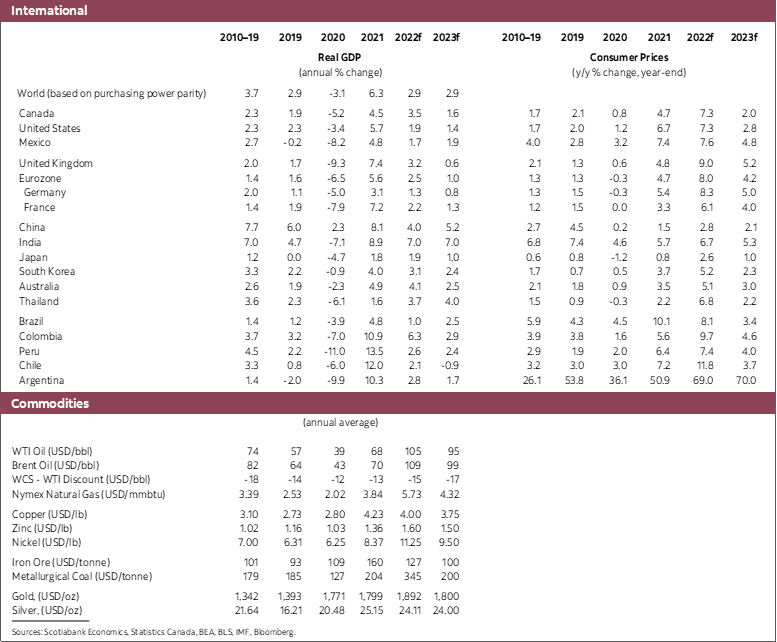

- Global economic activity is weakening as a result of COVID policies in China, still high energy prices, expectations of higher interest rates and the associated rise in the risk of recession in key economies.

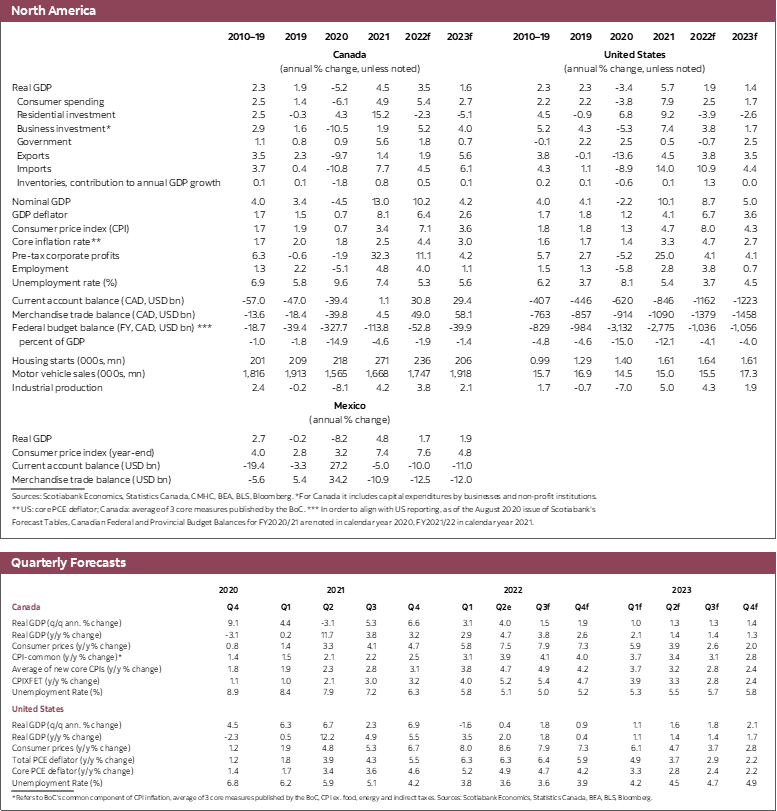

- We are marking down our forecasts for growth in Canada to a still healthy 3.5% in 2022 and 1.6% in 2023. Record levels of pent-up demand are expected to keep household consumption spending elevated despite rising interest rates, low consumer confidence, decades-high inflation, and weaker financial markets. This pent-up demand is expected to keep the Canadian economy from going into recession.

