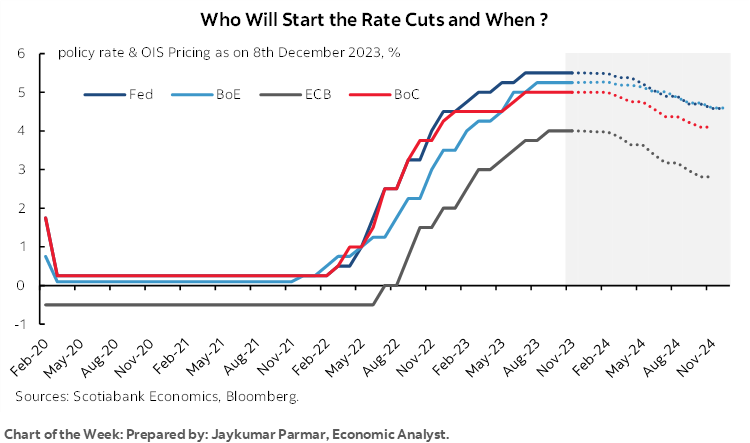

Chart of the Week

This will be a key week for global central banks. Over a dozen central banks will weigh in at a time when markets are frankly applying little differentiation across timing the beginning of their easing cycles. As this week’s cover chart demonstrates, the majors are expected to ease practically in unison despite material differences in their individual circumstances. This coming week could emphasize such differences.

Before delving into expectations, I’ll briefly remind readers of my bias. I’d love to see rate cuts. When the time is right and when we have enough conviction to deliver them in a meaningful and sustained way. Patience will pay if central banks hold out until they have higher conviction that inflation is down for the count and terminal rates can approach a more neutral setting with meaningful reductions. Premature easing could risk reigniting many of the imbalances that got us here in the first place. Acting with haste could easily make waste later by thwarting chances at more meaningful rate cuts.

FEDERAL RESERVE—THE DOTS WON’T MEET THE MARKET

A full set of FOMC communications is due on Wednesday afternoon at the end of the two-day meeting. The statement and Summary of Economic Projections including an updated ‘dot plot’ will arrive at 2pmET and be followed by Chair Powell’s customary press conference thirty minutes later.

No policy rate change is expected as the Committee extends the pause that has been in place since its last hike on July 26th. No changes to balance sheet plans are expected, including a continuation of the US$60B/month and $35B/month roll-off targets for maturing holdings of Treasuries and MBS respectively. The Fed remains a long way from the 10–12% of nominal GDP target for reserves.

Key will be four considerations as follows.

1. Statement

Key may be whether they soften reference to “tighter financial conditions” or even the unlikely scenario of striking it out. When they inserted this reference in the November 1st statement, they basically called the peak for US 10s. Since that time, the yield on the 10-year Treasury—a key driver of the 30-year mortgage rate—has fallen by about 70bps and back to levels seen in early September that were still higher than summertime yields. The two-year yield has fallen by about 50bps from the peak and markets have pivoted toward pricing a decent shot at a cut as soon as the March FOMC meeting. Watch for continued reference to strong growth and strong job gains. They might soften references to ‘solid’ growth in GDP tracking for Q4 after the 5% pace in Q3.

