- The FOMC cut 50bps, increased projected easing…

- ...yet left projected growth unchanged at a higher unemployment rate…

- ...that embeds more pessimism over future prospects absent increased easing

- This is a negative signalling effect from the Fed…

- ...that Chair Powell did not address and wasn’t even asked about

- Could it be the election?

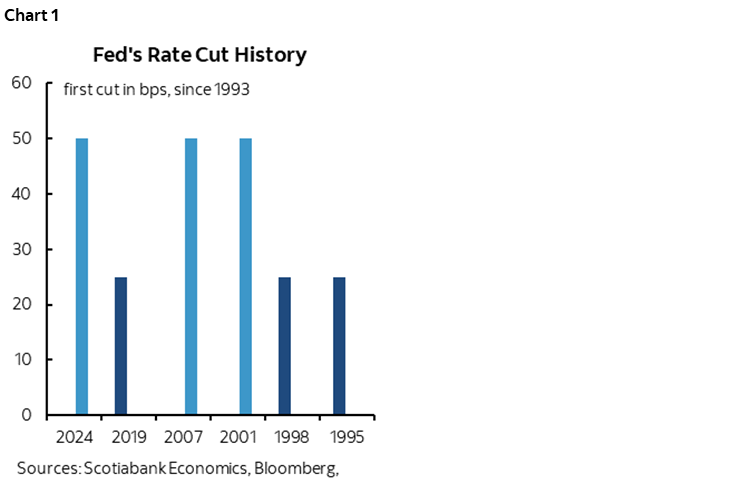

The Federal Reserve delivered an emergency rate cut of 50bps to a new upper limit of the fed funds target range of 5% in a non-emergency setting unlike the last two times they went big to start (chart 1). 2024 is now in the same company as the opening rate cuts in the dot-com and GFC eras. In so doing, they buried increased pessimism toward the outlook in the remainder of their projections and offered no explanation as to why.

How else can you explain why the Committee upped the size of its first rate cut and significantly increased the amount of projected easing throughout 2025, and yet delivered the exact same GDP growth forecast throughout the entire projection period and at a higher unemployment rate than they previously predicted? In the textbooks that I studied long ago, if you ease more, you probably get more growth and lower unemployment—all else equal!

The strong signal from the Committee is probably that they are more concerned about the risks facing the outlook for the US economy and seeking to counter them with more easing. That to me is a negative signalling effect if ever I’ve seen one.

What was missing from the entire suite of communications including Chair Powell’s press conference was why they are more concerned about the outlook. Sorry, but quoting statistics from the past handful of months and during their communications blackout doesn’t cut it. That shouldn’t be enough to sway the Committee toward more easing, and yet opting to signal faster easing should have been accompanied by upward revisions to projected growth and a downward revision to unemployment rates which did not happen.

Thus, the money question for the presser would have been “Chair Powell, why do you see the same economy at a higher unemployment rate despite the Committee’s shift toward more easing than previously guided?” And no one asked. The crickets were deafening. I want a re-do on that presser as Chair Powell got away scot-free from having to explain what they are seeing or fear about the outlook which would have helped markets have a better understanding of their thinking while formulating their own expectations. It’s possible that the coming election and its aftermath is one thing, but he’d of course never admit to that.

This is one reason why the Fed gets an ‘F’ for communicating into this decision and while communicating it. Chair Powell shrugged his shoulders in the presser by intimating they couldn’t offer better guidance on the size of the first cut in advance because they got data during their communications blackout. Not so fast, Chair Powell, you’ve used clandestine tactics to send messages to key media during blackouts in the past. Why not this time?

Clearly we’ve entered a new era in which Chair Powell has ended his approach of holding hands into perfectly set up meetings. As a result, this may drive heightened market volatility and even greater skepticism toward any forward guidance that is provided. The combination of poor communication and not being forthcoming on the fuller motivations behind the suite of forecasts will not help confidence.

