Next Week's Risk Dashboard

- Fed’s Jackson Hole symposium to be the focal point

- Powell’s keynote — why he’s more likely to dig in than acquiesce

- Powell could skirt by near-term references…

- …and focus more on the medium-term and the framework review

- Multiple key central bankers will attend Jackson Hole

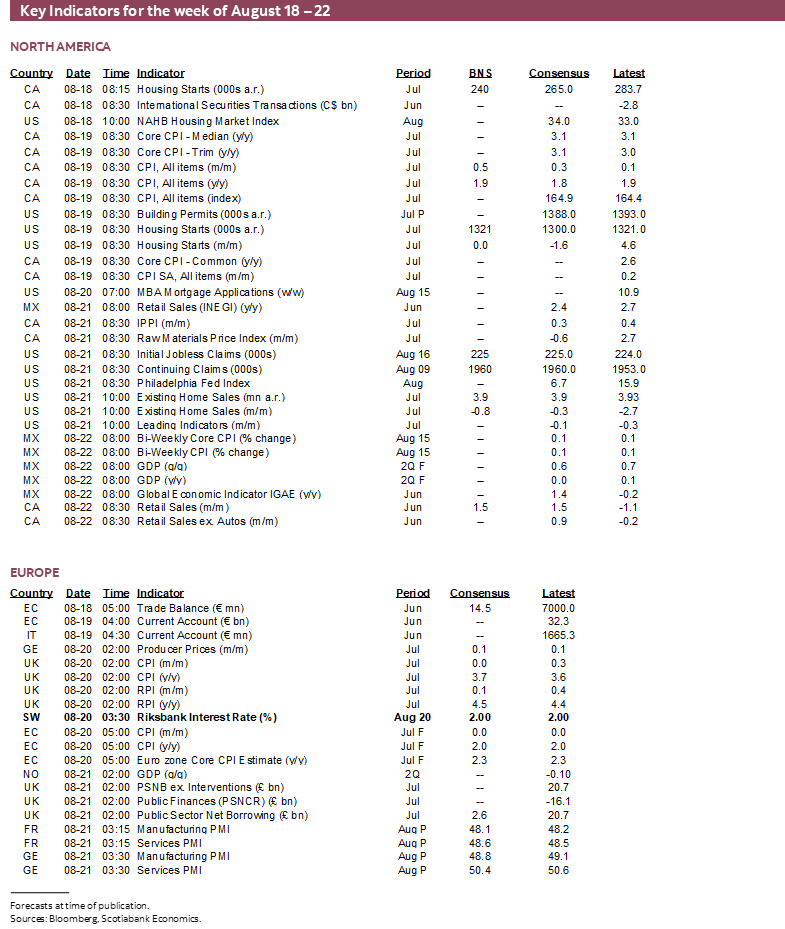

- Canadian CPI is one of two readings before the next BoC decision

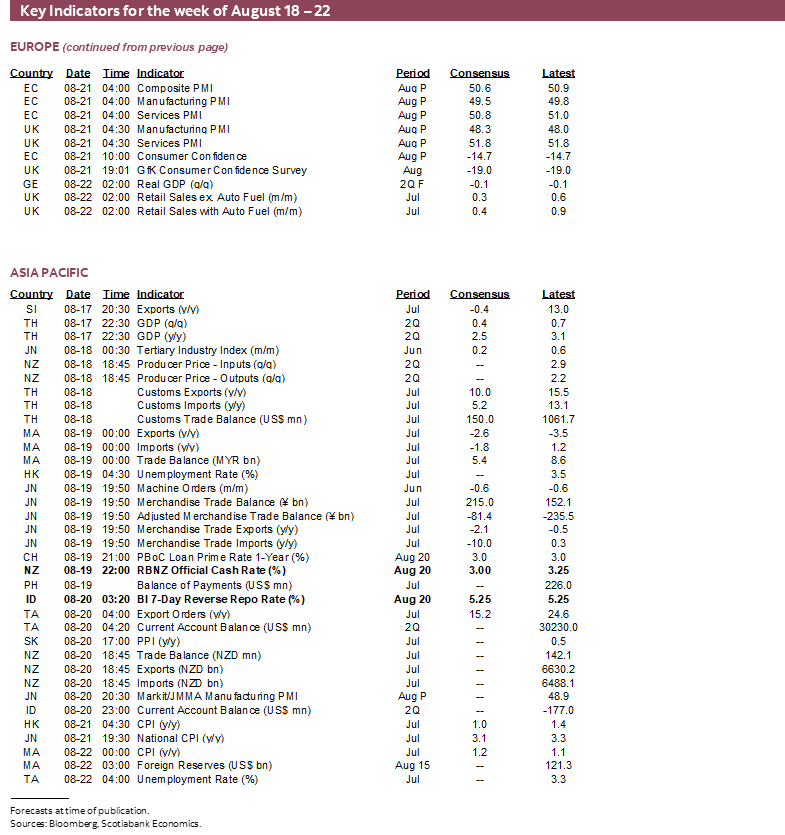

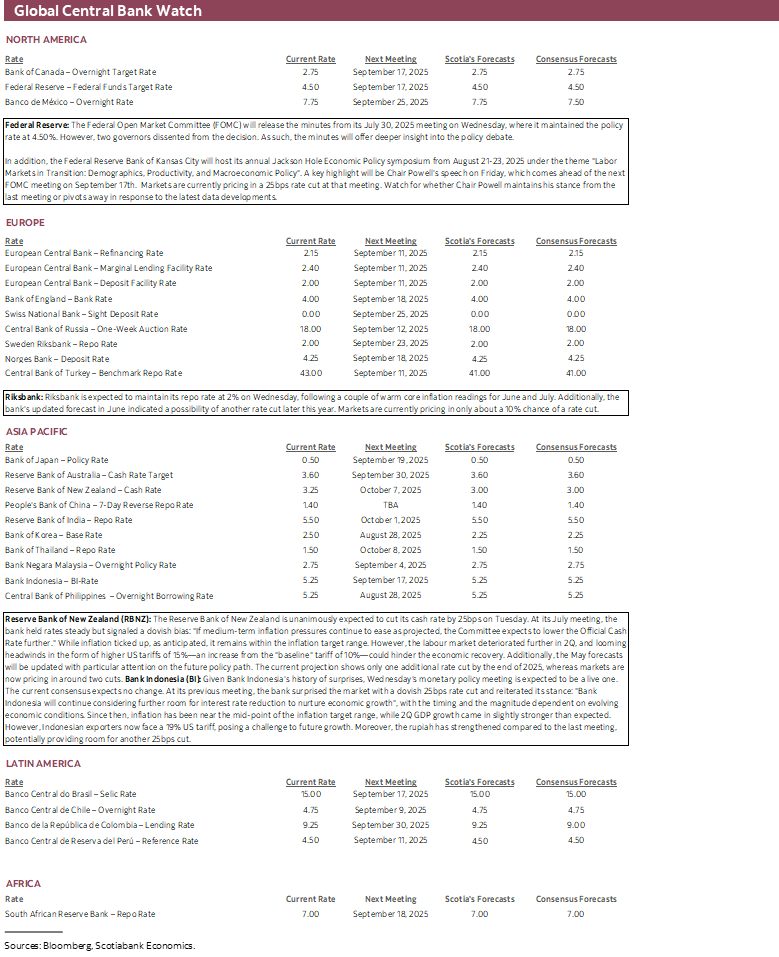

- RBNZ expected to cut

- Riksbank, BI expected to hold

- UK CPI: services still running too hot for further easing?

- Japanese core inflation expected to remain firm

Chart of the Week

This could be a seminal week for Fed watchers. As the dog days of August pass on, other developments will pale by comparison.

JACKSON HOLE—LOFTY EXPECTATIONS

The Federal Reserve’s annual Jackson Hole symposium will be held this week. It starts with interviews from the sidelines as officials arrive. The formal agenda will be released on Thursday evening. The key event will be Chair Powell’s speech on the economic outlook and framework review on Friday morning at 10amET. Multiple top central bankers will be in attendance. BoC Governor Macklem will be there, but it’s not clear whether he’s speaking. BoE Governor Bailey and ECB President Lagarde will speak on the same panel on Saturday. BoJ Governor Ueda may attend but is not confirmed at the time of writing. I’m sure the list will expand.

