Next Week's Risk Dashboard

• Long-run inflationary forces

• France’s election and market risks

• BoC’s Macklem to reinforce faster pace

• Canada’s economy accelerating?

• The BoJ versus the MoF

• Slightly cooler headline Eurozone inflation?

• BanRep likely to hike again

• The Riksbank’s about face

• To Russia, sans love

• Aussie inflation set to jump

• Q1 GDP: US, Eurozone, Mexico, Sweden, South Korea

• US releases: PCE, income, spending, ECI, confidence, durables

• Ontario’s pre-election budget

Chart of the Week

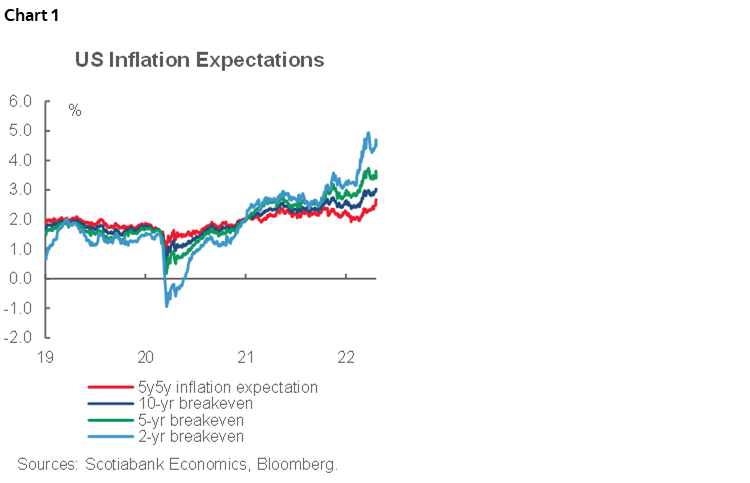

What if central banks never succeed in terms of reining in longer wave drivers of inflation and that structural drivers are being unleashed that could invoke profound longer term behavioural adjustments? Some of this view is why even the most preferred market-based measures of longer run inflation expectations like the Fed’s 5y5y measure are significantly above 2% (chart 1). This is occurring simultaneously to pricing fairly aggressive rate hikes. The market is signalling that central banks will struggle to get the genie back in the bottle for quite a period of time.

Markets are, of course, not always right. No one is. In this instance, however, they may well be bang on, except that the period over which inflation may be elevated could be much longer than priced. A plausible thesis is that central banks took excess credit for low and fairly stable inflation over the past 2–3 decades because structural forces were dampening inflationary pressures, but that they may struggle to contain inflation risk in future if those structural forces are simultaneously moving higher.

C-Suites the world over are realizing that the benefits of globalized supply chains that seek to minimize cost structures may have maximized operational risk given the US-China trade conflicts, the pandemic’s effects and now the war in Ukraine. Populism and geopolitical forces have motivated more uncertainty around policy frameworks. An effort to internalize more of their industry and company supply chains and pursue greater horizontal and vertical integration could mean higher cost structures being passed onto consumers. If so, this could unfold over many years with some more nimble industries better able to adjust more quickly than others with long-tailed legacy assets in place.

This force could combine with more restrictive trade practices to reverse the past disinflationary impact of China’s entry into the WTO over two decades ago. It could also combine with a shift away from technological change being disinflationary by lowering information costs and creating greater contestability, toward being inflationary with the pricing power going to firms better able to incur the massive and constant investments. Demographic forces could be turning more inflationary including through upward pressure upon the healthcare sector but also cooler growth in labour supply. Repricing of environmental risk including through carbon pricing efforts in enough jurisdictions to matter may add to these longer wave inflationary impulses. So could structural fiscal deficits and still excessively stimulative monetary policy. Higher expected prices might carry other influences like bigger cap-ex budgets to cash in on future expected price increases and perhaps revisiting neutral policy rate assumptions.

Another week of global central bank decisions is ahead of us amid rapid repricing of central bank actions. Their decisions should consider the nearer term effects, while leaving open the possibility they may not collectively succeed toward their end goals of containing longer run inflation expectations. Before I turn to a discussion of the upcoming central bank communications, markets will be hoping that another form of potential geopolitical risk won’t arise.

FRANCE’S ELECTION—RISK APPETITE WOULD LIKELY SUFFER IF MACRON LOST

The second and deciding round of France’s Presidential election will be held on Sunday. Projected results will be published soon after polls shut at 8pm Paris time (2pmET). Unless the count is very tight then we should have a good idea of who won shortly after that point. Recall that France does not allow early voting or voting by mail and so a US-style vote counting fiasco is unlikely.

