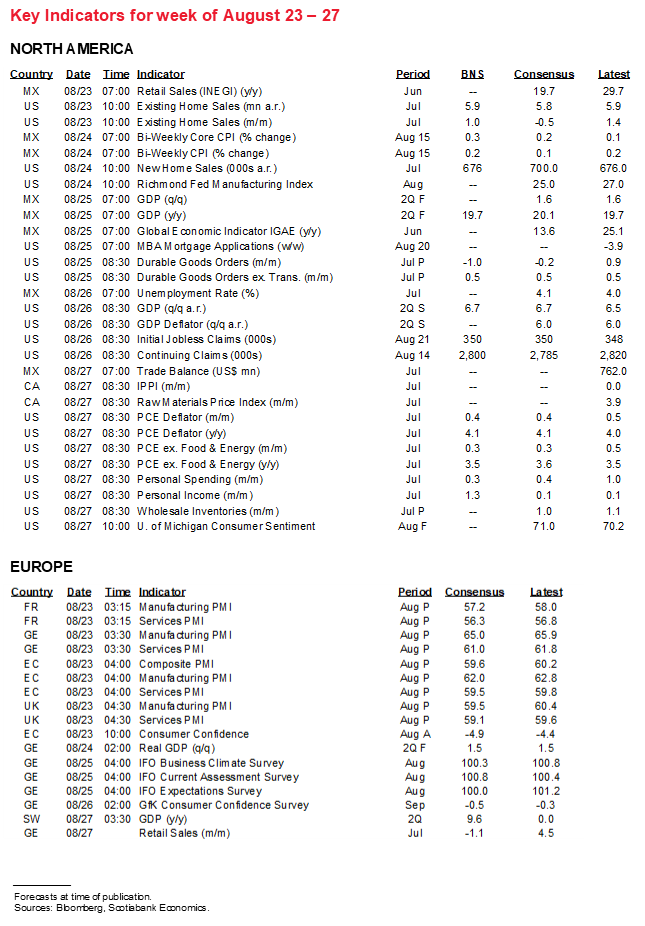

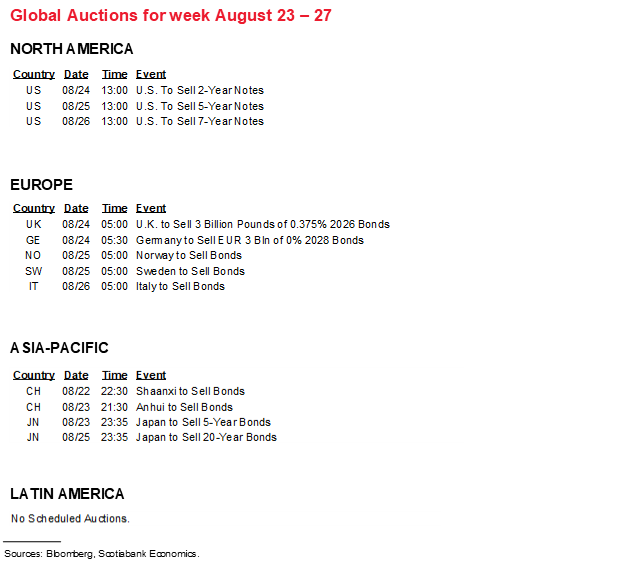

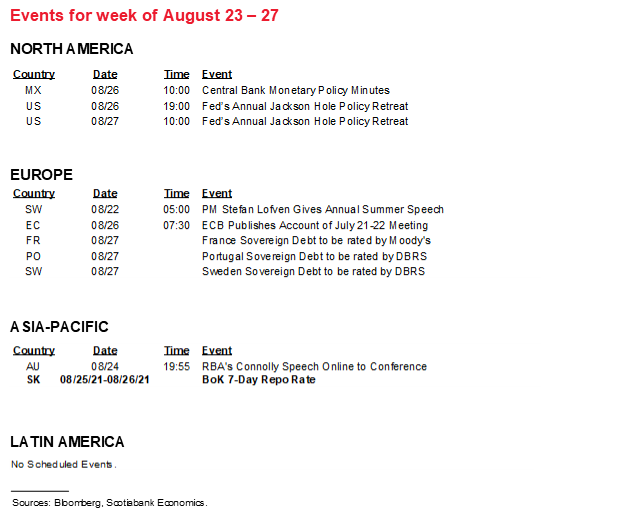

Next Week's Risk Dashboard

• Fed’s Jackson Hole to be a snoozer?

