- Canada’s federal Finance Minister is expected to table a budget in the coming weeks.

- Hopefully all of the “surprise” factors are already on the table with the new Liberal-NDP Supply and Confidence Agreement announced this week adding more upside to spending expectations.

- The Liberals had already channeled their intentions to execute on remaining election pledges (in the order of net new spending of $56 bn by FY27). The new pact—once netting out what the Liberals had planned to do anyway—likely adds another $15–20 bn over the life of the 3-year agreement and potentially $40 bn by FY27. Tack on another $12 bn (at least) for potential defense spending top-ups.

- Stronger-than-anticipated revenue performance should mask most of this new spending in the near term with a deficit path that largely mirrors the Fall plan, but consolidation starts looking fairly flat (around 1% of GDP) over the medium term. The new pact alone possibly adds a half of a percentage point to structural deficits over this horizon, notably by locking in commitments to universal pharma and dental programs.

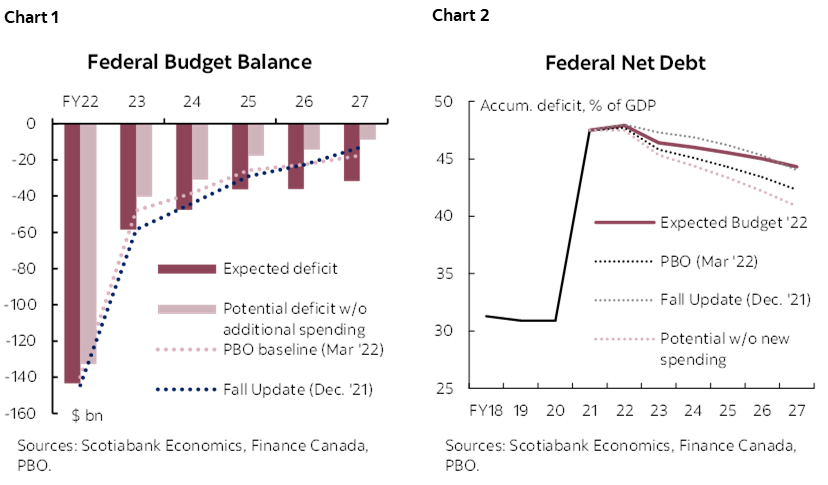

- Absent additional spending, the budget could have reasonably approached balance over the planning horizon (chart 1).

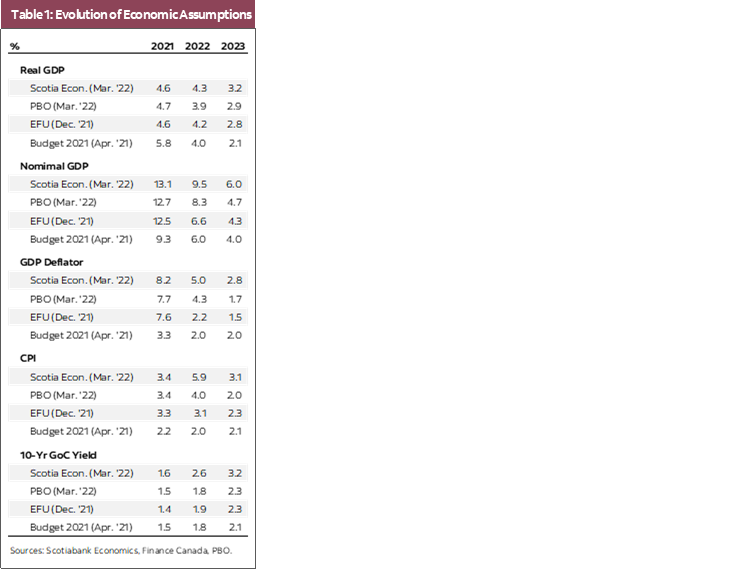

- Canada’s federal net debt should still slope downward but its trajectory would likely soften over the horizon (chart 2).

- While individual measures are relatively small and mostly targeted in the near term (and with some merit to support those hit hardest by inflationary impacts), the aggregate sends a message that spending is here to stay.

