- The BoC cut its policy rate by 25bps as most had expected

- The bias was cagey and noncommittal as expected

- There are multiple reasons why going back-to-back may not happen

- The BoC signalled no great concern over CORRA and funding markets at this time

- Statement comparison and press conference transcript are provided

The Bank of Canada cut its overnight rate by 25bps as widely expected by all but one Canadian dealer and basically fully priced going in. There was a mildly hawkish response in market rates (chart 1) perhaps due to the issues surrounding the bias that I’ll explain, but it was also correlated with simultaneous movement in US yields which is why USDCAD simply danced sideways (chart 2) ahead of the FOMC.

Key, however, is a significant question mark around the forward bias—if any. It may signal that there is a high bar to following up with another cut at the October 29th decision versus perhaps a cut-pause framework as advised going in. The odds of being done after just one cut are pretty low in my view given the overall tone of the rest of the statement and the general pointlessness to grabbing a single chip out of the bag.

The overall bias, however, was careful, cagey, noncommittal, and spoken in riddles—and hence very much in keeping with Macklem’s style that rarely holds the market’s hand. Our forecast remains for one more 25bps cut in Q4 but exactly when will be informed by data and developments.

A KEY STATEMENT OMISSION

A key omission from the statement may have contained information that was immediately flagged in my internal chat rooms. It could be much ado about nothing and needs to be combined with other points below.

The issue is that the last statement said:

"If a weakening economy puts further downward pressure on inflation and the upward price pressures from the trade disruptions are contained, there may be a need for a reduction in the policy interest rate."

Since it's such a short statement—at least compared to the prior one—why not just repeat a variation of that line to keep the bias open? Unless they are less sure now.

The BoC doesn't necessarily always think through wording shifts as carefully as they perhaps should, so maybe it's nothing.

Or maybe the Governing Council felt no need to repeat any such bias since markets are already leaning in the direction of another cut or more and not in need of a jolt.

It may also be that not repeating that line is also a signal they don't have confidence to go in a straight line but want considerably more data. That was the 2015 playbook when former Governor Poloz cut, skipped a rope behind the scenes, and then cut again.

Furthermore, when you’re at the fine-tuning stages of monetary policy when you've already come down to basically a zero real policy rate and well inside their estimates of neutral, you can take more time, require more evidence, barring clearer and bigger shocks ahead especially as trade and fiscal policy are very much up in the air.

Overall, I still like another cut this year and see nothing obvious here that they've signalled against that view, but at least October relative to December seems a bit richly priced imo based on current information.

OTHER REASONS FOR WHY A SKIP MAY BE IN THE CARDS

That’s not enough to hang an October pause call on.

October meeting pricing might also be too rich because of frequent references to the federal Budget on November 4th—after the next BoC decision on October 29th when they next issue a full forecast update. See the press conference transcript later in this note.

Further, Governor Macklem’s opening remarks to his presser indicated high uncertainty about the path forward for cost and price pressures:

“Looking ahead, the disruptive effects of shifts in trade will continue to add costs even as they weigh on economic activity. Governing Council is proceeding carefully, with particular attention to the risks and uncertainties. "

He expanded on this uncertainty in his press conference.

FULLER STATEMENT COMPARISON

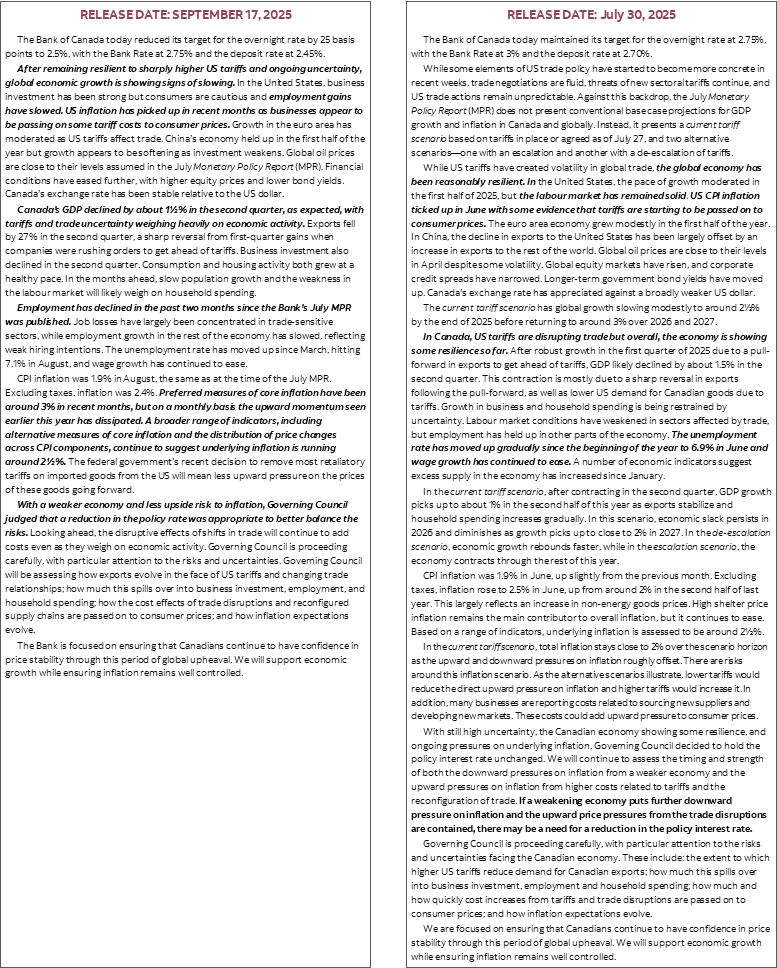

See the appendix for a comparison of this statement with the previous one in July.

