Next Week's Risk Dashboard

- Central banks have renewed confidence in hikes

- US earnings: good news is bad news for rates

- China’s GDP rebound

- PBoC will likely rely on credit easing

- Global PMIs to inform growth, inflation

- Canadian inflation faces renewed upside risk

- Canada’s housing rebound has only just begun

- Canada’s public sector drivers of inflation

- Canadian retail sales: more homes, more stuff?

- BI will likely hold

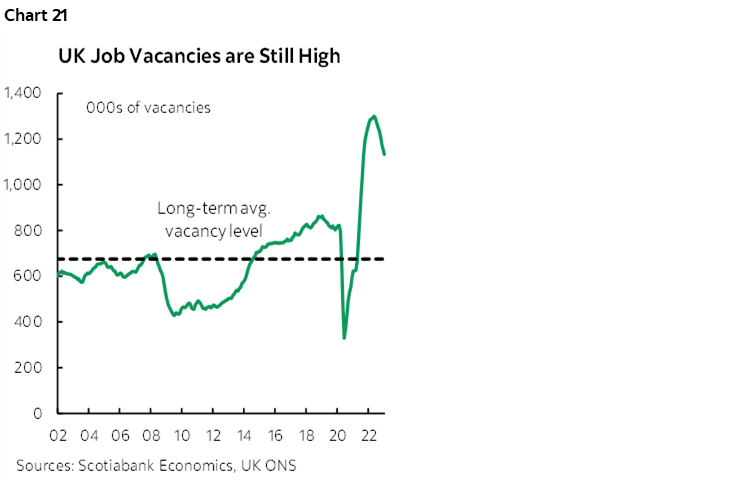

- UK job markets still have enormous vacancies

- Inflation: UK, NZ, Japan, Malaysia

- Other macro

Chart of the Week

Key developments over the coming week will be focused upon US earnings season and a fairly heavy line-up of global macroeconomic releases that may help to inform next steps by major central banks that begin to deliver decisions the following week and into early May. Renewed hawkish sentiment at the Fed, ECB and BoC suggest that a hiking bias is back.

CANADIAN INFLATION—RENEWING UPSIDES

Canada updates CPI inflation and subcomponents on Tuesday for the month of March. The estimates may influence the BoC’s posture toward persistent inflationary pressures, but there is a lot by way of data and developments between having set the narrative for now in this past week’s communications (recap here) and the next decisions on June 7th followed by the next full communications including forecasts on July 12th. For now, markets should treat this report as a placeholder and not least of which because other developments will inform future risks.

I’ve estimated a 0.7% m/m rise in total CPI in the conventional seasonally unadjusted manner in consensus surveys. Because March is often a seasonal up-month for prices, applying seasonal adjustment factors should have this translate into a rise of around 0.2% m/m SA. The year-over-year rate is expected to fall back to 4.5% from 5.2%.

This monthly headline estimate is compatible with what is implied by the BoC’s recent quarterly projection for CPI to land at 5.4% y/y in Q1 following readings of 5.9% in January and 5.2% in February.

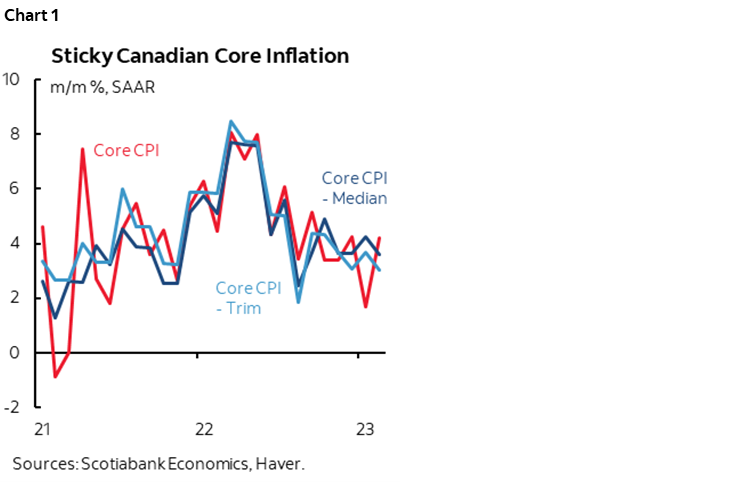

The BoC does not publish projections for its preferred trimmed mean and weighted median core inflation measures. The measures to watch will be the month-over-month annualized increases in these two gauges as well as month-over-month changes in the simpler CPI excluding food and energy measure that our very own René Lalonde prefers because it more closely aligns with output gaps and CPI over time. All three of these gauges have been sticky, signalling persistent inflationary pressures at rates above the 2% headline target (chart 1).

