Season’s Greetings!

Best wishes for a safe and happy holiday season from all of us.

To our clients & readers, thank you for your continued interest in Scotiabank publications.

The next issue of The Global Week Ahead will be published on January 8, 2021.

Risk Dashboard for Dec 21 to Jan 1

• Brexit

• US stimulus/funding deals

• CBs: PBOC, BoT, Turkey

• China PMIs

• Light US, Canadian, Asian releases

Chart of the Week

I’ll start this two-week holiday season edition of the Global Week Ahead with heartfelt wishes that a highly atypical holiday season will bring to all of our families, friends, clients and colleagues the very best they could wish for and with particular emphasis upon your safety and health during these troubled times. I’m sure the coming year will carry its own challenges, but on balance there is reason to be confident that 2021 will offer greater hope than the terrible challenges this year has brought upon the world and particularly the least advantaged.

The near-term path to 2021 that is considered in what follows will be marked by greater uncertainty in terms of the inextricably intertwined politics, economics and markets, before my favourite chart for 2021 gains more traction into the new year (chart 1). At the point of publishing, major question marks continue to hang over Brexit and the prospects for US stimulus and for funding the US government to avoid an ill-timed interruption of services during a pandemic. The cautiously optimistic scenarios are still preferred outcomes on both counts and could contribute to a more construction start to 2021 for markets and the global economy, but we’ll know soon enough! It may at least be comforting that you won’t have to pour over many central bank statements and forecasts and there will be a relative dearth of economic indicators to consider, so sit back, perhaps have a glance at what follows, but spend much, much more of your time cherishing your families, loved ones and friends. Merry Christmas and Happy New Year!

BREXIT—STUCK ON FISH

All that seems to stand in the way of avoiding a so-called hard Brexit outcome in the new year is to strike a compromise on fish. Good luck is required. While seemingly trivial, the issue strikes to the heart of a nation’s sovereignty by way of determining access to waters it controls. It also carries greater weight in terms of politics than the rounding error share that fisheries represent in UK GDP.

Canadians, for one, can probably relate. Recall the dispute with France in the 1980s over the maritime boundaries around the French Islands of St. Pierre and Miquelon and the contribution of huge European fishing trawlers and floating factories toward the long-term decimation of the east coast cod stocks. Or recall the political power wielded by the dairy industries on both sides of the Canada-US border in the quest toward a NAFTA 2.0 deal. Small sectors commonly punch above their weight particularly when fisheries get combined with growing concern about the environment.

At the time of writing, it appears as though most other major differences in the Brexit negotiations have been settled. The European Union has delivered an ultimatum to the UK to moderate its demands over controlling access to fisheries. Both sides are warning that while a deal may be struck, it may also fall apart which could be simply fairly typical posturing in the late stages of any high stakes negotiations.

US STIMULUS TALKS ENSNARE THE FEDERAL RESERVE

At the time of publication, we still don’t have either a deal to fund the US government beyond the midnight expiration of funding on December 18th or an agreement that would extend expiring stimulus and other measures on December 31st. A government shutdown is among the possibilities, but it seems to be a remote prospect as bipartisan members of Congress indicate they may pass another continuing resolution to fund the government at least over the weekend or possibly longer and until agreement can be reached.

Whereas President Trump has indicated support for a stimulus package, the obstacles to striking deals reside within Congress itself. Key disputes holding up agreement toward a roughly US$900 billion aid package and a bill to fund the government through the fiscal year ending next September include a last-minute effort to set provisions that would block the Federal Reserve from resurrecting credit facilities that expire at the end of 2020.

