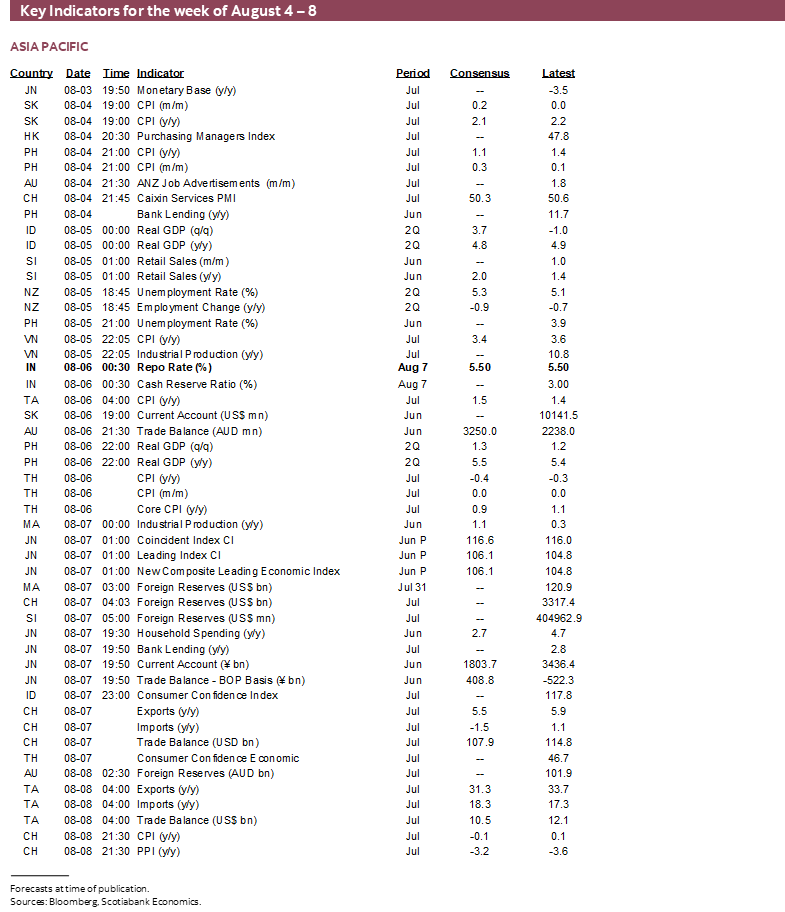

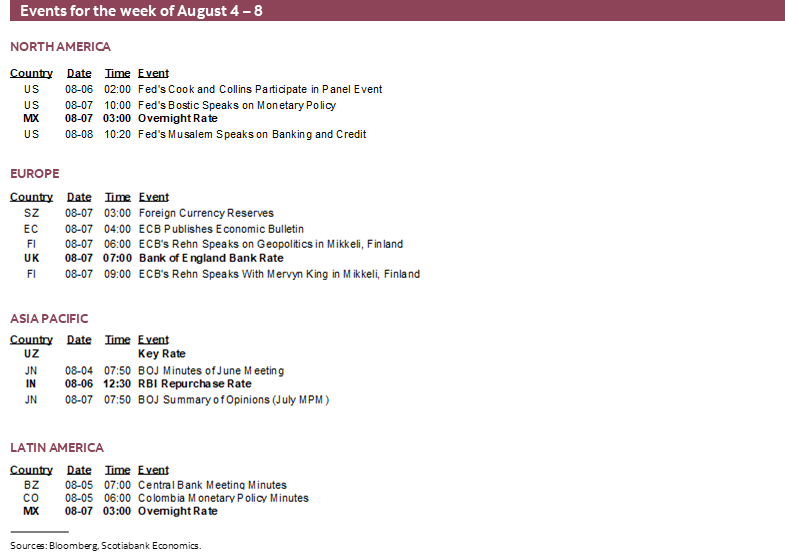

Next Week's Risk Dashboard

- Powell and moral hazard

- Tariffs put the US productivity miracle at risk

- Canada should dig in

- Are Canadian jobs still resilient?

