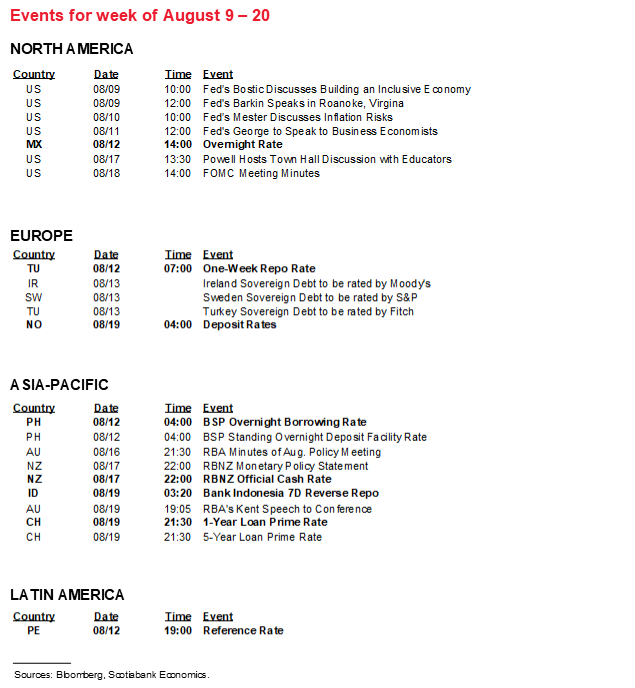

Next Week's Risk Dashboard

• Rising taper pressure

• US CPI: reining in ‘transitory’ rhetoric

• Banxico to hike…

• …and so might Peru

• Global inflation: China, India, Mexico, Brazil, Norway, Sweden

• Other CBs: Turkey, Philippines

• Global macro reports

• A sneak peek at the second week ahead…

• …highlighting FOMC minutes, CDN CPI, CBs and global macro

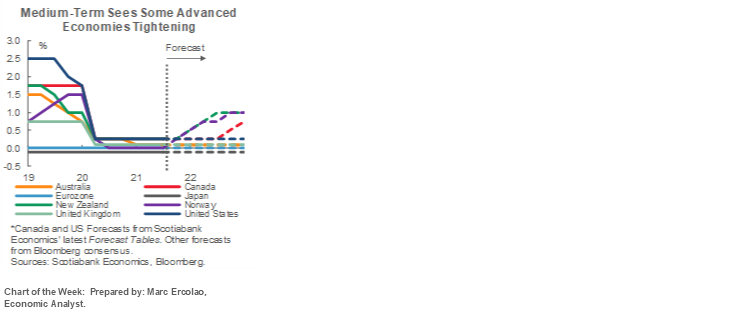

Chart of the Week

Markets are potentially returning to a more vulnerable point that involves assessing the implications of the rise of the Delta variant while US debt ceiling tensions may soon intensify depending upon whether Democrats choose the budget reconciliation approach to addressing the ceiling or gamble on Republican support come September. Alongside such considerations will be the start of the next round of inflation readings with a particular focus upon the US especially in the wake of strong US jobs reports.

At this point, a reasonable set of expectations includes leaving open the possibility that the US and others experience the same decline in Delta variant-driven COVID-19 cases as experienced in the UK where cases fell back almost as fast as they went up (chart 1). Policy is also more likely to use targeted measures and mostly avoid lockdowns in countries that have performed better than others on vaccines. Quebec’s (personally supported) vaccine passports are a vivid illustration of this policy bias and early evidence suggests that the adoption of such a system drives an acceleration in vaccinations.