- The stakes are high with monetary policy behind the curve and inflation expectations unanchored. The Finance Minister risks further undermining Ottawa’s credibility in its commitment to tackling inflation.

MANY MOVING PIECES

The bottom line may not look a lot different when Canada’s federal budget is tabled in a few weeks, but it will likely mask a variety of drivers. We expect similar deficits relative to the December Economic and Fiscal Update (Fall update) in the near term as stronger revenue performance is likely to be absorbed by additional spending, notably remaining election platform commitments, new commitments under the recent Liberal-NDP Supply and Confidence Agreement, and a possible top-up to defense spending. The net impact should still drive another sharp taper in the FY23 deficit to about -2.2% of GDP (from an estimated -5.8% in FY22 ), followed by gradual tightening thereafter to about -1.0% of GDP by FY27 instead of the earlier-projected -0.4%. Absent incremental new spending, the fiscal path could have reasonably approached balance by FY27 especially once even-stronger nominal growth is factored in.

Anticipated budgetary developments reinforce our outlook for the Canadian economy. The Canadian economy is at capacity, inflationary pressures are mounting, and expectations are becoming unmoored as policymakers scramble to catch up with reality. Incrementally more spending—even if merited in some cases—complicates this picture. The budget is likely to add more conviction to our outlook that monetary policy will need to shoulder the brunt of reining in inflation.

HEISENBERG’S UNCERTAINTY

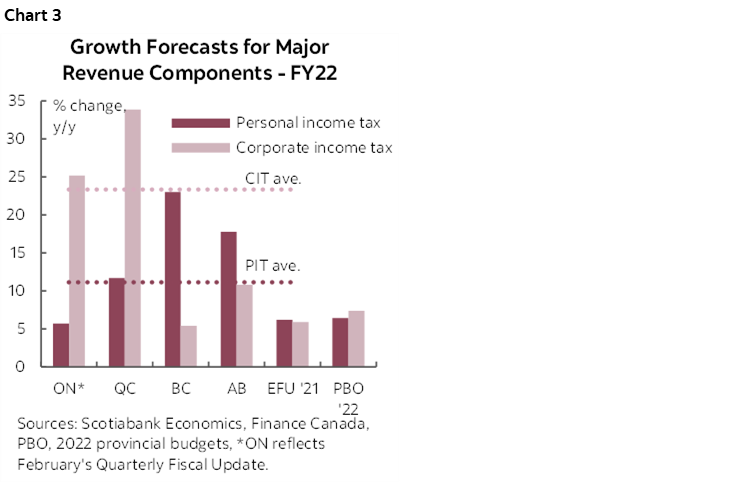

Economic assumptions will be woefully stale by the budget’s press time. Consensus forecasts from early February (that will inform this budget) won’t reflect recent developments related to the conflict in Ukraine which are likely to further fuel inflationary pressures. And recall consensus views in the Fall update still reflected a rather sanguine view on inflation. The Parliamentary Budget Officer (PBO) budget baseline from earlier this month also appears to underestimate these impacts (Table 1).

Scotiabank Economics has consistently led Bay Street in signalling the persistence of inflationary impacts. While there is less divergence around real GDP outlooks, Scotiabank’s nominal GDP growth outlook for 2022 (9.5%) is currently 2.9 ppts higher than the Fall outlook and 1.2 ppts higher than the PBO. The gap persists through 2023 with Scotia’s 6.0% nominal GDP growth forecast 1.7 ppts and 1.3 ppts above the Fall and PBO outlooks, respectively.

Not all of this will likely be baked into the economic baseline. A combination of the time lag along with trailing consensus suggests that the budget baseline economic assumptions could resemble the PBO’s assumptions with potential for upward revisions down the road.

MORE REVENUE TAILWINDS AHEAD

Inflationary pressures are likely to prop up government revenues. With parameters of personal income tax indexed to inflation, higher government revenue growth will likely dominate other drivers including inflation-linked expenditure pressures. Finance Canada’s sensitivities suggest a sustained 100 bps shock to GDP inflation could drive up revenues by $3.9 bn in the first year, only offset partially by expenditures linked to inflation (-$1.7 bn) for a net $2.2 bn improvement.