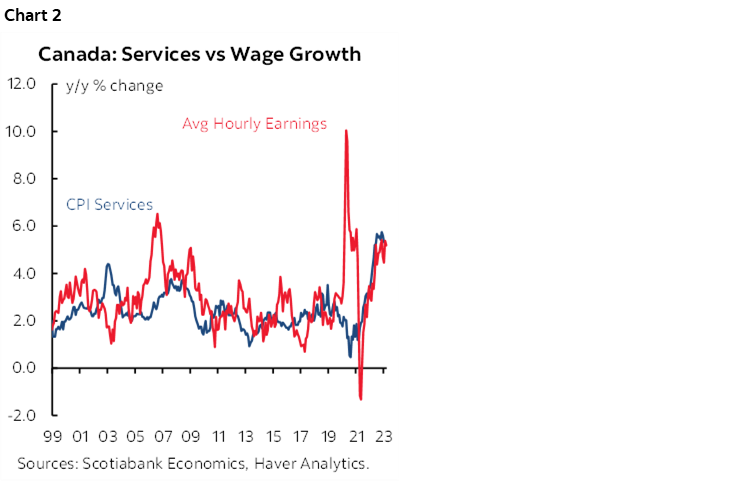

A key focal point for the BoC is services inflation and the correlation with wage growth (chart 2). A Canadian twist on this is that labour productivity is so poor which further reinforces inflation risk.

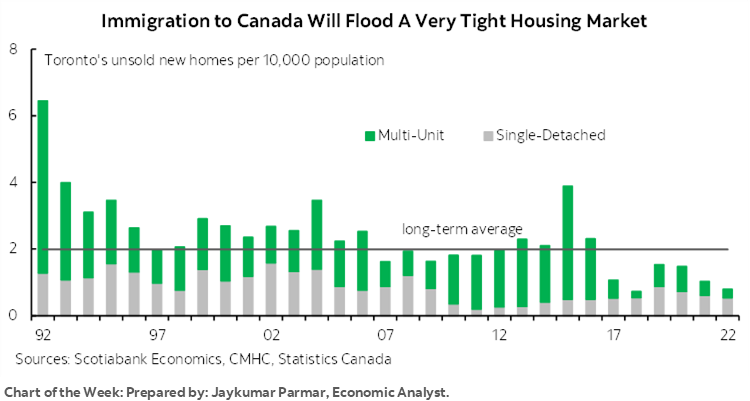

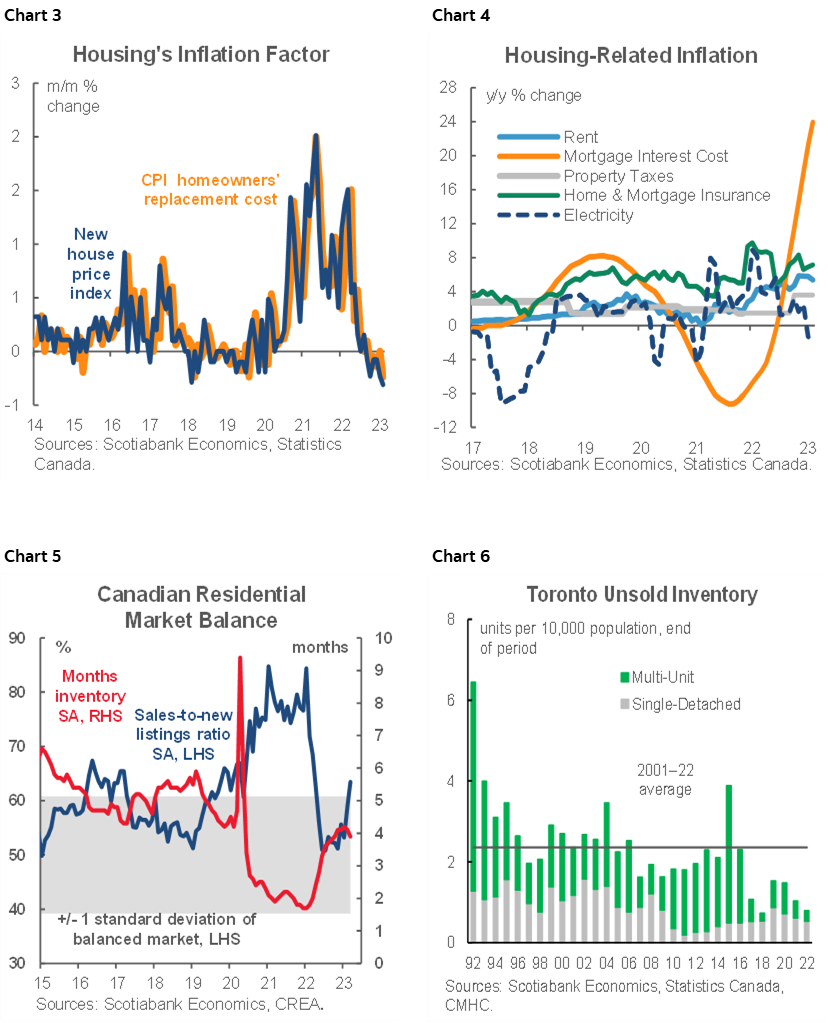

Housing is likely to continue to offer mixed effects but it’s the path forward that concerns me. Housing contributions have already waned in Canadian CPI by contrast to US CPI because of the way that Canada captures housing using replacement cost (not OER) which is driven by the house-only component of the new house price index (chart 3). Rent, however, continues to exert upward pressure as sidelined buyers in a weaker owner-occupied market have been pushed into tight rental markets (chart 4). The push to bring on housing supply in the face of tight resale market conditions (chart 5) and very lean unsold new home inventories including Toronto (chart 6) is so acute it is driving unexpected changes in the uses of real estate with one example being here. As Canada pushes immigration much higher into a market with little to no supply it is likely to challenge the BoC’s views on the impact upon inflation. The BoC assumes that higher immigration adds to both the supply and demand sides of the economy, but Canada’s housing market notoriously takes on demand first and supply reacts with long lags. The likely effect is to add to renewed house price and rent pressures that could resume flowing through to CPI. That pressure could resume more rather than less rapidly based on budding market dynamics. Brace for a return of all the tired real estate jokes. How do you make a million in real estate? Start with two.