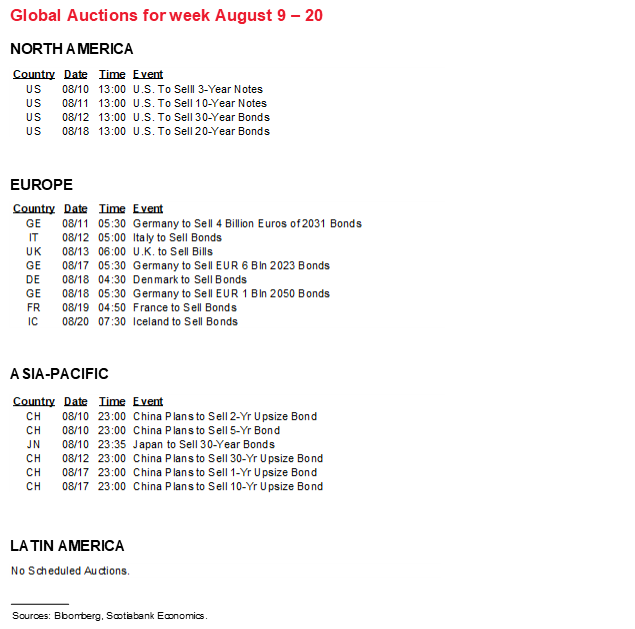

Alongside US and other inflation reports will be further monetary policy tightening across Latin American central banks and a number of global macroeconomic reports covering GDP, industrial output, trade, and US productivity-adjusted labour costs, among others.

US INFLATION—IT’S BEEN ‘SOME TIME’ ALRIGHT

After back-to-back nonfarm payroll gains that were each just shy of one million jobs, the latest bumps and wiggles in global—particularly US—inflation readings are likely to dominate market attention over the coming week. It’s likely too soon to expect material relief for price pressures and it will take considerable time to inform such prospects in any event.

Enter the next round of inflation figures. US CPI for July arrives on Wednesday August 11th and could hang in unchanged at about the prior month’s readings of 5.4% y/y and 4.5% y/y for headline and core CPI, respectively, and with increases of approximately ½% m/m in both cases. There is a lot of uncertainty around the estimates, but the pattern for a few months now has been toward higher-than-expected readings. Base effects alone will likely exert downward pressure on the year-over-year rates in both cases. July is typically a seasonally neutral month for headline and core prices. Gasoline prices probably added little to month-over-month pressures.

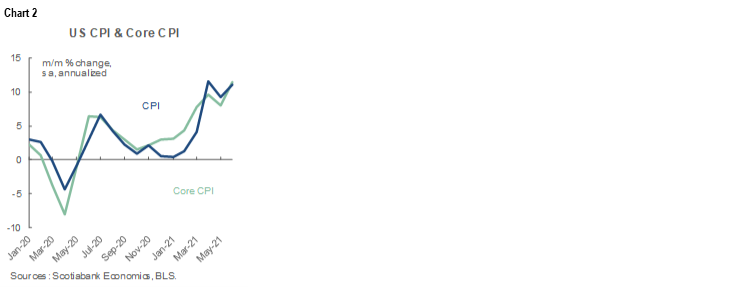

That leaves one guesstimating reopening effects on the month-over-month price swings that have tended to dominate the reasons behind inflation’s rise this year, despite those who still cling to the idea that inflation is all about year-ago base effects. That view has been disproven. Chart 2 shows the month-over-month annualized changes in seasonally adjusted CPI and core CPI that vividly depict the super-acceleration over the past five months and counting.

For how long could this last? As previously argued, supply chains are likely to remain tight with low inventories, soaring shipping costs and port congestion for a while yet and there is no clear evidence of relief in sight. How long ‘a while’ is will remain highly uncertain but there are a few points worth making about the “transitory” dialogue after first noting that transitory should be evaluated in the context of the full monetary policy horizon and not just the next CPI print or a handful over coming months.

Don’t Forget the Transitory Downsides

You’ve seen the charts showing the price gains in select reopening parts of the economy like airfare and lodging plus vehicle prices that make it look like inflation is narrowly based and once this effect subsides, inflation will magically crash back down again. Such an approach provides an incomplete and arguably intentionally biased take on inflation risk. For one thing, alternative central tendency measures of inflation that basically lessen the role of outlier movements have themselves turned upward (chart 3). Further, too often it seems that the transitory dialogue only emphasizes prices that are perhaps unlikely to continue to post strong gains going forward. That alone is debatable, but the potential transitory downsides to inflation readings get ignored.

For instance, core goods price inflation is strong and may persist given supply chain problems, but what if we’ve only begun to see core services inflation pick up as the economy reopens (chart 4)? Services ex-energy carry an almost 60% weight in CPI.