2. Policy rate projections

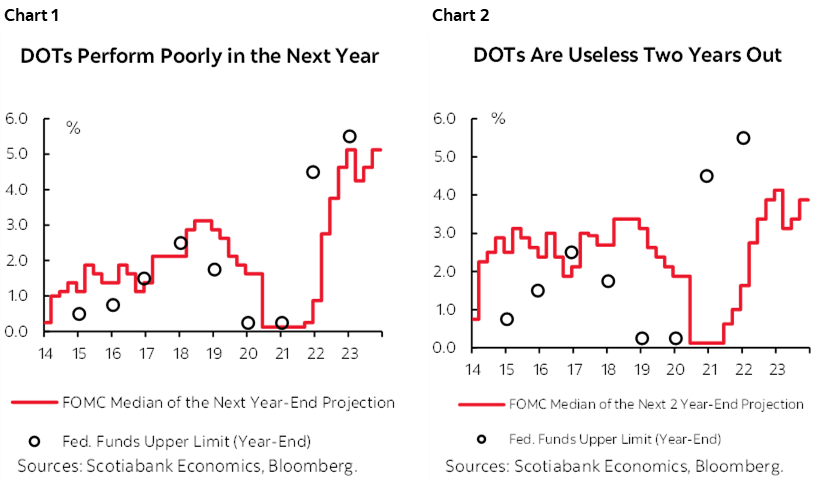

The dot plot of FOMC forecasts for the policy rate had an extra 25bps rate hike built in by this meeting and 50bps of cuts next year. A hike is very unlikely at this meeting especially given Powell’s high reticence to surprise markets and so the level of the fed funds target rate is likely to be revised lower to show unchanged at 5½% this year. Key is whether they leave it at that and retain only 50bps of cuts next year toward a lower year-end level of 4.875%, or whether they add to the median participant’s expected easing. I think they might tack on an extra 25bps of cuts down to 4.625% with a significant chance they merely retain 50bps. Either way, with markets pricing about 100–125bps of cuts by end the of next year, I wouldn’t expect anything other than for the Committee to disappoint. The residual question is then whether markets react to the dots as much as they did in September, or fade them given the poor track record (charts 1, 2).

3. Macroeconomic projections

GDP will have to be revised higher on the customary Q4/Q4 basis for this year given tracking that it is at least 50bps higher than the 2.1% pace recorded in the prior projection. That could come at the expense of next year’s 1.5% projection although it would be a hawkish signal if they retained it instead of pulling growth forward. Expect a mild downward revision to the unemployment rate this year and perhaps next year. Headline and core PCE inflation will be revised lower this year and perhaps next year as well. This could offer justification to adding an extra cut to the dot plot for next year.

4. Press conference

I didn’t say that, don’t quote me, it wasn’t me. Chair Powell is likely to douse the dots and the projections as he has tended to do in the past. Instead, Powell is likely to offer a replay of his comments during his fireside chat on December 1st just before going into the FOMC’s communications blackout. He will likely repeat that it is “premature to conclude with confidence” that a rate peak has been achieved and when policy may begin to ease. Expect emphasis upon history’s cautions in this regard. He will likely try to convince markets they are open to tightening again if necessary, but without success. One way in which he could do so is by referencing strong GDP growth and ongoing resilience in the job market including a recent pick up in wage growth. He may confront the easing of financial conditions. His time might be better spent counselling markets on the criteria for commencing policy easing, but I have a feeling we’ll hear him say they’re not yet at the point of broaching such a dialogue any time soon.

BoC’S MACKLEM—TOO SOON

Bank of Canada Governor Macklem delivers the Governor’s traditional pre-holiday speech on Friday in Toronto. He will hold a press conference afterward and so anything goes. As yet we do not have a speech title or topic, though I would expect a broadly similar tone to what we just heard from Deputy Governor Gravelle.

Recall the key takeaways from Gravelle’s speech (recapped here). Gravelle observed that “it’s pretty clear that we are not on a sustainable path yet” in reference to inflation being on a path toward durably landing on their 2% target when the evidence is at a highly nascent stage, and that “Once we have more confidence we are on a sustainable path to 2% then we might be in a position to even start thinking about cutting rates but we’re not even there.” The combined outcome suggests they wish to see a significant period soft underlying inflation readings, to then have confidence they will be sustained, and to then begin discussing rate cuts.

I would expect the Governor to say that’s basically impossible as soon as the March and April meetings when markets are pricing cuts, barring big unforeseen developments. He could very well lean the other way by noting the significant easing of financial conditions ahead of key developments over coming months such as a round of government budgets and the coming mortgage pre-approvals season into the Spring housing market.

ECB—UNCLE! NOW WHAT’S NEXT?

The hawks may have cried Uncle, but that doesn’t mean that cuts are ahead any time soon. That’s likely to be the overall takeaway from the European Central Bank’s communications on Thursday when they are expected to hold all policy rates unchanged.