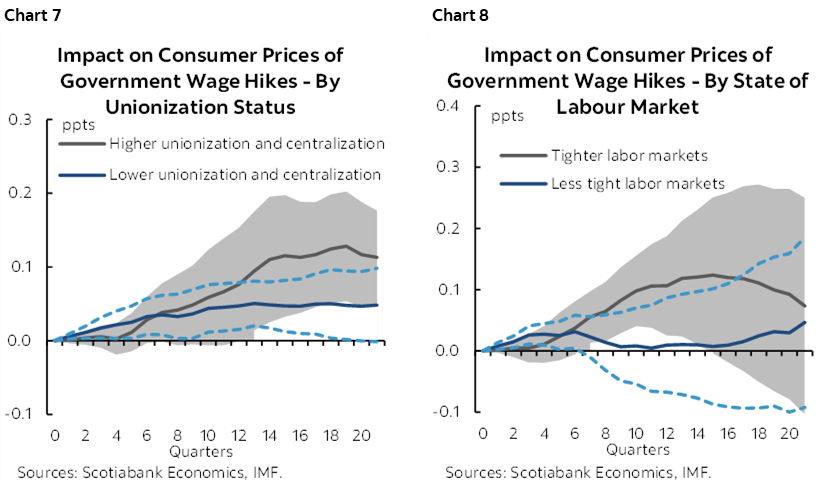

There are two other considerations. One is major pending wage negotiations in the public sector such as over 150,000 Federal employees in position to strike plus the pending appeal of Ontario’s Bill 124 and the imposed 1% wage settlement. The IMF’s latest Fiscal Monitor (here, Box 2.1) made a point of noting that public sector wage increases can spillover into private sector wage increases and CPI inflation and do so with persistent effects. Charts 7 and 8 are recreated from their publication. Chart 7 shows modelled persistence of public sector wage gains on private sector wages and into CPI according to various countries’ degree of unionization and centralized bargaining. Chart 8 does the same thing according to the degree of tightness or slack in the job market.

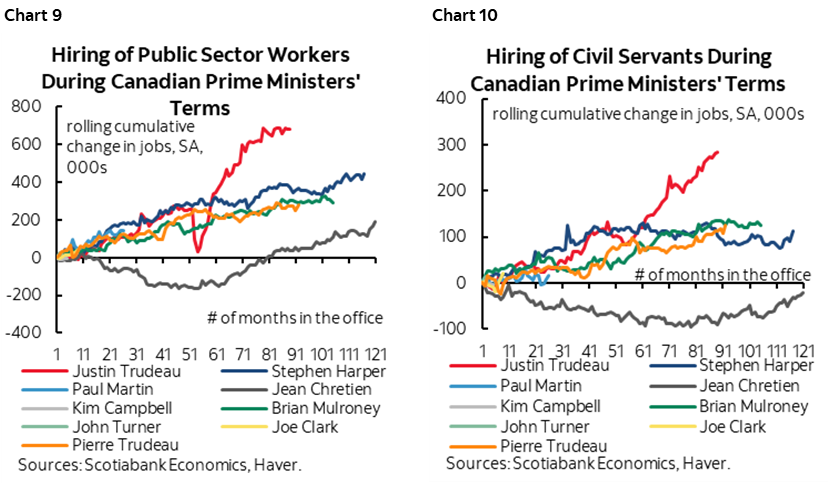

Canada’s job market is very tight and among the tightest in the world and the share of employees belonging to labour unions (29.4%) is roughly three times that of the United States, more than double Mexico’s, and higher than many European economies with notable exceptions being Italy and Belgium with Austria and Ireland not far behind (here). By corollary, Canada may have material risk of passthrough from public sector wage gains through private sector wage gains and into CPI. This may be particularly true in light of the large and sustained increased weight on public sector employment in Canada which busts the y-axis scale compared to history (charts 9, 10).

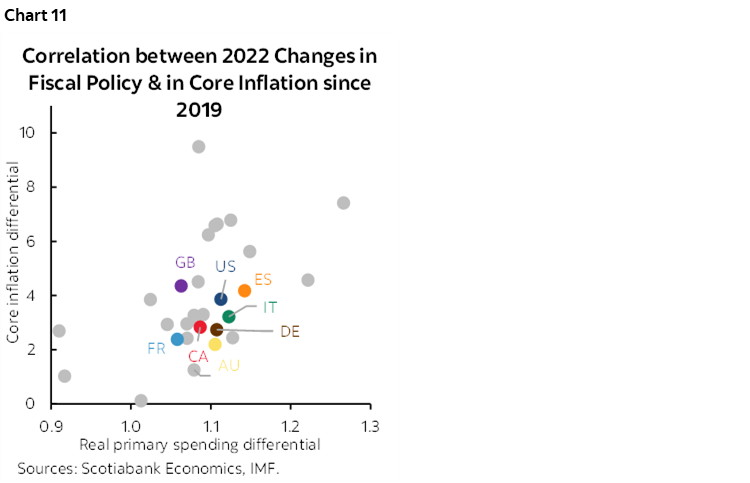

Another consideration is the ongoing impact of fiscal stimulus. From the same IMF publication is chart 11. There are countries that have driven more inflation with more spending than Canada, but the relationship points toward a material impact in Canada to date and the bias remains pointed higher.