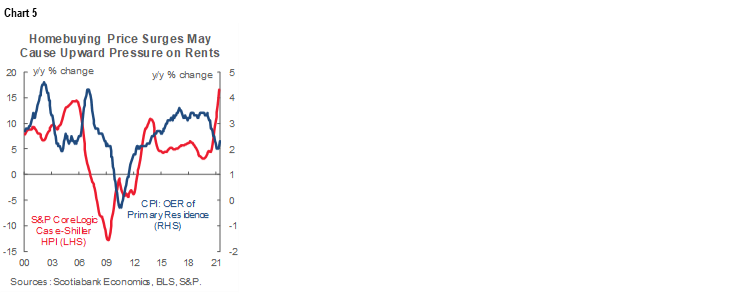

Or, what if the one-third weight on rent within CPI is only depressed of late because of the rate-induced feverish pace of home buying that when it stabilizes—and it may be doing so—will be followed by a return to the rental market? The rough connection between house price inflation and rent inflation over time would tend to support this view (chart 5). As buyers get pulled into housing markets thanks to low rates, they get pulled out of rental markets but this dynamic could just as well reverse as home affordability has become more strained.

Will new vehicle shortages that drove upward pressure upon used vehicle prices reach a point of stabilization with supply chain problems possibly putting further upward pressure upon new vehicle prices? Used vehicles were relatively cheap compared to new vehicles into the pandemic but soaring used prices have now made them relatively dear (chart 6).

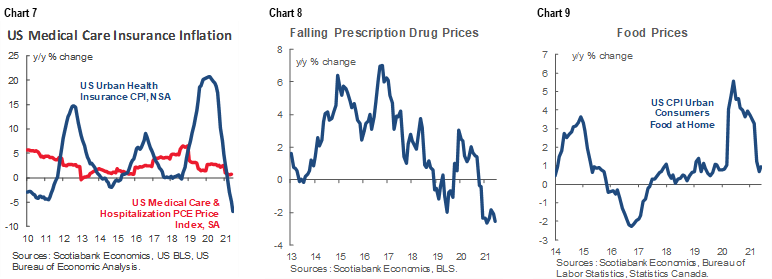

Also, has medical care price inflation suddenly and sustainably ground to a halt after decades of rising pressures driven by technology and aging populations (chart 7)? Has increased policy scrutiny temporarily driven prescription drug prices lower and, after this effect stabilizes, we could see a return to the forces that have driven prescription drug prices higher over time (chart 8)? Has the food-at-home category of prices only softened because of high year-ago base effects when the early stages of the pandemic were sparking widespread stockpiling and once this shakes out we could see a return to food price inflation (chart 9)?

The point to the above is that, at least to me, it’s unclear that higher inflation is transitory. It might be, but I’ve argued from the beginning that I’d prefer central bankers to sound less like a hedge fund manager talking a position and to sound more circumspect and open to bidirectional risks. That approach was entirely absent when inflation began to take off and both the Fed and BoC dismissed it as just base-effect driven and something that would hence magically disappear.

That policymaker bias is gradually softening. Chair Powell speaks less about it all just being base effects now, though he is still biased toward transitory arguments but at least now says that they will act if inflation is more persistent. US Treasury Secretary Yellen says inflation will be elevated “for some time” but fall back toward the Fed’s mandate toward the end of 2021. That probably no longer means 2%, given that the Fed’s revised long-run goals statement says “monetary policy will likely aim to achieve inflation moderately above 2 percent for some time” following the past undershooting episodes. Fed Vice Chair Clarida recently swung in favour of tapering bond purchases later this year as inflation has been more persistent and broad-based than he expected and he was previously the most dovish senior FOMC official not named Powell. In my view, it’s time for the FOMC to more aggressively set in motion the process toward the first reduction in purchases; the longer it waits, the more it risks overheating present conditions, pulling forward future activity, and subsequently trapping itself with no future way out.

