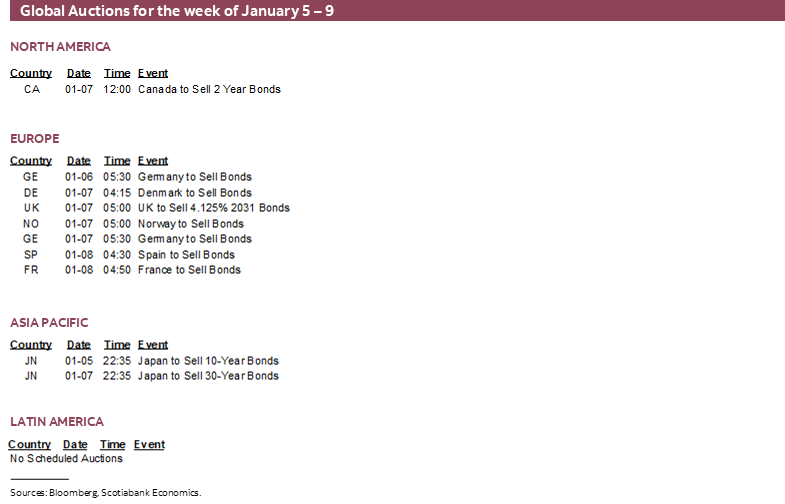

Next Week's Risk Dashboard

- Nonfarm payrolls will be overstated no matter what…

- …but could inform the Fed’s next move

- Canadian jobs still on fire?