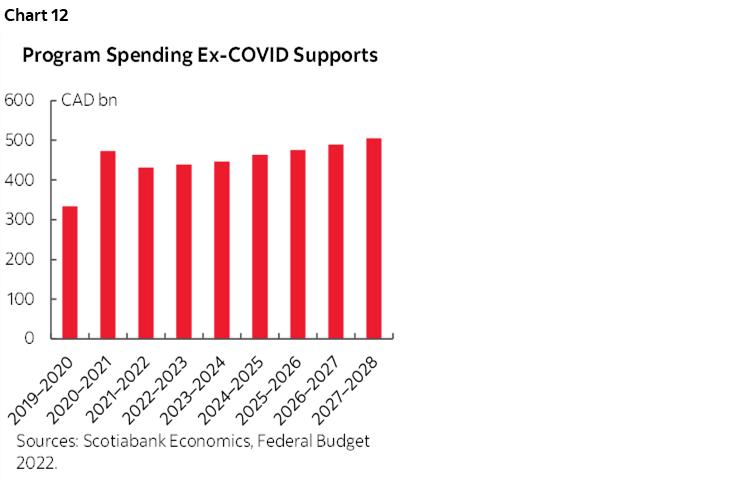

The Bank of Canada indicates that government spending will add 0.6 percentage points to GDP growth this year but that since the growth rate in public spending across all levels of government combined is in the vicinity of the growth rate in potential GDP this spending should not add to inflationary pressures. That seems a stretch. In the absence of this 0.6% contribution to growth, overall GDP growth would be projected to be close to nothing for the year using the BoC’s forecasts and the economy would be making quicker progress toward reducing excess demand and inflationary pressures should be moderated accordingly. There is also a stock argument to be made in that the injections of sustained increases in program spending since the pandemic have created persistent capacity pressures on the Canadian economy (chart 12) while driving labour scarcity as evidenced by the roughly 800,000 job vacancies—mostly at private employers—while one-in-two jobs created since the start of the pandemic have been in the public sector.

Overall, I think the BoC is sounding too sanguine toward inflation risk. Governor Macklem has said they discussed a rate hike at this latest meeting. There should be a non-zero probability of one being priced into OIS contracts in my view. Forecasters keep pushing out the point of achieving material slack while the job market keeps tightening and may behave differently this cycle (here). Oil production is at a record high and Western Canada Select crude oil prices are about 50% higher than the trough in December. The broad macroeconomic landscape may have had the BoC stopping hikes prematurely and perhaps especially if the Fed keeps ploughing ahead and in light of recently hawkish ECB comments. With inflation getting pushed against the ropes it would be a shame if Governor Macklem left the ring and went for a soda.

US EARNINGS—GOOD NEWS IS BAD NEWS

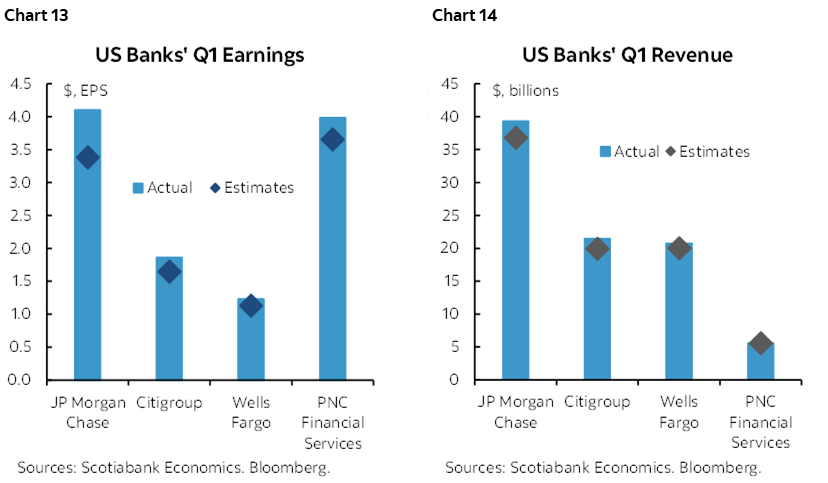

The earnings season will swing into higher gear after an impressive start marked by earnings and revenue beats at US banks (charts 13, 14).

About sixty more S&P names will release earnings over the coming week with more financials and a broadening of the sectors. Twenty-four more financials will make up a significant share of the names. A more complete picture of the health of the banking system may be provided by Bank of America, Goldman Sachs, Morgan Stanley, State Street, American Express, and several regional banks. Some of the nonfinancials will include names like Tesla, Netflix, AT&T, P&G, and Kinder Morgan.

This earnings season is arguably the most important in quite some time. There are several reasons for this.

