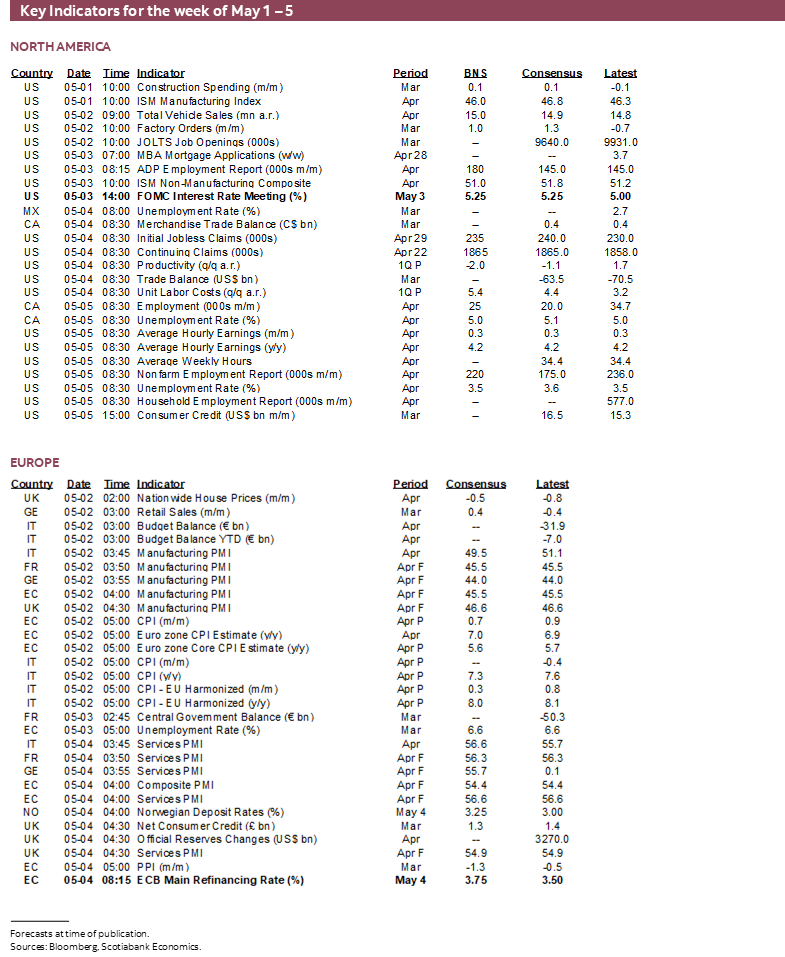

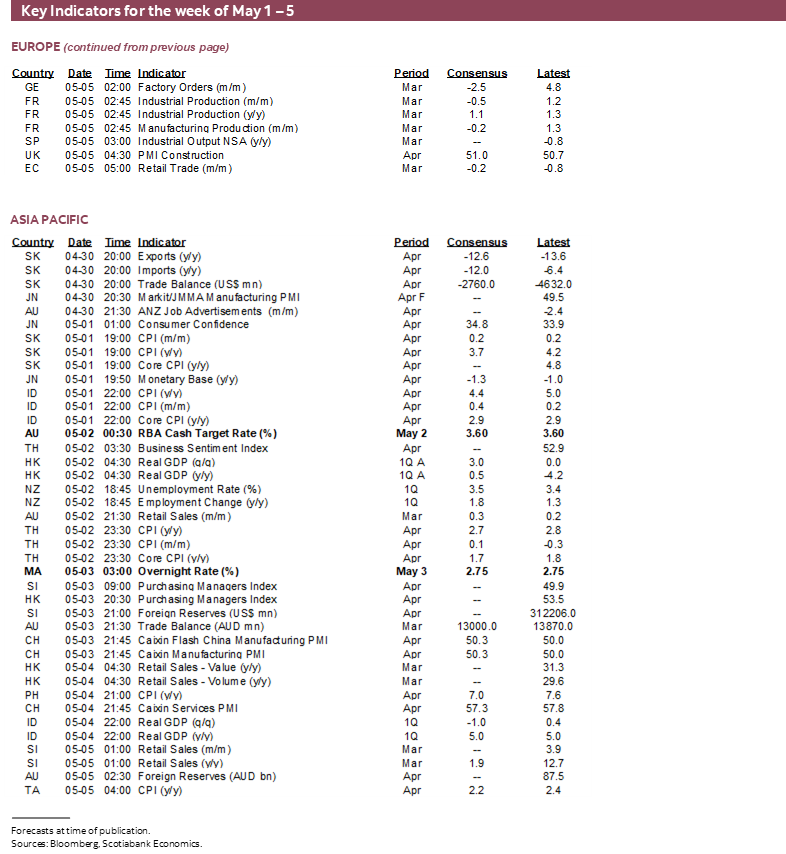

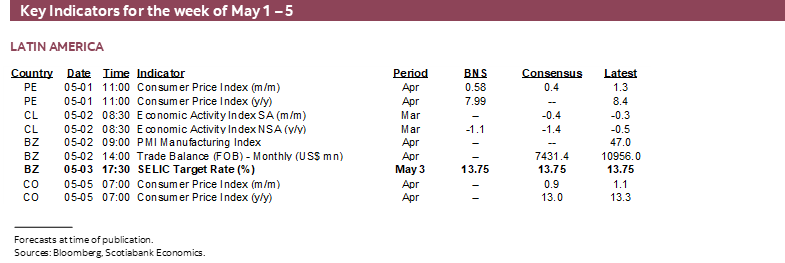

Next Week's Risk Dashboard

- Embracing change at US regional banks

- Fed to hike, retain optionality

- ECB to hike, defer guidance to June

- Is consensus underestimating US payrolls again?