- A massive global inflation data dump

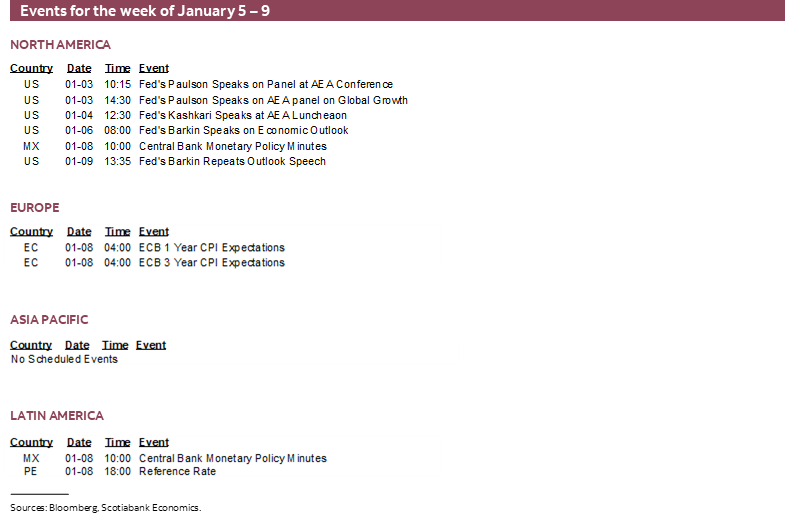

- BCRP likely to hold for a fourth time

- Global macro: US and Germany in focus

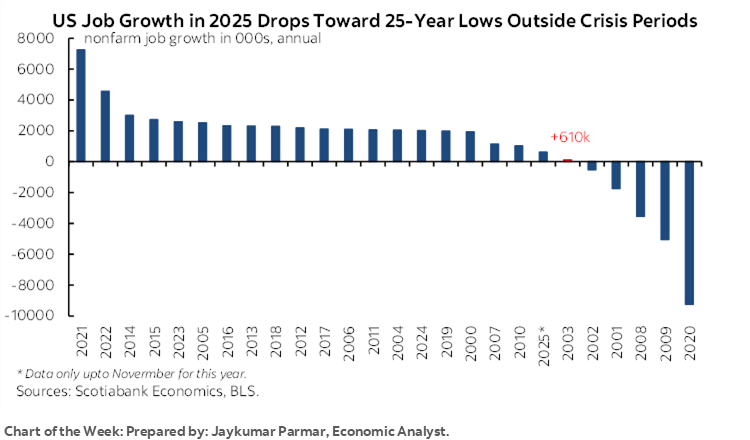

Chart of the Week

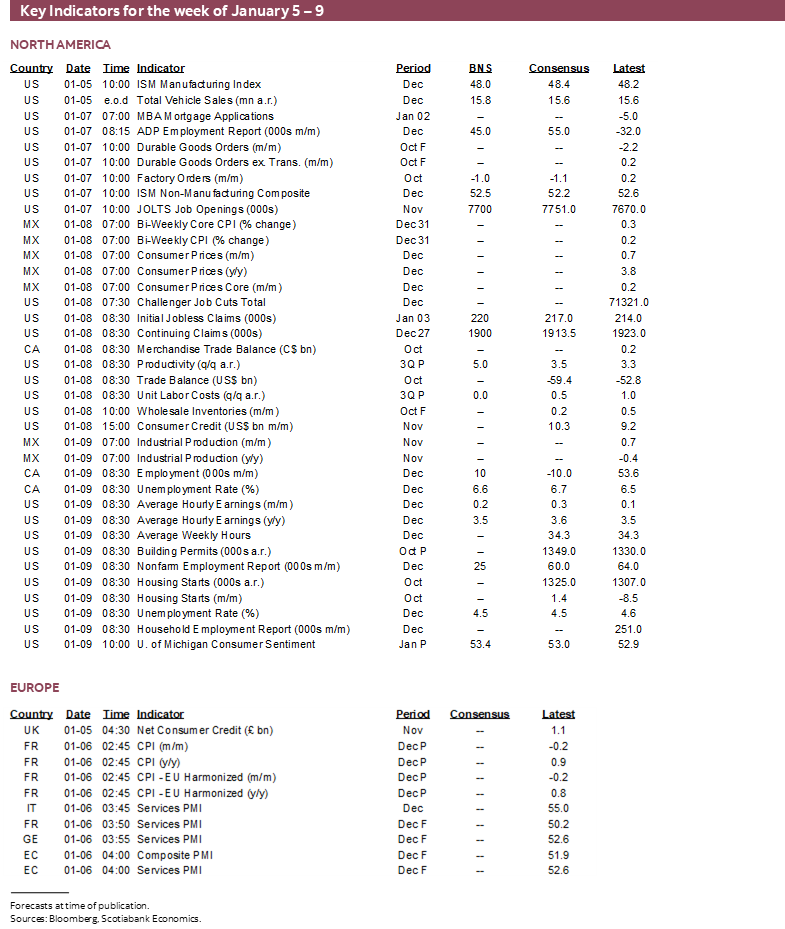

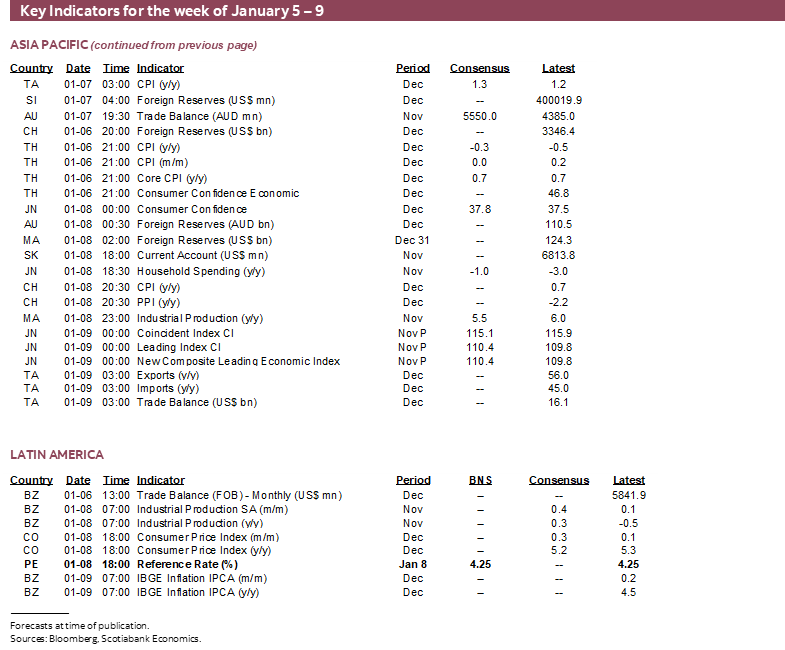

This will be a lighter year-end Global Week Ahead partly because of relatively few—but key—expected developments over the first full week of 2026 and frankly because many readers are about to pop champagne corks to bring in the new year. The main highlights will be US payrolls, Canadian jobs, a huge round of global inflation reports, and one solitary central bank decision out of Peru.

NONFARM—OVERSTATED, WHATEVER HAPPENS

Friday’s nonfarm payrolls will further inform the state of the US labour market on the path to the next policy decision by the Federal Reserve on January 28th.