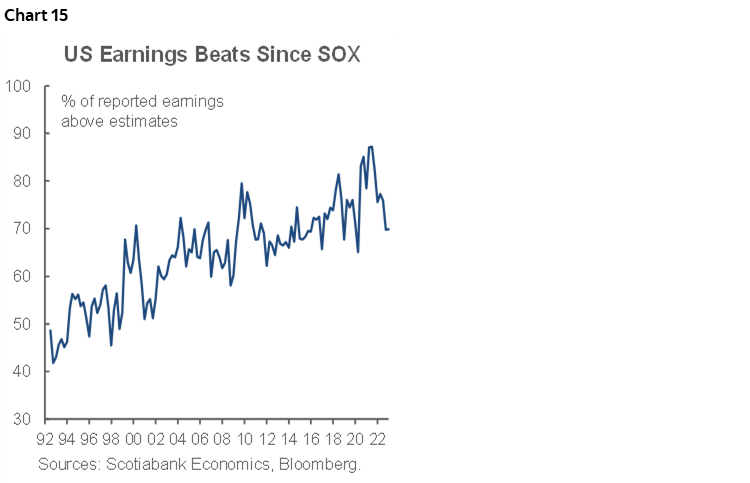

One is the usual focus on the latest results relative to marked down expectations into the season and whether those analyst expectations went too low which is a common feature of US earnings seasons since SOX (chart 15). So far the evidence suggests this happened once more, but how evenly this cuts through the landscape will also be determined by the rest of the banks that release including next week’s results.

Second is the guidance we may continue to get on how each individual bank views the broad sector’s health from a funding and liquidity standpoint in light of recent developments. That intelligence could inform the Fed’s perspectives on credit conditions. Last evening’s publication of the Fed’s weekly figures showed that banks borrowed less from both the discount window and Bank Term Funding Program (here).

Third is the set up in their results for the Fed’s stress tests. This year’s stress tests (here) will include a market shock to the trading books of the biggest banks and the release of how each individual bank fared. This is very timely in light of market volatility and it is in addition to stress testing for a severe shock to the economy and broad markets.

Fourth is that how the banks come through those stress tests may influence the Biden administration’s push for tighter liquidity and capital stress tests and the degree of pushback that it gets.

Fifth, and perhaps most importantly, if the banks’ results and their broader conditions continue to improve then the good-news-is-bad-news angle is that the Federal Reserve is more likely to hike its policy rate at least once more and perhaps more while maintaining restrictive policy by contrast to markets that have been toying with rate cuts this year.

CENTRAL BANKS—THE WAITING GAME

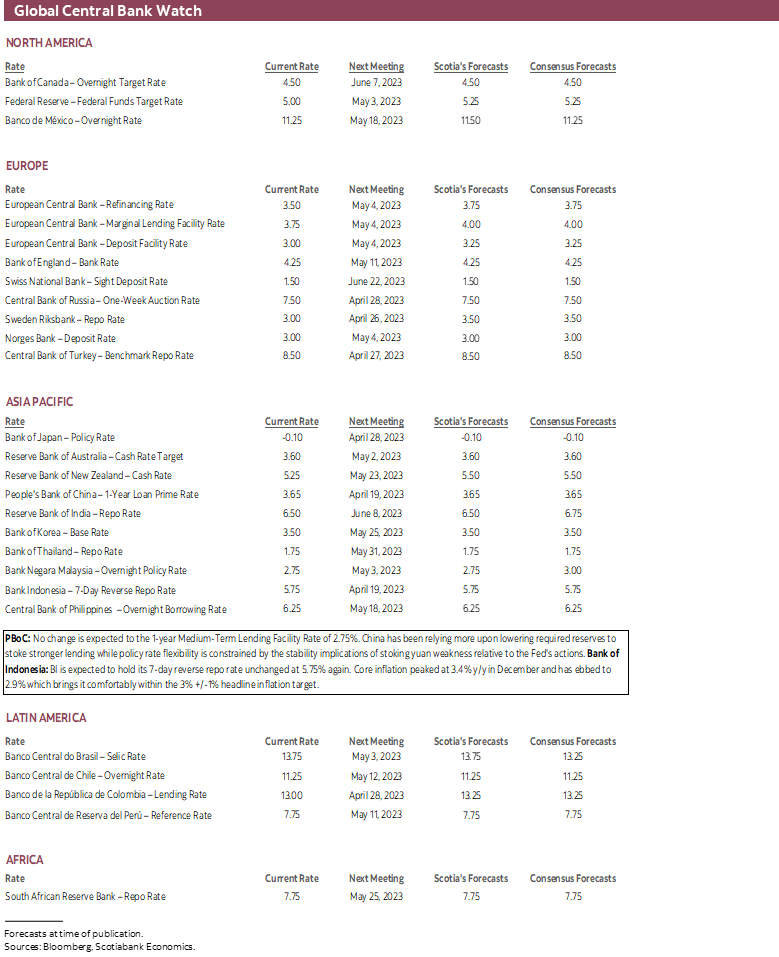

Central bankers will enter the coming week comparing notes they made at the annual IMF Spring meetings in Washington. There are few expected developments on tap as markets await the next big decisions that include the Bank of Japan on April 28th which will be Governor Ueda’s first command performance, the FOMC on May 3rd, the ECB the next day, the RBA on May 2nd and the Bank of England on May 11th.