- Firing the BLS head is a disturbing development

- Watch the rumour mill for Fed Governor candidates…

- …and no, Kugler did not disagree with Powell

- BoE to ease reluctantly

- Banxico likely to downshift

- RBI teed up a pause, then came Trump

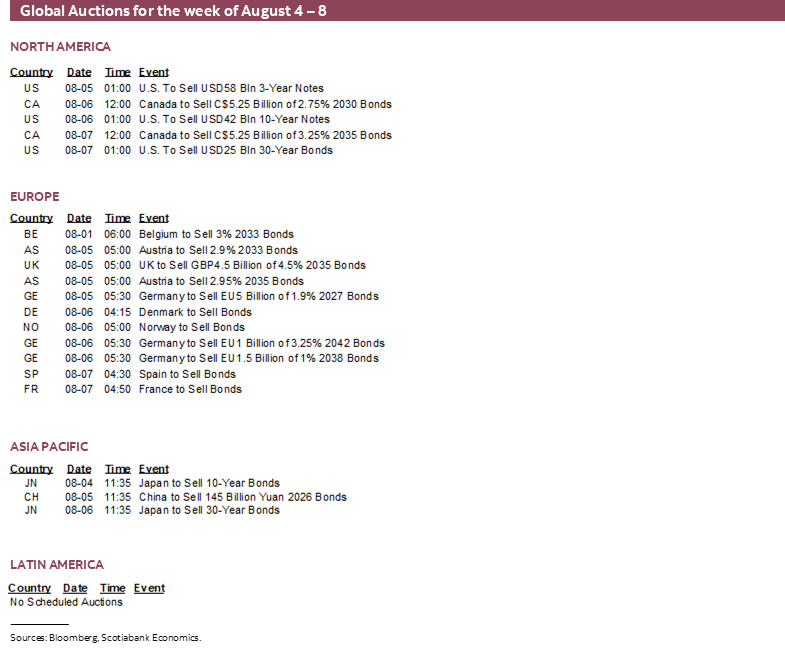

- A lighter global release schedule

- Canadian markets shut on Monday

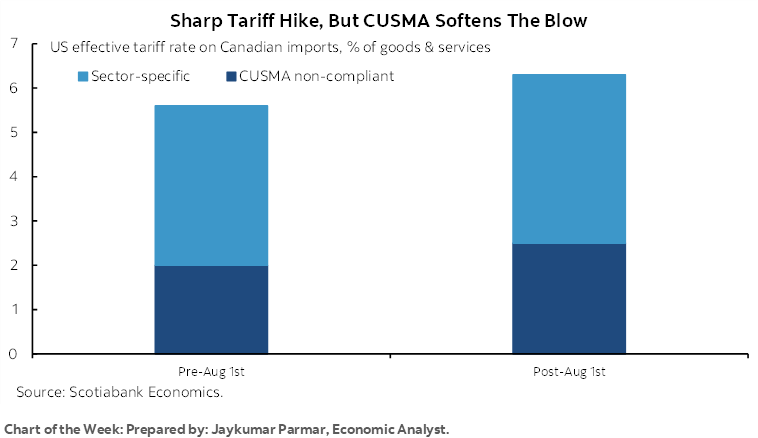

Chart of the Week

Perhaps the best hope for more sensible policies arrived at the end of this past week in a twisted sort of way but with the caution that the early signs are unfavourable. The possible market and policy aftermath may well be the biggest developments over the coming week and beyond in an otherwise relatively lighter calendar of global developments.

With the stroke of a virtual pen, three months of growth in US payrolls ground to a near halt (recap here). All’s not looking so good in Kansas, Dorothy. Including revisions, payrolls are now reported to have been up by only 19k in May, 14k in June and 73k in July. Even at lower required rates of employment growth amid tighter immigration policy those are weak numbers notwithstanding data quality issues.

Unhelpful Initial Signs

Admittedly, Trump’s first responses to the poor data were not encouraging. First, he blamed Fed Chair Powell, despite the fact it’s not US monetary policy that rapidly soured in recent months as opposed to the broader policy framework that drove a massive increase in uncertainty indices.

Second, after announcing he was moving nuclear submarines toward Russia, Trump announced he is firing the Commissioner of the Bureau of Labour Statistics. She heads the whole Bureau that produces not only the job numbers but also the price statistics (here) and her firing is despite her strong credentials (here). This is a very bad outcome for faith in US markets. Markets will question the credibility and politicization of her interim successor (here) and the ultimate successor and have doubts over his/her willingness to produce data on job markets and inflation statistics that the administration may not welcome. McEntarfer may have a strong legal case should it prove difficult to prove malfeasance or incompetence especially in light of budget cuts. There may be knock-on effects on the rest of the BLS staff. A step like this is usually unwelcomed by markets when it happens elsewhere and perhaps especially so in the US where data and institutional strengths have to date underpinned faith in markets.

A Silver Lining to Bad Data?

Markets pounced on weak jobs as evidence of a US economy that is losing its lustre. Stocks were already weakening before payrolls and in response to Trump’s latest tariff announcements (here) and summarized here while noting that the headline hit of 35% against Canada is in reality a small fraction of that.

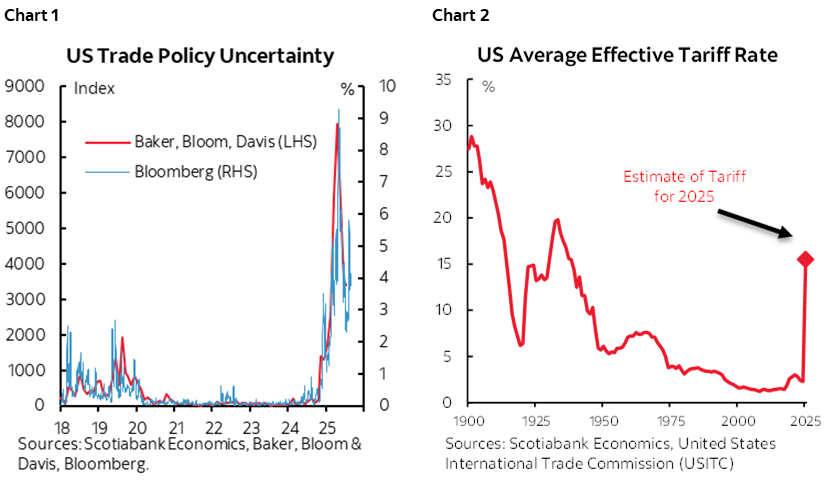

You could quip that only a practitioner of the dismal science would celebrate. Tut tut, that wouldn’t be very kind of you. What is to celebrate is that we may finally be seeing evidence in data and markets of the cost of trade policy uncertainty (chart 1), deepened US protectionism that is placing about a 15% tax (chart 2) on American shareholders, employers and consumers, DOGE cuts, sharply curtailed and frankly cruel immigration policy (here), and fiscal policy that for the most part merely extends previously existing tax policies and adds to bond issuance.

