- August’s drop and 106k lost jobs in two months is bound to catch the BoC’s attention

- The seasonally unadjusted plunge in jobs was the biggest ever for an August…

- ...but dubiously restrained by the highest SA factor on record

- Multiple counts of new information drive us to expect 50bps of BoC cuts

- Inflation risk has nevertheless not gone away…

- ...but fresh developments will pivot the BoC toward downside risks to future inflation

- Real wage gains above productivity are unlikely to be temporary, slack or not

- Canada jobs m/m 000s // UR %, SA, August:

- Actual: -65.5 / 7.1

- Scotia: 35 / 6.9

- Consensus: 5.0 / 7.0

- Prior: -40.8 / 6.9

Ouch. Canada’s job market was hit hard in August. The odds that the BoC will resume easing at the September meeting just went up. With materially fresh evidence, our revised call is a 25bps cut on the 17th followed by another in October and then hold. If they’re going to ease, then it’s totally pointless to do it just once.

66k jobs were lost in August. 106k were lost in the past two months. We can quibble about the drivers and other factors but the BoC is under significantly greater pressure to resume easing.

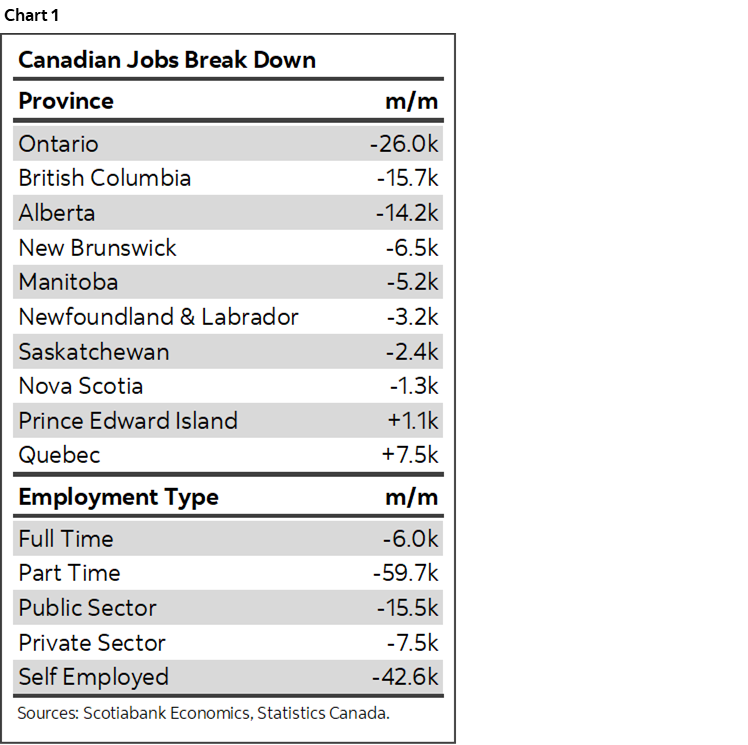

Chart 1 provides some details. It was mostly driven by a loss of part-time jobs this time (-60k) as full-time jobs were down 6k but after a 51k prior drop in f-t positions.

Most of the loss was in self-employed (-43k) which is more suspect in terms of data quality, but payrolls also fell by 23k led by public sector workers (-16k) as private payrolls fell by about 8k.

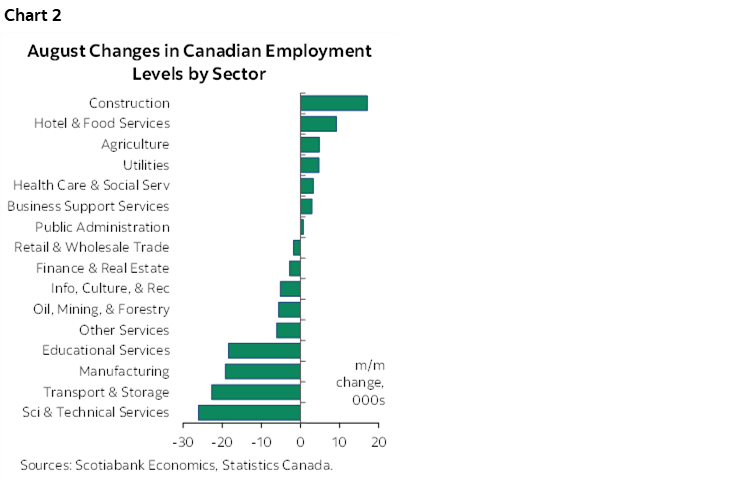

By sector, there were some bright spots like construction and leisure related hiring, but they were offset by broadly-based softness elsewhere (chart 2). Government job cuts are coming.