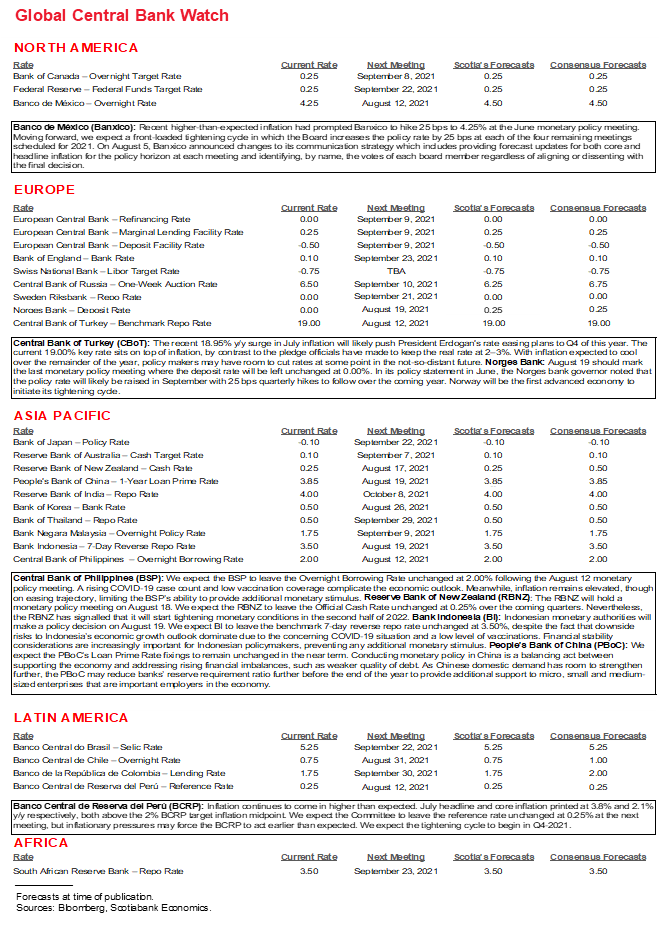

INFLATION TO KEEP PRESSURING SEVERAL OTHER CENTRAL BANKS

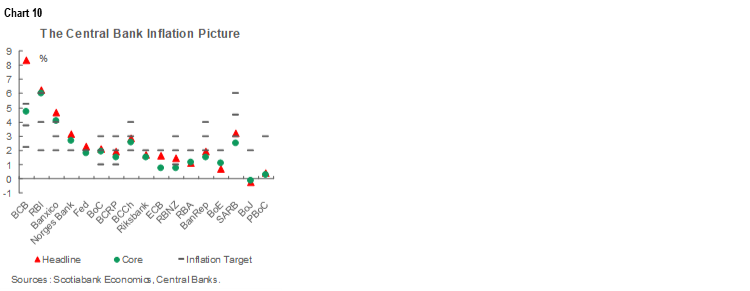

US inflation will dominate global markets, but several other countries are worth briefly highlighting. Chart 10 provides an instant depiction of where each of these countries’ central banks—and most other major central banks—sit in terms of actual inflation relative to their targets.