• Why a taper tantrum could be gentler this time

• EMs & tapering: then vs. now

• Is the US economy rolling over?

• PMIs: EZ, UK, US, Australia, Japan

• Election watch in Canada

• CDN bank earnings

• US incomes face upside

• Other macro

• CBs: BoK

Chart of the Week

When it comes to the approaching week, there is Jackson Hole, followed by everything else. That’s as much of a commentary on the importance that the Federal Reserve’s annual symposium has taken since 1978 as it is on the lack of a whole lot else going on during the dog days of August. There may not be big fireworks this time, but it presents an opportunity to revisit some key themes around the US economy and potential effects of shifts in Fed policy.

JACKSON HOLE—POWELL’S HAND HAS ALREADY BEEN REVEALED

Mark your calendars for this event that runs from Thursday evening to Saturday. The theme for this year’s symposium is “Macroeconomic Policy in an Uneven Economy.” That likely speaks to emphasis upon inclusive recoveries, what central banks can do if anything to promote them and concomitant risks.

We’ll get the detailed agenda by about 8pm Central Time (9pmET) on Thursday evening. Chair Powell is scheduled to speak virtually at 10amET on Friday about the economic outlook and will be available live here.

After holding a 100% virtual event last year, this year’s symposium was supposed to be in person but then the Delta variant changed plans so now it will be fully virtual again. Because of the original in-person goal, the event was reportedly focused upon domestic participants which likely reduces the significant of the event for observers of other central banks. For example, the ECB has confirmed that President Lagarde will not attend and the Bank of England has confirmed that Governor Bailey will pass. The BoC has not said anything publicly nor have other major central banks, although past participants have not always been known until the agenda is revealed. It’s unclear if anyone’s (virtual) participation plans may change nowl. That was likely a super smart decision in order to avoid the Fed’s event being a super spreader among central bankers with Wyoming’s case count having risen to over 2,000 cases.

The symposium is unlikely to offer any materially new information on timing the amount and path for the Fed to reduce bond purchases. It would be pretty surprising if it did, given the tone of recent communications. Minutes to the late-July FOMC meeting (recap here) were rather explicit in tamping down concern that the Fed might have been moving toward reducing bond purchases as soon as the September meeting and committing to an aggressive path toward shutting them down by next Spring or Summer. That view remains in the minority on the FOMC and held by nonvoting regional Fed Presidents including Bullard, Kaplan, George and Rosengren, although Kaplan may be softening his position somewhat. That said, 3 of the 4 hawks vote next year which could make for greater risk of policy dissents and/or fireworks. Instead, the majority on the FOMC leans toward tapering purchases later this year.

That doesn’t mean there is nothing to talk about. I’ll focus on four things of interest to market participants: what Powell will probably repeat on substantial further progress, why a potential taper tantrum could be less severe than in 2013, why there may be bigger vulnerabilities around EM capital flows this time and the debate over why we’ve seen (some) weakening economic indicators of late. The latter could dominate the Fed’s attention as it evaluates the possible impact of the Delta variant upon the economy.

ISSUE 1: SUBSTANTIAL FURTHER PROGRESS—NOT THERE YET

Don’t look for any epiphanies relative to the latest round of FOMC minutes (recap here). The FOMC consensus leans toward tapering later in the year and probably doing so along a somewhat prolonged path while observing more data on inflation and jobs.

There will be a lot of discussion on inflation at Jackson Hole. We’re likely to once again hear that present rates of inflation are unsustainable, but that the committee consensus thinks they are more likely than not to witness inflation slightly above 2% over the forecast horizon. For a further discussion on inflation drivers and uncertainty toward how transitory it may be go here.

On the full employment mandate, Powell will likely repeat his view that almost 6 million Americans who had jobs in February 2020 still do not have employment. The labour force participation rate is still 1.6 percentage points below February 2020. The U6 underemployment rate of 9.2% that also captures discouraged workers remains about 2¼% above the pre-pandemic level. Millions of Americans have yet to return to full employment and the breakdown of those figures continues to leave the relatively more vulnerable parts of the US population behind. Powell is likely to repeat that achieving full employment lies well within the 2021–22 monetary policy horizon which would reinforce expectations the Fed is leaning toward reducing purchases as the calendar flips over into 2022. The debate over whether the Chair is overestimating job market slack will continue with wage growth arguably being the best arbiter of this debate and with implications for inflation.