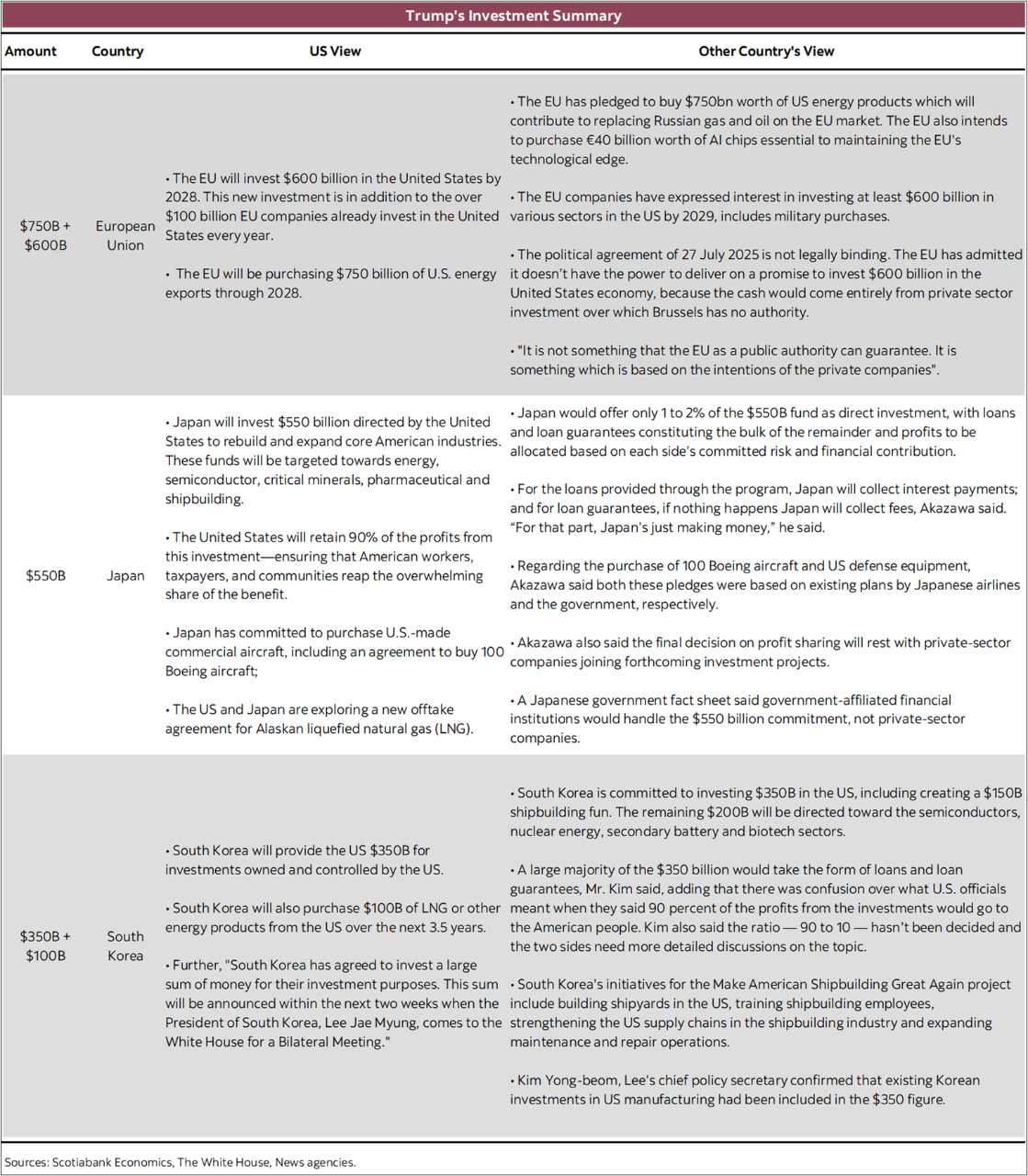

The rest of the world no longer faces much of any pressing need to retaliate against American protectionism and incur greater damage to their own countries in so doing. This is no longer, say, just a Canada-US fight with Canada fighting false claims being made against it. The ROW just needs to sit back, continue to offer immaterial changes in market access to US companies that already had very high access in many of the key markets, offer hollow investment promises (see summary table of the deals prepared by my colleague Jay Parmar) and watch America import the damage of its own policies. If those investments are actually real and achieved, then they would increase the US capital account surplus and—given the need for balance in the balance of payments—raise the current account deficit even further.'

Evidence of such damage is starting to appear. It is happening at an inopportune moment with midterm campaigning likely to intensify later this year into next just as further effects of the administration’s policies are likely to unfold.

Productivity ‘Miracle’ at Risk

Throughout it all, I hope we don’t wind up mourning the loss of America’s productivity miracle as perhaps the biggest casualty. Not today. Not tomorrow. Perhaps not for a while. As America builds a tariff wall around itself, the effects are likely to discourage long-run investment which is the exact opposite of what President Trump claims.

There is empirical support for this view. This piece, for example, argues that the period Trump romanticizes about because of its use of tariffs paid a steep price. A coddled domestic manufacturing base that was protected against foreign competition resulted in more business establishments, more hiring and higher gross output, but it achieved this at great cost.

For one, the evidence shows that these policies also raised inflation. Further, higher output and more businesses and employees were achieved with much less efficiency. The result was a reduced average size of business establishments operating at lower economies of scale in a more protected market, and reduced labour productivity because of the “entry of smaller, less productive domestic firms” to which you might add less competitive zeal applied by larger ones behind tariff walls. At the end of the day, the most important driver of a nation’s longer-run living standards is productivity growth which drives inflation-adjusted wages over time. American industrial competitiveness could suffer relative to other countries pursuing alternate policies.