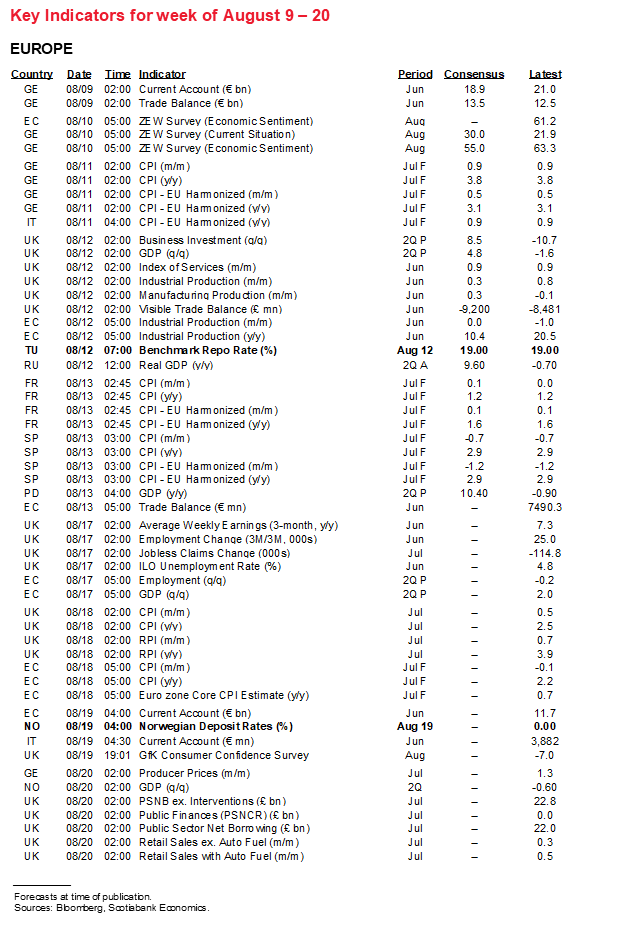

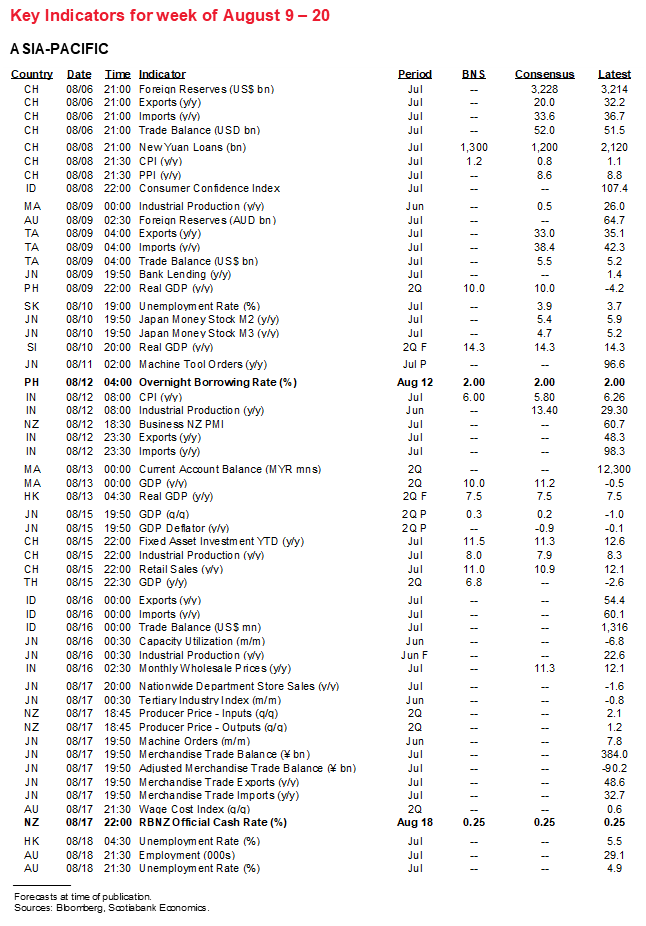

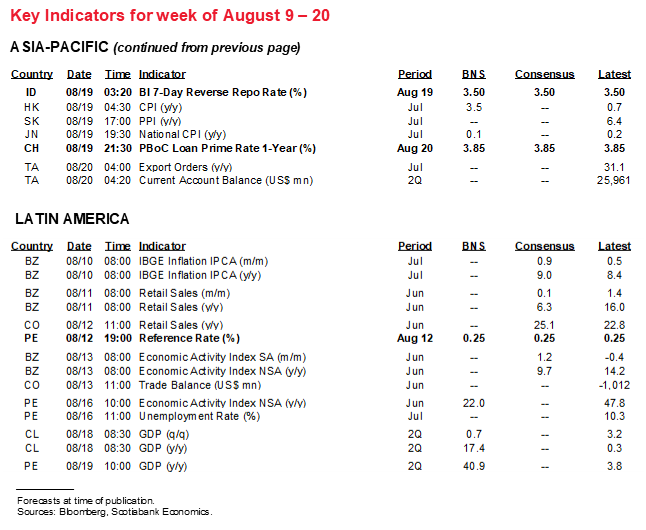

- China: China will update CPI inflation and producer price inflation for July on Sunday night (ET). Producer prices might be at a turning point lower in year-over-year terms which is just a commentary on commodity price changes for the most part. CPI and core CPI are soft in year-ago terms but rising along a somewhat noisy path as the year-ago base effects drop out.

- Mexico: CPI for July arrives on Monday morning before Banxico’s policy decision on Thursday (see below). Another solid ½% m/m rise is expected to keep the year-over-year rate just shy of 6% with core inflation climbing to just over 4½% y/y.

- Brazil: July’s print arrives Tuesday and is expected to keep rising with headline inflation approaching 9% y/y. Hence why Banco Central do Brasil has raised its Selic rate from 2% back in March to 5.25% and counting today and despite the ongoing COVID-19 tragedy.

- Norway: In its last policy statement on June 17th, Norges Bank guided markets that “the policy rate will most likely be raised in September.” Tuesday’s CPI inflation report for July isn’t likely to change that guidance. Norges already knew that headline inflation was running well above its 2% target at its prior meeting and a possible mild deceleration from 2.9% y/y in June likely won’t affect things. Underlying inflation has been considerably softer at 1.4% y/y with downside risk. It’s the month-over-month momentum that counts most, however, and we could see a powerful rise in the update.

- India: Thursday’s July inflation print could see at least the year-over-year reading pull off from over 6% y/y to under 6% while remaining at the upper end of the 2–6% inflation target range. Core inflation has been sharply rising but the central bank has tended to look through a considerable portion of the rise. Still, its latest policy decision rocked the Indian bond market when a dissenting voice emerged, liquidity withdrawal efforts were doubled and the inflation forecast was raised.