Even the PBO’s rather complacent view of inflationary pressures suggests material revenue windfalls in the years ahead. The PBO’s March fiscal reset pencils in small revenue windfalls initially—$3 bn in FY22—but with strong cumulative effects that augment revenues by an additional $40 bn by FY27. Scotiabank’s more (nominally) expansive growth outlook in 2022 (FY23) and 2023 (FY24), in particular, suggests there is easily (eventually) another $20 bn in revenue windfall potential over this horizon, but this won’t likely be baked into the baseline given a likely weaker consensus outlook for nominal growth.

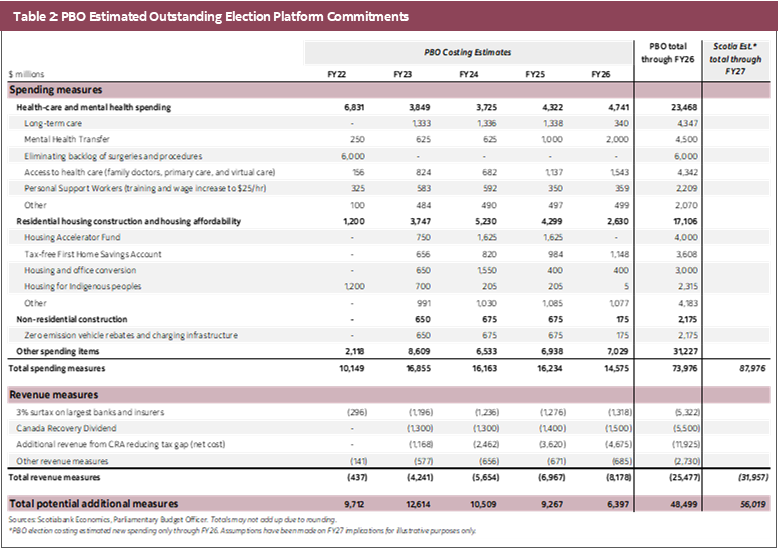

Near-term revenue momentum may be harder to ignore as FY22 comes to a close and early provincial budgets flag strong revenue tailwinds. First-out-of-the-gate budgets forecast very strong government revenue growth for the current fiscal year (FY22) including average upticks of 12% y/y and 23% y/y on personal and corporate tax revenues, respectively (chart 3). Despite a common tax base for the most part, the Fall update projected a somewhat weaker (though still strong) outlook for federal revenue growth with personal and corporate tax revenues both growing around 6% y/y. For illustrative purposes, simply applying the more recent provincial assumptions on federal growth rates suggests revenue windfalls in the order of $14 bn in FY22 alone. Even if revenue growth rates quickly revert back to historic averages, base effects from a very strong FY22 could drive cumulative (and additional) revenue windfalls in the order of $130 bn by FY27 (relative to the Fall update), but, conservatively, we assume only about half of this would be baked into the baseline in this budget.

Again, we expect a degree of conservatism would be built into revenue expectations. Our working assumption is that the budget could lay out net revenue improvements in the order of $67 bn by FY27 relative to the Fall update before new spending is incorporated.

DON’T BANK ON THOSE SAVINGS JUST YET

New spending is expected to absorb these revenue windfalls (and then some). According to the PBO’s analysis, outstanding election pledges could amount to a net $48.5 bn by FY26 (Table 2, back). We have assumed some of these commitments would impact the FY27 balance once the horizon is extended. For illustrative purposes, we assume total net new spending through FY27 would amount to about $56 bn ($88 bn in spending items and $32 bn in revenue-side measures). With notional funding set against all of these measures for FY23 (and many with funds to flow in FY22), it is reasonable to expect the bulk of promises would be set out in this budget. The government has near-promised it will execute against these earlier pledges.