There is a more constructive path away from this outcome. It requires de-escalation by the US administration. A repeat of 2018 when Trump ultimately abandoned the unelected folks in his administration who were giving him bad advice and pivoted rapidly. Midterms are coming, and turning around a US$30 trillion economy takes time; not acting soon enough puts a lot of GOP jobs on the line come November 7th 2026.

How Other Countries—and the Fed—Should Respond

What are other actors to do while we assess the Trump administration’s next moves? I’ll focus on two.

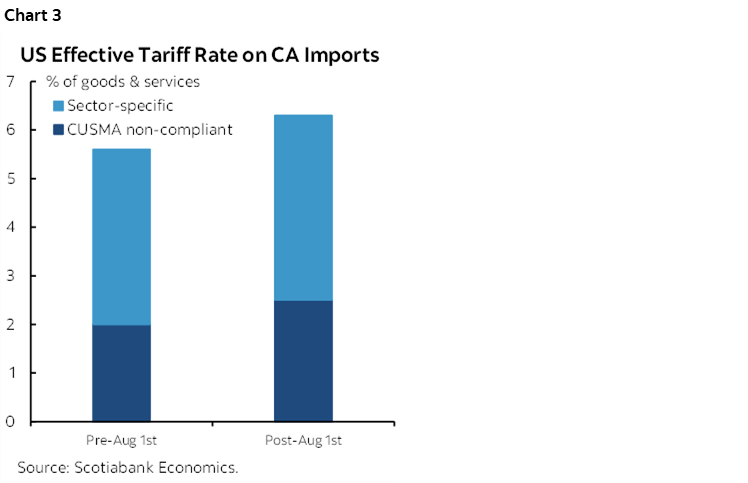

Canada is wise to dig in. Very possibly wiser than the Europeans, the Japanese, and the Koreans. Let the costs of US policies boomerang back on the administration and avoid “signing” (quotes because there is never legal text) a bad deal that Canada could be stuck with for a long time even if at greater short-run expense than what is so far a relatively modest hit to Canada’s effective tariff rate especially outside of the specific sector tariffs especially on metals (chart 3). The sector-specific hits are more of an issue for supportive fiscal policy than monetary policy.

Chair Powell would be well advised to think more strategically than some of the most vocal and dovish dissenters on his Committee. Powell’s biggest fear should be leaving behind a legacy that history books would use to paint him as an enabler of US protectionism. Bad policy >> bad data >> bad market outcomes >> dovish Fed >> bad policy….rinse, repeat. The moral hazard issues to easing in response to flawed macroeconomic policies are at least as important considerations as the uncertainty surrounding how the dual mandate of full employment and price stability may be placed at odds in a stagflation scenario for the US economy while posing a deep quandary for the Fed.

And so perhaps ongoing trade negotiations will combine with the coming week’s decisions by three central banks (BoE, Banxico, RBI) and some key data like Canadian jobs, US ISM and multiple global inflation reports to keep it lively.

CANADIAN JOBS—STILL RESILIENT?

Canada releases a batch of job market figures for the month of July on Friday. I wouldn’t be surprised to see some give back on the prior month’s creation of 83k jobs but will give reasons for why it might be more resilient.

In fact, I’ve tentatively gone with another gain of 20k and a stable unemployment rate of 6.9%.

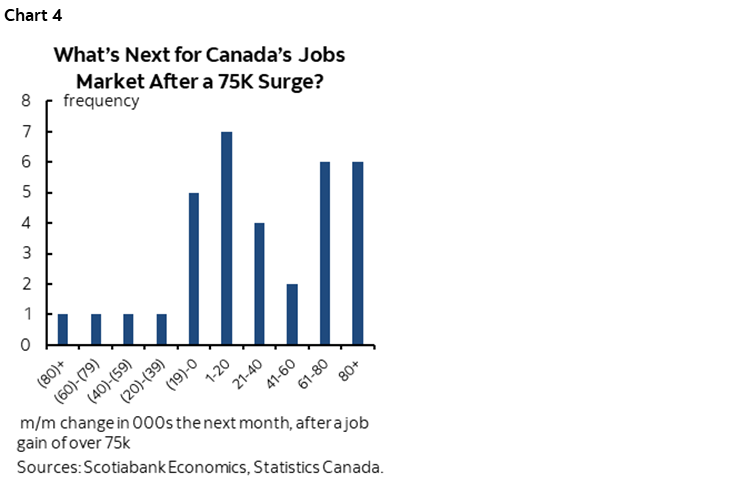

The high base effect represented by June’s 83k rise may be challenging in terms of the ability to post another up-month, but history isn’t onside with that concern. Since 1976, when the job gain has been over 75k in a particular month, the next month has been up again three-quarters of the time (chart 4). Why? Perhaps partly because of how Statcan rotates the local market samples which makes it slow moving and arguably invokes persistence. Each month’s survey rotates about one-sixth of the LFS sample out and replaces it with one-sixth of the sample size represented by new household respondents.