A small gain of 25k with a slight decline in the unemployment rate to 4.5% is expected. Consensus is somewhat higher on the magnitude of the gain. Nobody should have much confidence in their estimates for this reading given low data quality but data collection has returned to its pre-shutdown state which wasn’t great to begin with.

There are very few advance labour market readings available so far but we’ll get more next week ahead of payrolls. Consumer confidence jobs plentiful dipped. ‘Indeed’ job postings surged in December and late November over earlier in November which points to a rise in JOLTS job openings. ADP private payrolls appear to have been up by about 50k but track nonfarm poorly. Layoff trackers pointed to fewer in December. Initial jobless claims have been reasonably well behaved while continuing claims have recently trended lower and point to a correlated dip in the unemployment rate. Alt-data like Revelio and Homebase are not yet available for December.

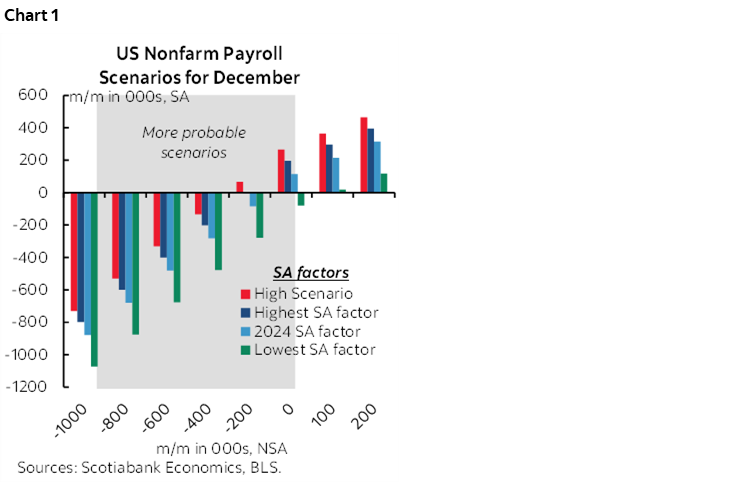

December is normally a down-month for seasonally unadjusted payrolls. What happens next depends upon how the BLS manages seasonal adjustments. In each of the three prior reports they have gone with historical all-time highs for monthly seasonal adjustment factors when comparing like months across time. If they do the same thing this time, then that could add some upside. Chart 1 shows scenarios for payrolls across differing seasonal adjustment factors and seasonally unadjusted readings.

And yet the arguments for how nonfarm payrolls are much weaker under the hood are likely to still apply. They were explained in my prior recap for payrolls (here). Take out healthcare hiring and private payrolls have been down or flat in six of the past seven months and healthcare hiring is vulnerable as subsidies expire. Adjust for benchmarking revisions that have yet to be incorporated and payroll levels are much lower by just under a million up to last March and by more since then. Adjust for fishy seasonal adjustment factors that went high in each of the three months since Trump started attacking the BLS after firing its Commissioner. We’re getting low quality jobs data out of the US for these reasons plus others like falling survey response rates.

At some point—probably not yet—we’ll need to keep an eye on weather-adjusted payrolls given the widespread earlier snowstorms and adverse weather than prior years. The San Fran Fed’s weather-adjusted payrolls could be instructive.

The breakeven rate of payroll gains has shifted sharply lower amid draconian immigration policies, but a fact is a fact—the sharply weakening trend in job growth is getting too close to past recessionary signals for comfort as also argued in the aforementioned linked note.

CANADIAN JOBS—I ASK MYSELF, DO I FEEL LUCKY?

Canada also updates jobs and related measures for the month of December on Friday at the exact same time as nonfarm payrolls (8:30amET).

And whoop-de-doo. The BoC is clearly on an extended pause as it evaluates a material amount of data and new developments after cutting down to a real policy rate that is about zero or even negative, depending on the measure of inflation or inflation expectations that is used. After a string of massive employment gains, one report won’t sway them which leaves us with bi-directional trading noise but probably no direct policy implications.

A small gain of 10k with a slight uptick in the unemployment rate to 6.6% could emerge.

Job growth has been running at a torrid pace over the past three months with gains of over 50k m/m in each of them. For two of those reports we’ve been hearing the next one must surely be down by a lot. Not. Yet there is the same hubris across consensus estimates now; maybe they’ll be right this time. Maybe not.

Historically, however, a trifecta of monthly gains over 50k has always been followed by….wait for it….another gain! Mind you, out of eight such occasions in the history of the Labour Force Survey, only two have been outside of the pandemic period.