ISSUE 2: THE US ECONOMY—STUMBLING, OR THE GREAT ROTATION?

What may take center stage at Jackson Hole will be discussion of the resilience of the US economy in the face of rising Delta variant cases and mixed readings on the economy. I realize many clients are questioning whether we’re at a risky inflection point for growth. Part of that concern is perfectly understandable with rising COVID-19 cases and recent weakening in some indicators. But part of the concern may not be fully accounting for other important interpretations.

First, let’s be sure not to come across Pollyannaish here before addressing other important issues. The rise of the Delta variant is a risk. We’re still erring on the side of a resilient US economy as happened last summer and through the winter and emphasizing the diminishing effects of successive case waves. Nobody has a clear crystal ball here and so we have to monitor behaviour very closely. For instance, is declining US air travel of late just a seasonal norm that happened the year before the pandemic into August, or signalling something worse (chart 1)? Is it reflecting diminished demand for flights or tougher airline restrictions that could push spending elsewhere in the economy? We’ll know more over coming weeks for this reading.

Second, I think the supply chain problems are softening the demand side in the interim because even though they may want to spend, folks can’t find product to buy. That means digesting demand side indicators with a bit of a dose of salt. Auto dealer lots are empty. The all-retailers’ inventory to sales ratio is at a 30 year low back to the early 1990s recession. Wanna buy something? You’ll have to wait, pay more or do without. Wanna buy a home? Good luck, the resale months’ supply has slightly risen of late but is still around a record low so you’re either going to pay or have endless debates and possibly arguments over what you can and can’t live with. This is important because it counsels against viewing some of the softer readings as an indication that the demand side is troubled.

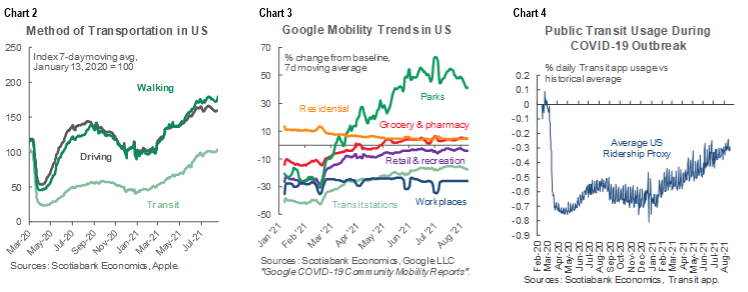

Third, economic data lags, and so to assess what’s going on at the margin we have to get a bit creative with alt-data. We didn’t have that when I first started my career but now we live in an age when Apple, Google and probably your employer watch absolutely everything you do 24/7—and you’re ok with that! The selfish benefit to economists is that it gives us a richer array of things to observe. Enter charts 2 and 3 that track mobility by mode of transportation and by venue. Apple readings show that Americans are not digging a hole and sticking their heads in the sand. Transit readings are holding up (chart 4). So is driving that may be topping out but at higher than pre-pandemic levels. So is walking. Google tracks where you are by type of venue and they say that there isn’t much of a shift going on other than decreased attendance at parks that matter little to the economy per se.

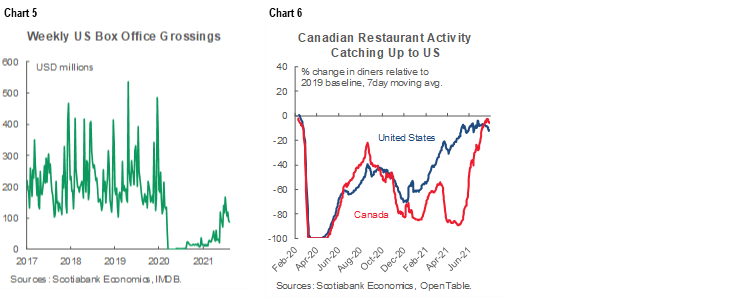

Fourth, we’re at an inflection point in the composition of consumer spending. That means perhaps less growth in spending on goods, more on services. Consumers’ spending on services has risen by 1–2% m/m for four straight months and next week’s July figures are likely to add to that. But the system of data we have dates back to the age of Ward and June Cleaver so we still have better and fresher gauges for the goods side than the two-thirds of the economy that is in services and the latter often results in a more complete picture with a longer lag and often heavy revisions. This means looking at different types of readings than just, say, retail sales that underrepresent services. For those, we can look at almost up to the minute gauges throughout August to date including hotel occupancy that has slightly softened but remains around pandemic highs (here), box office receipts (chart 5), flights and restaurant reservations (chart 6). These are among the readings to watch as consumers spend more on socially distanced activities and drive less growth in goods consumption. They are the most sensitive to the Delta variant but at least so far there is little evidence that consumers are pulling back despite the temptation to think otherwise.