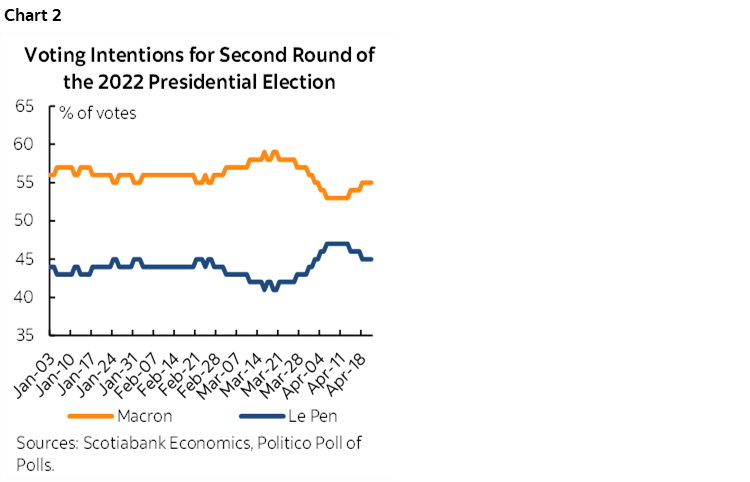

Macron is the favourite. He took almost 29% of the vote in the first round about two weeks ago which was almost 5 points above Le Pen’s share. He beat Le Pen by about a two-to-one margin in 2017. Current polls continue to give him an edge (chart 2.

The case for Macron is somewhat more about the case against Le Pen than the case for Macron, in my opinion. If Macron wins, then the market reaction may be fairly muted given what is at least partly priced and given the polls.

It could be a very different story if Le Pen wins. At a time when Europe needs unity, Le Pen advocates insular policies such as holding a referendum on declaring French law sacrosanct over EU laws which would essentially be like resurrecting her past desire for Frexit. Le Pen’s party is anti-immigrant at a time of a major European immigrant crisis as Ukrainians flee their war-ravaged country. If she succeeds, this stance could fan renewed break-up premia over bunds into Monday morning and a stock market hit.

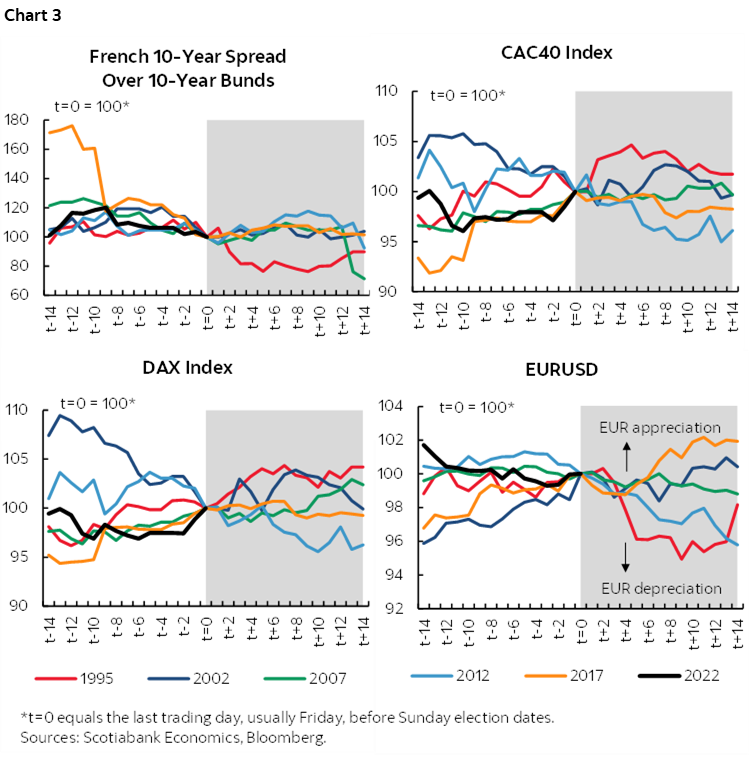

Chart 3 shows what happened to French spreads over bunds, the euro and stocks leading up to past first- and second-round elections and in the immediate aftermath. The last contest between today’s two candidates in 2017 was marked by a relief trade following first-round results and as polling evolved into the second round. Recall that when Macron won in 2017, the CAC40 rallied by about 7% between just before the first-round election on April 23, 2017 and the week or so after the May 7th second round. The German DAX put in a similar performance. The French 10-year spread over the 10-year bund yield also narrowed and the euro slightly appreciated to the USD starting when polls were favouring Macron. We’ve learned a thing or two around trying to anticipate market outcomes in the wake of events like US elections and Brexit votes, but the potential stakes involved this time could well mean that a Le Pen victory would be bad for risk appetite, at least initially.