- Sweden: July CPI is due out on Friday. By contrast to its Scandinavian neighbour, Sweden’s Riksbank has been in no rush to signal hikes. One issue that might help to understand this is the sensitivity around avoiding a repeat of past premature policy tightening. The other issue, however, is that Sweden is just not seeing the same inflation pressure thus far as Norway has seen. Headline CPI inflation is expected to hold around 1.3% y/y with little month-ago change and with underlying inflation running at 1.6% y/y.

CENTRAL BANKS—LATAM POLICY TIGHTENING

Out of the four central banks that will each deliver updated policy decisions on Thursday, only one is expected to change its policy rate with the risk of a hike at another.

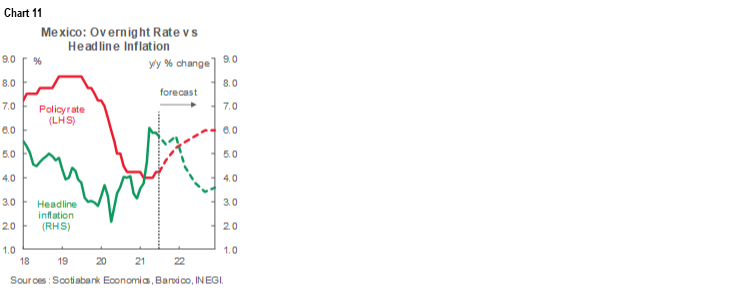

Banxico jolted markets when it hiked its policy rate by 25bps in June. It is likely to raise its overnight rate by another 25bps to 4.5% on Thursday. Given the speed of developments during unusual times, Deputy Governor Jonathan Heath may have been a tad harsh when he said the central bank “screwed up” inflation forecasts as justification to hiking. Still, it was refreshing frankness and the central bank acted on its surprise by tightening policy. The comments followed earlier ones from Heath about how “It turns out this temporary bubble perhaps isn’t that temporary. Perhaps we have a problem that’s a bit more structural that we need to focus on.” Other central banks perhaps take note. Going forward, our economists in Mexico City expect four consecutive quarter-point hikes through to year-end. That may be what is necessary to bring inflation lower (chart 11). Starting with this meeting, we’ll also get inflation forecasts and votes with names assigned.

Peru’s central bank faces hike risk next week but our Lima-based economist expects a hike at the following meeting. Inflation has risen above the 1–3% target range and landed at 3.8% in July. Political volatility has contributed to currency depreciation and concomitant imported inflationary pressures. If Peru hikes, it would join other tightening Latin American central banks including Banxico, Brazil and Chile.

Central banks in the Philippines and Turkey are expected to stay on hold.

OTHER GLOBAL RELEASES

There are a few gems in the global line-up of macro releases due out over the coming week.

Q2 GDP figures arrive in the UK and Russia (Thursday), Malaysia (Friday) and Philippines (Monday). The UK is expected to see strong growth of ~5% q/q non-annualized as its economy took steps toward reopening. Russia? Not so much. A contraction of over 1% q/q seems to be in the cards.

Other US releases will focus upon University of Michigan consumer sentiment including inflation expectations for August on Friday, as well as Q2 productivity and unit labour costs that should reveal moderated growth in productivity-adjusted wages but still at a 3–4% annualized pace.

Several countries will update industrial production and trade figures including production in the Eurozone, UK and India (Thursday) and Norway (Monday) as well as trade figures for Germany (Monday), China to start the week, the Eurozone (Friday), UK (Thursday), India (tbd), Colombia (Friday), Mexico (Wednesday) and South Korea (Thursday).

China might update financing figures for July sometime next week or the following week. Other releases include the UK services PMI (Thursday), German ZEW investor confidence (Tuesday), South Korean jobs for July (Tuesday), French jobs during Q2 (Friday) and retail sales figures out of Brazil and Colombia on Thursday.

SNEAK PEEK AT THE WEEK AHEAD OF THE WEEK AHEAD

Given summer vacations—at least in the northern hemisphere—the purpose of this section is to highlight expectations for the week after the week ahead and with other publications expanding upon the views. The indicator and central bank watch tables include expectations for this second week ahead.

Inflation reports will arrive covering the month of July in Canada (Wednesday August 18th), the UK (Wednesday) and Japan (Thursday).