Fifth, we’re at an inflection point in the consumer versus production side of growth drivers. Industrial production is doing just fine. If not for supply side challenges it might be growing even faster. Production, investment and exports might be taking over from ordering useless stuff off Amazon. Three cheers for that from a long-run wealth standpoint!

But the dominant challenge to reading the tea leaves in my view is that I’ve never seen a more damaged supply side than we have at present and that’s messing up a whole bunch of things including consumer confidence. For one, it feeds back on the demand side through shortages and higher prices and makes it challenging to assess economic conditions as those supply side challenges work themselves out. That’s going to take a long, long time and is not something to measure in a quarter or two on the calendar. In the meantime, the broad output gap as conventionally measured will soon shut and growing the supply side is going to become more problematic to the inflation outlook. Consider everything from port congestion to semiconductor shortages, shortages of multiple electronic components, broad inventory depletion, soaring shipping costs with container shortages, a partially obsolete capital stock set in place before the pandemic and now dealing with a fundamentally changed economy, lower labour force attachment with mismatched skills for a changed economy and retirement exits, the often forgotten impact of Trump’s fruitless trade wars, rolling COVID-19 restrictions impacting chains in Asia etc etc. The confluence of factors hitting the supply side is unprecedented for all practical purposes.

So where does this leave us on net? Cautiously monitoring a broad suite of readings, prepared to adjust if we see alt-data and other signals sharply deteriorate, but still erring on the side of cautious optimism. It’s August and so uncertainty into September is hardly unprecedented. Reading the tea leaves requires doing more homework than glancing at some of the conventional readings while assessing the demand and supply sides together in ways we’re not as accustomed to doing relative to prior periods.

Which brings me back full circle to the Fed. My personal belief doesn’t matter to forecasting the Fed, though it may to other variables, but fwiw I still side with the relatively hawkish FOMC members. If the supply side is so seriously challenged as to drive a fundamental reassessment of the supply-demand imbalances then we’d better embrace and get on with tolerating a cooler demand side—or else live with high inflation for longer. That probably means that all of the emphasis should be placed upon taking out more balanced insurance against inflation risk especially after no major central bank forecast anything close to the kind of inflation they now spend so much time talking through as something that’s gotta magically and sustainably disappear.

ISSUE 3: TAPER-TANTRUM LIGHT?

Will global financial markets have the same reaction to tapering this time that they did in the upheaval to the 2013 ‘taper tantrum’? A bumpy ride is likely for risk appetite not least of which since the whole point of reducing purchases is to gradually reduce incremental stimulus and tighten financial conditions which implies repricing assets from bonds through equities, currencies and commodities. The issue is how disruptive it may be this time. On that, it’s important to note the differences between 2013 and now that should make the effects less severe. I wrote about these earlier in the year alongside warning of inflation risk (here).

First is that the Fed learned its lesson on how to communicate its intentions better than in 2013. Today’s emphasis is upon gradually communicating intentions well in advance rather than dropping causal surprises in routine testimony.

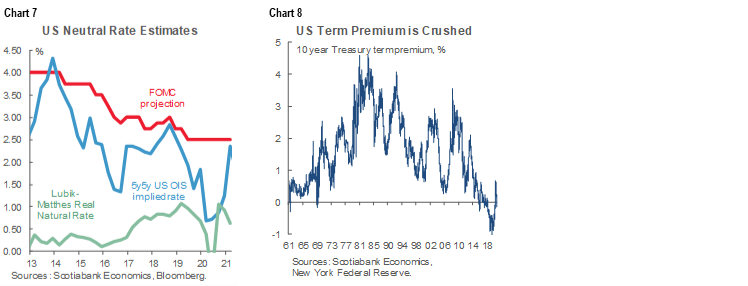

Second, there is probably a narrower corridor within which Treasury yields may be rocked than was the case in 2013 when the 10-year Treasury shot up from 1.6% in May 2013—when then-Chair Bernanke first guided that the Fed may taper over the coming meetings—to 3% by the time they did so in December of that year.