- Canadian jobs may keep growing as wage pressures mount

- Soaring N.A. labour costs

- RBA will probably pause

- Norges Bank to hike again

- Brazil’s central bank inching closer to easing

- Bank Negara to stay on hold

- PMIs: China, US-ISM

- NZ jobs and wages to inform RBNZ risks

- CPI: Eurozone, LatAm, Asia-Pacific

- Other macro

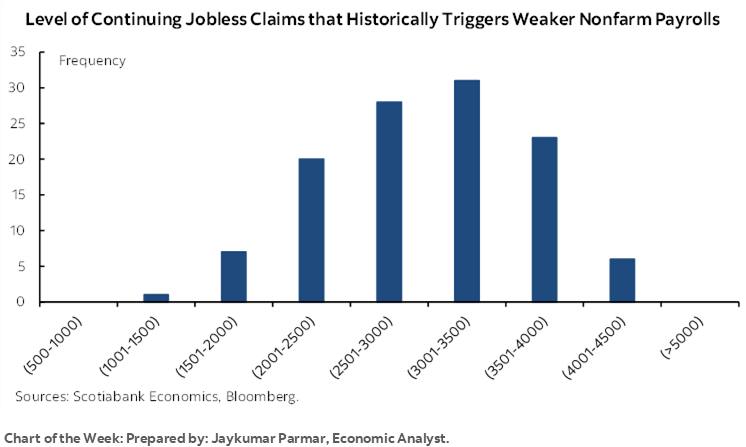

Chart of the Week

The coming week is packed with highly influential developments that will shape the broad tone of risks and opportunities overhanging global markets.

FEDERAL RESERVE—HIKE AND RETAIN OPTIONALITY

The Federal Open Market Committee meets on Tuesday and Wednesday and the outcome culminates in a 2pmET statement-only affair on Wednesday sans forecasts or dots and to be followed by Chair Powell’s press conference 30 minutes later. It seems highly likely that they will deliver another 25bps hike that would take the upper limit of the Fed funds target range to a new high of 5.25%. Of greater uncertainty is what the statement does on the bias.

Perhaps the smartest thing to do would be to merely refresh the date on the last statement and keep the broad messaging intact. That statement’s description of current conditions generally still holds. So does reference to tighter credit conditions with uncertain effects even while developments since the March meeting have been more constructive than feared. I’ll leave the matter of regional banks to the next section of this report with separate treatment.

It would also probably be prudent to retain the line that says “some additional policy firming may be appropriate in order to attain a stance of monetary that is sufficiently restrictive to return inflation to 2 percent over time.” A cost-benefit approach to evaluating the merits of altering this sentence at this juncture probably reveals little by way of any benefit and potentially at a great cost. Strike down reference to possible further hikes and markets will have their ‘gotcha’ moment on a clear signal the Fed is done, and the next move is lower; this would probably drive a pile-on effect into the front-end of the Treasury curve and with that a return of rate cut pricing that the Committee may find to be premature.

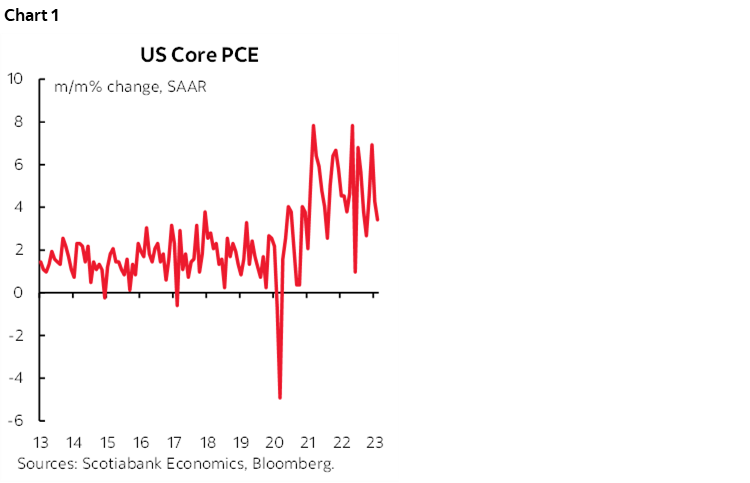

Furthermore, core inflation remains very sticky (chart 1) and so do labour market drivers of inflationary pressures as addressed in the section of this report that covers nonfarm payrolls. It would seem to be extraordinarily premature to declare policy tightening to be at an end while the focus shifts to the lagging effects when those lagging effects that began with market tightening in the Fall of 2021 have yet to bear much fruit toward durably getting inflation much lower.