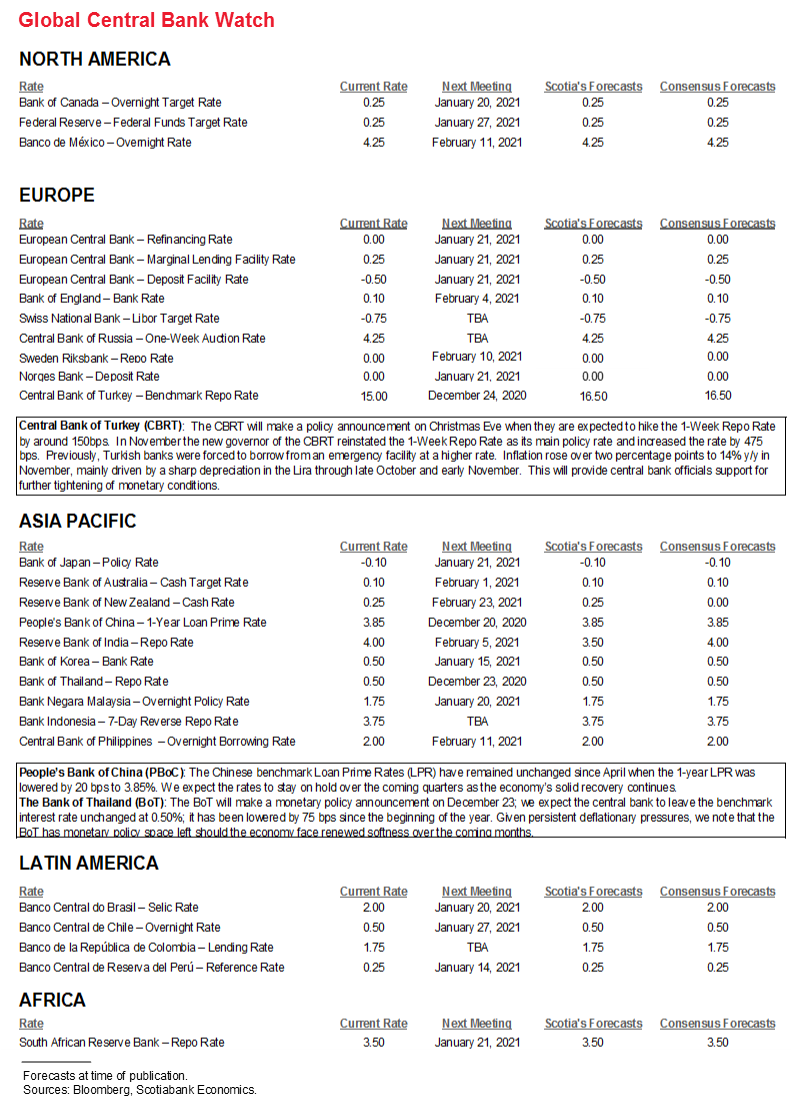

CENTRAL BANKS—TURKEY’S REVENGE

Only three central banks will weigh in with policy decisions over the next two weeks.