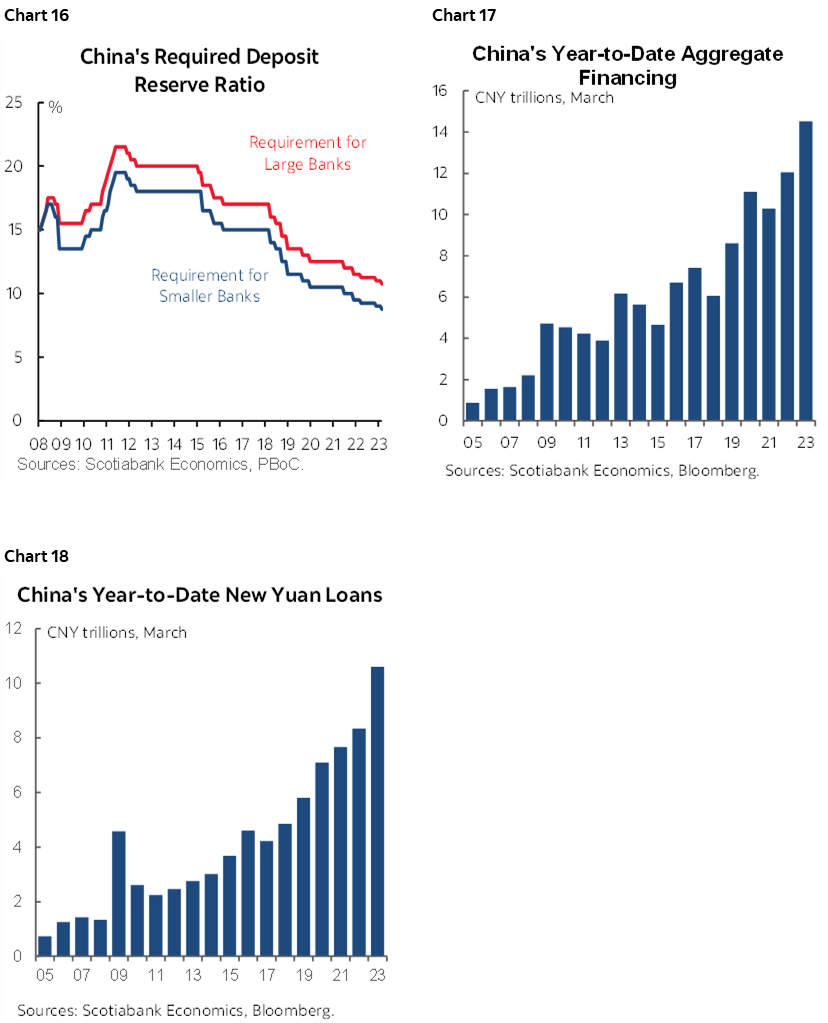

The People’s Bank of China is widely expected to leave its one-year Medium Term Lending Facility Rate unchanged at 2.75% to start the week. That may reinforce expectations for Chinese banks to leave their 1- and 5-year Loan Prime Rates unchanged on Wednesday evening (eastern time as always). Instead of stoking stability risks to the yuan and financial system by cutting rates while the Fed is likely to keep hiking, China has been relying upon relaxing lending standards (chart 16) which has stoked rapid loan growth in what is the quickest start to the new year ever (charts 17, 18). The PBoC may also be guarded with knowledge of the week’s coming indicators. Q1 GDP is forecast to rebound from no growth in Q4 to between 1% and 2.8% q/q non-annualized growth in Q1 according to consensus estimates. Industrial production and retail sales will probably post strong gains during March on Monday evening and the unemployment rate could dip.

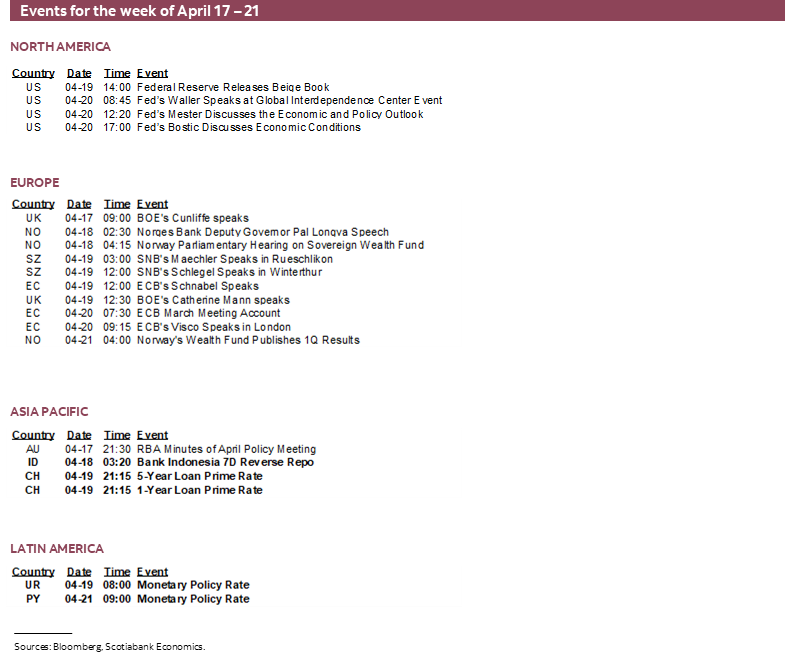

Fed-speak will return with names like Governors Bowman (Tuesday and Thursday) and Waller (Thursday), Chicago’s Goolsbee (Wednesday), New York’s Williams (Wednesday), Cleveland’s Mester (Thursday) and Atlanta’s Bostic (Thursday) and Boston’s Cook (Friday) on tap as well as Wednesday’s Beige Book. There is a variety of viewpoints among FOMC officials but much of the recent commentary has been slanted toward openness to another hike in May.