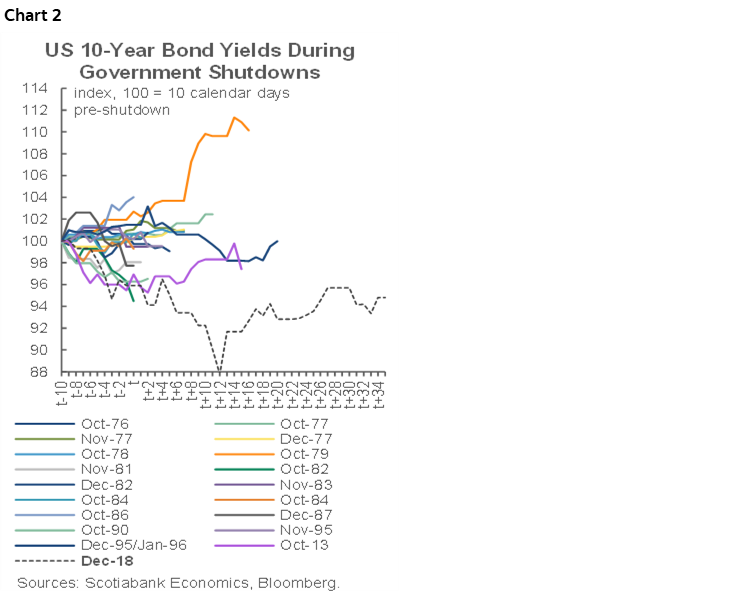

The Committee probably also has no appetite at this point for removing reference to how it ‘may’ hike again in a more certain sense. The FOMC is likely nervous going into developments like the debt ceiling with an x-date of sometime in July or August. The general pattern is that whenever the US courts the risk of government shutdowns that may (like in 2013) be related to debt ceiling spats or other disagreements, Treasuries often rally and stocks often weaken in the lead-up to the developments (chart 2).

REGIONAL BANKS, SYSTEMIC RISK AND OPPORTUNITY

One question that clients ask is the degree to which regional bank problems in the US are a sign of everything unravelling that should merit a much more cautious stance by the Federal Reserve. Developments this week may further inform this risk and particularly surrounding the next player of concern which is First Republic Bank’s share price collapse amid deposit flight that prompted speculation the FDIC is moving to place the bank under receivership.

Still, I turn that thesis on its ear in order to argue that the problems facing regional banks will persist but don’t have to pose major systemic risk while instead offering the opportunity to address them once and for all.

The first of two main arguments to this effect is that there is a vastly more sophisticated infrastructure for managing and containing systemic risk due to developments over the past fifteen years or so. Going into the Global Financial Crisis there were more limited tools for addressing risks posed by targeted failures in the financial system. Few had heard of truly unconventional monetary policy with most of our understanding of what central banks could do confined to the policy rate and liquidity support. If there was any awareness of unconventional monetary policy, then it was a vague recollection of measures like forced buying of government debt and yield curve controls during and after wartime.

Today, however, we have a vastly better understanding of the policy tools at the disposal of modern central banks. Examples include TARP, TALF, PEPP, APP, a Bank Term Funding Program, tweaks to borrowing at the window, new facilities targeted toward repairing parts of the markets for a wide variety of financial instruments, a repo facility, swap lines across global central banks to address dollar funding liquidity, blanket guarantees of at least some uninsured deposits, large funding infusions from the Federal Home Loan Bank and a panoply of too many other initiatives to rattle off.

The experience gained with these responses and policy instruments is what enabled central banks and others to rapidly respond to the demise of Silicon Valley Bank and Credit Suisse. Into 2008, such implosions would have derailed the global financial system just as Bear Stearns and Lehman did. Today they have so far been absorbed into a still functioning financial system.

That’s not to say that market volatility and uncertainty won’t persist particularly in terms of the information barriers surrounding where the next problems may lie and the reverberating effects. But the system’s ability to absorb such risks is vastly greater now and the clear signal from policymakers is that they will draw upon this wealth of experience to dive on the grenade(s).

The second part of this thesis is that now is perhaps finally the opportunity that the US has long waited for in terms of ending the cycle of problems at regional banks each time the punchbowl is withdrawn and in a way that crafts a more modern, safer and sounder banking system for the 21st Century.

For such a sophisticated, first world economy with its impressive ability to restructure and innovate while having very deep capital markets and an upper echelon of a dozen or so world class banks, the US nevertheless has a still outdated system of unstable regional banks. At risk of being a Canadian commenting on why, I'll draw on lessons from history and money and banking before turning to the opportunity.

Fear of all things big in the founding and development of America coincided with a bias toward keeping banks small. President Andrew Jackson's fight with the Second Bank of the US (as close to a central bank as existed at the time) resulted in repealing its charter and fragmenting the overly powerful banking industry as he saw it. A depression ensued. That's Act 1.

