- Our forecasting approach is based on a sophisticated macro-econometric model of the Canadian economy. We regularly add to this model to increase our ability to understand current and prospective developments. Given the importance of inflation and labour market dynamics in recent months, we are updating our approach to include forecasts of wages and unit labour costs. In our model, wages impact inflation through their impact on unit labour costs, which then ultimately impacts our rate calls.

- In 2022, we forecast that total compensation per hour worked will grow by 4%. This is well below our inflation forecast of around 6% for the year and falls farther short of economic fundamentals when incorporating expected productivity gains.

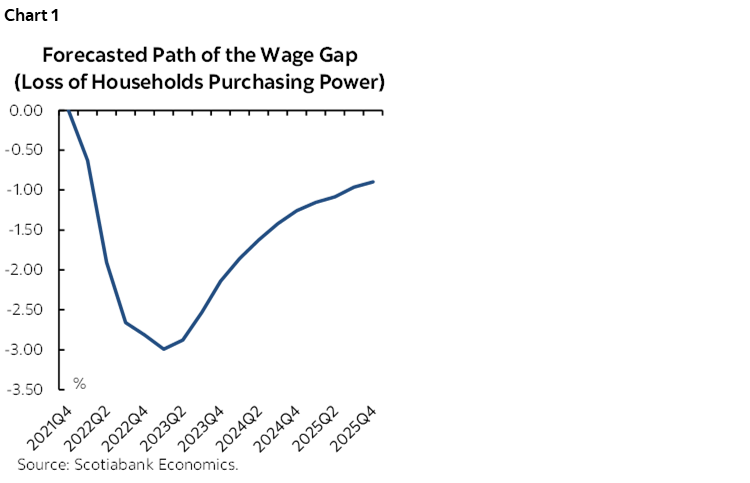

- Therefore, we forecast an important and persistent 3% deterioration of the household net purchasing power and an increase of the net cost of living that will continue beyond 2023. This may justify temporary provincial and federal income assistance targeted mainly to low-income households.

- We anticipate that total compensation per hour worked growth will accelerate to around 6% in 2023 to partially close the wage gap with inflation and productivity. Starting in 2023 this wage catch-up will generate additional inflation pressures which, other things being equal, forms part of the basis for our view that an aggressive tightening of monetary policy is required by the Bank of Canada.

I. CONTEXT

Strong demand, covid-related supply constraints and bottlenecks, and elevated commodity prices all contributed to a significant and persistent rise of inflation. In our latest published forecast, we expect that total CPI inflation will average 5.9% in 2022 and 3.1% in 2023, despite an expected notable tightening of US and Canadian monetary policies. In a recent note we showed that inflation expectations have become de-anchored from the Bank of Canada’s target and will remain so for at least the next two years. This context gives rise to two important questions regarding the interaction between inflation and wages. First, given high inflation, what will happen to the purchasing power of households? Will wages rise sufficiently to cover the inflation and expected productivity gains? Second, how will the evolution of wages contribute to inflation in the forthcoming years? In this note we build a model that allows us to try to answer these important questions.

II. THE MODEL AND OUR APPROACH

We build a model that forecasts total compensation per hour worked, labour productivity and unit labour cost. In line with mainstream economic theory, we assume that total compensation reflects labour productivity gains and inflation in equilibrium. In our model, total compensation and wages also react to the state of demand in the labour market proxied by the unemployment rate gap and to the supply of labour proxied by the NAIRU. Our Canada/US large macroeconomic model provides the forecast for CPI inflation, unemployment rate gap, NAIRU and total production. For more details on our model see the Appendix.

The model allows us to forecast what we call the wage gap, which is equal to total compensation per hour worked minus total CPI and minus labour productivity. This wage gap captures the evolution of the net purchasing power of the household. If the wage growth is not sufficient to cover inflation and the productivity gain, relative to equilibrium, the households are losing purchasing power and the effective cost of living is going up. In our core CPI Phillips curve, inflation is a function of the growth of unit labour costs which is equal to wage growth minus labour productivity growth, both forecasted by our model. Therefore, the model also allows us to capture the wages pressure on inflation to shed some light around the two questions asked in this note.

III. RESULTS

Table 1 shows the forecasted growth for total compensation per hour worked given by the model and compares these forecasts with our total inflation forecast. In 2022 this approach suggests that total compensation per hour worked will grow by around 4%. This does not to cover the inflation (5.9%), much less inflation and the expected productivity gains. This opens an important and persistent negative wage gap of 3% (see chart 1) that culminates in 2023Q1. Our results suggest that total compensation growth will accelerate to around 6% in 2023 to partially close the wage gap. Therefore, we anticipate a significant and continuing deterioration of the household net purchasing power and an increase of the net cost of living that will persist until 2023 and beyond.

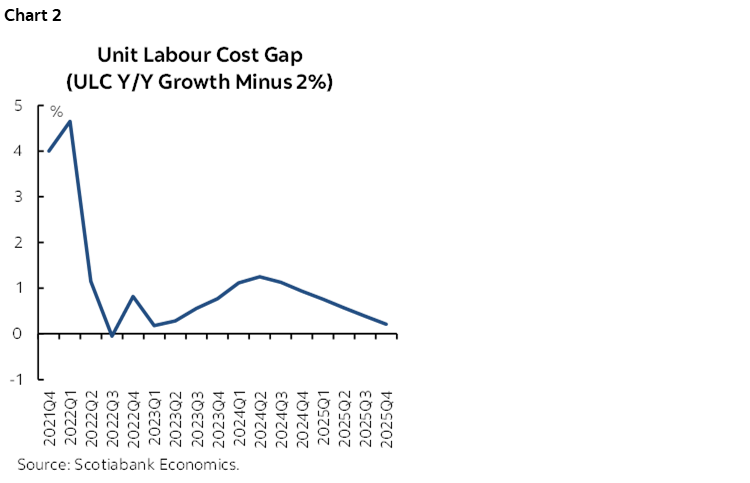

Chart 2 shows the forecasted path of the growth rate of unit labour cost (Y/Y) minus 2% (the inflation target) which is the wage variable that feeds the core CPI inflation’s Phillips Curve in our large Canada-US macroeconomic model. Wages should add significant pressure to inflation in 2023.

IV. POLICY IMPLICATIONS

The expected loss of purchasing power by households may justify an intervention to help the low-income households adjust to rising inflation. The eventual income assistance provided by the provincial and federal governments should be temporary (because the deterioration of the wage gap is temporary) and should target the low-income households. Finally, starting in 2023, the Bank of Canada should expect inflation pressures coming from unit labour cost in the setting of its monetary policy which, other things being equal, will require a more aggressive and a faster increase of the policy rate.

APPENDIX: THE MODEL

Drivers of the variables (sign of the effect in parenthesis)

1. Total Compensation per hour worked (Productivity and Cost report)

- Labour productivity (+)

- Total CPI inflation (+)

- Unemployment rate gap (unemployment rate – NAIRU) (-)

- NAIRU (+)

- Real exchange rate (-)

2. Hours worked (Productivity and Cost report)

- Potential GDP (+)

- Output gap (+)

- Wages (-)

3. Total production (Productivity and Cost Report)

- Anchored on the GDP forecast of our Canada-US large macroeconomic model

Note that the combination of total compensation per hour worked, hours worked, and production forecast give us the labour productivity forecast and, therefore, the forecast of unit labour cost. Also, the forecast of CPI inflation, unemployment rate gap, output gap, potential GDP and the NAIRU come from our forecast based on the Scotiabank Canada/US macroeconomic model.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.