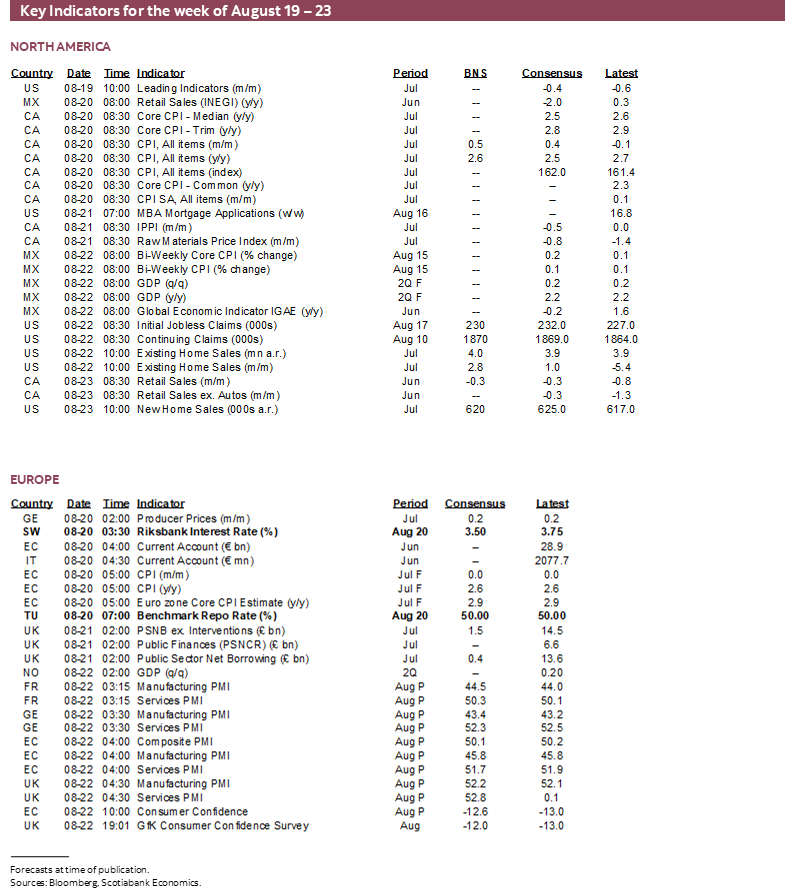

Next Week's Risk Dashboard

- Powell to reaffirm September cut pricing…

- …but subsequent market pricing may be too dovish

- Harris riding a DNC peak on light policy substance

- Canadian core CPI to inform reaccelerating trend

- Canada on nationwide rail strike watch

- Global PMIs on tap

- Canadian data focused on retail sales

- US data focused on housing softness

- ECB watchers focused on wage report

- Sweden’s Riksbank to deliver a second rate cut

- Turkey’s central bank to hold

- BoK, BI and BoT expected to hold

- Chinese lending rates expected to be unchanged

- A pair of LatAm GDP updates

- Other potential Jackson Hold speakers and interviews

Chart of the Week

POWELL MAY NOT BE DOVISH ENOUGH FOR MARKETS

This is a truncated version of the Global Week Ahead given that I was on vacation. It will highlight expected developments by region sans any special topics.