That’s primarily because the Fed and the market have lowered their estimates of the Fed’s long-run neutral rate (chart 7). Market measures don’t necessarily perform any better at estimating the neutral rate than fed funds futures perform at predicting the fed funds target rate, so a neutral rate around 2% or slightly higher is assumed. Back in 2013 the conventional wisdom was that this neutral policy rate could be double today’s estimates. We (and I) have learned a bit since then! With the policy rate constrained by a positive lower bound given the Fed’s rejection of negative rates, a lower neutral rate estimate today than in 2013 with near-zero term premia tacked on (chart 8) should contain the upside pressure upon the whole term structure of interest rates to less than what was the risk in 2013–14. Markets are notorious for undershooting and overshooting resting points, but this corridor argument could contain the ultimate resting point. That means less potential shock to the bond market that could sell off within a lower and flatter term structure of interest rates and hence across discount rates for equities.

To these points one could add other aspects of how the markets have changed since the 2013 tantrum. Back then there was very little negative-yielding debt in the world versus US$16½ trillion of negative-yielding debt today (chart 9). While correlated selloffs are likely across global bond markets in a taper scenario, carry out of negative-yielding markets into Treasuries may contain at least some of the potential rise in Treasury yields. So do firmly anchored negative policy rates in areas like the Eurozone and Japan that pay investors to take cash and reach for yield wherever they find it. Downward pressure upon relative carry now versus 2013–14 including via negative policy rates in the Eurozone and Japan could contain currency movements as well. If so, then negative rates elsewhere and carry into the US Treasury market could actually serve to expedite the withdrawal of Fed stimulus. In addition, there remains a large glut of global excess savings that can help contain higher yields and pressure on individual countries’ capital accounts, but not thwart such effects.

That doesn’t mean a bond sell-off would be a delightful experience this time, but it’s a reason the US 10-year yield is forecast in a tapering scenario to rise to 2% later this year into next. That would still be relatively low by historical standards, but a notable sell-off from today’s levels.

ISSUE 4: EM VULNERABILITIES

While there may be a less disruptive impact on domestic financial markets, will that hold true for emerging markets? If not, will that provide a negative feedback effect on domestic asset markets? That’s unclear, but one way of approaching it involves looking at how their country risk parameters may have changed since then.

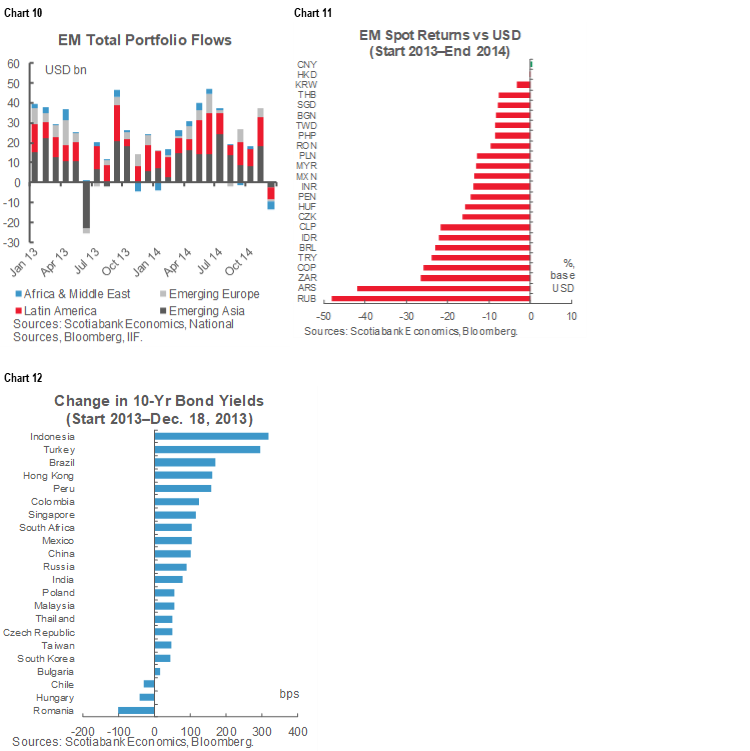

Recall that in 2013, the initial taper tantrum resulted in a large withdrawal of portfolio flows from emerging markets (chart 10). This was true across both equities and bonds. The second-round response continued to offer capital flows, but the market demanded a steadily higher return which drove many currencies sharply lower over 2013–14 (chart 11). This was not just the case for EMs either, as other higher beta currencies weakened—such as the Canadian dollar that depreciated by over a dozen cents from early 2013 through to early 2014. The repricing of the US 10-year note and capital flight from EMs also drove their own bond yields sharply higher (chart 12).