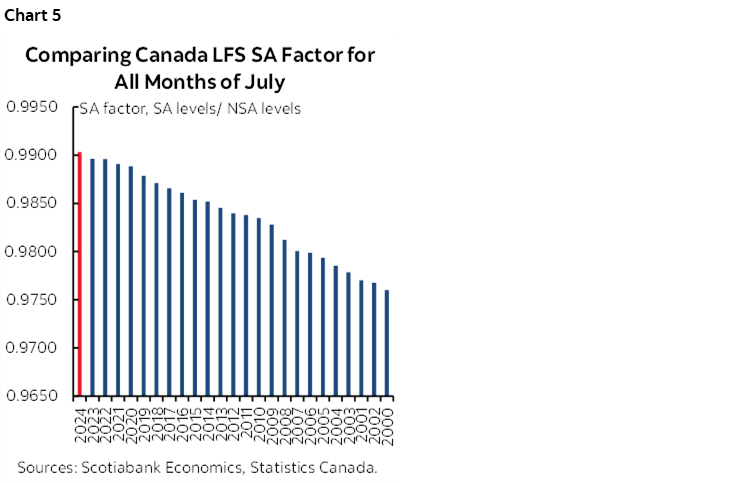

Further, there is a high bar set against expecting a material drop through the combined effects of possible seasonally unadjusted (NSA) changes in employment and the seasonal adjustment factor. If we get the same SA factor as last July that was on the high side as a pattern of recent years (chart 5), and the same record low NSA change as last July, then seasonally adjusted employment this time would be up by 42k. Put another way, there would have to be a new record amount of jobs lost in seasonally unadjusted fashion equal to -175k jobs lost NSA paired with last year’s July SA factor to get a flat jobs print.

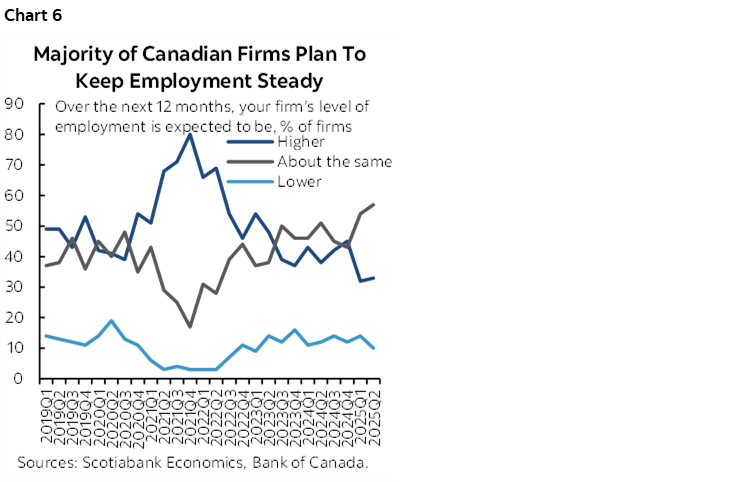

Among other possible influences are tariff effects which may be very sector-specific (eg. steel). Most firms in Canada continue to say they will look through tariff effects at least for some time while retaining staff (chart 6). At some point there may be civil service layoffs given federal program spending review that is being conducted, but that’s likely after a fall budget. The Federal government spends C$65B on employment costs per year for 358k workers. Weather effects might continue to be positive after relatively high hours lost due to weather in May and June. A home market substitution effect for travel and vacation spending could continue to buoy seasonal sectors. Wildfires may disrupt job markets in prairie provinces and northern Ontario, but Statcan estimates that only a small share of GDP (0.125%) is represented by the affected areas (here) and the affected share of the job market is likely within spitting distance of that estimate.

Hours worked will further inform GDP growth as Q3 starts after posting a mild 1.3% q/q SAAR gain in hours during Q2.

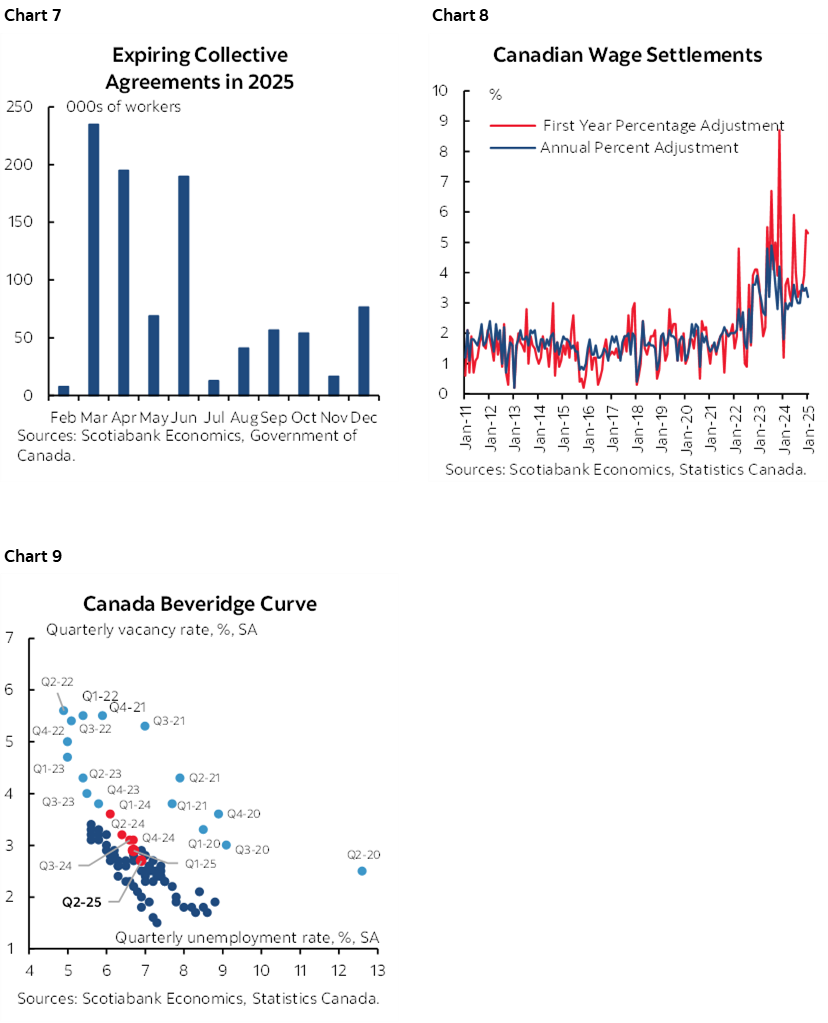

Wage growth has been erratic, but the number of workers on expiring collective bargaining arrangements this year and next (chart 7) paired with the pattern of wage gains being secured in deals (chart 8) may continue to drive resilient wage gains. That stands in contrast to a view that argues the labour market has become more balance with the unemployment rate and job vacay rate more aligned at lower levels than previously (chart 9).