Fast forward to the McFadden Act of 1927 that banned interstate banking and branching in a short-sighted populist action that nevertheless lasted for decades. The result was a panoply of unstable local banking monopolies.

Only by the 1970s with the rise of monolines in mortgages and cards and state/regional banking pacts did this start to get chipped away. Dumb regs like the Interest Equalization Tax, confiscation of Soviet and Arab deposits that drove markets offshore to Europe’s benefit, and regulation Q worsened things along the way.

But it took the thrift crisis to set the stage for the move to the Riegle-Neal Act of 1994 that repealed the McFadden Act and introduced truer nationwide banking. The BofA and Nationsbank merger in 1998 was the big bang in the aftermath but the trend ever since has been toward consolidating small local players.

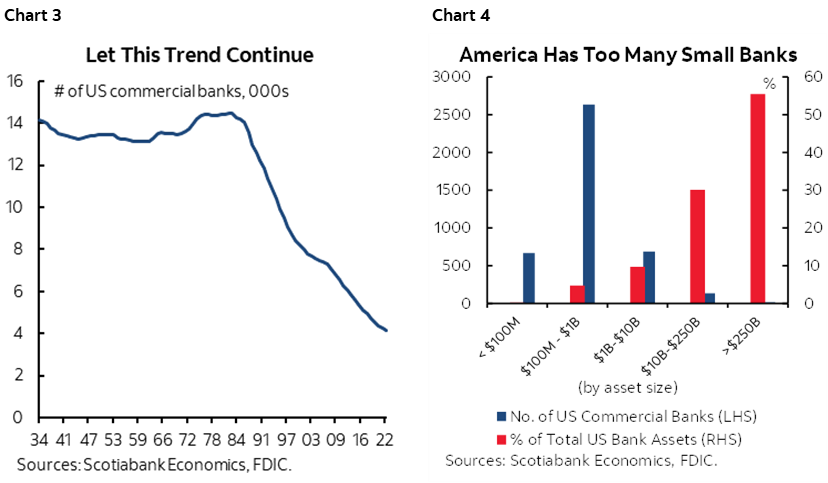

From 14–15,000 banks the US now has just over 4k banks (chart 3) and the vast majority of them remain tiny (chart 4). 80% of these banks have assets under US$1B. These are the lemonade stands of banking. 17% of banks have assets between $1B and $10B which is still tiny. 3% of banks have assets between $10B and $250B which in the world of banking remains small.

These banks a) lack loan diversification, b) lack funding diversification, c) have unsophisticated Treasury operations outsourced basically to the Federal Home Loan Banks while often mismanaging or not minding gaps, d) have unsophisticated risk management functions if anything at all (looking at you SVB...) and with that they have high failure rates that always get exposed when the security blanket gets pulled back.

This is a massive opportunity for US regulators to coax expedited consolidation. To counter the charge that everything that has been done since 2008 has driven higher moral hazard, regulators can and should now reap the advantages provided by more effective management of systemic risk by focusing upon broad market functioning and folding weaker players into the stronger parts of the financial system.

Powell’s legacy is dented by a misreading of inflation risk that took us to this point, but repairing that legacy depends upon success in combating inflationary pressures and perhaps setting the future conditions for a more stable and efficient banking system beneath the upper echelon of the biggest players.

If the US blows this opportunity that is presented by the intersection of market supports and controlled consolidation, then the long-term pain of persistent turmoil among regional banks will act as a deadweight upon the economy for many more years.

NONFARM GAINS, PRODUCTIVITY AND INFLATION LOSE

Nonfarm payrolls for the month of April land on Friday. I have estimated a gain of 220,000 jobs with a slight decline in the unemployment rate to 3.4% and wage growth at a steady 0.3% m/m SA pace that would keep the year-over-year rate unchanged at 4.2%.

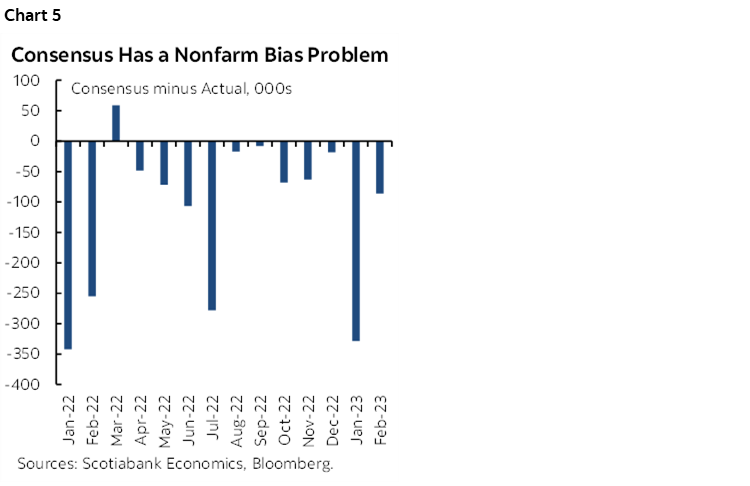

The pattern whereby consensus has materially underestimated job growth over an extended period of time is vividly depicted in chart 5. There has only been one single month in the past year in which consensus overestimated growth in payrolls and that was March of 2022. Consensus has a serial pattern of underestimating job growth much like underestimating quarterly GDP growth; even Q1 GDP at 1.1% q/q SAAR was better than the 0% consensus expected coming into the year and the underlying details were much more constructive than the headline reading with evidence of a strong US consumer.