Bank of Canada Governor Macklem and SDG Rogers will appear twice before parliamentary committees on Tuesday and Wednesday (11:30amET each day). It may be unlikely that we will hear anything further after this past week’s communications including on game day when the policy statement, MPR, opening statement and press conference were offered followed by Macklem’s discussion at the IMF meetings on Thursday and then the revelation through discussion with journalists on Friday that a possible nearer term rate hike had been considered.

Bank Indonesia is also likely to stay on hold on Tuesday as core inflation comes back in line with its 3% +/-1% headline target band.

Minutes to the RBA’s meeting on April 4th will arrive on Monday evening.

THE REST!

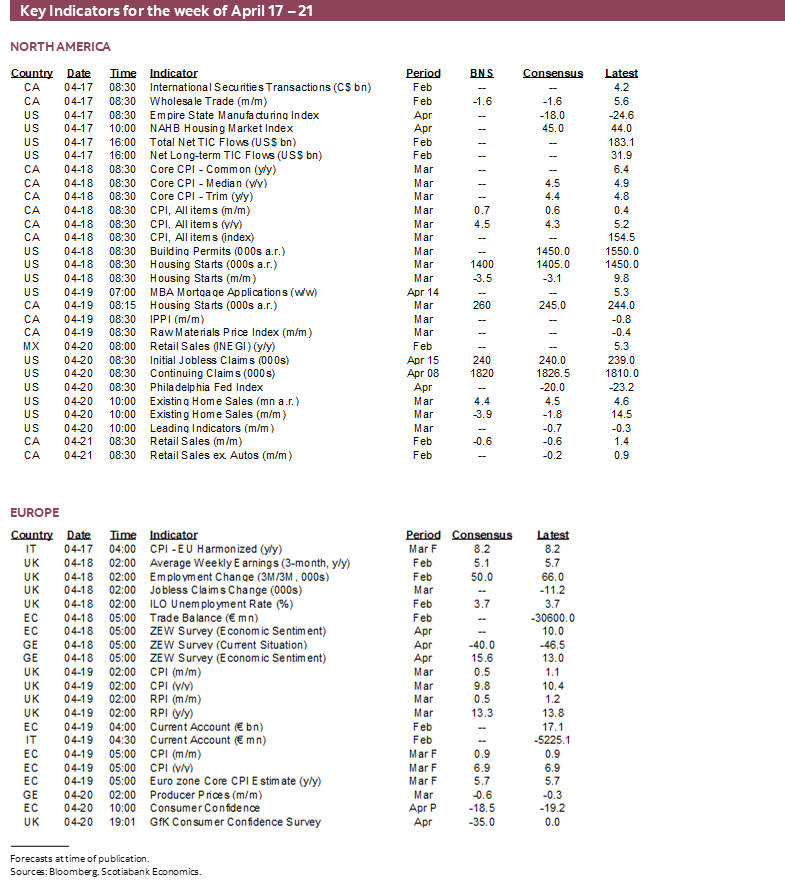

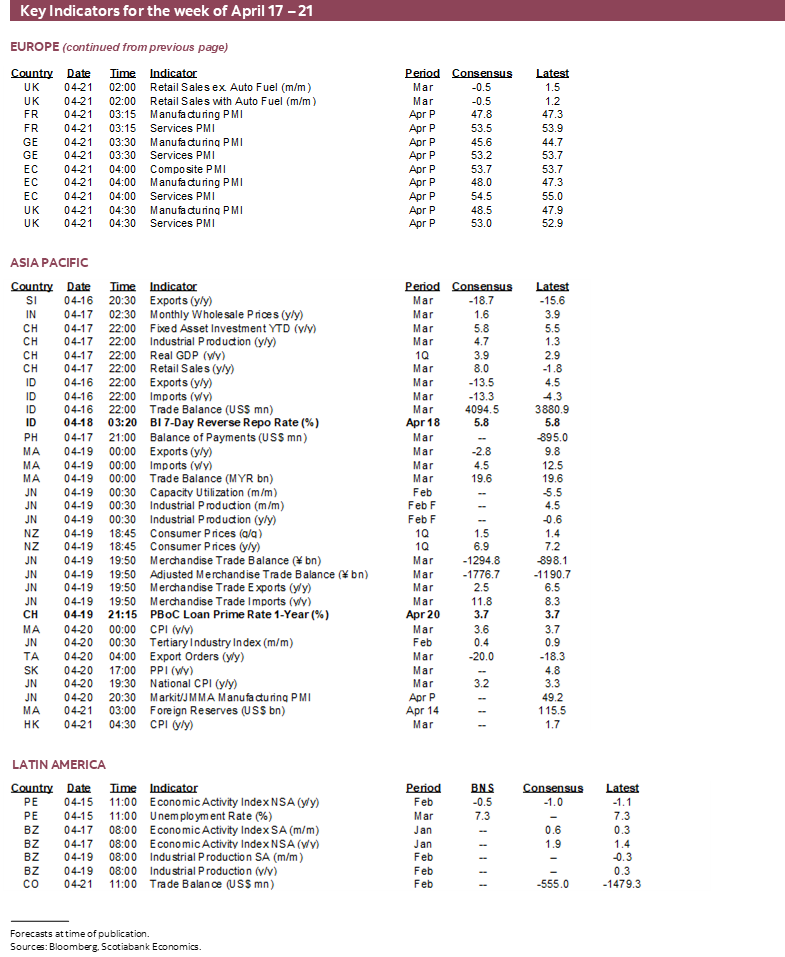

There will be an active fundamentals calendar over the coming week and beyond what has already been covered. At the top of the list are global PMIs, UK and Japanese inflation, UK job market conditions and updates on the Canadian consumer.

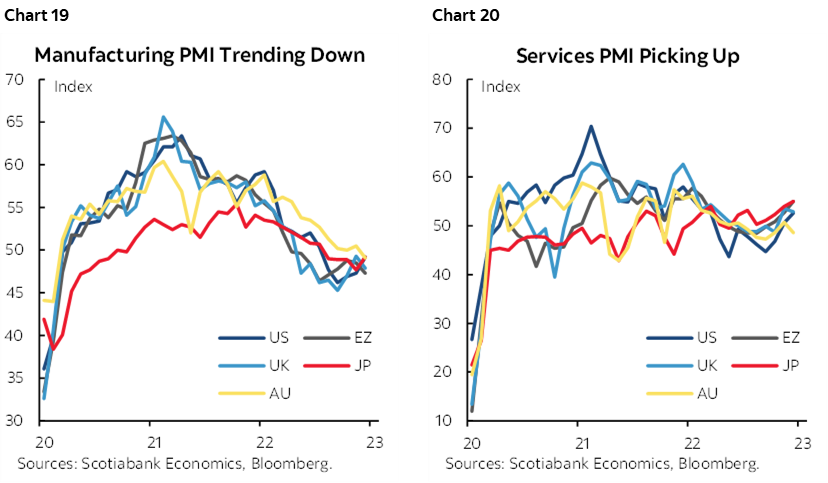

Global purchasing managers’ indices are useful gauges when it comes to estimating current quarter GDP growth as shown in charts 19–20. They can also inform inflation tracking, hiring appetite and production plans. Australia and Japan will update theirs on Thursday followed by the Eurozone, UK and US gauges on Friday.

