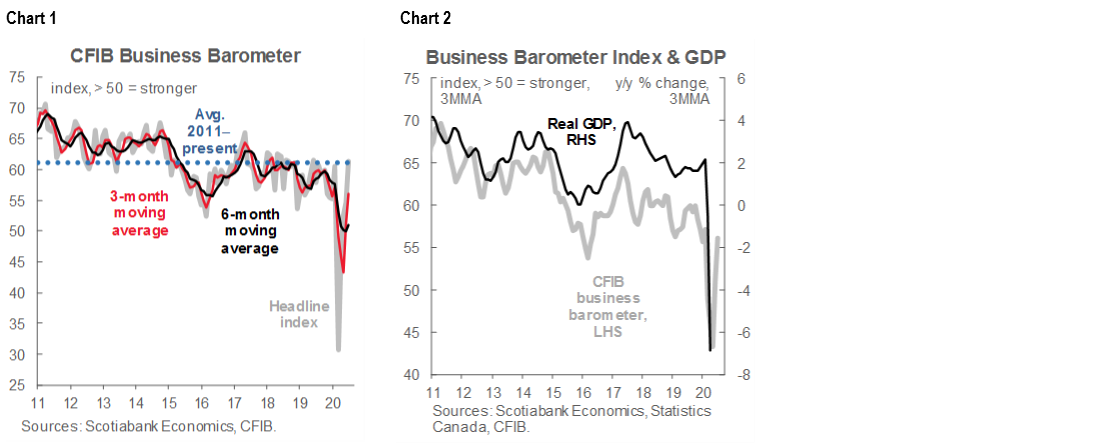

Small- and medium sized enterprise (SME) sentiment continued its recovery, increasing 6.7 points to 61.3 in July.

Although the headline is more in line with its historical average, other measures are nowhere near their normal levels due to the unique characteristics of the pandemic’s economic shock.

Some possible reasons for the high index score could be that many business owners have a much lower expectation of how “good” performance will look 12 months out, resulting in the index temporarily overshooting, as well as a survivor effect with many of the weaker businesses polled pre-pandemic no longer replying in July.

SME SENTIMENT RECOVERS WHILE OTHER MEASURES REMAIN WEAK

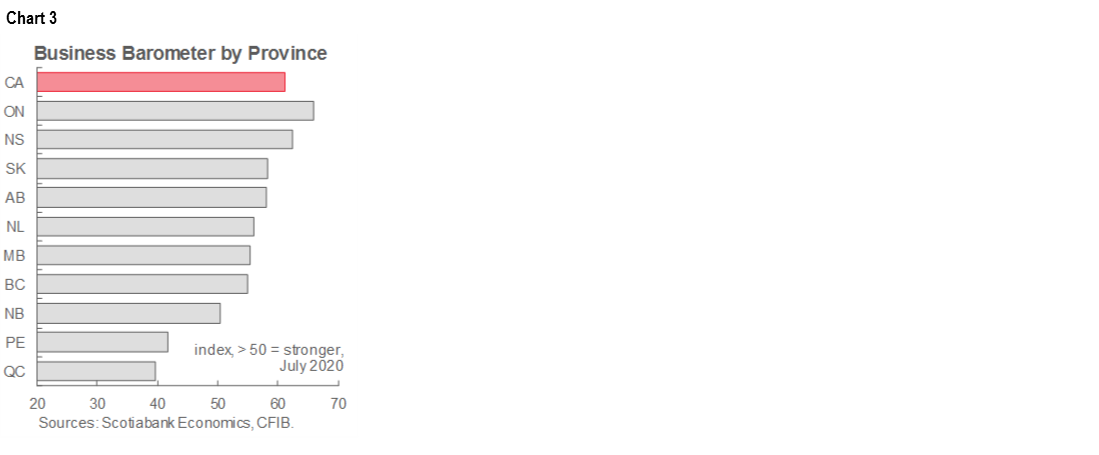

The Canadian Federation of Independent Business’ (CFIB) monthly Business Barometer Index increased to 61.3 in July, more in line with its historical average (chart 1). SME sentiment is normally a leading indicator of economic activity, supporting what looks to be a bounce back in Q3 (chart 2) barring any setbacks in the coming months. As governments begin to lift more restrictions, the durability of the recovery will depend on how successful the general population remains at keeping the virus at bay.