The recently announced Liberal-NDP Supply and Confidence Agreement further adds to spending expectations. The majority of the 25-item list of shared priorities were already reflected in the Liberals’ election pledges, but notable concessions—namely a commitment to establish national pharma and dental programs—are material. The estimated incremental budgetary impact of the agreement (beyond prior Liberal pledges) is likely around $15–20 bn over the three-year life of the pact, while an inevitable tail to these commitments would likely put the 5-year total closer to $40 bn. The phased approach to the pharma commitment (costed at $11 bn/yr by the PBO once fully operational) would mitigate the near-term impacts, but the agreement could eventually add another 0.5% of GDP (~$13 bn) to structural deficits over the medium term.

The agreement also reinforces expectations that targeted revenue-raising measures would be unveiled in this budget. Recall, over 45% of the cumulative $25.5 bn (through FY26) would come from closing tax gaps (with a high degree of uncertainty around revenue potential), while another $11 bn would be raised through a 3% surtax on large banks and insurers, as well as a new Canada Recovery Dividend. The latter has been flagged in the new Liberal-NDP shared priorities, just as the NDP is pitching for an expansion of the surtax’s base to capture more businesses. The government has so far resisted calls for a more comprehensive review of Canada’s tax architecture that could achieve multiple objectives including enhancing growth, removing inefficiencies, and redistributing wealth (or rebuilding fiscal buffers). At best, this is likely a missed opportunity to launch an independent process with multi-party support. At worst, a more punitive and targeted approach towards markets could erode confidence at a time when a rotation to business investment is critical to Canada’s medium-term growth outlook.

Tallying it up, the net impact on the bottom line over the horizon (FY27) could be around $42 bn in net new budgetary spending. This includes potential new spending in the order of $140 bn ($88 bn in remaining Liberal platform commitments once the horizon is extended through FY27, an incremental $40 bn under the new Liberal-NDP agreement, and a $12 bn defense top-up) along with net revenue impacts in the order of $100 bn ($33 bn in revenue-raising measures along with $67 bn improvements reflecting revenue windfalls).

WHAT (ELSE) IS LIKELY IN

The challenge for policymakers across the country and around the world has been shifting focus from the urgent (health) to the important (long-term growth). This budget will likely be no exception. Health-related spending comprised almost a third of outstanding Liberal platform pledges ($23 bn/ 5 years) including a one-time $6 bn transfer to provinces for surgical backlogs, and over $12 bn to mental health, access to care, and long-term care. The new Liberal-NDP agreement vaguely recommits to these priorities, but wording appears to be less firm (or mostly silent) on united calls from provincial leaders for a sizable increase to the Canada Health Transfer (starting at $28 bn/yr). This budget is not expected to tackle this issue.

Affordability—housing in particular—is expected to be another central plank of the budget. Election pledges laid out $17 bn (5 years) in new spending for housing affordability measures including $4 bn for a Housing Accelerator Fund and $3.5 bn for a Tax-Free First Home Savings Account. Recall, the Liberals had set a target to build or repair 1.4 mn new homes over 4 years. The agreement likely adds a couple of billion in the near term to this priority including extending the Rapid Housing Initiative and topping up the Canada Housing Benefit. Supply-side measures should help address shortfalls, but are unlikely to do so in a timely manner to tamp down near-term inflationary pressures. Some measures could actually fuel housing demand on the margins—including the doubling of the Home Buyers Tax Credit and a 25% reduction in CMHC mortgage insurance costs—working against the Bank of Canada’s efforts to rein in price appreciation.

Other affordability measures are likely to receive substantial airtime. There were a number of smaller election promises that targeted lower-income households including an expanded Guaranteed Income Supplement for low-income seniors, an enhanced Canada Worker Benefit, and a new disability benefit, among other targeted provisions. Measures in isolation are relatively small and there is clear merit in protecting the most vulnerable, but the aggregate signals a clear spending bias at a time when policymakers’ inflation-tackling credibility is fragile. The government walks a fine line to the extent it tries to offset impacts on those hardest hit by escalating prices for essential goods given the potential for unintended consequences that could make matters worse by fueling further price escalation.