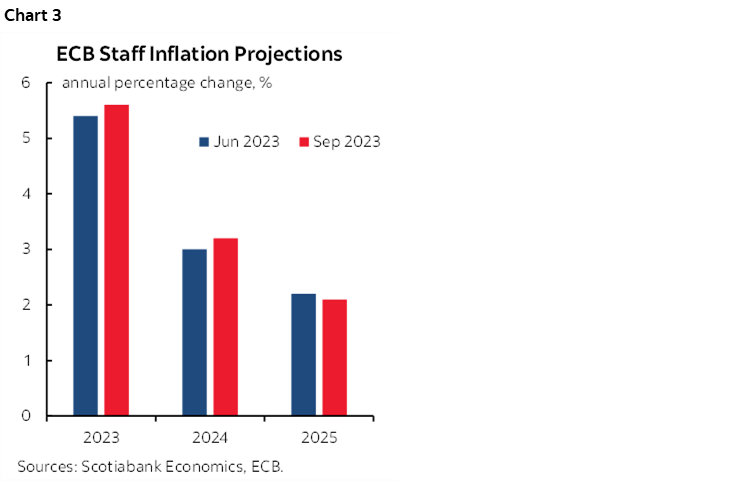

That doesn’t necessarily mean it will be an uneventful meeting. Updated staff projections are expected to revise GDP and inflation forecasts lower, but key will be how large the forecast revisions may be in relation to market pricing for a first rate cut as soon as the March 7th meeting and for aggressive easing over the duration of the year. High for long would be informed by retaining a forecast for inflation not to hit 2% until 2025. The prior two rounds of inflation projections are shown in chart 3.