She also has a history of being a tad too close to Russia and especially Putin and her party gets bankrolled by Russians because, in her own words, no French bank would finance them which one might surmise has something to do with, oh, let’s say break-up premia? Counterparty risk? A liquidity shock? Nahhhh. Le Pen’s rebranded party, National Rally, which used to be the National Front led by her father, also has deep anti-immigrant roots. Le Pen says she wants lower inflation but would advance (inflationary) tax cuts without saying how she’d pay for them. In populist fashion, Le Pen would also lower the retirement age to around 60 compared to Macron’s desire to raise it to 65 and with the unemployment rate already toward record lows. Le Pen’s approach could worsen pension challenges. Econ 101 would say lowering the retirement age by ~5 years and giving more money to people would probably fan wage and price pressures.

All will not end on Sunday night, however, as National Assembly elections are scheduled on June 12th and June 19th with all 577 members facing the electorate. They will determine the degree to which the victor in the Presidential election may be able to get his or her way on policy matters. Rhetoric around the Presidential election could therefore face reality within about two months, but from a market standpoint it may very well be a bad start if Le Pen were to be victorious.

MORE & FASTER CENTRAL BANK HIKES

Four central banks will deliver policy decisions over the coming week and further guidance will be forthcoming from the Bank of Canada.

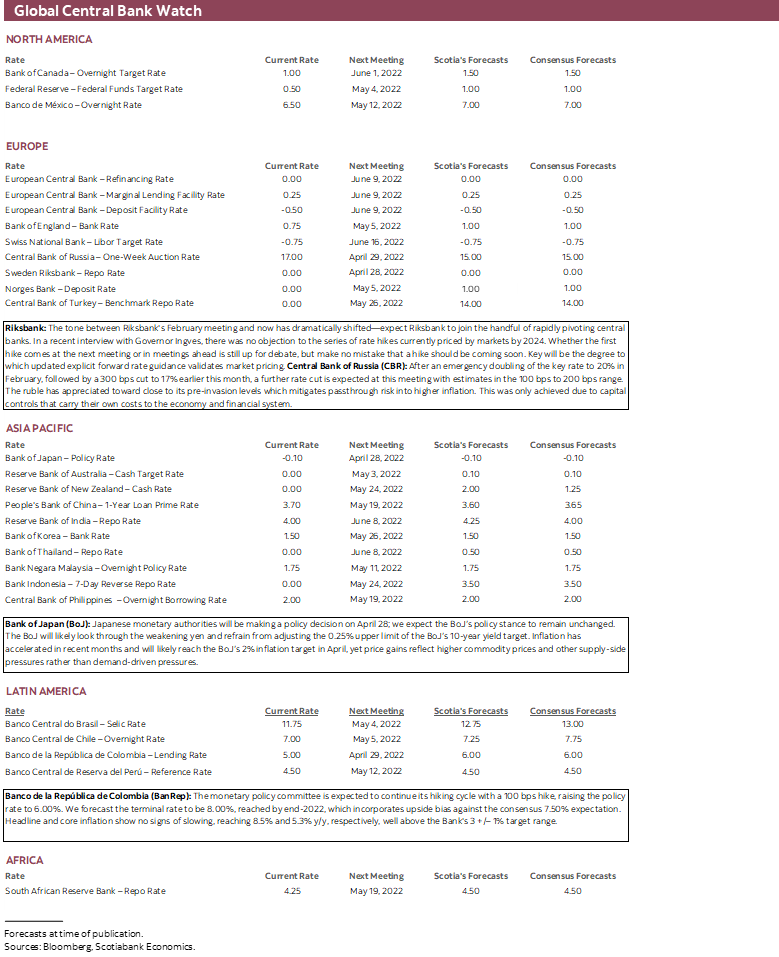

Bank of Canada Opens the Door to Even Bigger Hikes

Bank of Canada Governor Tiff Macklem and SDG Rogers deliver parliamentary testimony at 11amET on Monday. There will be an opening statement published on the BoC’s web site and then two-way banter with MPs. Since the Bank of Canada communications on April 13th, another inflation report has added to the heat. After hiking by 50bps, Macklem repeated guidance that the central bank will act forcefully which likely tees up at least another 50bps hike on June 1st with upside risk to the size of the hike. Considerations around the pace and magnitude of rate hikes will likely be a focal point during his testimony.

In fact, during a media roundtable at the G20 meetings in Washington, Governor Macklem left the door wide open to a bigger hike than 50bps. When asked if this was a possibility, he remarked “I’m not going to rule anything out. We’re prepared to be as forceful as needed and I’m really going to let those words speak for themselves.” His comments reinforced his prior point that a pause was likely only upon returning the current 1% policy rate toward the neutral rate range of 2–3% reasonably quickly. Macklem also appears to have somewhat thrown in the towel on the argument that supply chain driven inflation may begin easing up in favour of expressing concern that endless serial supply-side shocks are unmooring inflation expectations.

BoJ vs. MoF

Will the Bank of Japan welcome a softer yen and reinforce its commitment to ultra-low yields, or will it hint at a future reduction of monetary accommodation in the face of positive shocks to inflation and yen weakness relative to the dollar?