US—POWELL’S SPEECH TO BE KEY

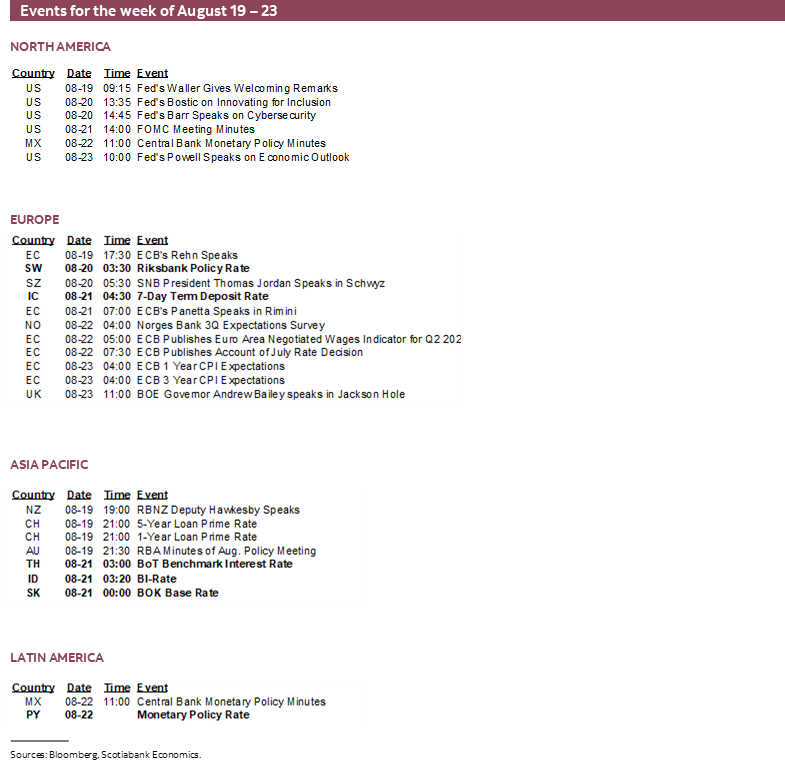

The Kansas City Federal Reserve’s annual Jackson Hole Economic Policy Symposium will stand out as the week’s major focal point. This year’s theme is “Reassessing the Effectiveness and Transmission of Monetary Policy.” The agenda, including the full list of presenters, will be released on Thursday evening and then two days of presentations will unfold. We’ll receive a fuller list of attendees over the week. Also watch for customary interviews from various global officials from the sidelines throughout this week.

Powell to Tee Up September but Fall Short of Market Pricing Thereafter

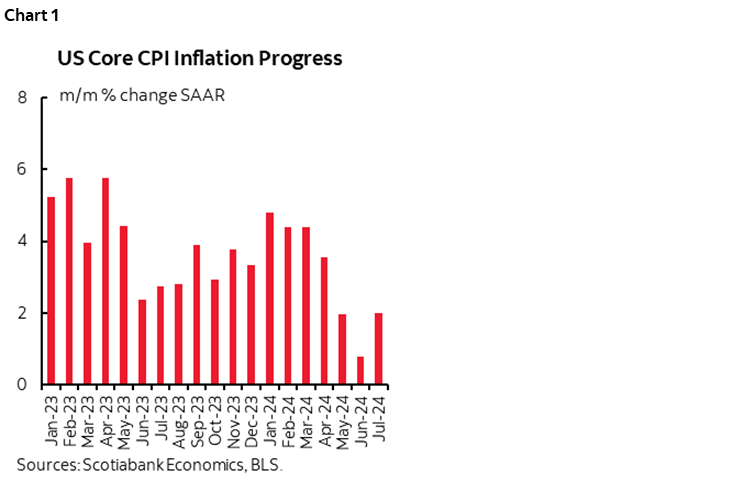

Chair Powell delivers the main event at JH when he speaks on the economic outlook on Friday at 10amET. After another dovish core CPI reading that met expectations and makes it three in a row (chart 1), I fully expect him to reaffirm market pricing for a quarter-point rate cut on September 18th possibly by invoking reference to how it will ‘soon’ be appropriate to begin easing. I don’t expect him to sound as—let alone more—dovish than what is generously priced by way of 100bps of cuts by year-end which seems like it’s overshooting. He’ll likely defer that part of forward guidance to the Committee’s refreshed September dot plot. He’ll likely signal that the Committee has ticked the box for having ‘greater confidence’ that inflation is under control. I don’t expect him to ring alarm bells on the labour market and instead expect him to reinforce references to ongoing rebalancing away from excess demand for labour while being prepared to act if the job market further deteriorates. He’ll likely repeat references to the need to proceed gradually, balancing the risks of being too restrictive for too long against prematurely easing too rapidly in light of history’s cautions against doing so. Barring unforeseen shocks and severe market dysfunction, the message of the day is likely to hinge on one word: gradual.