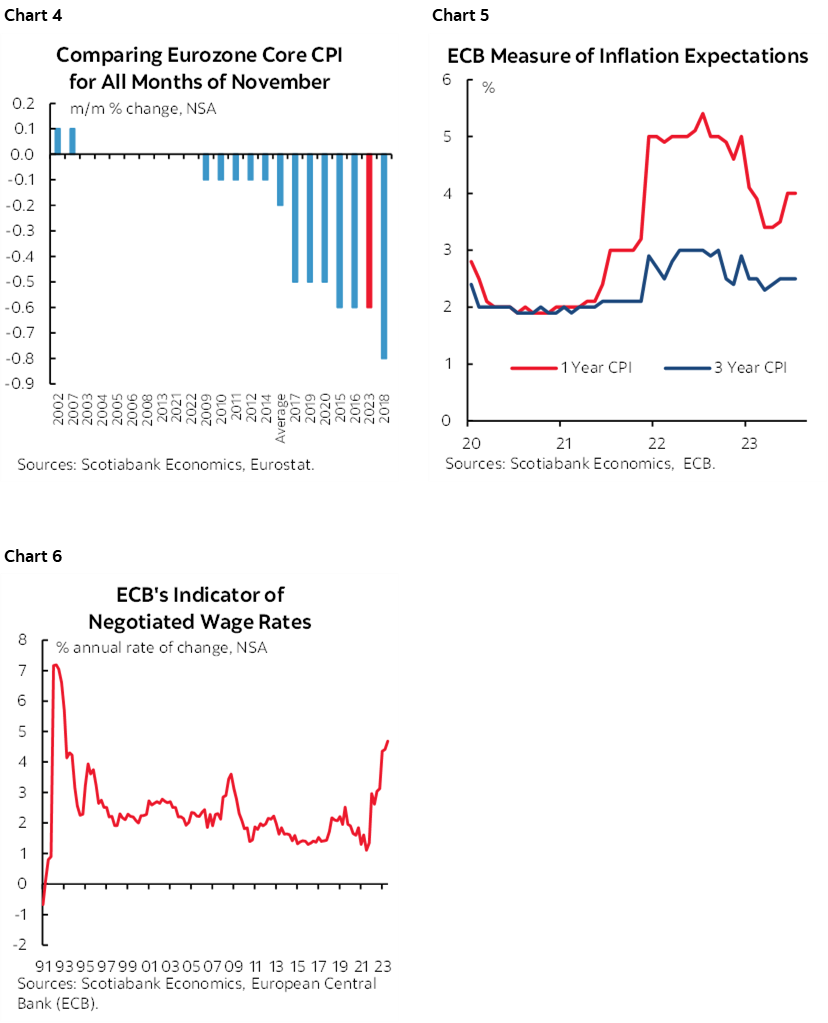

While recent inflation has been trending softer (chart 4), it still seems extraordinarily premature to expect the ECB to begin discussion on when to ease. Inflation expectations are still well above target (chart 5) and wages continue to rise at a relatively rapid pace (chart 6). Core inflation has pulled back, but at 3.6% y/y it remains unacceptably high while President Lagarde will probably downplay recently soft inflation by requiring much further evidence.

We might hear more about bringing forward the end to reinvestments of maturing bond holdings under the Pandemic Emergency Purchase Program. They long ago stopped reinvesting Asset Purchase Program holdings, but the pandemic program’s guidance has stood at reinvesting until around the end of next year. That was until Lagarde loosely remarked that bringing forward the end of reinvestments “is a matter which will come probably for discussion and consideration within the Governing Council in the not too distant future and we will re-examine possibly this proposal.” No action is likely this week and we might wind up hearing that discussion has been deferred to a subsequent meeting, but a surprise could be as impactful or more so than forecast guidance.

BANK OF ENGLAND—AN EXERCISE IN FUTILITY?

The Bank of England is likely to leave Bank Rate unchanged at 5¼% on Thursday. This one will only offer a statement and meeting minutes, sans forecasts or press conference which limits the ability to say too much.

Expect a few of the MPC members to continue to vote for an additional hike but to be outnumbered again. The tone of the minutes in particular may attempt to lean against pricing for about 75bps of cuts next year. Governor Bailey recently stated that the easy part in getting inflation down was done by energy prices but “the rest of it has to be done by policy and monetary policy. The second half, from there to two, is hard work and obviously we don’t want to see any more damage” in reference to achieving the 2% inflation target.

Bailey went on to state “that’s why I have pushed back of late against assumptions that we’re talking about cutting interest rates or we will be cutting interest in anything like the foreseeable future because it’s too soon to have that discussion.”

Markets didn’t so much listen to him and so it’s unclear they will be more inclined to do so this time around. Recent inflation has ebbed, although November data will arrive the week after the decision (chart 7). Wage growth is also ebbing in the UK (chart 8).

PBoC—A PROBABLE HOLD WITH RELIANCE UPON OTHER TOOLS

China’s central bank is expected to leave its 1-year Medium-Term Lending Facility Rate unchanged at 2.5% on Thursday evening (ET). The risk is clearly slanted toward a cut, but two cuts in June and August have been followed by a holding pattern over the past three meetings.

The policy rate may be at equilibrium for the time being, but other stimulus tools are being monitored. There may be an easing bias given yuan appreciation since early November as market expectations for easing by the Federal Reserve have intensified even if they have gotten carried away.

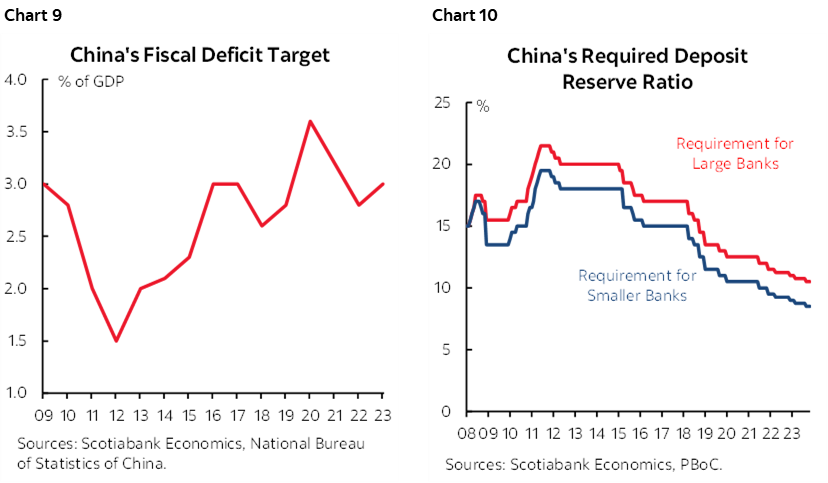

A recent Politburo meeting chaired by President Xi Jinping indicated a bias toward increasing fiscal stimulus. That could indicate a bias toward raising the targeted deficit ratio from last year’s level (chart 9) as indicated by local analysts, but a clear challenge to doing so could be Moody’s move to put the country’s credit rating on negative outlook. Perhaps rumours of another potential cut to the required reserve ratio may have greater merit (chart 10).