We’ll find out on Thursday, but Governor Kuroda probably already set much of the script by saying:

“The Bank of Japan should persistently continue with the current aggressive money easing toward achieving the price-stability taret of 2% in a stable manner. There is still a long way to go to achieve the 2% target in a stable manner.”

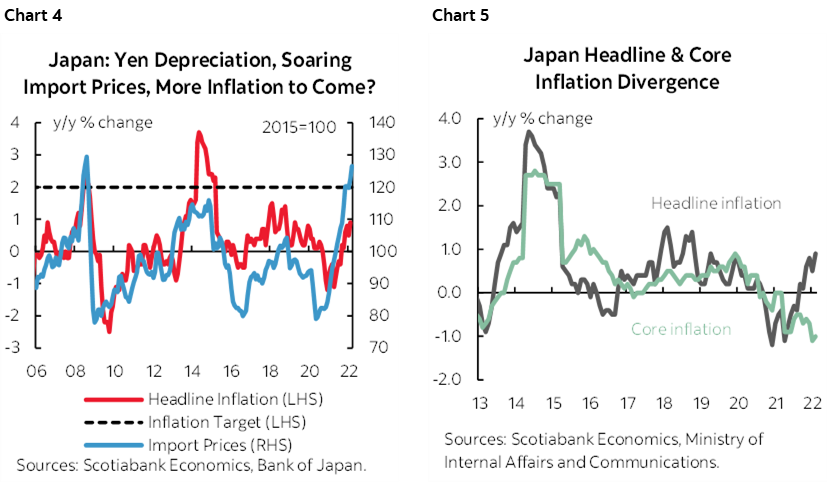

Therefore no changes are expected for the policy balance rate of -0.1% or the 0% 10-year yield target and the quarter-point ceiling that the BoJ has guided to be its operational limit. Still, inflation just crossed 1% for the first time since 2018. That’s well below the 2% target, but there is likely to be further upward pressure over the duration of the year. In fact, 2% y/y inflation is achievable in the near term, though durability will be the key to the BoJ. Chart 4 shows that rising import prices are likely to be driving CPI inflation higher when passed through. Chart 5 shows that the price pressure to date has been to headline inflation as core inflation is still very weak. That might continue.

The Bank of Japan has estimated (here, especially pages 20–21) that a one standard deviation move in the yen (roughly 4%) adds about 0.1–0.2% to inflation over 2–8 quarters; the recent move has been much larger than that and would imply that if it were to stick then all else equal Japan would get a 0.3–0.6% lift to inflation by the time it peaks within about a year and a half and then subsides. Further, the same paper estimated that a one standard deviation in oil prices of roughly 15% would add 0.1–0.3 percentage points to inflation inside of a year. The move in oil prices has been roughly three times that size which may imply—all else equal—that higher oil prices could add 0.3–almost 1% to inflation in nearer-term quarters before trailing off.

The challenge for the BoJ is that they wish to have confidence that inflation will remain at their 2% target over the medium term if they are to tighten policy. The yen and oil drivers of nearer term inflation are unlikely to sustain inflationary pressure around the 2% target throughout the monetary policy horizon of relevance to the BoJ. Japan is experiencing a relative price shock as a commodity importer with a weakening currency but the second-round effects in the context of soft wage gains could more likely be disinflationary in Japan than elsewhere.

That could leave whether and how to address currency appreciation to the Ministry of Finance. The yen has appreciated from about 115 to the USD in early March to shy of 130 now. Some believe that crossing 130 could trigger formal intervention. Finance Minister Suzuki has said that sudden moves in the foreign exchange market like what has happened to the yen are undesirable and that there should be a response with a sense of urgency. It may be doubtful that the MoF could sustainably weaken the yen given that the dominant driver is the relative stance of BoJ monetary policy compared to the Federal Reserve. The BoJ appears rather unlikely to alter its stance despite the MoF’s concerns.