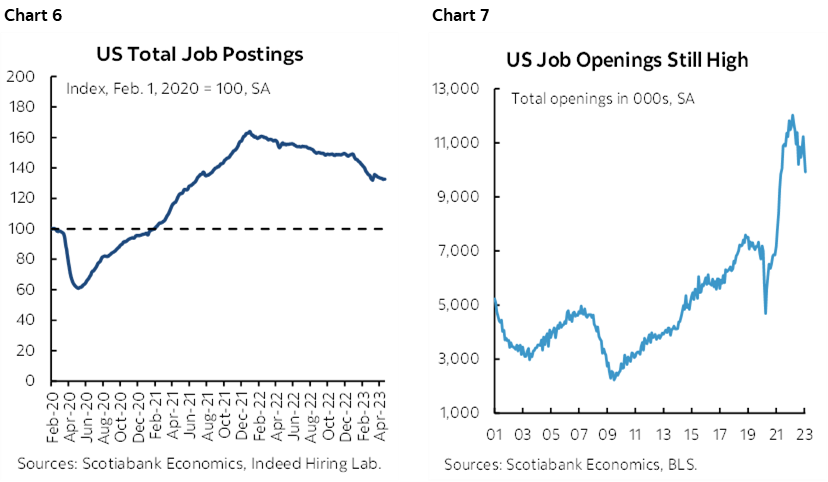

One reason for this forecast is that while the number of job postings is diminishing (chart 6), the total outstanding number of job vacancies remain very high and provide momentum in the pipeline of hiring activity (chart 7). Vacancies are off their peak, but there are still nearly three million unfilled openings compared to the pre-pandemic ‘norm.’ In a system that is generating basically near-zero population growth, it takes time to fill these openings in the absence of much more concrete evidence that they are being cancelled. This process can persist for quite a while yet and may be driven by the ongoing rotation of the hiring activity away from sectors that benefited earlier in the pandemic toward the sectors that have long been starved for workers.

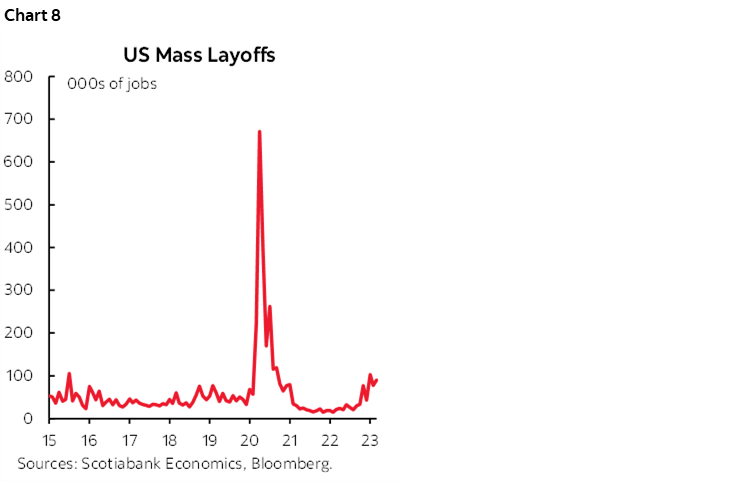

We may receive further information over the course of the week that informs this estimate. Challenger layoffs during April will arrive the day before nonfarm; so far they have risen only toward pre-pandemic norms and not to levels that are incompatible with net job growth (chart 8). Layoffs so far this year have been running at a roughly 80k–100k monthly pace which carries unfortunate consequences for the folks whose lives are affected but is so far not a terribly significant macroeconomic effect.

JOLTS job openings (Tuesday), ADP payrolls (Wednesday) especially if they are a big shock, and the employment subindex to ISM-services (Wednesday) also fall into this set of further information that is pending.