The UK will also deliver a round of monthly updates for total employment and wage growth in February, payroll employment in March, and retail sales in March (Friday). Significant gains in jobs, a moderation of wage growth, a drop in retail sales and firm but softer inflation figures are expected. The UK, like many other global economies, still has high job vacancies (chart 21).

Inflation reports will be delivered by the UK (Wednesday), New Zealand for Q1 (Wednesday), Japan (Thursday) and Malaysia (Thursday).

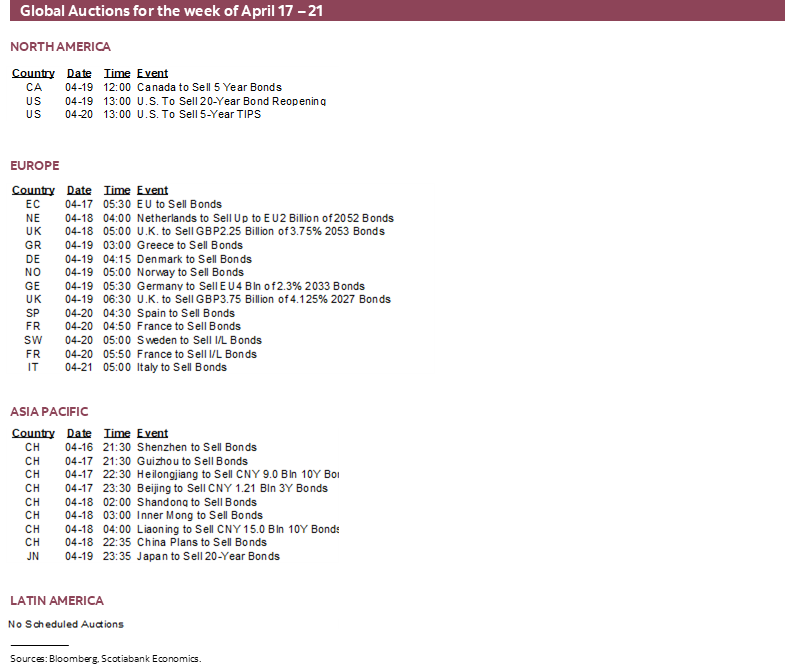

Canada will primarily focus upon CPI, but there will be a few other reports to consider. We already have advance guidance from Statcan that retail sales slipped in February so I went with -0.6% m/m, but key will be volumes and preliminary March guidance amid evidence of a robust travel season. Housing starts during March (Wednesday) might get a lift from permits and wholesale trade during February (Monday) expected to fall by 1.6% m/m round out the reports. As I write this, summer has broken out in Springtime at least in the Toronto area and right in time for the April reference week for jobs and with perhaps positive effects on spending related to outdoor activities which could make for upside risk into Spring data.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.