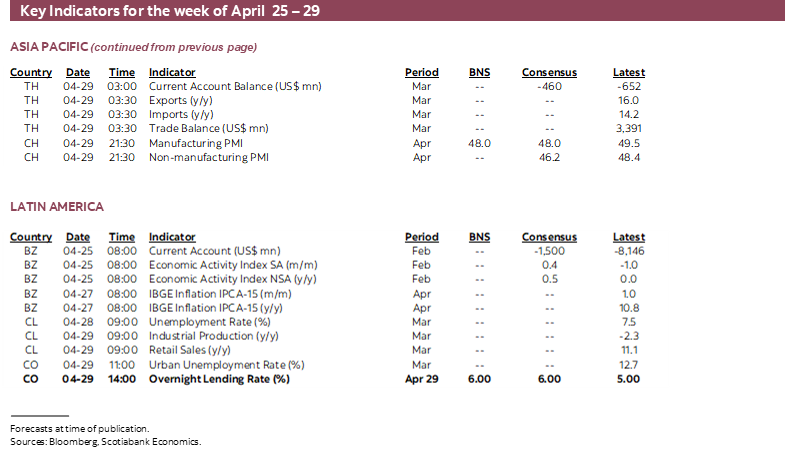

BanRep To Deliver Another Large Hike

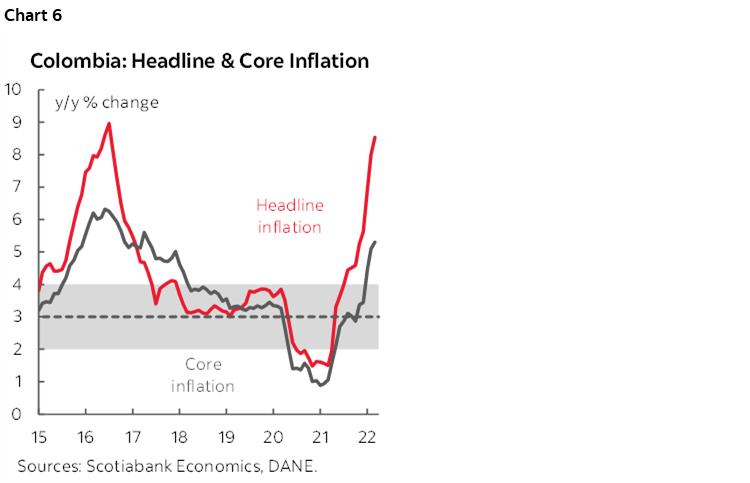

Scotiabank’s Bogota-based economist Sergio Olarte expects Colombia’s central bank to hike its overnight lending rate by 100bps to 6% on Friday. That follows an identical move on March 31st. Since then, inflation accelerated with prices up 1% m/m in March and 8.5% y/y from 8% the prior month while core inflation picked up to 5.3% y/y (chart 6). Both measures are above the 2–4% inflation target range. Scotia forecasts the terminal rate to be 8.00% by the end of 2022.

The Riksbank’s About-Face

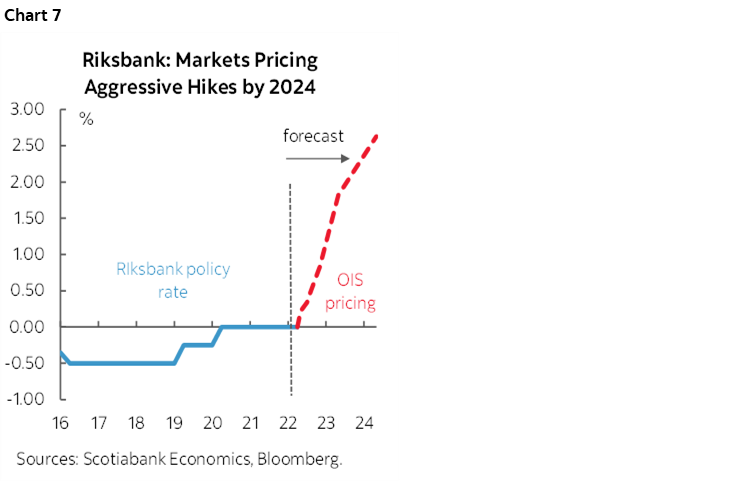

A leopard may not be able to change its spots as the popular expression goes, but central bankers sure can. Enter Sweden’s Riksbank as another example. Governor Ingves’s recent comments appeared to validate market pricing for a string of rate hikes starting as soon this meeting (Thursday). Deputy Governor Floden has also remarked that “We must raise the policy rate much earlier than we planned in February.” Indeed, a lot has changed since the Riksbank’s prior Monetary Policy Report showed a policy hold lasting into 2024 (here). Chart 7 shows the path currently being priced by markets. Key will be the degree to which the central bank validates this path in its revised explicit forward rate guidance.

To Russia Sans Love

Russia’s central bank is expected to continue cutting its policy rate on Friday. Cutting you say?? I thought their economy was getting walloped! Well, it is. In fact, the central bank had been hiking for about a year before Russia’s tragic invasion of Ukraine and then accelerated hiking with 11.5 percentage points worth of increases when war broke out. From a peak of 20%, it already reduced the policy rate to 17% earlier in April during an unscheduled move and set up expectations for a further reduction at this scheduled meeting. Shortly after the prior cut, the bank noted that “further normalization of risks for financial stability” would determine the size of future rate cuts. What the central bank is primarily referring to is the status of the ruble (chart 8). It had initially collapsed from about 75 to the USD just before the invasion toward almost 140 by early March but subsequently appreciated back toward about 80 at present. That’s not because Russian’s economy has suddenly improved. It’s solely because the central bank enacted a variety of capital controls that manipulated the currency. It had blocked USD withdrawals from bank accounts and banned the sale of all foreign currencies to residents while blocking foreign sales of domestic securities and hence rubles. That may well come at its own price alongside extreme damage to Russia’s economy from the allies’ sanctions and the high cost of the war. Restricting the capital account can foment domestic imbalances by not allowing a flexible exchange rate to adjust to shocks more effectively and can introduce welfare costs and deadweight losses to the economy.