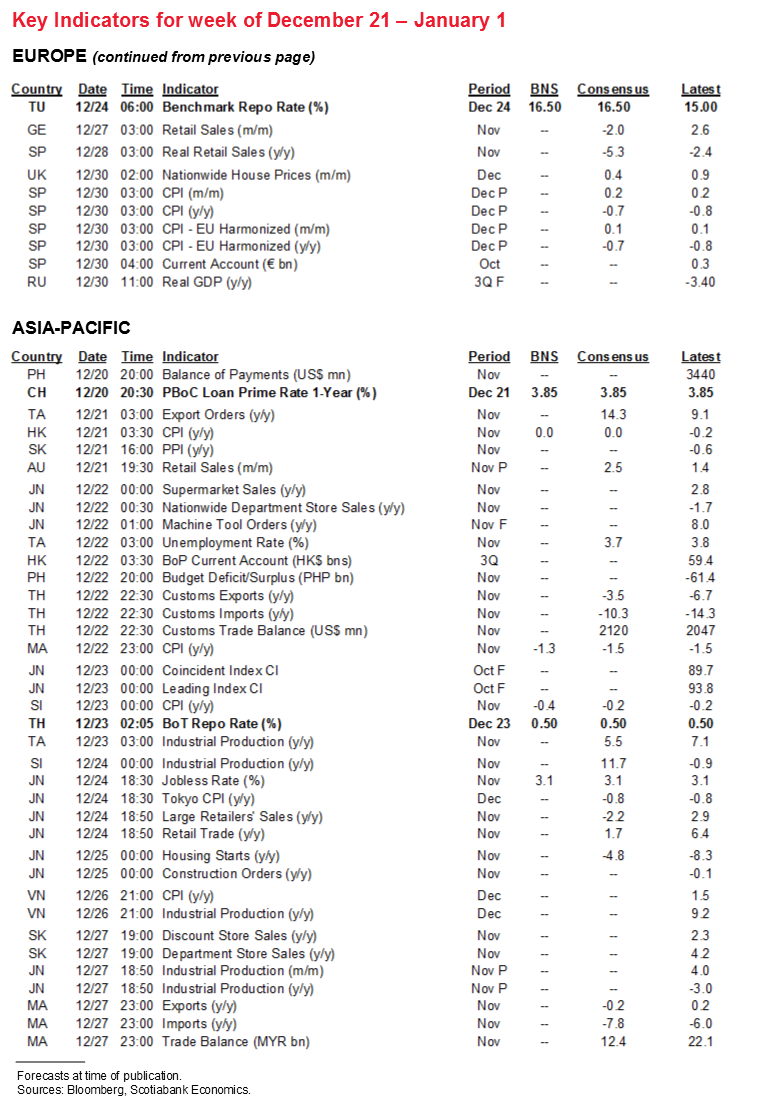

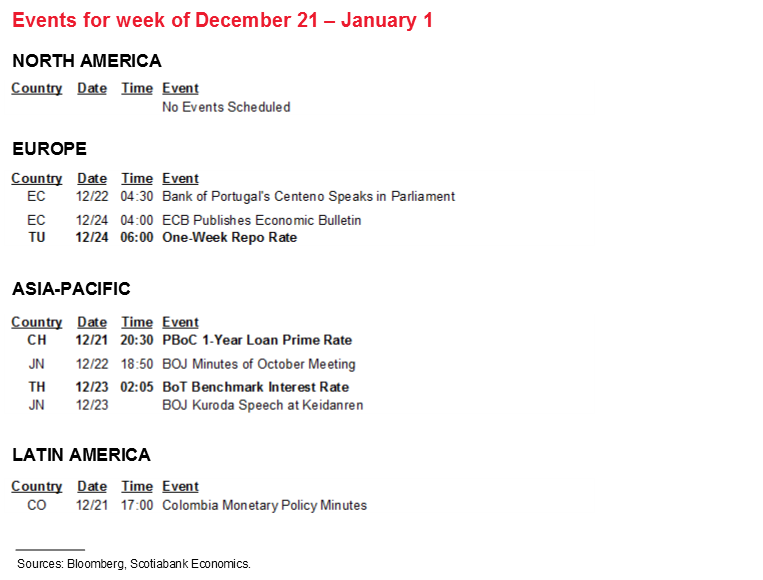

The People’s Bank of China is expected to leave its one- and five-year Loan Prime Rates unchanged on Sunday December 20th at 3.85% and 4.65%, respectively. This expectation was confirmed when it recently left its one year Medium Term Lending Facility Rate unchanged at 2.95%. 2021 will amplify debate over whether the PBOC should continue toward normalizing policy in the face of tumbling inflation (chart 2). Present inflation may reflect lagging effects of the pandemic shock on supply chains while a recovering economy could reassert price pressures over 2021–22. Still, inflation has usually fallen shy of the PBOC’s 3% target.

Turkey’s central bank is expected to hike on December 24th. Well, Merry Christmas to you too! A minority think they may hold at a one-week repo rate of 15% but most expect a hike between 100–200bps. One driver of such expectations is sustained upward pressure upon inflation. Turkey’s core CPI rate of inflation is running at over 13% y/y and has roughly doubled since about one year ago. If they hold off hiking then one reason might be that the lira has been somewhat stabilized over recent weeks following its steady depreciation over the year (chart 3) and so inflation pass-through may be perceived to be peaking.

Taiwan’s central bank is expected to leave its benchmark rate unchanged at 0.5% on Wednesday December 23rd.

MACRO INDICATORS—CHINA, US & CANADA TO DOMINATE

Most of the indicator risk will be focused upon releases out of China and the US over the next two weeks, but even at that it will likely be fairly modest risk.

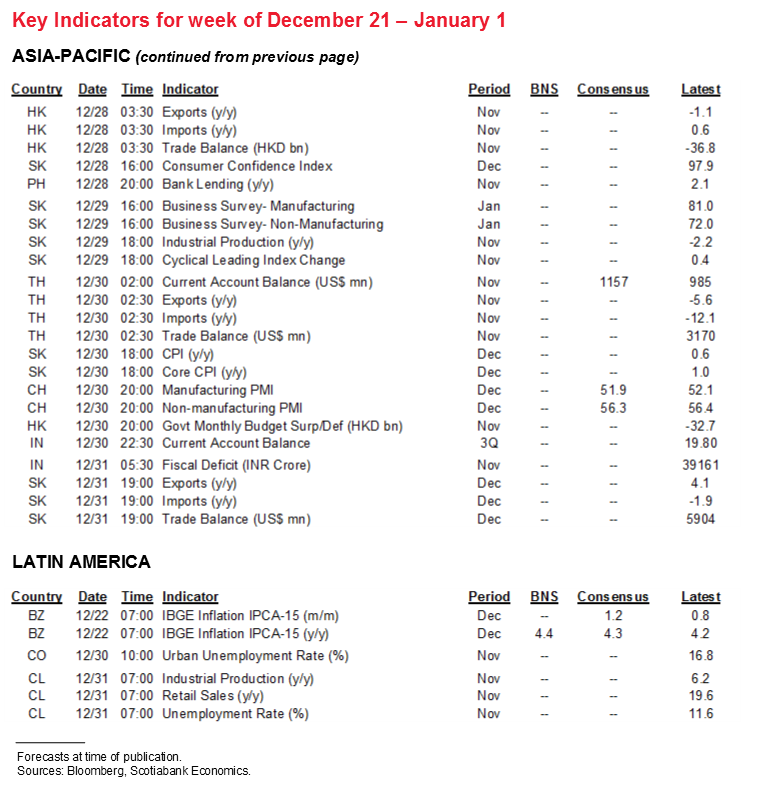

China’s state versions of the purchasing managers’ indices will be the main release of potential significance to global markets over the holiday period. They arrive on Wednesday December 30th. China’s economy has benefited in part from restocking across the world’s major economies as well as a recovering domestic economy as reflected in rising PMIs (chart 4). It’s uncertain whether this will persist through lockdowns and restrictions that have swept through its major trading partners.