Forward Guidance

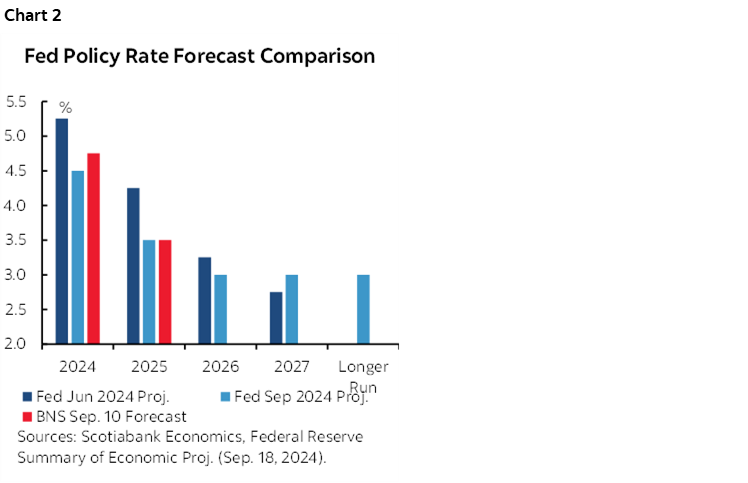

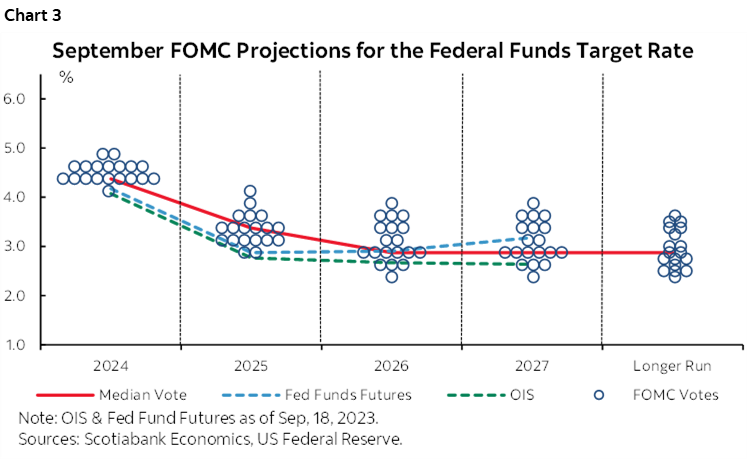

Charts 2 and 3 show the Committee’s refreshed expectations for the policy rate. The revised ‘dot plot’ shows another 50bps of cuts over the remaining two meetings this year but opinions vary. Two Committee participants see no more cuts this year, seven think there will be 25bps more, 9 expect 50bps of cuts and one expects 75bps of cuts which may imply one more 50bps cut this year in that person’s opinion, The median estimate is probably a signal that this is a one-and-done 50bps cut unless they wish to front-load 100bps of easing and then skip which seems unlikely.

The FOMC also projects another 100bps of cuts next year and then another 50bps of cuts in 2026 at which point the Committee’s median forecast indicates that rate cuts will end. The Committee’s median estimate for the longer-run neutral rate was slightly raised to 2.9% from 2.8%.