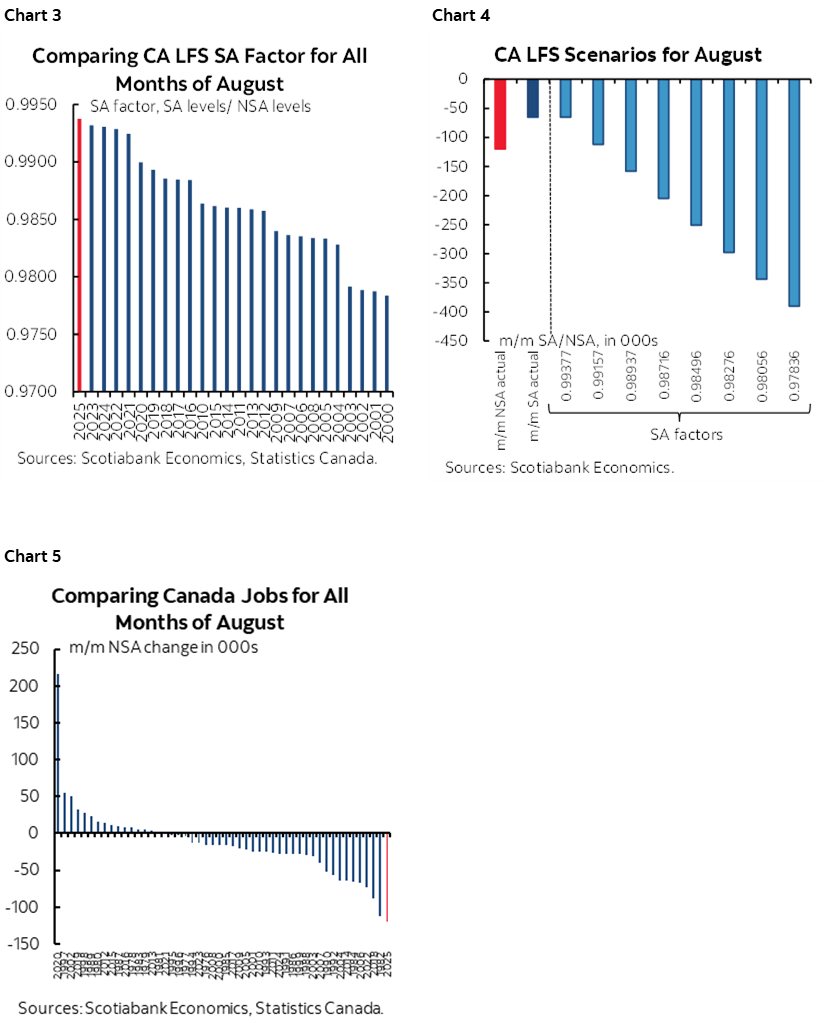

The rub lies in the fact that had it not been for another record high seasonal adjustment factor (chart 3), the decline in employment would have been bigger. Potentially a lot bigger (chart 4). The plunge in seasonally unadjusted employment was very large—in fact it was the biggest on record back to 1976 when comparing like months of August (chart 5).

I remain unsure about trusting autopilot SA factor calculations driven by statistical models that have a recency bias. My bias is that seasonality from recent years in the pandemic and afterward may not be as profound now but we’re dealing with SA factors that assume they are. That suggests jobs might have been weaker yet if not for SA factor effects.