The official focus this year is on “Labour Markets in Transition: Demographics, Productivity, and Macroeconomic Policy.” Yawn. The unofficial focus across financial markets will be whether Powell pivots, or digs in on an extended pause against market pricing for cuts starting in September. I doubt he will speak directly to September in what is typically a short speech sans Q&A that is focused upon the broader path ahead. He may focus heavily on the promised conclusions of the framework review that Powell has said would be finished by the end of summer and to be followed by addressing communications tools including the Summary of Economic Projections in the Fall.

If Powell weighs in on the near-term, a hint at September would perhaps employ terms like ‘soon’ or ‘somewhat soon’ in reference to an easing bias. I doubt he’s of that mindset and think that a September cut remains overpriced. A pivot would give traders’ itchy trigger fingers—that have been jonesing for a cut all year—their gotcha moment as an excuse to pile on more aggressive easing that the FOMC may not be comfortable courting at this time. The Fed has not won the last inflation battle given recent PPI and CPI readings and the requirement to have much more data given factors like residual seasonality and sampling deficiencies. Job growth has slowed of late, but is not that far below sharply lower payroll breakeven rates in light of tighter immigration policy. Confidence in where the balance between upside risks to inflation and downside risks to job markets may reside remains unsettled and awaiting much more evidence. The issue of how tariffs, immigration changes, and broader macroeconomic policies may impact inflation remains at a highly nascent stage. Policy is not materially restrictive. The economy remains resilient including consumer spending. To cut soon could make the Fed look thoroughly politicized given the heat from Trump. Financial conditions are broadly stimulative. We’ve seen plenty of times when two, three, or even four Governors have dissented. The moral hazard issue is that material easing could embolden more unwise policies like protectionism.

CANADIAN INFLATION—SEPTEMBER’S BANK OF CANADA DECISION WON’T HANG ON JUST THIS READING

Canada refreshes inflation tracking with the July CPI report due on Tuesday. It’s one of two CPI readings before the next BoC decision on September 17th with the next one arriving the day before such that not much rests on just this one reading. My estimate is for a 0.5% m/m seasonally unadjusted rise in headline CPI based on limited observables such as gas prices, seasonal influences, and some housing and food price tracking. What will matter, however, is what will happen to the average of the two preferred core inflation readings used by the BoC that have remained hot and are impossible to estimate in m/m SAAR terms. They have averaged 3.4% m/m SAAR over the past three months. Service price inflation has been trending warmly, the breadth of price pressures has been rising, and key may be any early tariff effects on some goods prices both directly—through Canada’s limited retaliatory measures—and indirectly—through supply chain effects. The core measures exclude tariffs, but not the possible pass-through incidence effects.

GLOBAL CENTRAL BANKS—A CUT AND TWO HOLDS

Three regional central banks will weigh in with decisions this week. Most forecasters expect the RBNZ to cut by 25bps on Tuesday evening (10pmET), Sweden’s Riksbank to hold at 2% on Wednesday morning (3:30amET) and Bank Indonesia to hold at 5¼% with mild cut risk on Wednesday morning (3:20amET). See the accompanying Central Bank Watch table for a little more on each.

GLOBAL DATA—PMI DELUGE, JAPANESE AND UK CPI

PMIs start arriving with releases by Japan and Australia on Wednesday night (ET) followed by India, the Eurozone, UK and US on Thursday morning. Watch for potentially clearer indications of tariff effects on prices, orders, and hiring patterns.

UK CPI is expected to be soft at a seasonally-typical reading that is little changed in July. Core CPI has been too hot at 3.7% y/y and services have been leading the pressures at 4.8% y/y, thereby calling into question the need for any further easing by the Bank of England. Japanese CPI is expected to follow the deceleration in the already known Tokyo gauge that dipped beneath 3% y/y in July, but note that it was driven by commodities as CPI ex-food and energy was stuck at 3.1%.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.