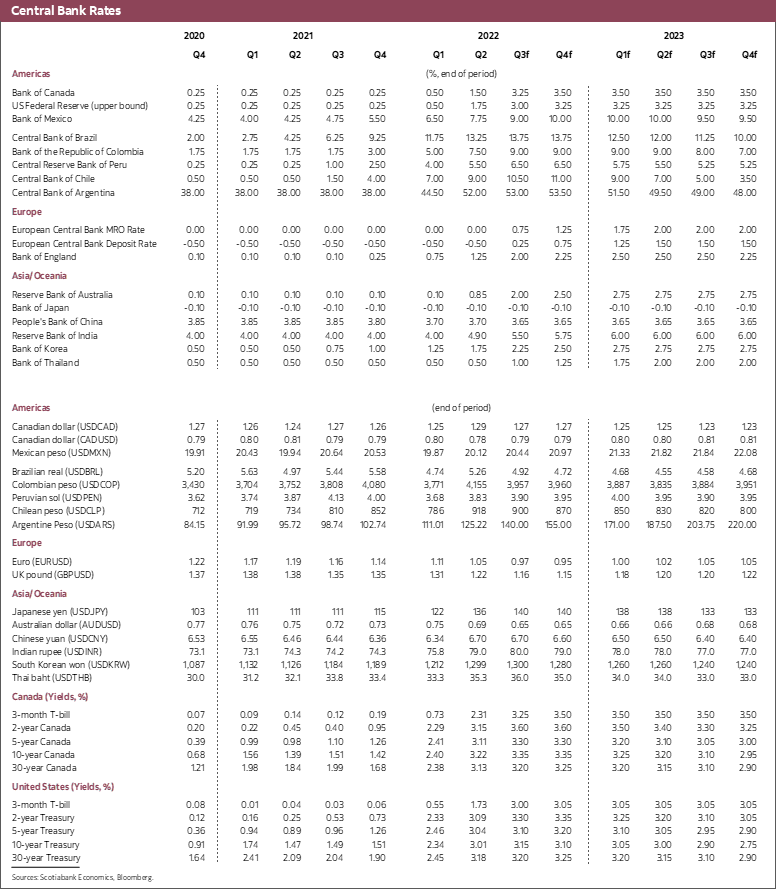

- We now expect the Bank of Canada’s policy rate to peak at 3.5% later this year and remain at that level through next year.

The global outlook continues to soften as the interaction between financial markets and the real economy clouds the outlook for both. The impacts of the lockdown in China are having a depressing impact on commodity prices that is being reinforced by worries of a potential recession in the US and, more likely, in Europe. Equity markets reflect these cyclical concerns as inflation continues to accelerate, leading to an upward revision to expected rate paths in a large number of countries. We now expect global GDP growth of 2.9% this year and next. We are revising our inflation outlook owing to evidently greater inflationary pressures in the data observed so far in 2022. Our base assumption remains that a recession is avoided in Canada and the United States, but clearly the risks of a recession have risen. Key to our assessment of these risks lies in the state of consumer spending and how that responds to the various drivers of household behaviour.

In Canada, we continue to believe there is a historically high level of pent-up demand on the household side. This forms the basis of our view that real GDP will rise by 3.5% this year and 1.6% in 2023 as this pent-up demand is multiple times higher than what we have observed over history and reflects a number of fundamental drivers of consumption over the last year, in addition to an interruption of spending patterns that occurs, and persists, because of the pandemic. The strength of this pent-up demand likely explains some of the resilience in consumer spending in the face of a very sharp drop in consumer confidence, the loss of purchasing power coming from higher inflation and of course higher interest costs. These important headwinds to household spending will hold back the pace at which this pent-up demand is resolved, but we predict that pent-up demand will prove to be the more powerful driver of consumption through 2023.

Evidence of this behaviour is perhaps most visibly seen in discretionary spending categories. This type of spending is usually the first to be foregone when households watch their expenses. Travel and food purchased from restaurants are perhaps the most vulnerable spending categories to households managing their expenses. Yet, at a macro level, these expenditures are rising at a rapid pace. OpenTable reports that seated diners in Canadian restaurants have continued their rebound and were 20% above 2019 levels as of July 16. The pace of rebound has accelerated through all of the BoC’s rate increases so far. For travel, the Canadian Air Transport Security Authority reports the number of screened travellers has risen very rapidly this year, yet volumes from June onwards still only stand at around 80% of total passengers screened in 2019. Again, these data suggest no impact yet from higher interest rates or concerns about the cost of living and are all the more striking given the evident hassles and frustration with travels these days.