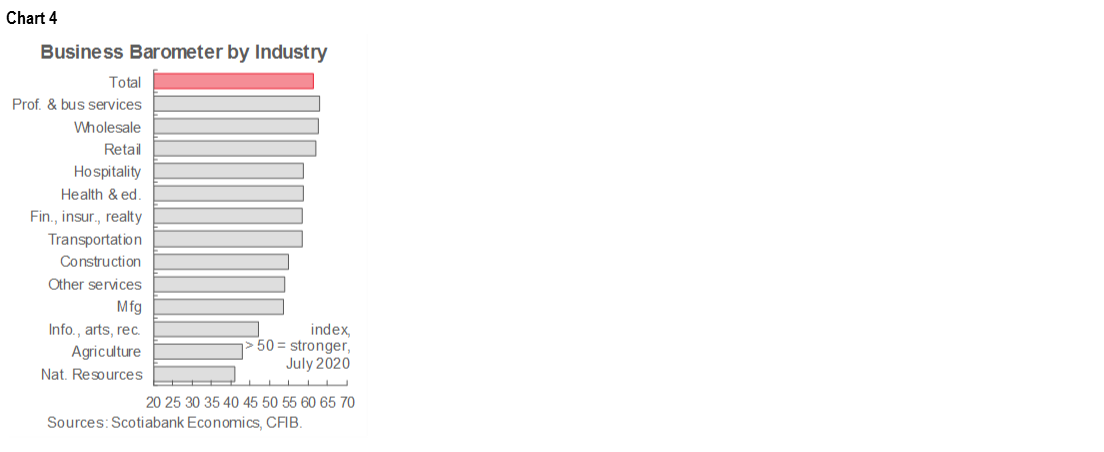

Provincial business sentiment continues to improve, with 8 out of 10 provinces now above the 50 point threshold (chart 3). Ontario posted the strongest gain in July, increasing 12.0 points to 66.0. Quebec SME sentiment increased slightly to 39.6 but remains the most pessimistic province.

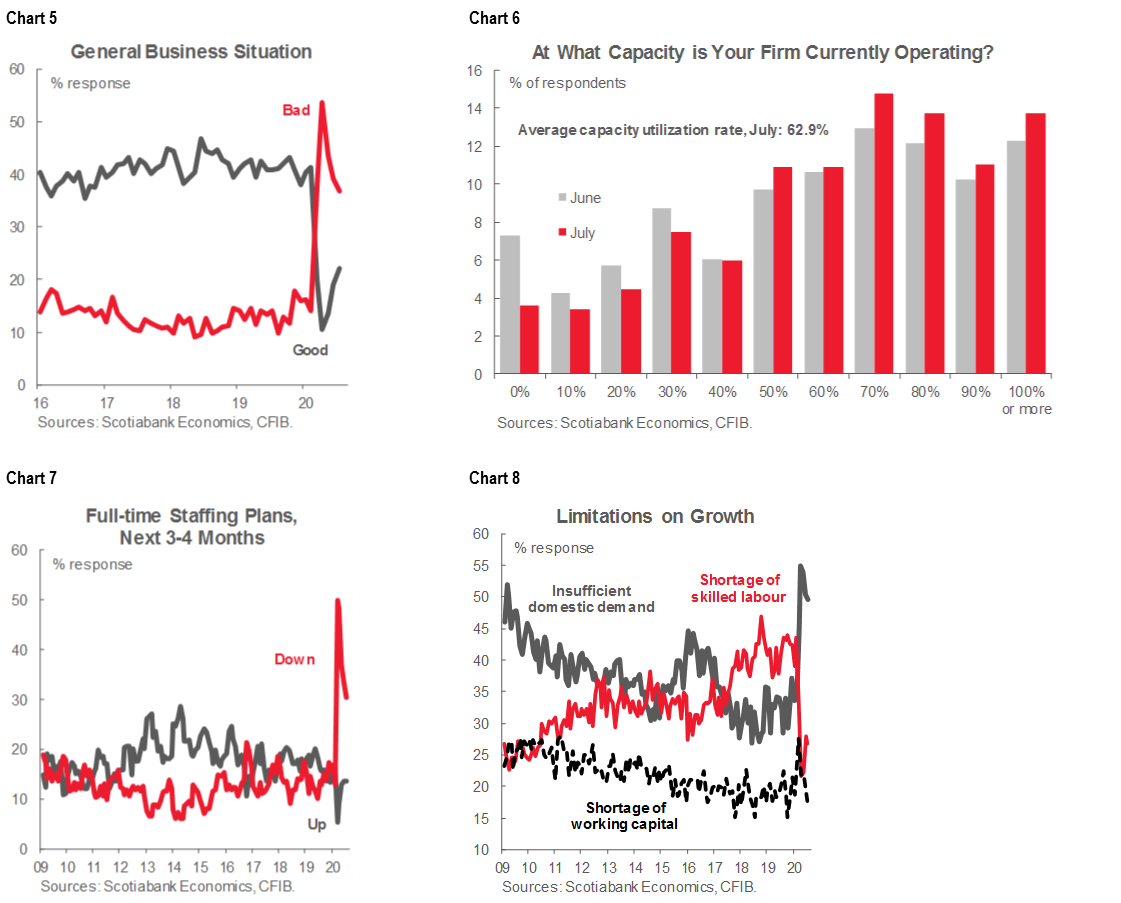

Similar to the provinces, sentiment by industry continues to improve with 10 out of 13 industries also breaking the 50 point threshold (chart 4). Professional and business services was the most optimistic industry in July but, not surprisingly, retail sales had the largest single month gain, increasing 11.3 points to 62.0 as restrictions were increasingly eased across jurisdictions. Also not surprisingly, sentiment remained weak in agriculture and natural resources, two of the harder hits industries during the pandemic.

General business indicators, though improving, remain depressed compared to historical levels. The view of the general business situation improved slightly in July (chart 5), as did the average capacity utilization rate (chart 6). However, full-time staffing plans continue to remain low (chart 7) as insufficient domestic demand remains the top concern for business owners (chart 8), casting doubt on the speed of a future recovery in labour markets. Possible reasons for the difference between the headline index level and other measures could be that business owners have lowered their expectations for what is considered as “good” performance 12 months out as well as a survivor effect with many of the weaker businesses polled pre-pandemic no longer replying to the survey in July. This could lead to a temporary overshoot profile in the index during the recovery.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.