Another reason for another possible gain is the LFS methodology’s practice of rotating out new household responses one month at a time over a rolling six-month period. The first month’s respondents get dropped and new respondents are added for the latest month. This heavily weights the survey to the same panel of respondents which can at times drive persistence.

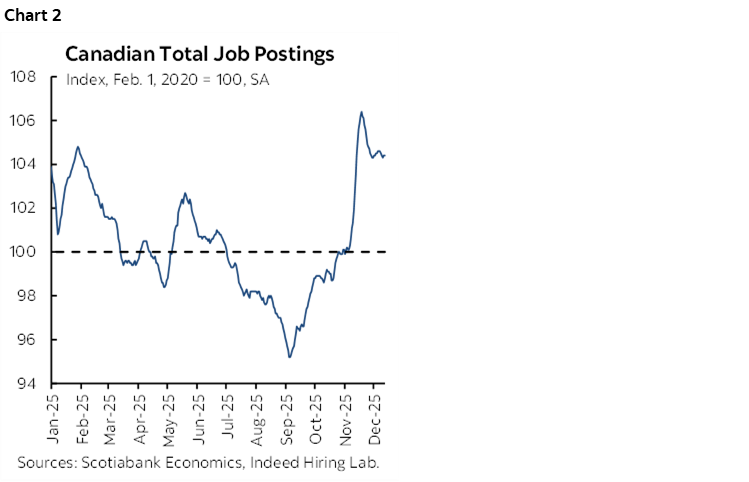

But it’s not all about technical excuses. Seasonally adjusted job postings have been on fire as marked by a steep upward trend since September that held in at high levels in December (chart 2).

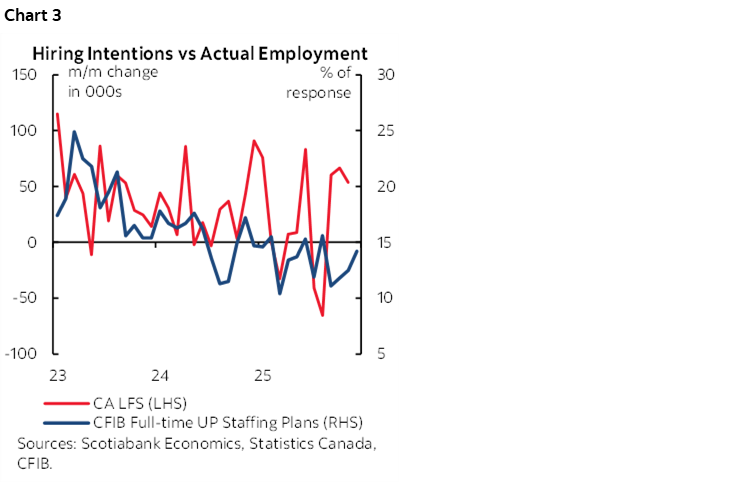

The BoC points to hiring intentions as a sign of weakness. As previously argued, it should not. Chart 3 shows no real usefulness to hiring intentions as a tracker of trend job growth. It’s about as useful as asking consumers what they expect for inflation without having the foggiest understanding of what inflation is truly about and how it’s measured.

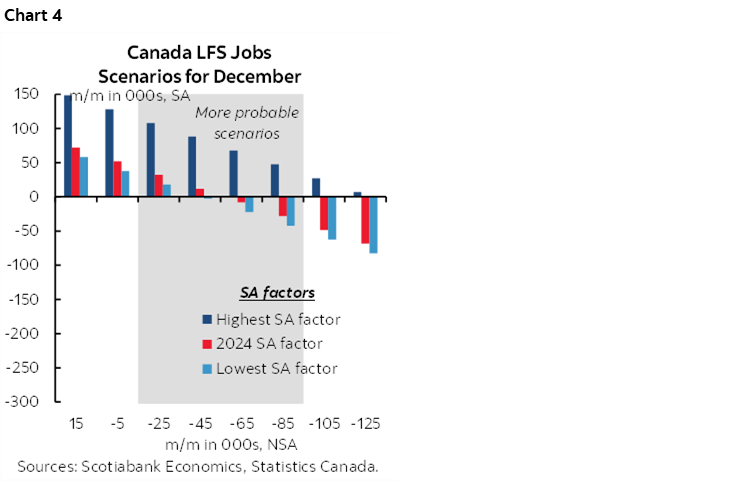

A further argument is that December is normally a seasonal down-month for employment with the sole exception being last December. Chart 4 shows scenarios around seasonally unadjusted changes married to varying seasonal adjustment factors. The pandemic and post-pandemic error has tended to employ lower than average SA factors for months of December which may tamp down the estimated change in jobs.