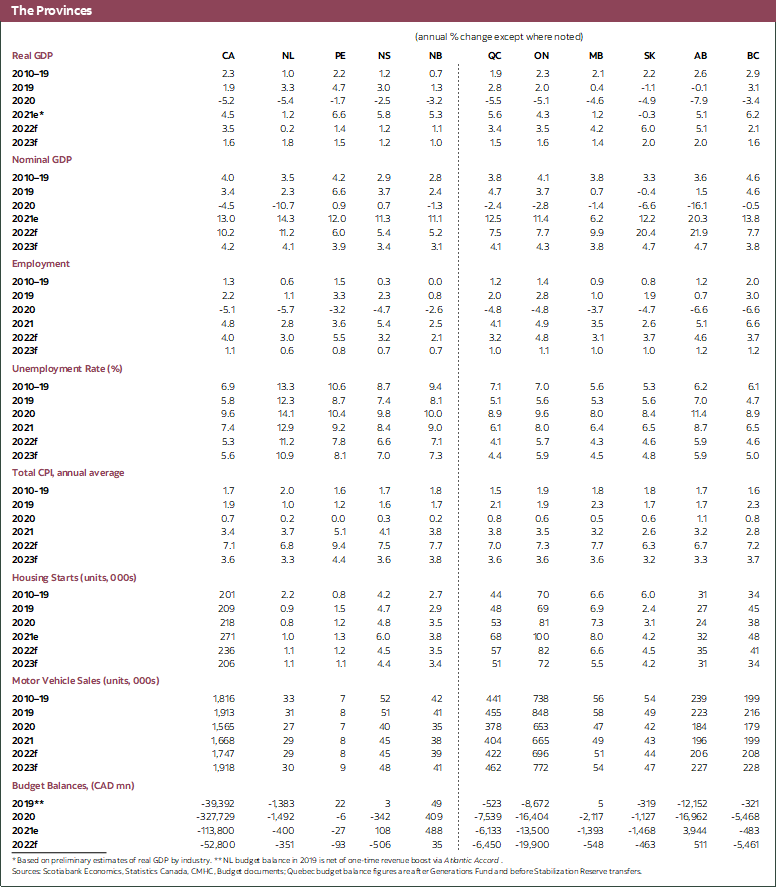

Despite this resilience, there is no doubt that rising costs, worries and higher interest rates are eating into consumer demand. We expect consumption growth to slow substantially as pent-up demand is satiated in 2023, but the activity seen so far would undoubtedly be higher if the inflation and rates outlook were different. This is abundantly evident in the housing market, where activity is slowing rapidly in response to higher interest rates, with higher mortgage rates further reducing affordability. So far, the adjustment in the housing market has been relatively smooth with local markets returning to more balanced conditions and prices falling somewhat. Lower prices and their impact on household wealth are built into our view of household spending, but prices remain well above year-ago levels.

Inflation remains a problem almost everywhere in the world. In Canada, we anticipate inflation will average 7.1% this year, with monthly inflation likely peaking in July. Inflation is then expected to “slow” to a still above target, and above consensus, 3.6% in 2023. A broad range of supply chain indicators and input prices suggest inflation will cool in coming months. Yet, despite that and a marked downward revision to the growth outlook, incoming inflation has been hotter than anticipated and wage pressures suggest that inflation will be stronger than earlier anticipated in 2023. Unit labour costs, a key factor driving inflation in our models (see here and here), are rising at the most rapid pace since 1991. The extreme tightness of the labour market, in which the unemployment rate is at the lowest level since 1970 and job vacancies continue to hit record levels, suggests that the rise in wages has some ways to go. Moreover, as confirmed by Governor Macklem in his latest decision, inflation expectations are problematically high. We had come to this conclusion in March.

Given the more persistent strength of inflation, we now forecast that the Bank of Canada will raise its policy rate to 3.5% later this year and keep it there through 2023. This is 50bps more than our last forecast. Higher interest rates than that do not appear necessary at this point, and we don’t subscribe to the view that the Bank will raise rates above that level only to cut them in 2023.

As noted above, we remain of the view that a recession will be avoided but risks of a recession are material. Higher inflation associated with a resurgence of supply chain challenges, weaker equity markets and higher interest rates than forecast are potential triggers. Should a growth recession occur, we believe it would be relatively mild given the historical strength of both corporate and household balance sheets and the incredible strength of the labour market. It has been so difficult for firms to attract and retain workers that we consider it likely that firms would choose to hold on to workers through a mild contraction in output rather than risk losing those workers permanently. Moreover, the more than a million job vacancies suggest firms would likely start by scaling back hiring plans before we observe significant job cuts at the national level.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.