SWISS NATIONAL BANK—ECB LAGGARD?

A hold at a 1.75% policy rate is widely anticipated on Thursday. A tightening bias remains in place and the Swiss franc has appreciated against the euro since early October on bets that the ECB is more likely to begin easing sooner than the SNB. This view may become increasingly challenged as inflation continues to wane. November’s inflation rate fell to 1.6% y/y with core at 1.4%. The SNB only meets four times a year and so—barring exigent circumstances—it’s under less pressure to have to talk so much by comparison to other central banks!

BANXICO—SOONER OR LATER

Banco de México is unanimously expected to hold its overnight rate unchanged at 11¼% on Thursday. Its last hike was back in March that ended 725bps of hikes. Mexico’s central bank is heavily influenced—but not straightjacketed—by what the Federal Reserve does and so, to a certain extent, what it decides to do into 2024 hinges in no small part upon whether markets are overly exuberant toward the prospect of Fed rate cuts as soon as Q1.

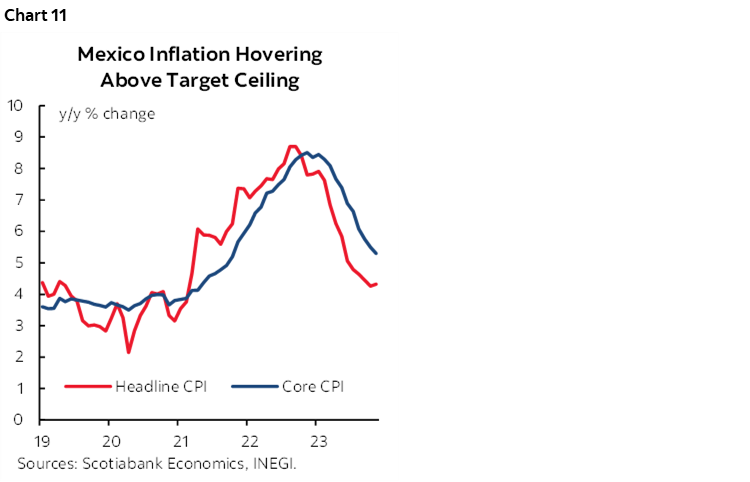

In the meantime, the peso has appreciated by about 5% to the USD since about late October and inflation has continued to ebb. Core CPI slipped to 5.3% y/y in November, or over 300bps lower than the peak in late 2022. As inflation approaches Banxico’s 2% +/-1% target (chart 11), the prospect of easing lies in store for 2024. After Banxico changed its forward guidance for the policy rate to remain unchanged for an “extended period” to “for some time” at its last meeting, the hint is a willingness to possibly move sooner than later.

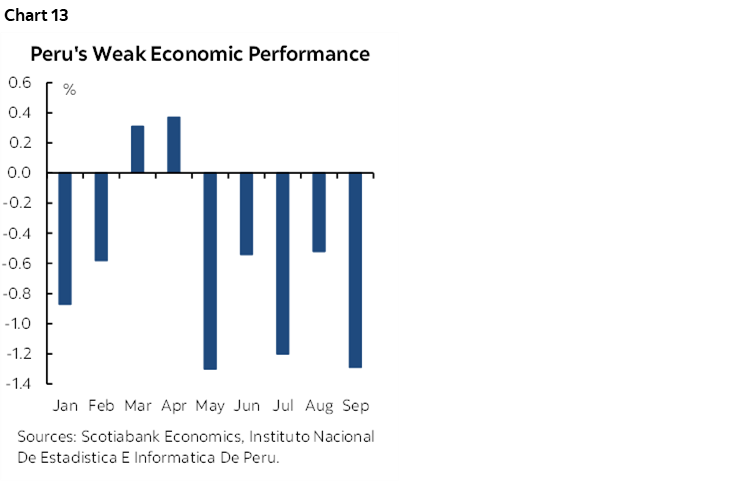

BANCO CENTRAL DE RESERVA DEL PERU—RAPID PROGRESS

Peru’s central bank is expected to cut its reference rate by another 25bps to 6 ¾% on Thursday evening (ET).