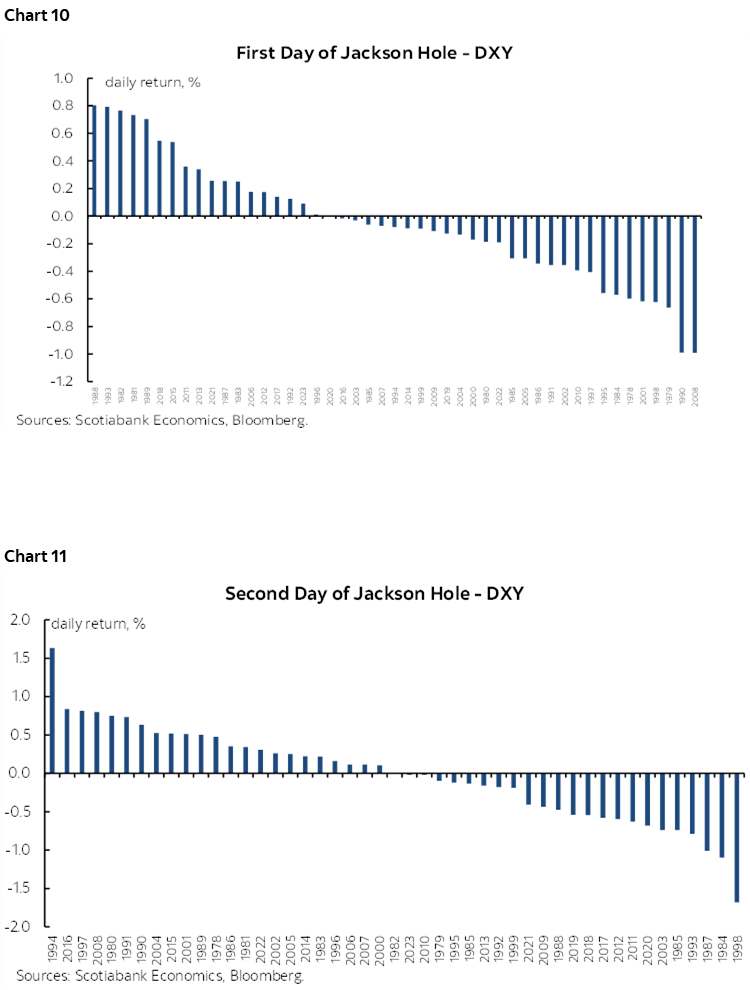

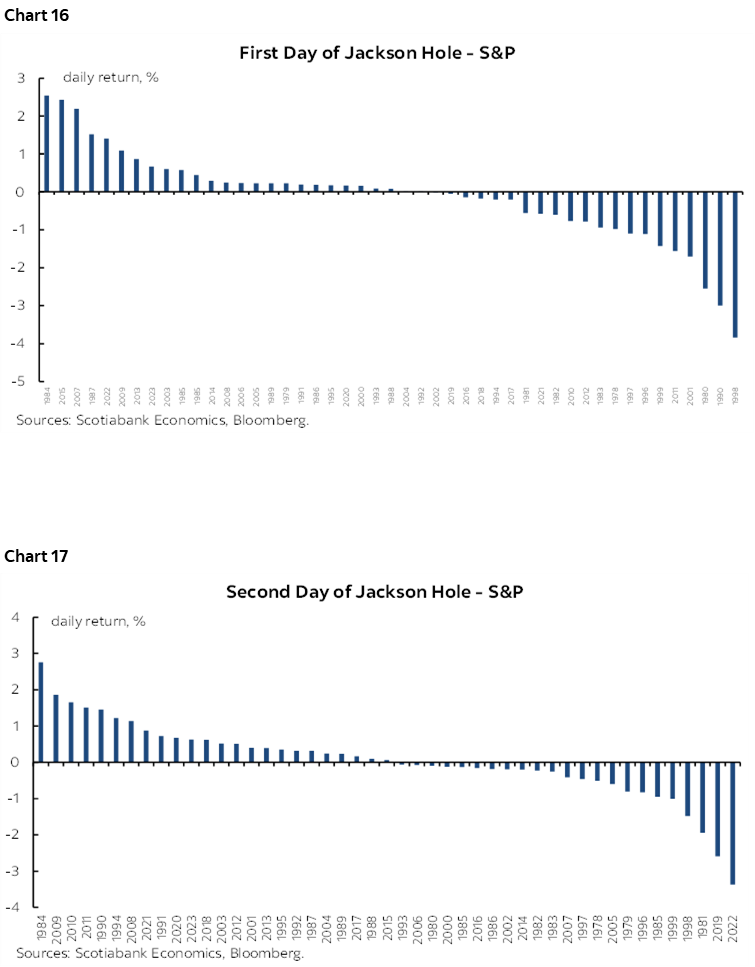

I’ve placed eight charts at the back of this publication that show the effects of Jackson Hole on various market metrics after the first full day of proceedings and also after the second day that spills over into Monday following the symposium’s conclusion over the weekend. In general, there are more small rather than big moves outside of key turning points and it may be difficult for Powell to make this year’s symposium as impactful as some of the ones that have really moved markets in the past.

Could a DNC Peak Follow the RNC Peak?

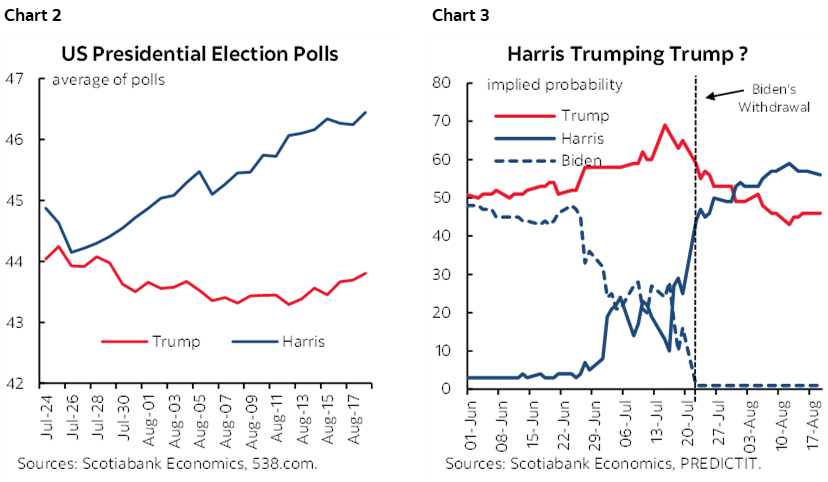

With Trump’s election chances slipping away (charts 2, 3), the focus shifts to the Democratic National Convention (DNC) that commences tonight through to Thursday in Chicago. So what. The Harris and Walz ticket is already set. The list of speakers reads like a list of relics from the party’s past including both Clintons and both Obamas. We may get further details on the policy platform after parts of it have been shared in bits and pieces.

Her plans are not terribly inspiring thus far. Harris plans to build three million more homes which feels like it takes a page from the Trudeau administration’s plan north of the border which itself is laughably unachievable. Her threats against price gouging please the left wing but is just soap box politics and bad economics, yet her openness to capping prices and raising wage floors flunks Econ 101. Exempting taxes on tips is silly, unfair to folks who pay their taxes regardless of the source of income, distorting, but generally small potatoes from a fiscal deficit standpoint. Her plan to raise the Federal minimum wage is costly and keeps the pressure on inflation risk. Expanding child tax credits to US$6k/child is costly with probably very little effect on birth rates. Harris is under little pressure to reveal a broader platform because she’s currently riding on momentum effects. I remain of the opinion that her chameleon ways remain very much oriented toward a highly interventionist, big government policy bias while her stance on trade is biased toward protectionist environmental and labour distortions.