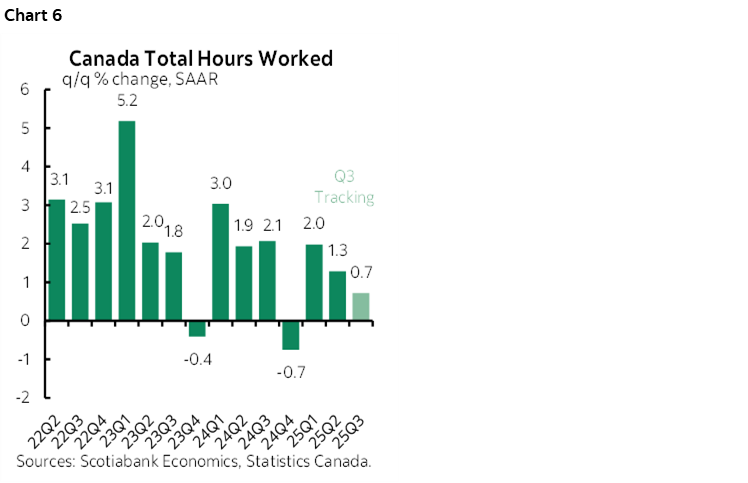

Hours worked were up only 0.08% m/m SA. They are tracking only a 0.7% q/q SAAR gain in Q3 (chart 6) which is fairly soft as input to GDP defined as hours times labour productivity with the latter hardly being Canada’s strong suit.

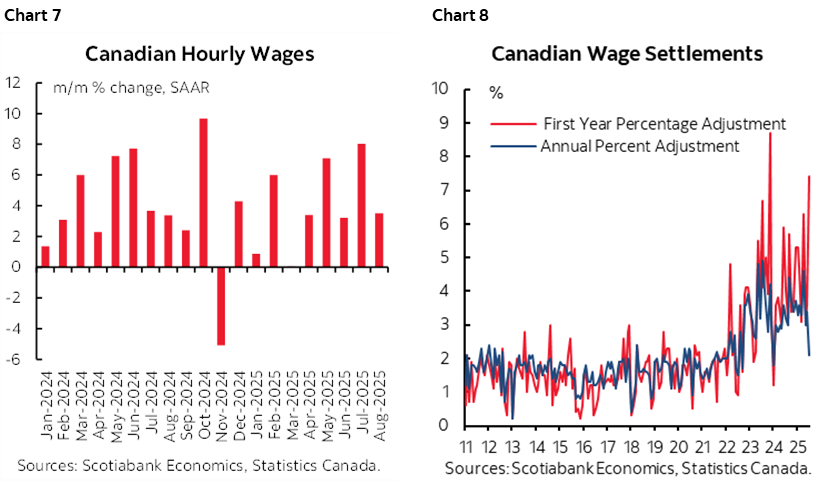

Wage growth is nevertheless still warm (chart 7). In fact, collective bargaining agreements are pushing contract wages sharply higher as revealed in freshly updated figures (chart 8). Canada, you’ve got a competitiveness problem here as wages are soaring while productivity is tumbling. The country is not helping itself in the face of trade turmoil by amplifying stagflation risks that are a central banker’s worst nightmare.

Yet for now, the additional reasoning for the BoC to be easing is based on the following:

- The BoC previously showed inflation falling back to 2.1% y/y in 2026Q4 and 1.9% in 2027Q4. They would likely be more concerned about downside than upside risks to this in light of fresh domestic and US developments. Insurance easing against the risk of undershooting 2% inflation in future may dominate in the nearer term, final domestic demand be damned.

- Second, developments in the US are material. Up to now, our argument had been that the tariff shock to Canada was small in weighted terms after taking into account high USMCA/CUSMA compliance. Therefore as long as the US economy held it together, Canadian exports could be buoyed as the income pull effect on exports offsets the price effect. That’s less clear now as the US job market stumbles and growth risks mount with the Fed in easing mode. Canada is highly trade dependent especially on the US.

- Tariff retaliation is (mostly) gone which lessens risk of import price pass through into Canadian inflation.

- It’s also unclear where the balance may lie in the October federal budget. We’re told it will apply austerity—likely on operating spending—while ramping up investment spending. Where the net lies, when, and by how much is highly uncertain as it has taken too long to present fiscal plans at a point of high uncertainty. That probably means the BoC can’t afford to wait given lags in policy effects.

The combination of factors probably merits additional easing by the BoC but it’s not without risks to how the BoC may look at things. One cut wouldn’t be worth Macklem getting out of bed to deliver as the effects would be scant and markets would pressure him to keep going. 50bps back to back and then we’ll see.

All of which would be a pivot away from inflation risk, for now. The interest sensitives are showing responsiveness to prior easing; witness Q2 consumption growth and final domestic demand plus some housing momentum. Trend core inflation remains too warm in m/m SAAR terms but we’ll see the next batch of readings the week after next. Arguments for persistent cost pressures remain sound, such as supply chain turmoil, higher inventory holdings as a buffer, labour market wage and productivity pressures. Easing as an insurance play now could well motivate regrets later—and with that some take back.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.