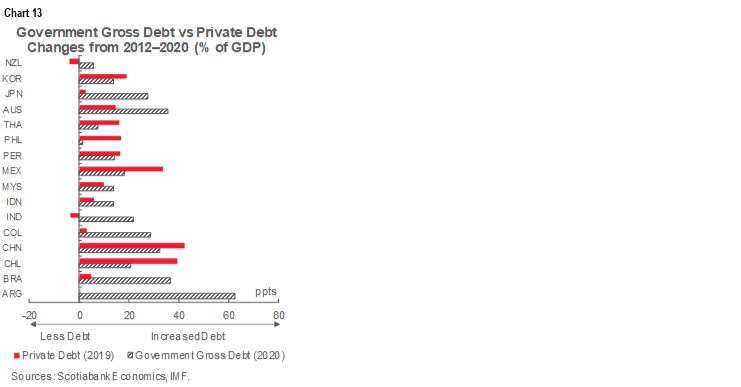

That EMs may be more vulnerable to capital withdrawal and higher return expectations is partly indicated by chart 13 that shows how much their private and government debt has risen since the eve of the 2013 tantrum to the eve of the pandemic. The figures go up to just before the pandemic on a comparable basis, but the imbalances have hardly lightened during the pandemic. Said debt has to be rolled over and refinanced at higher flows than in 2013.

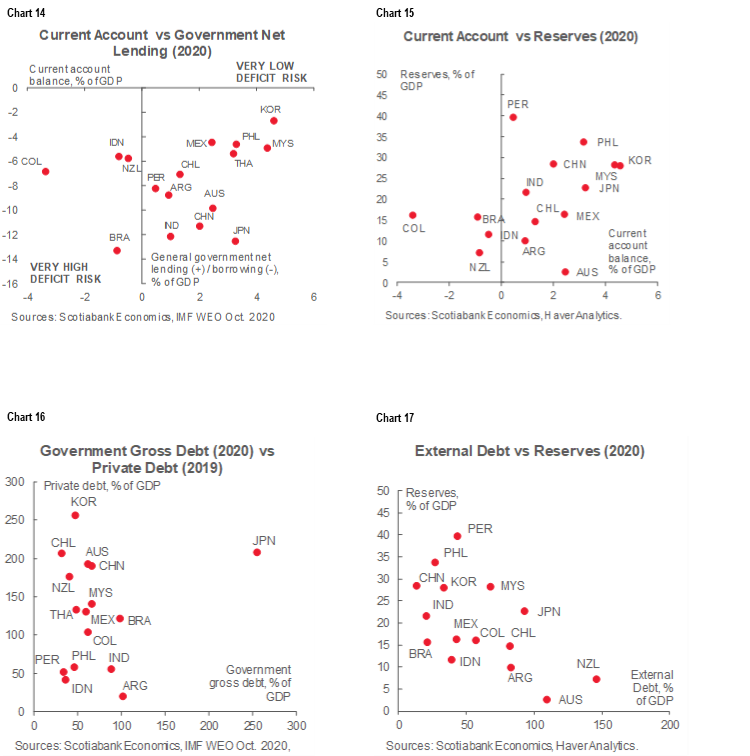

The importance of not treating EM as a broad asset class rather than dissecting prospects on a differentiated basis is nevertheless illustrated by charts 14–17 that depict the vast differences in measures like external debt, reserves and current account balances. Fed tapering that pulled back the security blanket on EMs set in motion a round of challenges by unveiling what lurked beneath and therefore served as the catalyst to broader challenges.

Does any of this mean the Fed shouldn’t withdraw stimulus because of EM concerns? Probably not which I’ve long argued. The Fed’s mandate is geared to the domestic economy albeit in consideration of foreign feedback effects. You could give all the time in the world to EMs to prepare for a smaller Fed security blanket and many probably wouldn’t.