Finally, the government’s green transition agenda is expected to be showcased in the context of economic growth. Plans are already largely set out against Canada’s legislated net zero target of 2050 (and its interim 2030 target) through a combination of carbon taxes and targeted investments. The first Emissions Reduction Plan is expected later this month. The budget is likely to layer onto these plans with additional funding for the Net Zero Accelerator Fund, expanded EV rebates and charging infrastructure investments, as well as details around forthcoming clean tech tax incentives. With governance presently at the core of global energy market discourse, we will be watching for any shift in tone, at least, as to positioning Canada’s energy sector in this rapidly evolving global context.

It is not evident that there will be any game-changers on the growth front. It is arguably not for a shortage of ideas (this shop, for example, put forward a bold, yet simple, approach to financially incentivizing provinces to reduce interprovincial trade barriers), rather it is likely a question of bandwidth given the vast array of priorities and a predilection for redistribution policies.

MARKETS RIGHTLY DISTRACTED

The anticipated deficit path should put net debt on a firmly downward trajectory. The federal accumulated deficit should peak just shy of 48% of GDP this year (FY22)—roughly in line with the earlier outlook landing around 44% of GDP by FY27. A declining debt trajectory is likely to remain the loose fiscal anchor.

A higher interest rate environment will put upward pressure on debt servicing costs but these are still expected to remain low by historic standards. Debt servicing costs currently sit at around 0.9% of GDP. The Fall update projected the share to grow to 1.3% by FY27, whereas the PBO projects it closer to 1.5% over that horizon. Incorporating a higher interest rate outlook could push this closer to 1.7% of GDP, all else equal, but this is still well-below historic highs above 6% of GDP. Note, we have not made substantial adjustments to net budgetary impacts as a result of higher interest rates given lower actuarial provisions for future liabilities would likely offset projected debt service cost increases.

Borrowing requirements may shift modestly largely owing to non-budgetary factors in the near term. The Fall update had projected a financial source/requirement of $155 bn for FY22. It could be reasonable to expect TMX cost overruns to be incorporated in this current fiscal year (in the order of $10 bn). With the budget expected to set out FY23 borrowing requirements, another net $20 bn could be added to the earlier financial source/requirement of $64 bn projected in the Fall update to account for reprofiled repayments related to CEBA loans (while lowering FY24 projections by a commensurate amount). This would add to incremental market supply in the order of $64 bn and $88 bn in 2022 and 2023, respectively, from the anticipated roll-off of government bonds from the Bank of Canada’s balance sheets.

Nevertheless, markets will likely be preoccupied with global developments when Canada’s federal budget is tabled. Notably, the Russian invasion of Ukraine is compounding inflationary pressures and is driving mostly hawkish interpretations for central banks’ reaction functions that is putting upward pressure on bond yields around the world. In the near term, risk sentiment and the timing of policy rate changes will likely add to volatility and drive relative shifts, while economic and fiscal fundamentals may matter more over the medium term. In this context, we anticipate the budget would likely reinforce drivers behind our rate outlook for Canada including a widening in the differential with the US with potentially more upside risk related to greater supply signalling.