Also keep an eye on potential weather effects that may have to be considered for December and thereafter. Flooding in BC might be impactful. So may be the earlier and broader than normal flu season.

In any event, while it’s a noisy survey, one cannot credibly dismiss the three strong consecutive gains given the 95% confidence bands around their estimates would still have posted a positive trend and maybe even a much more positive one at that (chart 5).

GLOBAL INFLATION—INFLATION WATCHER’S PARADISE

Multiple major regions of the world economy will update inflation figures. In many cases it’s likely that no central bank policy decision hangs in the balance.

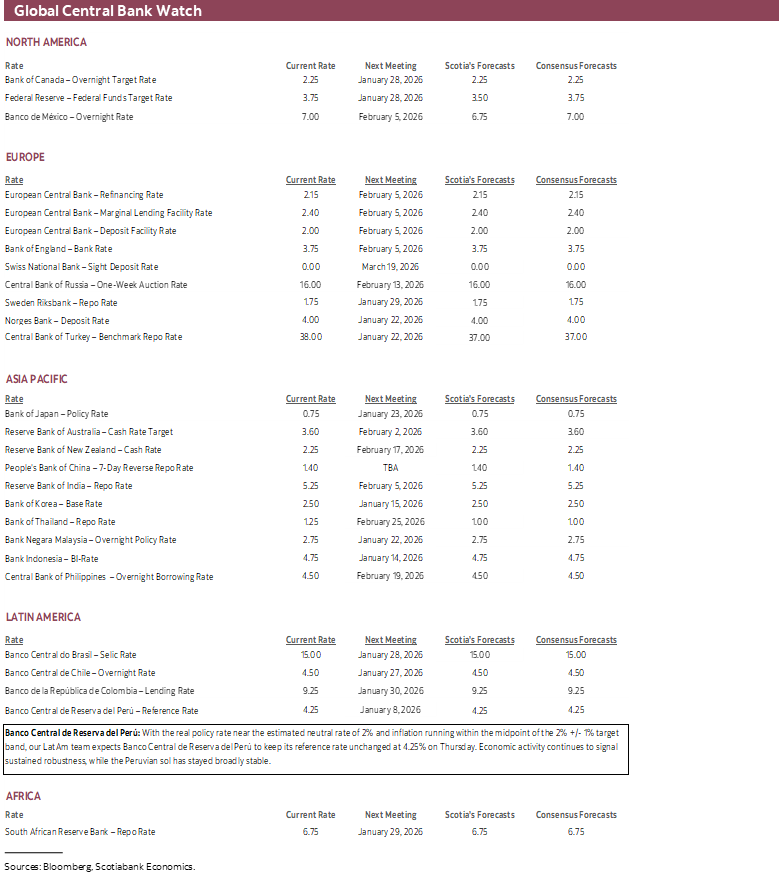

Chart 6 updates where inflation readings stand in relation to central bank targets around the world. In most cases, the war on inflation has yet to be won which may help to explain why many central banks have hit pause on their easing cycles—like the BoC, ECB, RBA—or are encountering dissenting voices from within—like the BoE, and Banxico.