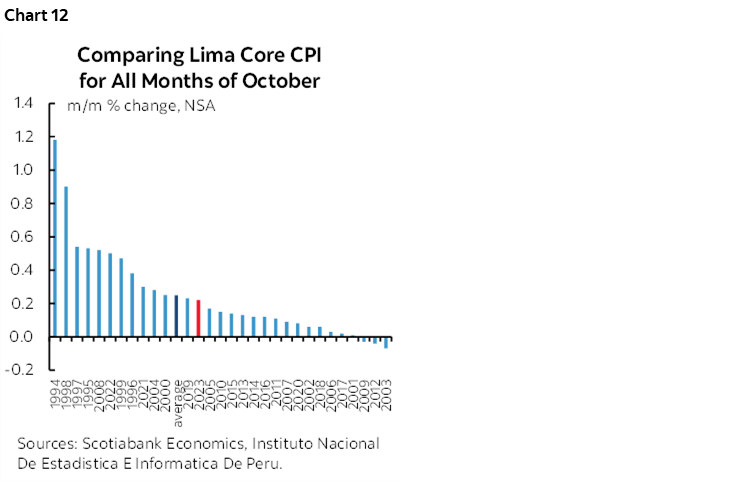

Inflation has been falling from a peak of 8.81% last year to 3.6% y/y in the latest reading for November and with the core rate at 3.1%. Core inflation has been rapidly decelerating and not just because of year-ago base effects. Core pressures are soft at the margin as well (chart 12).

The BCRP targets 2% +/-1% inflation and this is readily within reach next year. The 750bps run up in the reference rate from 2021H2 to early this year has a long way to continue dropping from its present 7% rate. That’s especially as GDP continues to weaken (chart 13).

NORGES BANK—NOVEMBER CPI COULD BE DECISIVE

Most expect Norway’s central bank to remain on hold at 4.25% with a notable minority expecting a 25bps hike. Normally this central bank has a tendency to tee up future moves in advance with explicit forward rate guidance. That has recently softened, however, which explains the ambiguity within consensus.

In its last statement on November 2nd, Norges said “There will likely be a need to maintain a tight monetary policy stance for some time ahead. Whether additional rate hikes will be needed depends on economic developments.”

They went on to flag more rapid improvement in inflation than they had expected in their September Monetary Policy Report. This meeting will offer a fresh MPR and updated forecasts to help further inform the policy bias.

It’s worth noting that since they issued their last statement, underlying inflation surprised higher than expected with a rise of 0.6% m/m and 6% y/y (5.7% prior) in October. November’s update on Monday could be important to the decision just three days later.

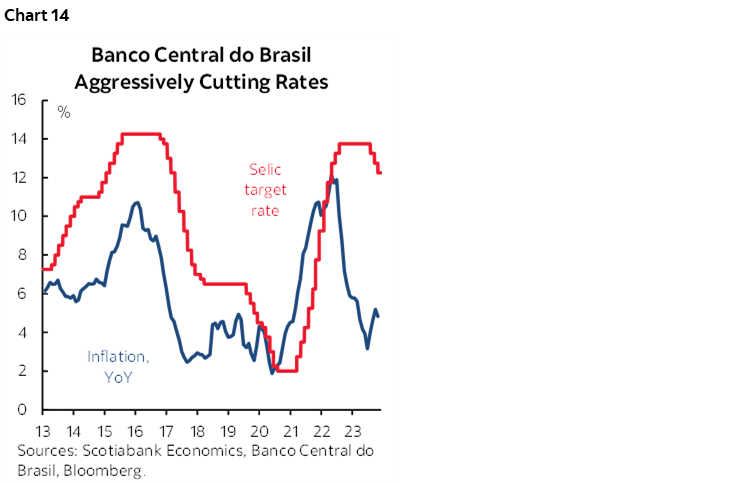

BANCO CENTRAL DO BRASIL—A LONG WAY TO GO YET

Brazil’s central bank is widely expected to cut its key Selic rate by another 50bps on Wednesday. Why? Because they said so!