Forecasts

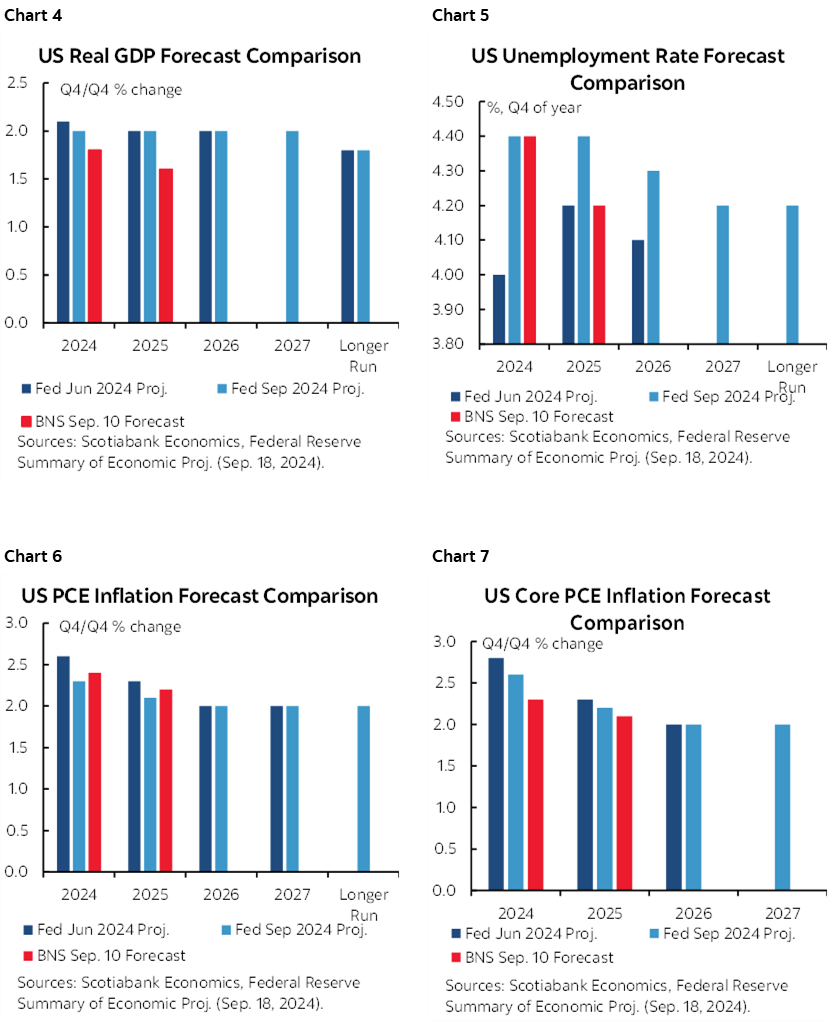

Charts 4–7 show the Committee’s updated forecasts and compares them to their June projections and our September forecasts. GDP was revised down a tick for this year to 2% and left unchanged at 2.0% throughout 2025–26 with 2% freshly inserted for 2027 and an unchanged long-run potential growth rate of 1.8%.

The unemployment rate was revised up to 4.4% from 4% for this year, and by two-tenths in each of 2025 (4.4%) and 2026 (4.3%) before a freshly forecast 4.2% rate in 2027 and an unchanged 4.2% long-run natural rate.

PCE inflation was revised down three-tenths to 2.3% this year, down two-tenths to 2.1% next year, and then left at 2% in 2026 and with 2% added for 2027 with an unchanged 2.0% long-run estimate. Core PCE inflation was revised down two-tenths this year to 2.6%, down a tick to 2.2% next year, and left at 2% in 2026 with 2027 freshly forecast at 2% and no longer-run forecast as usual.

Stocks ended the day slightly weaker. The US Treasury curve ended steeper through higher longer-dated yields. The dollar appreciated.

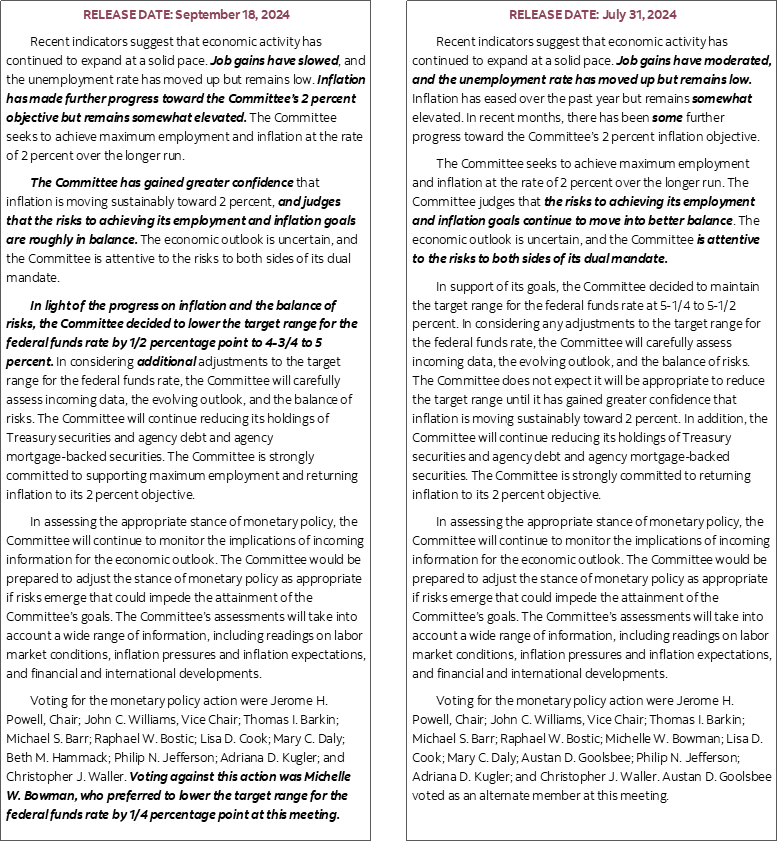

Please see the accompanying statement comparison. The original statement is here and the SEP can be found here

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.