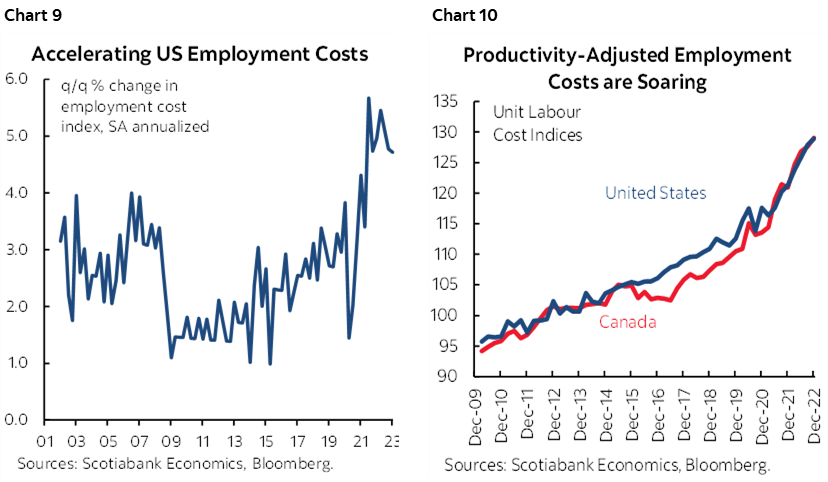

Alongside such arguments will be consideration given to productivity and productivity-adjusted labour costs. Q1 US labour productivity (output, or real GDP, per hour worked) will be updated on Thursday at the same time as unit labour costs. Because of the rate of expansion of hours worked and the relatively soft gain in GDP, labour productivity likely suffered with an estimated 2% q/q SAAR drop. Weaker productivity and a rising employment cost index will likely drive a rapid acceleration of unit labour costs that I’ve estimated to be a gain of over 5% q/q SAAR. Since labour costs have been outstripping productivity growth by a fairly wide trend margin for quite some time the outcome is incompatible with durably getting inflation lower. Charts 9 and 10 vividly depict this point by showing the acceleration of the trend line in employment costs and unit labour costs.

CANADIAN JOBS & WAGE PRESSURES

Canada updates job market readings for the month of April on Friday. With the usual trepidation, I’ve guesstimated a gain of 25k with a stable unemployment rate of 5%.

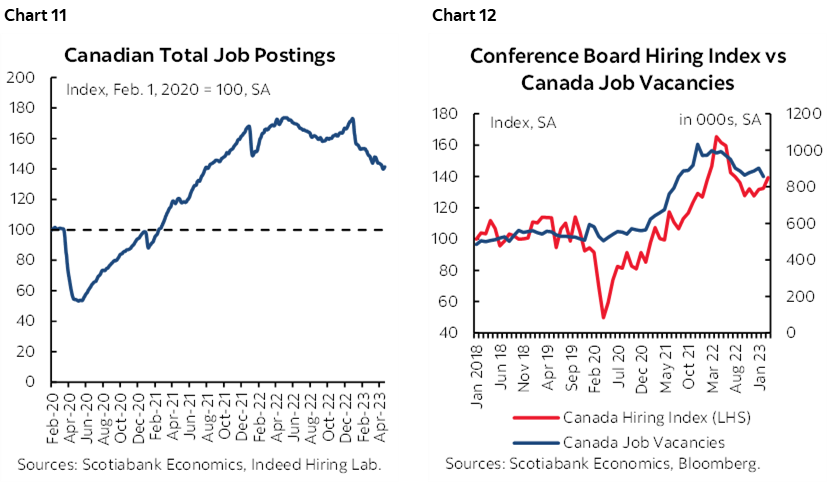

Like the US, job postings have been softening (chart 11) but job vacancies remain high at about 850k which lies between 300–350k above pre-pandemic ‘norms’ although perhaps few of us can remember what used to be normal for much of anything. Vacancies lag with data only up to February, but a slightly fresher hiring index for March from the Canadian Conference Board indicates the vacancies likely remained high in March and hence going into potential hiring decisions in April (chart 12). The ongoing need to fill these vacancies may be a source of resilience to Canadian job creation for some time yet.

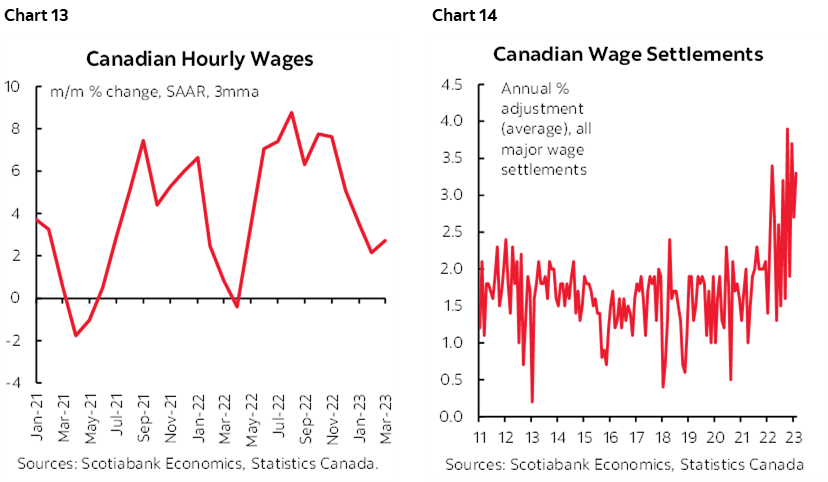

Like the US, however, the cost takes the form of movement in unit labour costs or productivity adjusted employment costs that have sharply accelerated over recent years (chart 10 again). With the clear exception of anyone reading this report, someone somewhere in the Canadian economy is getting paid more at a quicker pace than they are producing, and the combined effects represent labour-cost driven inflationary pressures.