Light US Data Focused on Housing, PMIs

US data risk will be light and follows the release of minutes to the July FOMC meeting on Wednesday. The annual benchmark revisions to nonfarm payrolls may attract fleeting attention on Wednesday. S&P PMIs for August (Thursday) will be part of a global wave of PMI updates. Existing (Thursday) and new (Friday) home sales will be updated and may stabilize against a weakening trend.

CANADA—CPI IN FOCUS, ON STRIKE WATCH

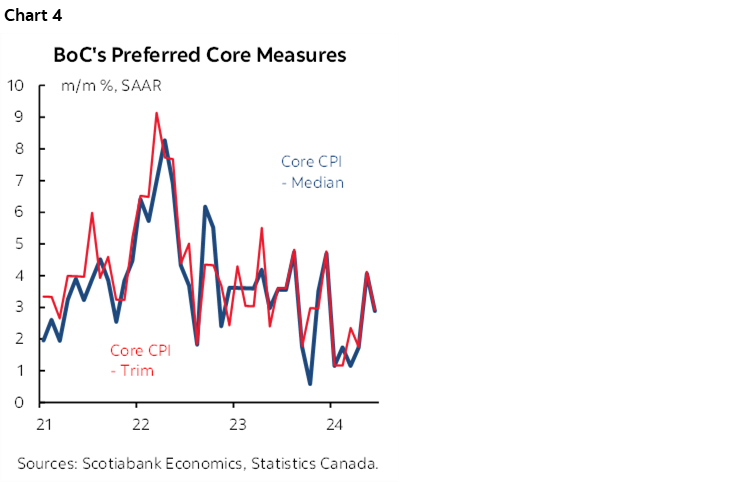

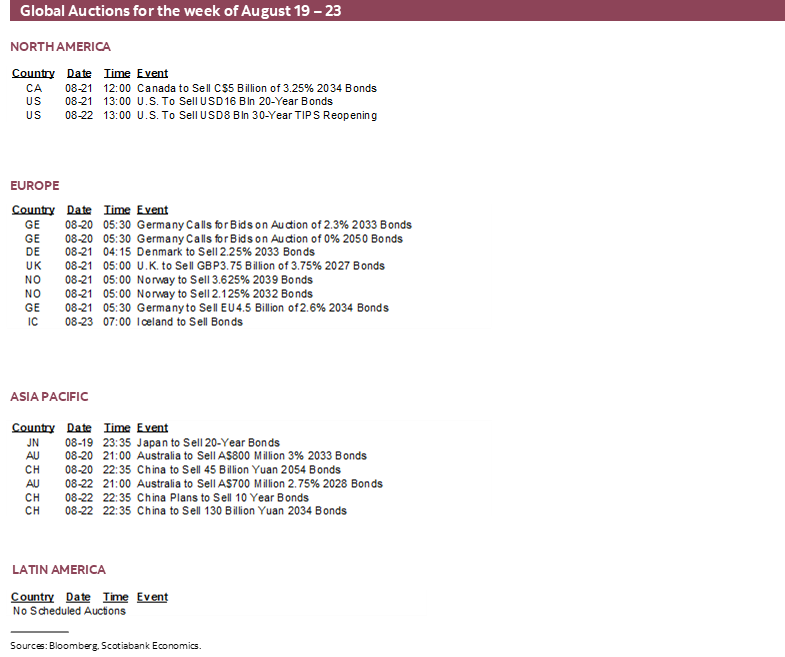

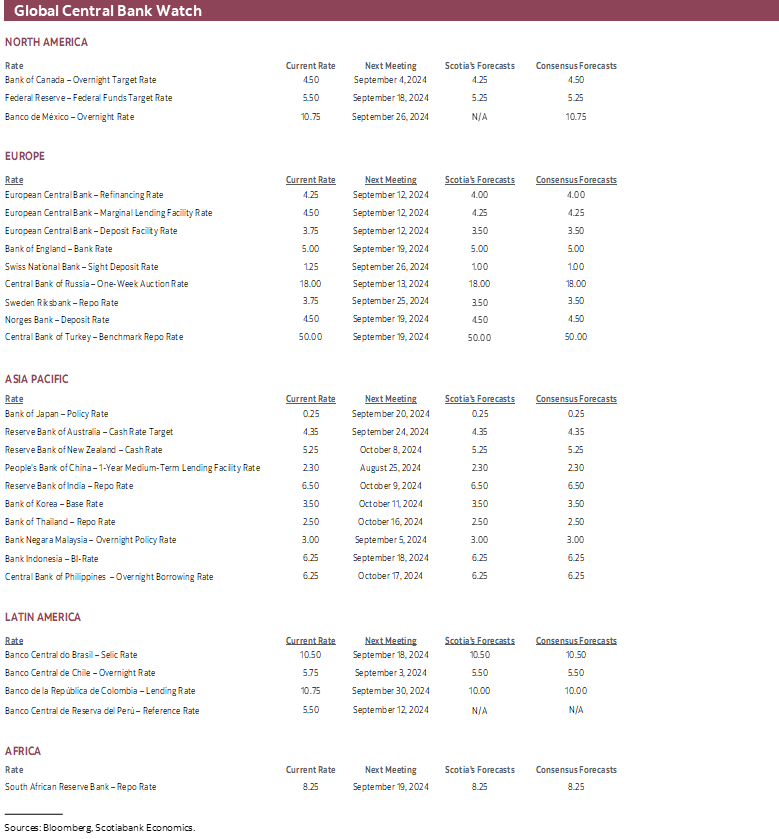

Canada updates CPI for July on Tuesday. I’ve estimated a 0.5% m/m NSA rise and slight downtick to 2.6% y/y. However, after two months of reacceleration (chart 4), the key will be whether a third month of upside pressure in m/m SAAR measures of trimmed mean and weighted median CPI occurs. That is impossible to estimate in advance given the limited data and high sensitivity of the readings to the distribution of price changes. The reading probably matters little to the BoC that appears intent on delivering meaningful easing before potentially reassessing.

It’s unclear whether BoC officials will attend Jackson Hole and in what capacity.

Canada is on strike-watch. Again. The country has been crippled by large scale and widespread strikes in the private and public sectors since the Spring of 2023 and this week could amplify the risks to economic indicators once again. Watch for further developments on the path toward what appears to be likely strikes at CN and CP rail this week unless some last minute arrangement can be struck.

A pair of retail sales estimates arrive on Friday just before Powell speaks which means they’ll capture only a few minutes of market attention if that. Statcan provided earlier guidance that June’s nominal sales were down -0.3% m/m SA, but this estimate is typically subject to high revision risk and was based on only half of the available survey sample. More important will be details for June like volumes, plus advance guidance for July’s tracking.

The BoC is supposed to refresh its Senior Loan Officer Survey including measures of credit tightening on Monday but it seems to be delayed.