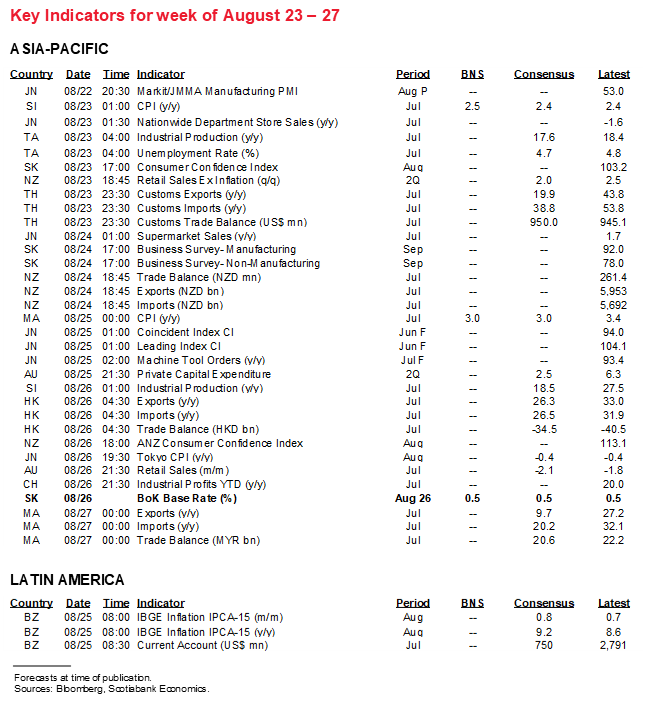

PMIS—DELTA TO TEST GLOBAL RESILIENCE

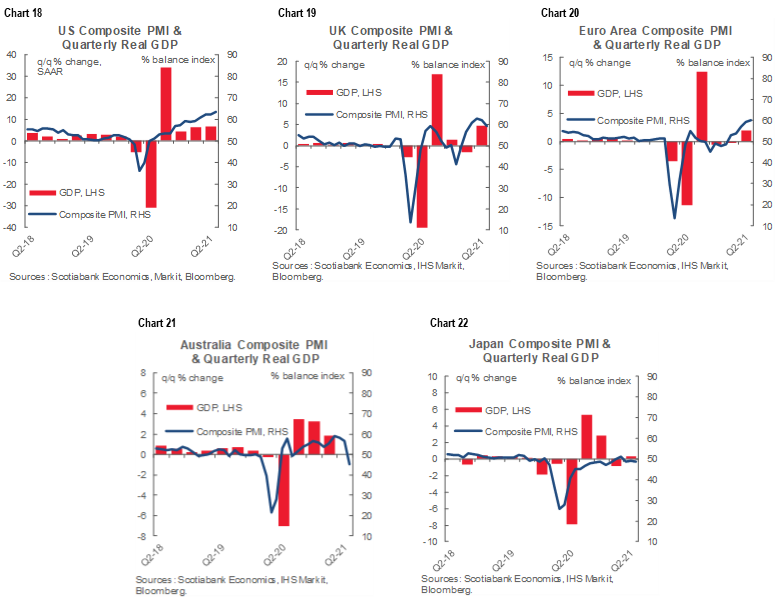

It’s time for another round of monthly updates of global purchasing managers’ indices. They serve as rough leading proxies for the direction of risks to GDP growth.

All of them arrive on Monday across their respective time zones. US (Markit, not ISM), Eurozone, UK, Australia and Japan are all on the docket. Charts 18–22 shows recent trends. The rise of the Delta variant may test resilience in areas like the US, Eurozone and UK while Australia and Japan are likely to continue to be very weak.

THE REST—US PARENTS GETTING A 4TH ‘STIMULUS CHEQUE’

US markets will digest a round of consumer and housing updates as the dominant factor on the rest of the global macro release calendar.

Where I’m off consensus the most is on Friday’s US income growth figures for July. I think consensus either forgot about or is unaware of the changes to the child tax credit that took effect in July (here). That will be like a fourth stimulus cheque but this time exclusively for parents of kids 17 and under. Combined with a bottom-up components approach to estimating incomes that also considers higher wages and salaries we should be looking at an income gain over 1% m/m and possibly quite a bit over 1%. 80% of recipients would have received the amounts through direct deposit on July 15th with the remainder getting a cheque in the mail around the same time. That is likely to add to the mountain of cash sitting on top of US household balance sheets that has rapidly risen by about US$3 trillion through the pandemic and not least of which because households are still catching up to recognizing the manna from heaven (chart 23). Not much of that disbursement was probably spent since the amounts arrived in the second half of the month and given recognition lags and so the drop in retail sales during July may be offset by a gain in services spending to net out to a small gain in the total consumption numbers.