Aa key added consideration will be evidence on incremental wage pressures in the form of the growth rate in average hourly earnings of permanent employees. The trend has been highly erratic over recent months (chart 13). Set against this point is the evidence that collective bargaining agreements in the private and public sectors are registering quickening wage gains in Canada and have yet to fully show up in wage data (chart 14). While I understand the pressures upon many households and the quest for higher pay (who wouldn’t!) expressing concern toward this development is not a left or right issue. As argued in last week’s Global Week Ahead that drew upon international research from IMF economists, when such wage pressures arise they are more likely to spill over into broadening wage pressures and into core inflation. The international evidence applies differentially depending upon the nature of the economy in terms of factors like the degree of tightness in the job market and the rate of unionization. Canada has among the tightest labour markets anywhere and among the highest unionization rates across countries that at about 30% is triple the rate in the US. I strongly believe this to be a consideration while monitoring the state of labour negotiations presently underway in Canada and connected to developments such as Ontario’s pending appeal of the court decision that struck down Bill 124. The Ontario Court of Appeal is slated to hold hearings on June 20th – 22nd. Left, right, or anywhere in between, the issue at hand is the potential for reigniting inflationary pressures in Canada alongside other developments such as widening agreement around what I’ve been saying for a long time now in terms of how housing is approaching an inflationary inflection point.

ECB HEADLINES OTHER CENTRAL BANKS

The ECB, RBA, Bank Negara and Brazil’s central bank will round out an active week for central bank policy decisions.

ECB—Hike & See Ya in June

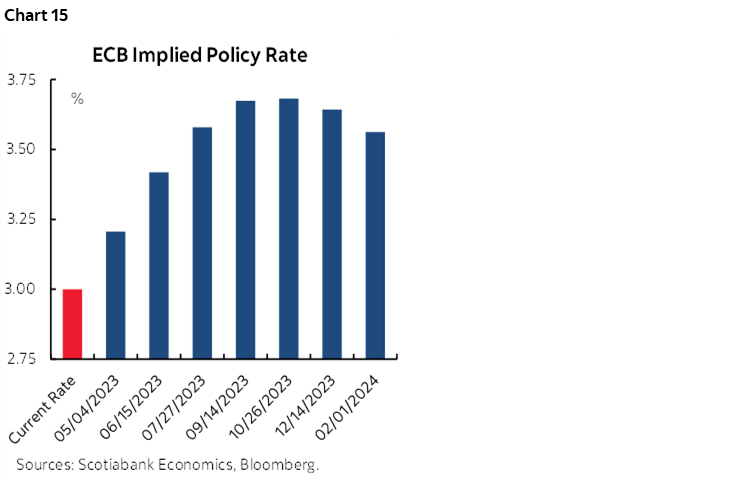

A generally hawkish tone is expected when the European Central Bank delivers its latest decisions on Thursday. Markets are primed for a 25bps hike in the deposit rate that would reduce the pace from 50bps moves and with most of consensus in agreement. There is a small tail risk of a larger move, but the bias is likely to be more informative.

At present markets are pricing a cumulative 75bps of rate hikes from a target deposit rate of 3% toward a terminal rate of 3¾% by the July or September meetings (chart 15).

There will be no fresh forecasts delivered at this meeting after the full update in March. The next forecast update is due with the subsequent decision on June 15th. President Lagarde may therefore leave much of the discussion on the outlook, risks and terminal rate estimates for the June meeting. She is, however, very likely to emphasize how inflation remains elevated and to point to an acceleration of wage pressures (chart 16).