Whatever the outcome, not much will hang on this one set of figures. The next Bank of Canada decision is on September 17th. There are two Labour Force Survey releases and two CPI releases due out before then, plus all manner of trade policy deadlines and possible fiscal policy trial balloons before a budget in early fall.

CENTRAL BANKS—RELUCTANT CUTTERS

Three central banks weigh in with decisions this week. One may continue to reluctantly ease. Another may slow its pace of easing. And another might extend a somewhat erratic pattern by sitting out this meeting.

Bank of England—Cautiously Less Restrictive

The Grand Old Lady of Threadneedle Street is widely expected to cut by 25bps on Thursday. Markets are priced for it, followed by a hold in September, and a decent shot at another cut in November. The BoE’s ‘gradual and careful’ mantra has been following an oscillating pattern of pauses and cuts that have offered the market predictability.

Bank Rate remains restrictive at 4.25% relative to neutral rate estimates (here), and the gradual approach probably makes sense given at least three considerations.

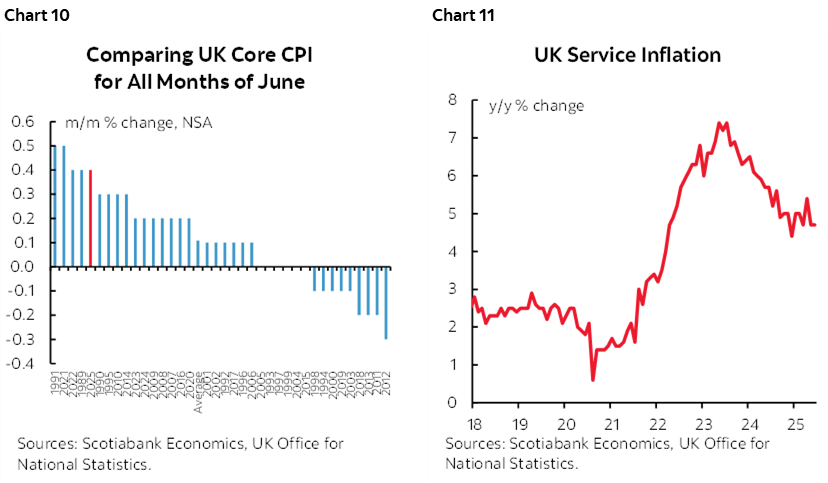

For one, two of the past three CPI readings have posted relatively hotter than seasonally unusual gains in core inflation including the latest one (chart 10). Service inflation remains particularly robust (chart 11).

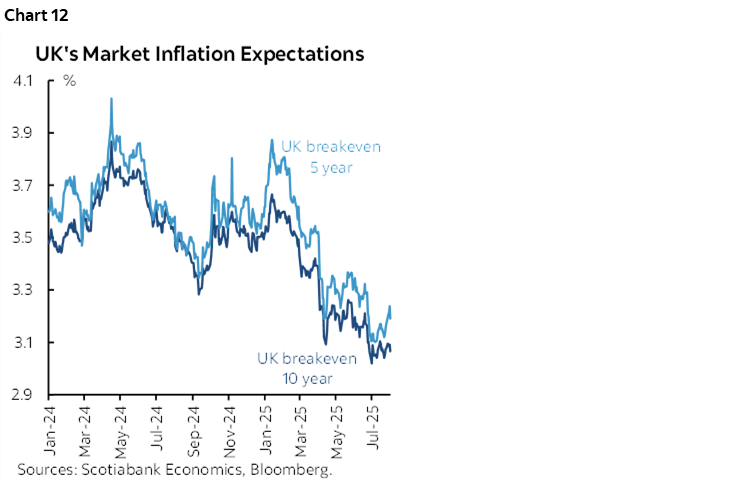

Second, inflation expectations remain relatively high; bond market measures show inflation expected to be over 3% across all horizons beyond one year (chart 12) and the GfK consumer confidence report has shown inflation expectations rising over the past year with uncertain effects from global supply chains and tariffs still ahead.

Third is the reality that the UK economy is not in great shape. GDP shrank in each of April and May. Industrial output has been falling for three months in a row and seven of the past nine. The service sector has performed a little better but shown signs of weakening over the past couple of months. And while aggregate employment has been supported by smaller businesses, the UK has lost about 186,000 payroll jobs since last July but total employment has been more resilient as off-payroll and principally smaller employers have held up.

As Governor Bailey recently put it, “we continue to use the words ‘gradual and careful’ because…some people say to me ‘why are you cutting when inflation’s above target?”

Banco de México—Downshifting

Banxico is expected to cut its overnight rate by 25bps to 7.75% on Thursday. That would be a softer cut than the series of four consecutive 50bps cuts leading up to this decision.

One reason for expecting this downshift is guidance provided the last time they cut on June 26th. They did so in central banker language. The prior statement in May when they cut 50bps had repeated the line that they could cut “by a similar amount” in June, and so they did. The June statement changed this language by saying “Going forward, the Governing Board will consider additional cuts to the reference rate” which is much less committal. Further, the accompanying language sounded more data dependent.

There have also been divisions of late on the Governing Board. The decision to cut 50bps in June was split as four policymakers supported the move but one—the influential Deputy Governor Jonathan Heath—voted for no change.