US markets will also face the Fed’s preferred inflation gauges for July on Friday. Little change in year-over-year rates is expected for headline and core PCE inflation given what we already know about CPI. Existing home sales (Monday) could get a lagging lift from earlier gains in pending home sales while new home sales (Tuesday) could rebound from the prior month’s drop, but model home foot traffic continues to decline. Wednesday’s durable good orders face downside risk through autos but will shoot for a fifth straight monthly gain in capital goods orders ex-defence and air. Thursday’s first revision to Q2 GDP growth of 6 ½% is expected to be little changed.

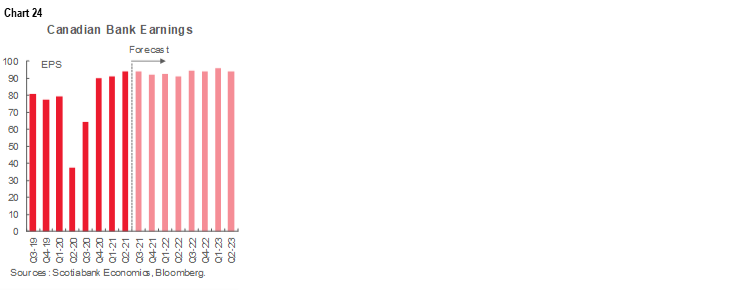

Canada’s calendar goes relatively quiet with no releases or major events on tap. Election watching will have Canada observers monitoring polls as poll composites (see front cover chart) underweight more recent polls that are showing Liberals and Conservatives as neck and neck in terms of the share of the popular vote. Otherwise, bank earnings for fiscal Q3 will dominate following the strong rebound to date and given analysts’ consensus future estimates (chart 24). Bank of Nova Scotia (my employer) kicks it off on Tuesday before the market open. BMO follows that morning, followed by RBC and National the next day and then CIBC, TD and Canadian Western Bank on Thursday.

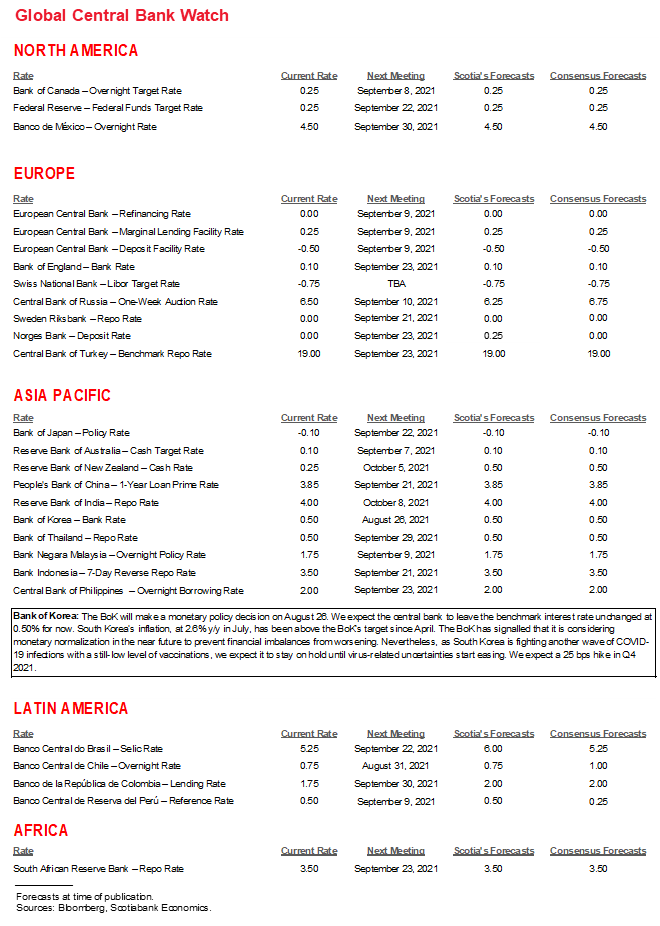

The only central bank on tap will be the Bank of Korea’s decision on Thursday. Consensus is split on this call with a slight majority expecting the 7-day repo rate to be unchanged at 0.5% and just under half of consensus expecting a hike of 25bps. With the Delta variant on the rise we could see another central bank hesitate to pulling the trigger but accompany that with hawkish forward guidance.

LatAm markets face a quiet calendar with just mid-month inflation estimates for Brazil (Wednesday) and Mexico (Tuesday) to go along with Banxico meeting minutes on Thursday.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.