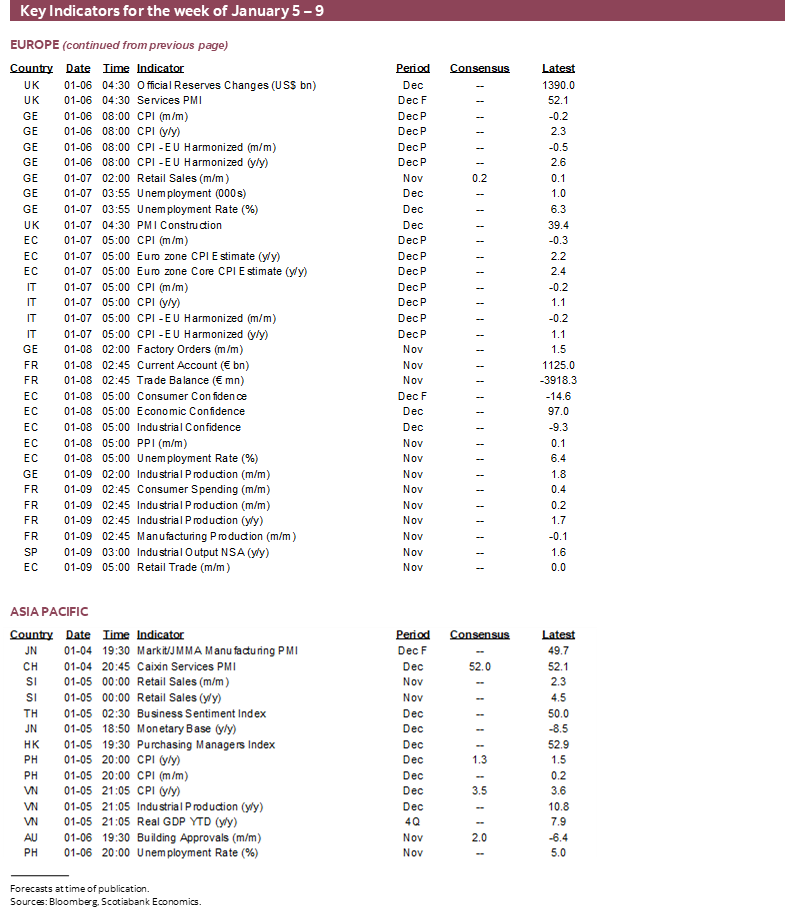

The Philippines (Monday night ET) kicks it off followed by France and Germany early Tuesday morning, then Australia Tuesday evening. Italy weighs in on Wednesday morning before the Eurozone tally and along with Taiwan. LatAm countries start releasing on Thursday (Mexico, Chile, Colombia). Chinese CPI and PPI (Thursday) will be followed by Brazil, Norway, Switzerland and Sweden on Friday.

BCRP—A FOURTH HOLD

Peru’s central bank perhaps didn’t take the hint when it noticed that no other central bank on the planet will be active this week. Or they march to the beat of their own drummer, in which case, good for them.

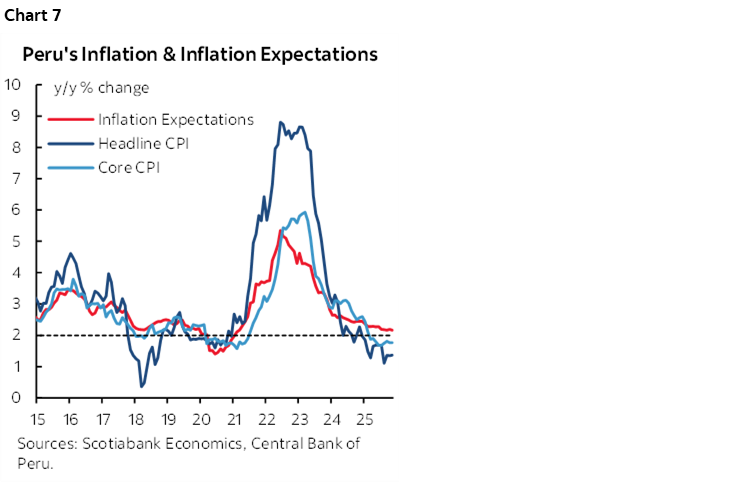

Thursday’s decision is expected to be another hold at a reference rate of 4.25% for a fourth straight meeting. CPI—due on New Year’s Day—is unlikely to alter the pattern of readings in the lower half of the 1-3% target range (chart 7). Key is that economic growth remains strong as indicated by the monthly activity index that continues to grow at around 3½% y/y.

GLOBAL MACRO—CATCHING UP

The rest of the docket will be rather light to start the new year. The US is the only major source of data releases after suspending many of them through the government shutdown and still catching up.

ISM-manufacturing could slip based in part on mostly weaker regional manufacturing surveys (Monday). ISM-services could be range-bound at moderate growth levels (Wednesday).

Monday’s vehicle sales during December are likely to be little changed around 15¾ million annualized and based on industry guidance.

Wednesday’s factory orders will likely shrink by considerably less than durable goods orders that were dragged lower by the transportations sector, as nondurable goods orders hold up better.

We have no guidance for trade figures during October (Thursday) particularly in the absence of the advance merchandise figures. Canada will also update trade figures for October on the same day and watch for revisions that could impact Q3 GDP that was initially estimated at 2.6% q/q SAAR with possibly incomplete trade data.

In addition to payrolls on Friday, housing starts for October and the University of Michigan’s consumer sentiment reading are also due before the Federal Reserve’s Q3 economy-wide balance sheet accounts.

Other than the US, the main other game in town will be Germany as it releases retail sales, unemployment, factory orders and industrial production over the back half of the week.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.