EUROPE—ECB’S WAGES TO INFORM ECB POLICY PRICING

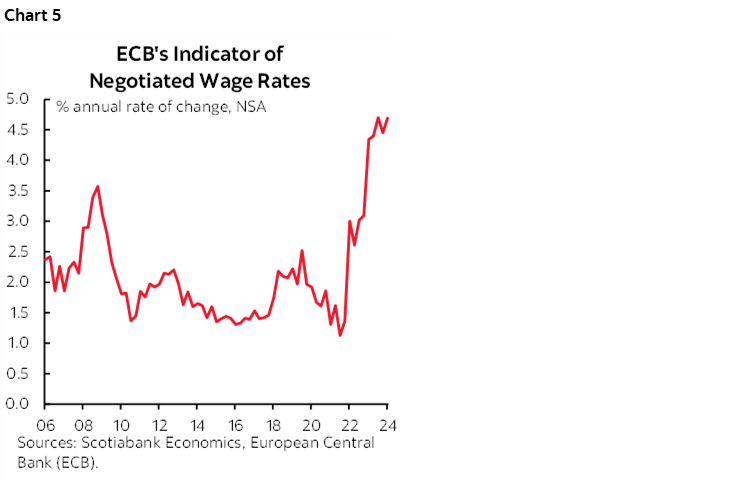

Markets are priced for another ECB rate cut on September 12th and gradual further easing that may be informed by Thursday’s release of negotiated wages for Q2 in light of the ongoing hot trend (chart 5).

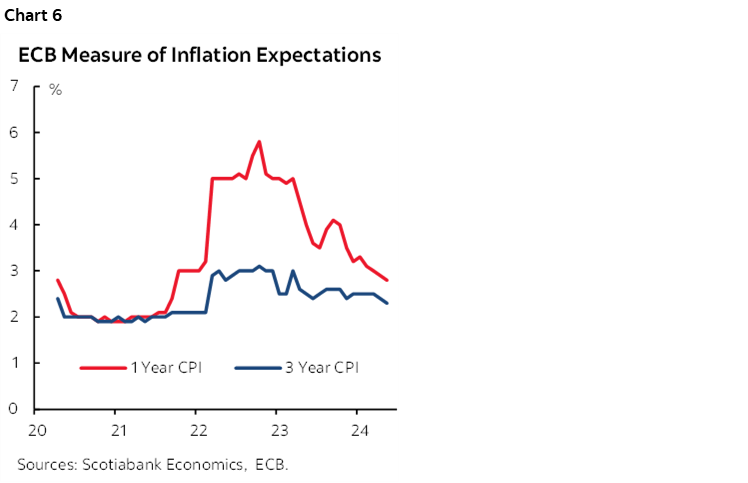

The ECB’s measures of 1- and 3-year inflation expectations in July will likely remain averaging around 2½% when we get the figures on Friday (chart 6).

BoE Governor Bailey speaks at Jackson Hole on Friday at 11amET and hence right after Powell.

Eurozone and UK PMIs for August will be refreshed on Thursday as part of the week’s global wave of PMI updates that will inform growth tracking, supply chain developments and price pressures (charts 7, 8).

Sweden’s Riksbank is expected to deliver its second rate cut of the cycle tomorrow after the first cut in May. That will bring the policy rate down to 3.5%.

Turkey’s central bank is expected to extend its policy rate hold at 50% tomorrow.

ASIA-PACIFIC—A TRIO OF CENTRAL BANK DECISIONS

Three central bank decisions will pair up with refreshed PMIs to dominate local market risk beyond spillover effects of global developments such as the Fed’s symposium.

China’s 1- and 5-year Loan Prime Rates are expected to remain unchanged tonight.

Each of the Bank of Thailand (Wednesday), Bank Indonesia (Wednesday) and Bank of Korea (Thursday) are expected to remain on hold. In addition to domestic developments, each central bank may wish to hear what Powell has to say and to observe the market reactions particularly in terms of FX.

PMIs will be updated by Australia (Wednesday), India (Thursday) and Japan (Thursday). Japan also updates its national CPI measure on Thursday that tends to reveal little beyond the already known soft m/m SA Tokyo measure (chart 9) and hence should pose little risk to carry trade pricing.

LATIN AMERICA—GDP UPDATES AND FED-WATCHING

Spillover market effects from the Fed’s retreat and light local data will dominate.

Chilean Q2 GDP landed at –0.6% q/q SA on Monday morning and in line with expectations but with a mild upward revision to 2.1% q/q SA for Q1 (from 1.9%). Peru’s Q2 GDP report (Friday) is expected to further accelerate to over 3% y/y.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.