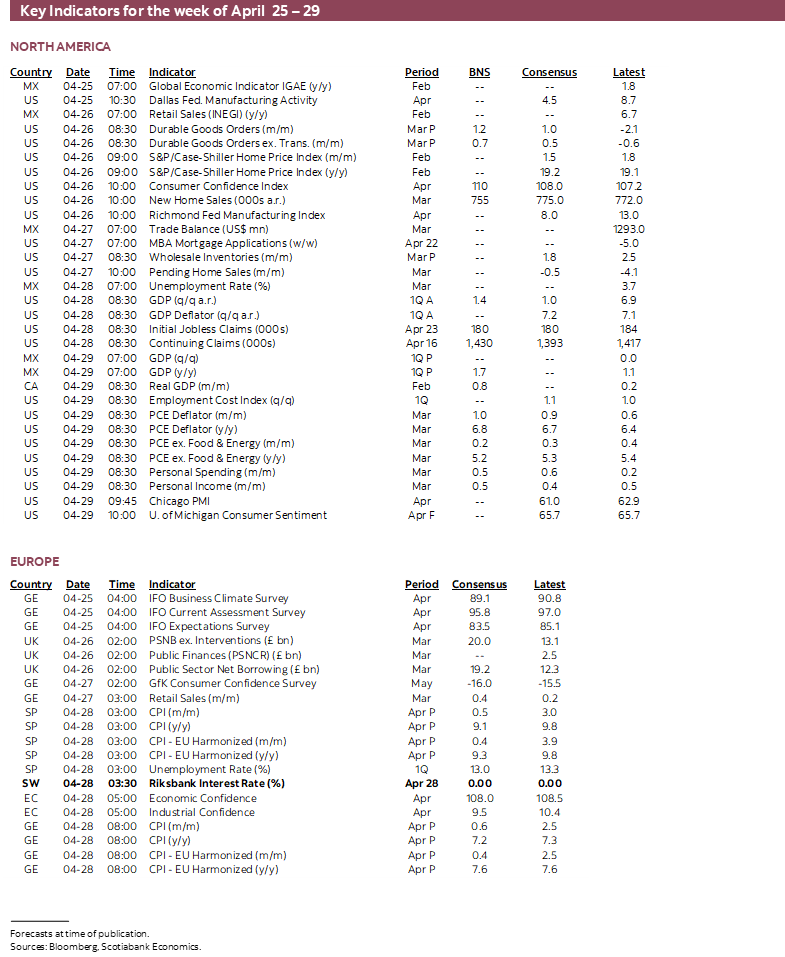

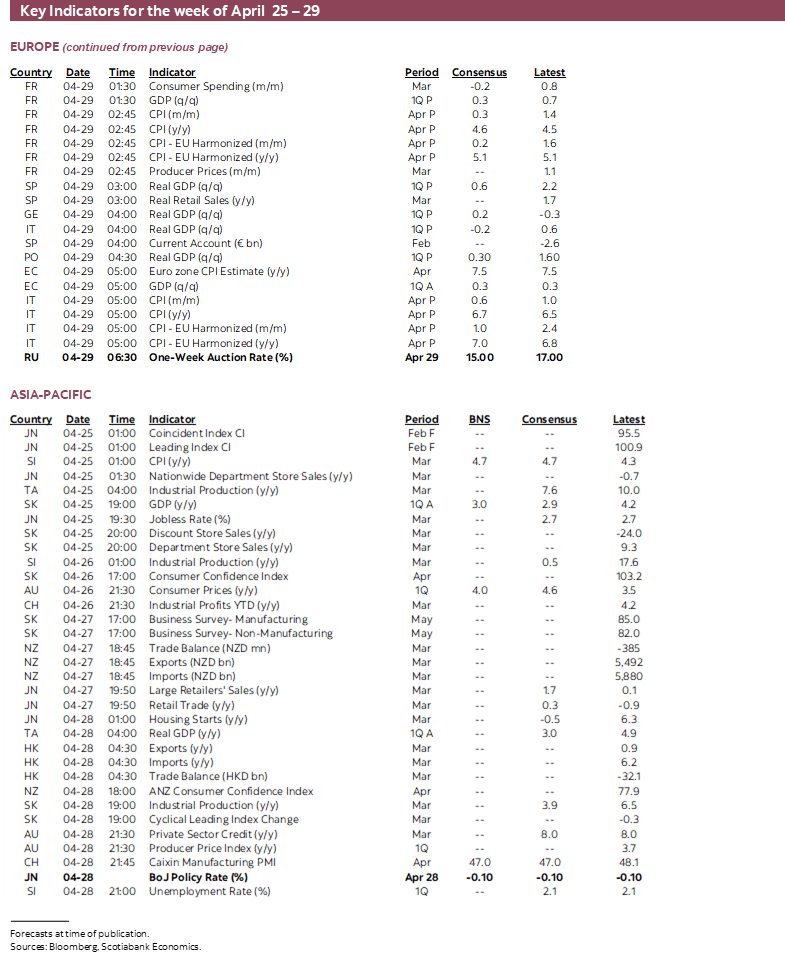

MACRO READINGS—INFLATION AND GDP WILL BE THE FOCAL POINTS

A few gems will dominate the global calendar of macro releases with a particular slant toward inflation updates and first quarter growth tracking.

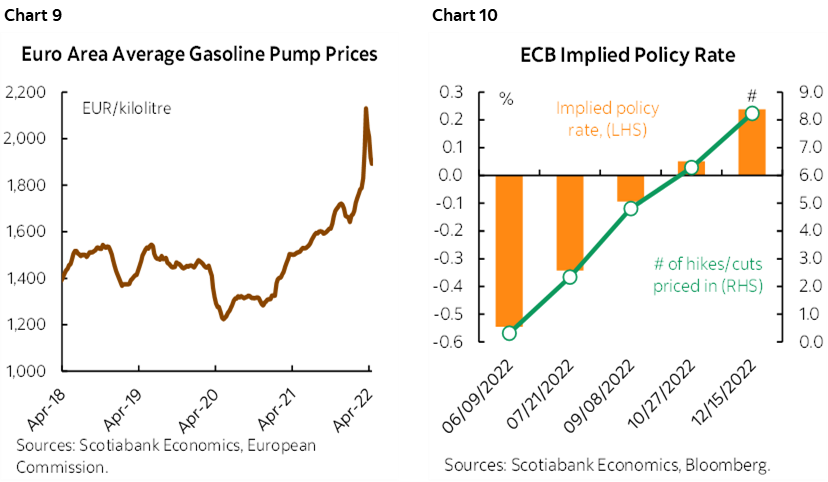

One key factor will be the next round of Eurozone inflation updates with the add-up arriving on Friday. Individual countries will start to release on Thursday when Germany and Spain update April CPI and then Italy and France release just ahead of the eurozone tally on Friday. Month-over-month headline prices may cool somewhat in the first flash estimates given the decline in gasoline prices (chart 9), but any further upside to core inflation would only add to market pricing for an ECB rate hike to arrive as soon as July or by at least Q3 (chart 10). ECB President Lagarde has done a complete 180 degree turn from “very unlikely” to see rate hikes in 2022 back in February to now saying there is a “strong likelihood” that rates will be raised this year.

Canada will update GDP figures with not only the final estimate for February but also a preliminary guide to March. StatCan said on March 31st that the flash estimate for February GDP was a 0.8% m/m rise. I see no reason to adjust that based upon limited data including revisions since then and based upon a simple regression equation I run. We have very limited data for March, but a 1.3% m/m gain in hours worked was a good sign given GDP is an identity expressed as hours worked times labour productivity.