Heath remains cautious into this meeting. He recently stated the following:

“Core inflation is the component that is susceptible to monetary policy actions. Therefore, a decline in headline inflation that was due to the behaviour of non-core inflation is not a result of monetary policy and does not merit further rate cuts.”

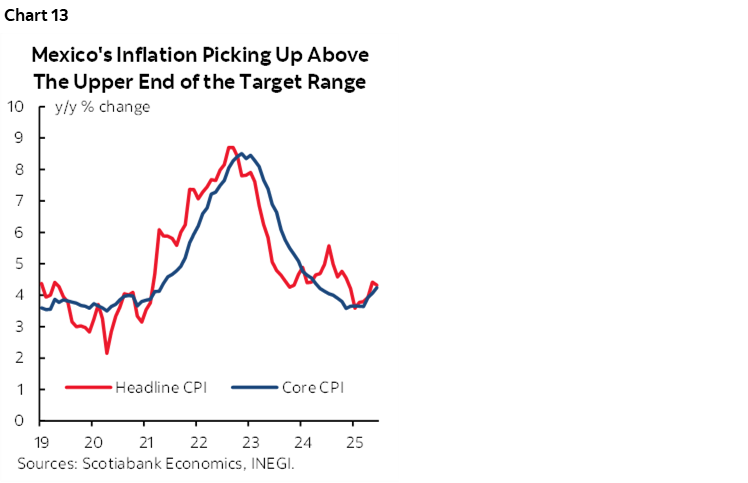

Recent inflation numbers have picked up above the upper end of the target range of 2–4% (chart 13). If Heath eventually succeeds at winning over his colleagues, then consensus expectations in a July 25th Bloomberg survey for another 125bps of rate cuts by the end of 2026 are far too aggressive.

Reserve Bank of India—They Teed Up a Pause and then Came Trump

A small minority expects the Reserve Bank of India to cut its repurchase rate on Wednesday. Most expect a hold at 5.5%.

Part of the reason for a hold is based on guidance provided at the June meeting. That statement said the Monetary Policy Committee “decided to change the stance from accommodative to neutral. From here onwards, the MPC will be carefully assessing the income data and the evolving outlook.”

That was a change to the previous change in May when the statement read that the MPS “decided to change the stance from neutral to accommodative.”

Recall that this shift was a neutral-hawkish bias on the larger than expected 50bps cut.

Even the most untalented pattern spotter might conclude that this meeting could shift back to an accommodative stance. Jesting aside, a limiting factor against further easing is renewed depreciation of the rupee given trade tensions with the Trump administration. The currency is back to previous weakness against the USD earlier in the year and presents upside risk to import prices passed into inflation. Hot money flows may already find the tight 100bps RBI spread over the Federal Reserve to be unappealing even without tariff risks. On that count, watch the RBI’s updated inflation forecasts particularly closely while it attempts to navigate through assumptions on volatile US-India trade policy.

GLOBAL MACRO—A LIGHTER WEEK

A lighter global release calendar will be lacking any shock-and-awe types of updates from a market standpoint but will have to offer across multiple markets. Watch for movement toward filling an unexpected vacancy on the Fed’s Board of Governors after Adriana Kugler resigned. Trump claimed she did so because of disagreement with Powell, yet Kugler’s comments two weeks ago sounded very much in agreement with Powell including her line “I find it appropriate to hold our policy rate at the current level for some time.”

What follows are perspectives on the releases from my colleague Jay Parmar and I.

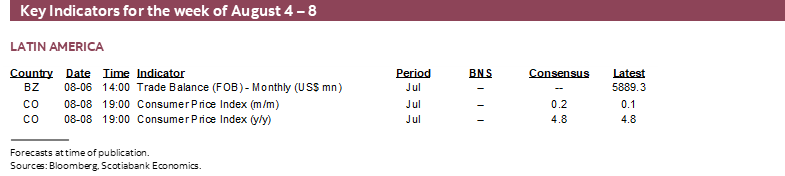

Canadian Trade to Inform GDP Tracking

Canada refreshes trade figures for June with possible prior revisions that will help to further inform tracking of Q2 GDP growth. At present exports are tracking a steep drop of over 30% q/q SAAR in Q2 after a pair of quarters of about 10% growth and with imports tracking a smaller 10% decline after about 6–9% gains in the prior two quarters. Because imports are a leakage from GDP, the drop in imports in Q2 after tariff stockpiling will lessen the net trade drag on Q2 GDP. The import figures will also give an updated sense of how investment performance is tracking, since most capital goods purchased by Canadian companies are imported. The volume of imported capital goods is tracking a drop of about 28% q/q SAAR in Q2 after surging by 29% in Q1; we’ll need to see if investment weakness is merely the unwinding of tariff front-running.

Light US Calendar Focused on ISM-Services

The US macro release schedule will be pretty light this week. The main highlight will be the ISM-services release for July on Tuesday. A small improvement is expected. Otherwise, the rest of the US calendar has relatively minor releases in between this past week’s nonfarm payrolls and the following week’s CPI that I’ve tentatively estimated to post gains of 0.2% m/m SA in both headline and core readings.