Governor Roberto Campos Neto recently said “We understand that the 50 basis point pace is adequate…and appropriate for the coming meetings.” Note the plural reference which likely means 50bps reductions at each of the next two meetings in Q1 and then we’ll see. The 50bps cut pace began in August and has taken the policy rate down by 150bps so far. Given how far it climbed, there could be a long string of substantial easing moves ahead of us in 2024 with consensus expecting about 300bps of easing from here until the end of next year.

Supporting such easing is the speed with which inflation has been coming down in Brazil (chart 14). The central bank will target 3% +/-1.5% inflation in 2024 and the present 4.8% y/y inflation rate is expected to move inside this band by around mid-year.

BANGKO SENTRAL NG PILIPINAS—DEFINE HAWKISH

The central bank of the Philippines is widely expected to stay on hold at an overnight borrowing rate of 6.5% on Thursday. A small minority believe that it could hike again after tweaking its stance with a surprise off-cycle 25bps hike in October before holding flat in November. Guidance has pointed toward willingness to take further action but not decisively so. Governor Remolona recently said “Hawkish means we could either pause or we could hike on December 14th.” Alrighty then!

CENTRAL BANK OF THE REPUBLIC OF CHINA (TAIWAN)

CBCT is expected to leave its benchmark rate unchanged at 1.875% on Thursday. They’re a precise bunch of folks. They raised the policy rate by 12.5bps back in March and have been on hold since then. Inflation has pulled back to 2.9% y/y in November with core falling to 2.4% —its lowest rate since early 2022.

CENTRAL BANK OF THE RUSSIAN FEDERATION—IT SERVES YOU RIGHT

Consensus is divided between a hold at a key rate level of 15% versus a further hike of as much as 100bps. The central bank hiked by an eye-watering 200bps in October, or double consensus which might explain the wild uncertainty into this one. The policy rate has been increased by 750bps since July in order to counter inflationary pressures. Inflation is running at about 7 ½% y/y with core up 6.4% y/y. Seems to me that the best way to impoverish your own people outside of the ruling elite is to start an illegal war with further pain ahead for Russia’s economy excluding military spending.

US INFLATION—HOW LOW WILL IT GO INTO THE FED?

The latest batch of US inflation numbers lands right before the start of the two day FOMC meeting on Tuesday morning. CPI for the month of November is expected to be weak, but there is considerable uncertainty about how low the core measure of inflation may go.

I’ve gone with an estimated headline CPI drop of -0.1% m/m SA and a deceleration in the year-over-year rate to 3.1% from 3.2% the prior month. Core CPI is estimated to be soft at 0.1% m/m SA.

Headline CPI will be soft because of a significant decline in gasoline prices. Used vehicle prices also slipped according to industry guidance, but new vehicle prices were little changed. Shelter, including owners’ equivalent rent and rent of primary residence, will probably remain hot.