A slew of US releases will arrive as follows:

- Tuesday brings out durable goods orders during March that will aim to resurrect gains in core orders as a guide to business equipment spending while also getting an assist from plane orders.

- The Conference Board’s consumer confidence gauge (Tuesday) probably got a boost in April given a rise in the UofM consumer sentiment reading plus solid job gains as wage growth resumed, gas prices pulled back somewhat and the S&P moved off the lows in March.

- New home sales (also Tuesday) might face more downside given that model home foot traffic declined.

- The first shot at Q1 GDP growth is expected to reveal something around 1½% q/q at a seasonally adjusted and annualized rate (Thursday). Omicron and the war’s effects may sap some growth after an explosive Q4 growth rate of nearly 7%.

- Fed Chair Powell guided late last year that the Employment Cost Index was among the variables he is watching most closely. The Q1 estimate arrives on Friday and is expected to rise at another 1%+ q/q non-annualized rate.

- The Fed’s preferred inflation gauge is likely to closely follow higher the large CPI gain in March, but core PCE inflation may slightly pull off the prior month’s 5.4% y/y at least temporarily the already known soft gain in core CPI.

- Personal income and spending are likely to both grow at similar ½% m/m rates when March’s figures arrive on Friday. The soft retail sales control group will need a services lift to propel spending while job and wage gains will do most of the heavy lifting for total income growth.