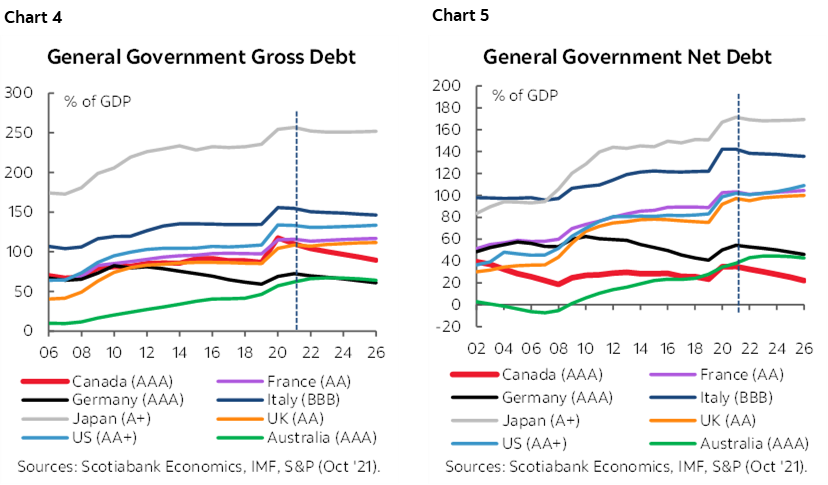

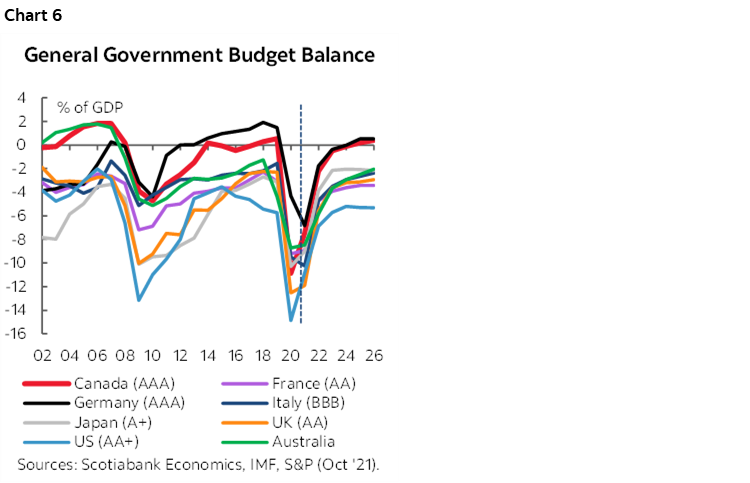

Canada’s fiscal fundamentals are still attractive, but expect some warning shots from rating agencies. Canada’s general government gross and net debt levels (i.e., federal and provincial debt net of financial assets) confer an advantage over most peers (charts 4 & 5), while stale data from the Fall do not yet reflect even sharper consolidation among provinces which hold about half of Canada’s government debt. On a flow basis, Canada’s higher discretionary spending (and consequent faster clip of consolidation) relative to most peers places its debt on a slightly more favourable trajectory (chart 6). On most metrics, Canada is rivaled only by Germany, which is set to launch a major new spending package later this Spring. The impact of the Ukrainian invasion is also likely to reinforce divergences in growth outlook along regional and commodity-dependence factors. Nevertheless, Canada’s lack of reserve currency status puts a lower tolerance on debt levels that limits the usefulness of such comparisons, while rating agencies (but not likely markets) could raise eyebrows at adding more structural spending without offsetting growth expectations.

BOTTOM LINE

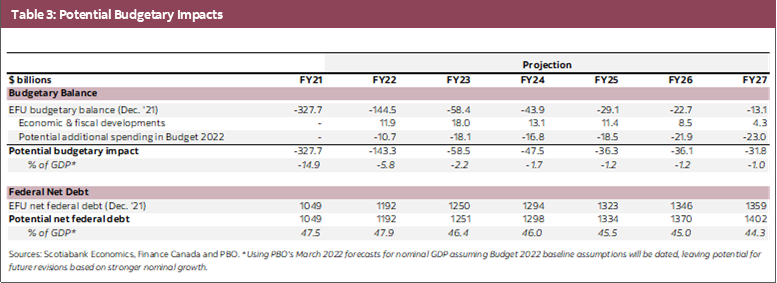

More spending has been signalled in the lead up to this budget. Near-term impacts on the bottom line may be masked by strong revenue performance, but the pace of consolidation would slow considerably over the horizon if and when more spending is incorporated into the baseline. See Table 3 (back) for our best guess on the fiscal path in the upcoming budget. With no budget day set, yet there is still potential for more announcements to come. On balance, we think there is more downside risk to this outlook (i.e., higher spending and/or more conservative revenue assumptions). Watch this space.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.