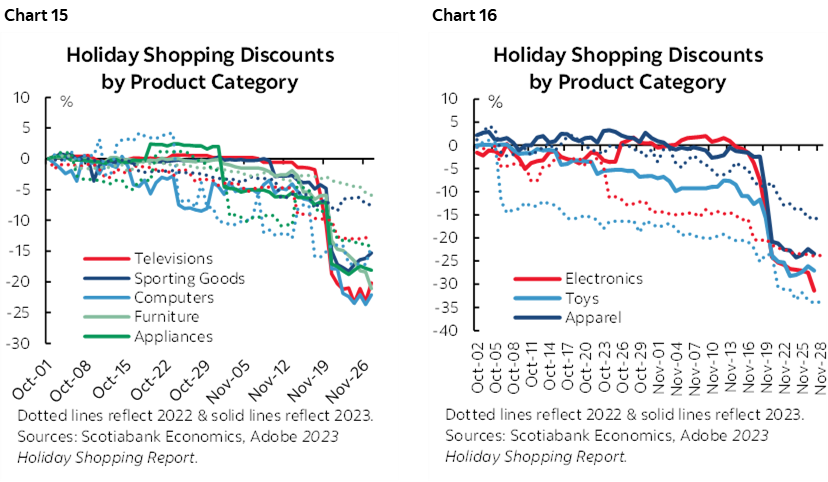

Where additional downside pressure may come from could be in terms of evidence of deeper price discounting into the holiday shopping season across a range of goods. Charts 15 and 16 show the pattern of discounting this year versus last year by way of comparison. If core retail sales during November prove to be strong next week, then sales will have required deeper discounts.

I need to caution that my estimates, done on a best efforts basis, are materially below consensus. Most economists are in the 0.2–0.3% range for core CPI. That said, it wouldn’t take much tweaking of the numbers to get an even lower core inflation reading than I went with. By added way of comparison, the Cleveland Fed’s ‘nowcast’ for core CPI estimates a rise of 0.3% m/m SA for the softest gain since late 2021. That measure, however, has persistently overestimated core CPI inflation throughout the past year.

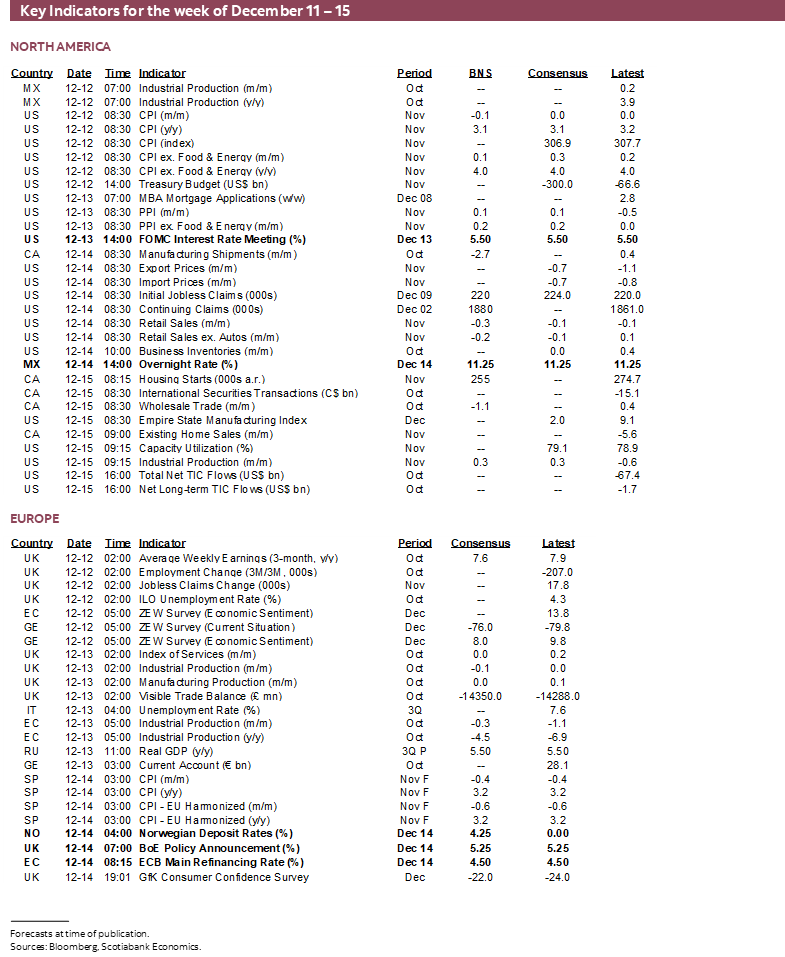

Global calendar-based data risk will also be elevated over the coming week. I’ll write more about the readings through daily notes. For now, some of the key highlights will include US retail sales (Thursday), UK job markets (Tuesday), global purchasing managers’ indices (Thursday/Friday), Australian jobs (Wednesday), and China macro data for November (Thursday).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.