RBA—Waiting for Wages

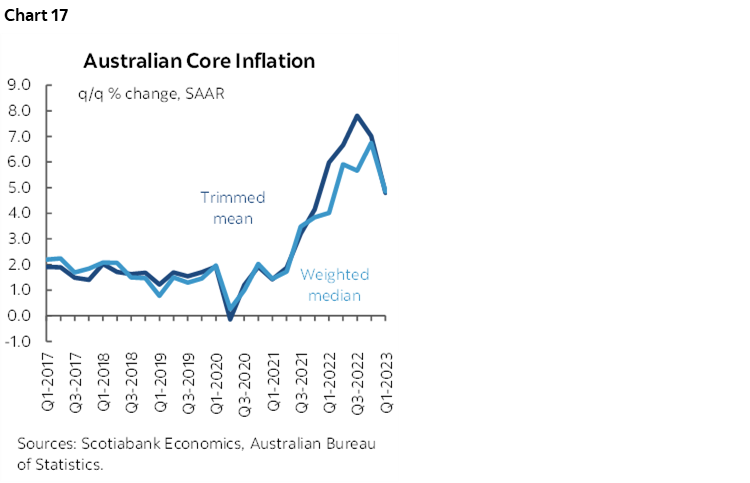

Most within consensus expect the Reserve Bank of Australia to hold its cash rate target unchanged at 3.6% on Tuesday. A minority of economists expect a 25bps hike. Futures markets are priced for no change and so clearly a hike would be a surprise. This follows a rally in Australian rates and weaker A$ that followed in the wake of Australian core CPI measures for Q1 that came in a touch weaker than expected (chart 17). They are still hot readings that work out to 4.8% q/q SAAR in both cases and hence well above the RBA’s 2–3% headline CPI target. That indicates that while incremental pressures at the margin have eased, they are still sticky—as is the case in Canada. What the minority may be going with is that jobs and PMIs have been strong of late and Australia is closer to the lift from China than other central banks, but a continued pause is likely to be accompanied by leaning against cut pricing with a mildly hawkish bias and with an eye on wages that arrive on May 16th and hence after the meeting.

Negara Likely to Stand Firm

It's a similar playbook for Bank Negara Malaysia as it delivers its next update on Wednesday. Most expect a hold at 2.75% with inflation on an ebbing trend but a minority think there could be a 25bps hike to a new overnight policy rate of 3%.

Brazil’s Pause Extension

Banco Central do Brasil is unanimously expected to stay on hold with an unchanged Selic Rate of 13.75% on Wednesday. The policy rate has been unchanged at this level since last August. Whether at this point or a subsequent meeting, falling inflation is making it more possible to contemplate easing (chart 18).

Norges To Hike Again

Norges Bank is expected to hike by 25bps on Thursday in keeping with prior guidance.

OTHER GLOBAL MACRO—CHINA’S PMIs TO DOMINATE

Additional risks will be primarily focused upon Chinese PMIs with regional markets facing a number of updates on jobs and inflation.

China updates the state’s purchasing managers indices with April readings into the Asian market open on Monday. These growth signals have sharply rebounded since Covid Zero ended and stimulus was applied through credit easing and targeted fiscal measures. Private sector PMIs will be updated later in the week and are relatively more skewed toward smaller producers and away from the SOEs.

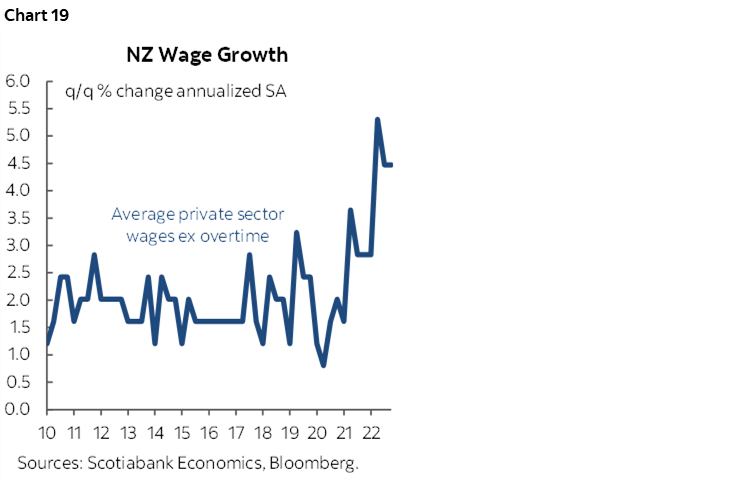

New Zealand Q1 employment and wages will be updated on Tuesday night (eastern time always in this publication). Key will be whether wage growth momentum is maintained (chart 19).

While the Fed and nonfarm will dominate considerations, the US release calendar will have a number of other items to consider. Construction spending during March (Monday) is expected to be little changed. April’s ISM-manufacturing may follow the balance of the regional Fed surveys lower (Monday). Factory orders should get a lift from durable goods orders that were up by 3.2% m/m but the new information will be nondurable goods orders (Tuesday). Vehicle sales probably increased a touch toward an even 15 million units during April based upon industry guidance (Tuesday). ISM-services could soften a touch given the softer retail sales report albeit other parts of the services sector may be more resilient (Wednesday). Finally, the US trade deficit will probably narrow in March’s release (Thursday) given we already know that the dominant merchandise deficit narrowed.

Beyond jobs, Canada updates trade during March (Thursday) and the manufacturing PMI for April on Monday, neither of which are likely to be significant influences upon local markets but will help to further inform growth tracking.

A slew of countries will update CPI readings over the coming week. Peru and South Korea kick it off on Monday, followed by Indonesia and Thailand on Tuesday, Philippines on Thursday and then both Colombia and Taiwan on Friday.

European and other global markets will start the week shut for International Workers’ Day since what better way to celebrate having a job than to take a day off, I suppose.... Other European indicators will include French industrial production during March (Friday), German retail sales (Tuesday), exports (Thursday) and factory orders (Friday), and Italian retail sales during March (Friday).

Other Asia-Pacific readings will include Australian retail sales (Tuesday) and trade (Wednesday) plus Hong Kong’s Q1 GDP (Tuesday) and retail sales (Thursday).

Beyond inflation and the BCB, LatAm readings will be confined to PMIs from Mexico (Tuesday) and Brazil (Thursday).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.