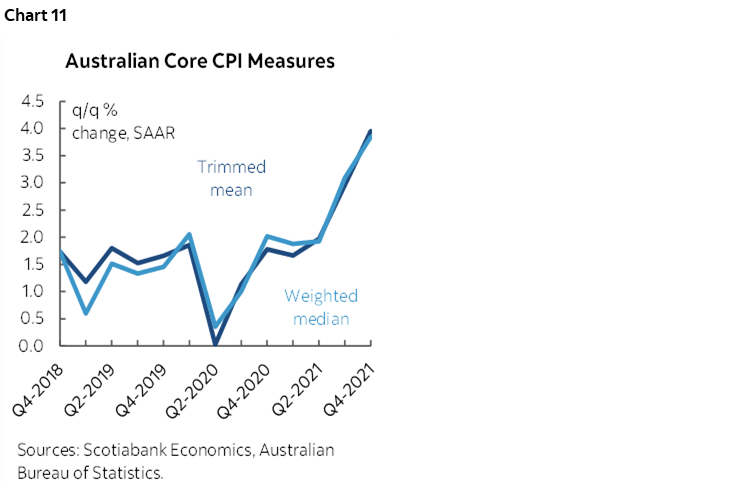

Australian inflation probably accelerated again in Q1 and we’ll get the numbers on Tuesday evening (again, all times eastern in this publication). Quarter-over-quarter annualized rates of core inflation have skyrocketed (chart 11). Wage growth won’t be updated for Q1 figures until May 17th, but it too picked up into the end of 2021. With markets pricing a full quarter-point hike by the June 7th meeting, any further upside surprises to both measures could either cement a hike at that time or pull it into the May 3rd meeting.

Global Q1 GDP readings will also arrive from a cross-section of other countries. Friday brings out Eurozone figures that are expected to repeat something similar to Q4’s soft growth (0.3% q/q SA). The bigger hit is likely to come in Q2 that fully captures the impact of Russia’s villainous invasion of Ukraine. Individual countries within the Eurozone will release that same day. Sweden will also update Q1 GDP (Thursday) and is expected to be little changed with downside risk after the strong prior quarter. Mexican Q1 GDP growth (Friday) is expected to accelerate perhaps toward the ½% q/q SA range after the economy stalled out over 2021H2; higher oil prices are benefitting the economy. South Korean Q1 GDP growth (Monday) is expected to decelerate following the prior quarter’s strong showing; South Korea has generally been better able to control COVID cases but is indirectly affected by China’s downside risks.

ONTARIO’S BUDGET TO REVEAL IMPROVED BOTTOM LINE

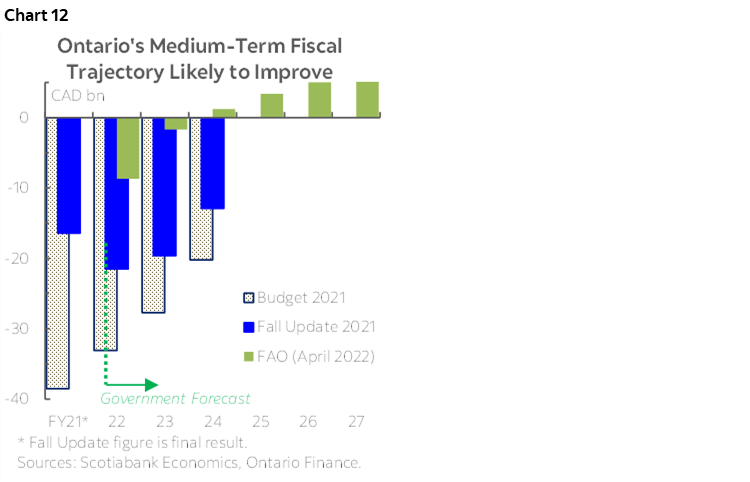

Scotia’s Laura Gu notes that Ontario will release its budget on Thursday where we expect to see an improved bottom-line despite potentially more new spending (chart 12). Recall that the province’s fall update projected deficits of -$21.5 bn (-2.3% of nominal GDP) in FY22, -$19.6 bn (-2%) in FY23, and -$12.9 bn (-1.2%) in FY24. The province’s Third Quarter Finances slashed the FY22 deficit to -$12.1 bn (-1.4% of GDP), attributable to significantly higher tax revenues, particularly from corporate taxes. Outer-year projections should also improve as big-ticket policy measures announced to-date are modest in scale compared to the revenue upside. Recent forecasts by the FAO project a surplus by FY24 absent new spending measures. We don’t expect the consolidation path to be quite this steep once the government’s prudent practice of conservative forecasting and contingencies is incorporated, and perhaps more importantly, if and when additional pocketbook measures are introduced as the provincial election approaches on or before June 2nd. The policy measures already announced—most notably the elimination of licence-plate fees and the gas tax relief—should erode some of the anticipated revenue windfalls. The federal-provincial agreement for the childcare program will add an average of $2.6 bn per year in transfer revenues from FY23 to FY27 but would be offset by commensurate new expenditures. Nevertheless, overall, we think that the revenue upside will likely overweigh spending pressures, putting the debt-to-GDP ratio on a lower trajectory relative to the fall update.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.