I’ll be particularly focused upon Canadian inflation. It’s possible that the prior month’s dip in the year-over-year rate will bounce back. Base effects will be a neutral influence this time. A modest seasonal effect on prices is likely and with a small assist from gasoline prices. The dominant influence will nevertheless be reopening and supply chain pressures that could lift the month-over-month unadjusted rate to 0.4% and the year-over-year rate back to 3½%.

Across central banks, minutes to the incrementally hawkish FOMC meeting on July 28th will be released on Wednesday the 18th. Recall the outlines of what the July statement and Chair Powell’s press conference offered here. The statement noted that since ‘substantial further progress’ was mentioned last December, “the economy has made progress toward these goals.” After another nonfarm gain of almost one million and given inflationary pressures, the key is how close the FOMC is to tipping the language toward having achieved ‘substantial’ progress. Powell was also cautiously optimistic toward the Delta variant, saying that successive rounds of COVID-19 infections “have tended to be lessening.” The general tone in response to questioning on inflation was defensive in my view, while Powell noted “we don’t have much confidence in the size or timing of that” in reference to inflation moving down over time. Minutes may reflect a more in-depth discussion on tapering Treasury and MBS purchases with emphasis to be placed on the frequency of citations around opinions on whether the criteria have been met, whether they may soon be met, how many participants favour acting soon and perhaps when.

Norges Bank will likely reaffirm plans to hike in September on the 19th. Chart 12 shows its last policy rate path. The RBNZ could raise its policy rate on the 17th but forward guidance may be mindful regarding Delta variant risks across Asia-Pacific countries. The People’s Bank of China recently adopted more of an easing stance by cutting the required reserves ratio, but its policy decisions on the one- and five-year Loan Prime Rates on the 19th and forward guidance will be carefully watched in the context of renewed Delta variant risks hitting an economy that was already challenged by softened growth.

Retail sales updates will inform the state of US, Canadian, UK and Chinese consumers and the evidence could be slanted toward soft US and Chinese figures.

The US (Tuesday 17th) will require a strong sales gain excluding autos and gas in order to avoid a renewed dip in July’s retail sales given we already know that supply challenges pushed auto sales lower.

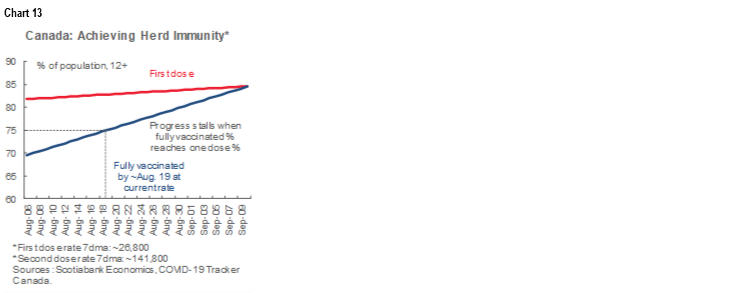

Canadian retail sales (Friday 20th) are expected to post a strong gain of 5% given advance guidance from Statistics Canada that may not have fully captured the reopening effects later in the month, plus advance guidance for July’s retail sales for which we know that auto sales were higher, gas prices were higher and overall retail prices probably edged higher to be informed by that week’s CPI reading. Canada is on the path toward herd immunity later this month (chart 13).

UK consumers posted a pretty modest ‘rebound’ of 0.3% m/m in June as the economy began to reopen and following a 2% prior decline. July’s reading on the 20th will inform the volatile trend as PM Johnson remained committed to further reopening steps last month. Job market updates on the Tuesday of that week will also inform consumer fundamentals.

Chinese retail sales may suffer a deceleration in year-over-year growth in July (August 15th) as Delta variant restrictions resulted in significant declines in metro ridership and traffic congestion in several regions.

Can Australia keep the streak of powerful job gains alive as its major cities went into lockdown due to rising COVID-19 cases? That’s doubtful and so the 144k rise in employment over the months of May and June could face risk of renewed decline.

Other releases will include GDP reports out of the Eurozone, Japan, Norway, Thailand, Chile, Colombia and Peru. After a quiet prior week, Canada will also record an expected gain in manufacturing shipments, possibly soft home sales and starts, and a dip in wholesale trade. Other US releases will be oriented toward the industrial sector including industrial production that should rise in July (Tuesday) and each of the Philly and Empire manufacturing reports.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.