Global Inflation Round-Up

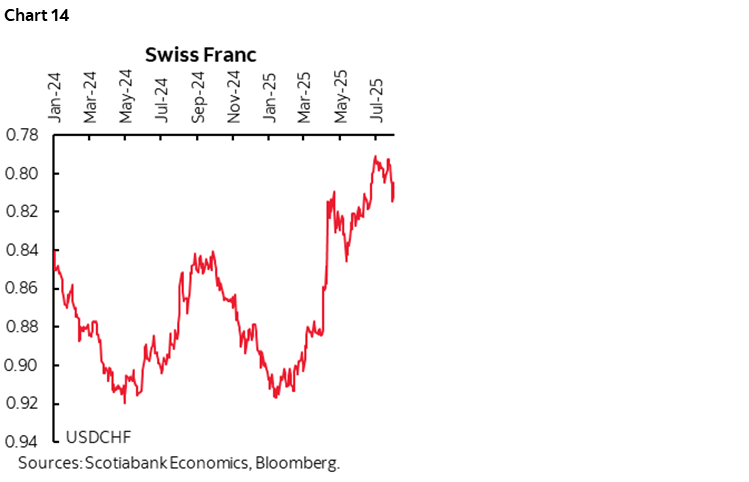

Several countries will release their July inflation reports throughout the week. Starting with Switzerland on Monday, headline inflation is expected to show stalled growth, while core inflation is projected to hover near 0.6% y/y, following June's upside surprise. However, the strengthening Swiss franc (chart 14) increases the downside risk on inflation ahead.

For Sweden’s Riksbank, another round of warm inflation readings (Thursday) could delay the possibility of a rate cut later this year.

China is set to release a pair of key inflation readings (Friday night), covering both consumer and producer prices. In June, consumer inflation showed some firmness, rising 0.1% y/y and beating expectations, while core inflation climbed to 0.7%—the highest since April 2024. However, expectations of softer consumer demand in the second half of 2025 could lead to further cooling of inflation. On the producer side, deflation has deepened, with prices falling by 3.6% y/y—the lowest level since August 2023. Continued deterioration is expected amid weakening external demand, slow consumer demand and absence of a trade deal.

Mexico's inflation data (Thursday) will be released on the morning of its central bank's monetary policy meeting. Although it is unlikely to alter expectations for a 25bps rate cut at this meeting, the key question will be whether the upward trend continues to push inflation above the upper end of the inflation target range.

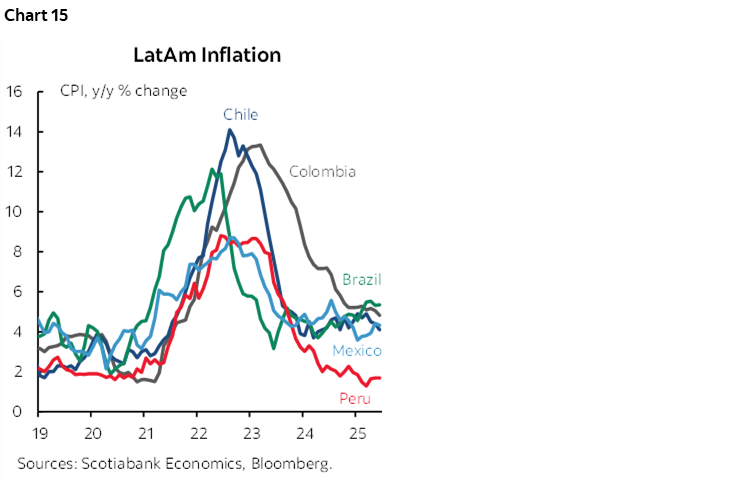

Meanwhile, both Chile (Friday) and Colombia (Friday) will publish the first of two inflation readings (chart 15) ahead of their next monetary policy meeting. A continued slowdown in inflation could reinforce the case for further rate cuts.

Inflation data from South Korea, the Philippines, and Thailand will be closely watched ahead for their August monetary policy meetings. Following a last-minute trade 'deal' with the US, the BoK's warning of 'significant' uncertainty from US tariffs may have lost momentum, placing greater emphasis on domestic economic data, like inflation on Monday, in shaping near-term rate decisions. Similarly, in the Philippines, modest inflation (Monday) and resilient Q2 GDP (Wednesday) are expected to strengthen the case for a 25bps cut at its August meeting. While in Thailand, core inflation (Wednesday) is expected to remain near the lower bound of the 1–3% inflation target range, keeping the door open for further easing.

Other Releases

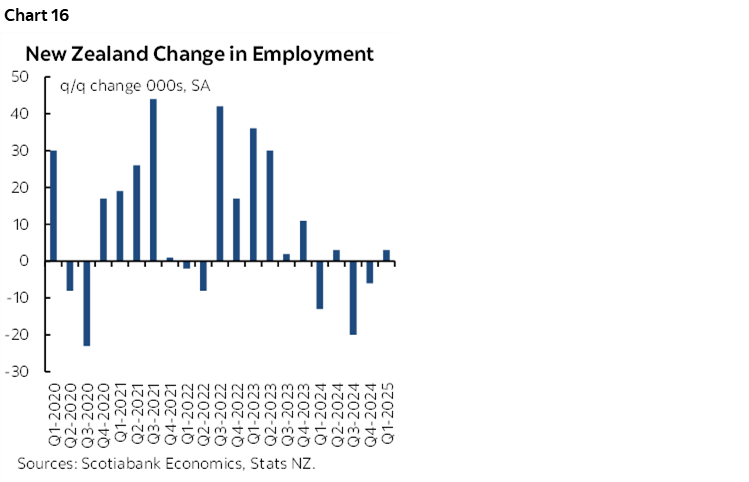

New Zealand will release its delayed Q2 labour market data on Tuesday and a continued slowdown is expected (chart 16), alongside a rise in the unemployment rate to 5.3%. Monthly filled jobs have already signaled this weakening trend in job numbers.

Finally, Indonesia will release its Q2 GDP growth figure on Tuesday, which is expected to show a further slowdown to 4.8% y/y—potentially the last dip before a rebound is anticipated in the second half of the year, supported by improved exports following the US trade 'deal'.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.