US releases will be front-loaded into the first of the coming two holiday period weeks and especially on two days. On Tuesday, the Conference Board’s consumer confidence metric for December is expected to rise a touch, existing home sales for November are expected to soften given weakening pending home sales, and the Richmond Fed’s manufacturing gauge will be released to further inform ISM-manufacturing expectations.

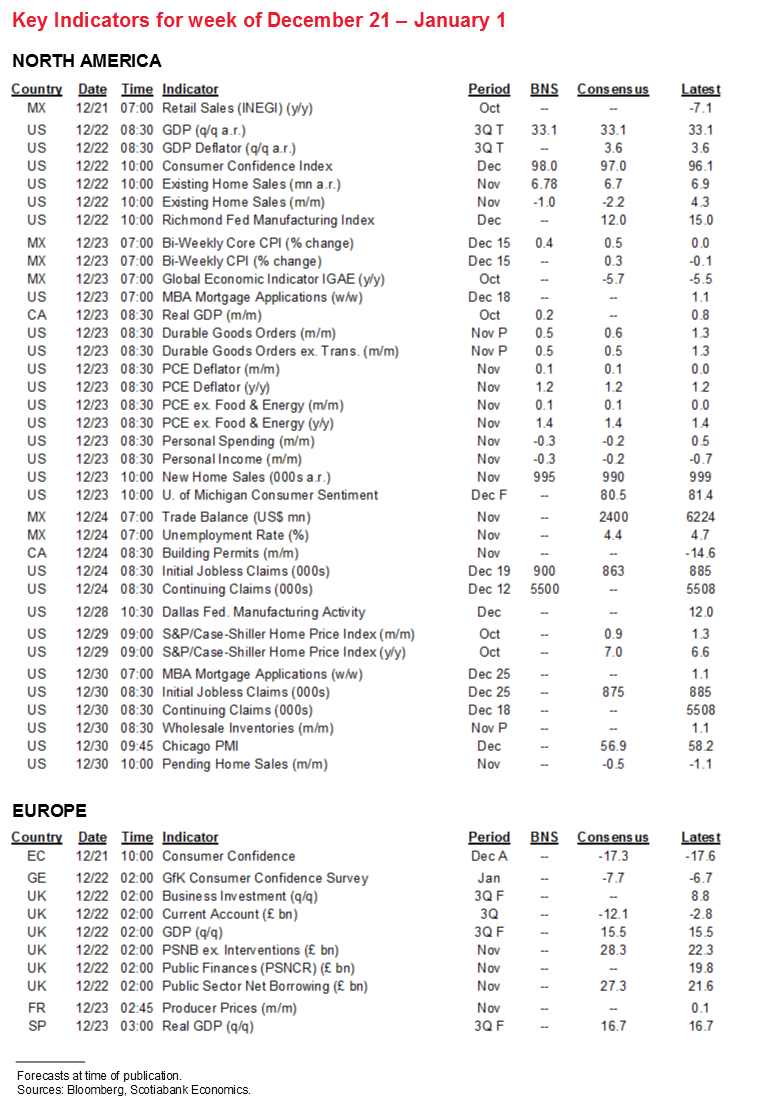

On Wednesday, markets will be watching for another rise in US core capital goods orders in November and a probable softening in consumer spending given what we saw in retail sales combined with tightening restrictions on services and weaker incomes. Headline and core PCE inflation are expected to be little changed, and so are new home sales in November. Weekly claims will be the following week’s only real focus.

Canada only faces GDP for October on the Wednesday before Christmas. StatsCan guided on December 1st that the economy probably grew by about 0.2% m/m in October. Since then, retail sales volumes registered a mild 0.2% m/m gain in October, manufacturing sales volumes were flat and wholesale trade volumes were up by 1.0% m/m. On net, these readings somewhat beat expectations overall but it’s also the case that revisions were more positive than not. As such, it’s feasible that September GDP gets revised up to cancel out potential upside in October’s growth rate. There will be no other scheduled releases or events in Canada over the two-week period.

In Europe, the week of Christmas will offer absolutely nothing on the macro calendar while the subsequent week only brings out retail sales from Germany and Spain as well as Spanish CPI to kick off another round of Eurozone inflation readings.

Latin American markets will be no different from Europe and Canada. The first of the two holiday weeks will only bring out Brazil’s mid-month inflation reading for December (Tuesday) and Mexico’s retail sales for October on Monday and unemployment figures for November on Thursday. The week of New Year’s only offers up Chilean retail sales and industrial production during November on the Thursday.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.