On the additions side, there is clearly more concern about the global and US economies as expected. Ditto about the Cdn job market with explicit reference to two months of declines. Flagged GDP, but not as much emphasis upon robust final domestic demand as I might have expected.

But on the omissions side and as noted, key is the bottom right paragraph in the earlier statement that's gone as flagged immediately in my client chats. A meek attempt at forward guidance in the prior statement is now replaced by basically nothing.

I'm encouraged to see them continue to move away from referencing the y/y trimmed mean and weighted median gauges in favour of m/m SAAR. It's about time. The y/y TM and WM measures are slow moving, m/m weighted and compounded measures that each month take in only one new month and drop the first month while adding any revisions to SA factors. It's not a spot y/y calc. It's a m/m weighted slow moving measure. By the time that turns, it's lights out and you've reacted too late. The key is smoothed m/m SAAR TM and WM and other core measures which I've emphasized for ages but the BoC was slow to move to this

NOTHING SAID ON FUNDING MARKETS AND CORRA

As expected they did not do anything about funding issues. Nor should they have as I’ve written. See Q&A #6 in the press conference transcript below. There was no mention of funding markets in the statement itself or the published opening remarks.

That said, I thought SDG Rogers’ answer was a bit weak. To blame CORRA widening largely on a bond settlement still seems like a stretch to me. The most predictable thing about Canadian fixed income markets is the BoC’s bond maturity schedule that is publicly available and well understood. It wasn’t an unexpected shock with no advance preparedness being possible unless mass sleep apnea suddenly struck trading desks. There were other plausible explanations for CORRA widening that I’ve flagged. One was the other explanation Rogers gave relating to hedge fund activity in Canadian funding markets and the impact around the period in which rate cut bets took off. Remiss from the rest of her answer was reference to correlated funding market challenges in the US and Canada and how the US may be in the driver’s seat in terms of the integrated cross border influences. If so, then it may be the Fed’s fight with the BoC as the spectator to potentially benefit vicariously from whatever the Fed may do about it. The BoC may not wish to address factors affecting another central bank, but that’s not the same as saying we shouldn’t.

PRESS CONFERENCE TRANSCRIPT

Here is an attempt at providing a transcript of the Q&A portion of the press conference that followed Governor Macklem’s reading of his written remarks. Any errors or omissions are to be blamed on my typing abilities!

Q1. Was there a lack of conviction that the easing in inflationary pressure is sustainable and is that why your guidance is rather cagey?

A1. There was a clear consensus to cut by 25. We considered a hold or a cut. What tipped the balance in favour of a cut was the clear sense that the balance of risks has shifted. I outlined the main reasons for that. The inflation picture hasn't really changed a great deal since where we were last January. (ed. yes it certainly has for core m/m SAAR....). The more recent monthly measures on the core measures has come off. If you look at the inflation data there is more comfort that some of the upward pressures are easing off. There are still some mixed signals there. We know there are offsetting factors. The guidance really is we're not being as forward looking as normal and paying close attention to the risks and uncertainties. If those shift we're prepared to take action. [ed ie: no answer...lol]

Q2. Any thinking on fiscal policy?

A2. There have been a number of announcements of the most directly affected sectors. More recently there have been announcements on big projects. From our perspective, as those plans become more concrete we will be assessing their macroeconomic impact. The budget will be tabled on November 4th. It's less about individual measures and more about the overall macro impact. Once we have the budget we will be assessing the implications for the plans on the outlook and what we need to do with interest rates. [ed. waiting for the budget...]

Q3. You are cutting with core inflation at 3% and other measures at 2 1/2%. Aren't you taking some kind of a risk here with inflation pressures?

A3. Total inflation has been running below 2% largely because of the elimination of the consumer portion of the carbon tax. The more recent monthly readings have been running around 2 1/2% over the past three months. Other measures of core are similar. The percentage of the basket that is rising is roughly around where it is when inflation is running around 2 1/2%. At this point, inflation pressures look a little more contained and with a weakening economy that puts downward pressure on capacity and inflation we felt a cut was appropriate.

Q4. What would you need to see on inflation and employment to cut again this Fall?

A4. If there was just one thing the job would be so easy. Tariffs are weakening the Canadian economy. You can see that in the directly affected sectors. Employment growth has slowed in more of the economy. We will be looking at spillover effects across more of the economy. When we talk with businesses they are finding all new costs as their supply chains adjust. The reality is that tariffs increase trade frictions with out biggest trading partner and that has efficiency costs that monetary policy cannot offset. We can help the economy adjust while containing inflation. It's going to be about balancing those risks. If the risks tilt further we're prepared to take more action but we're going to take it one meeting at a time while being less forward looking than usual. We'll make that assessment in October when we get there.

Q5. Would you rather just wait and take a decision in December after you see the budget?

A5. If the Budget was the only thing happening that might make sense but we'll get a lot of new information between now and then. We're particularly focused on what's going to happen to exports; we saw a very sharp drop in Q2 because they were pulled forward and because of tariffs. Going forward we'll be watching very closely where exports go, how that spills over into the rest of the economy, where do those costs go and what happens to expected inflation. We'll be looking at the balance of risks. I expect we'll get more information on fiscal policy between now and our next decision but the Budget pulls it all together.

Q6. Are you considering a technical adjustment to the deposit rate given funding market pressures? Can you explain CORRA developments?

A6. Rogers answering. There have been a number of factors. One was the bond maturity that strained funding. The greater presence of foreign hedge funds in Canadian funding markets can be a bigger influence when there is a change in rate cut pricing. There is not plan to change the discount rate at this time. We expect turbulence as settlement balances get down toward our target rate but we have a number of tools we can use. [ed. summary: expect nothing on CORRA at least for quite a while]

Q7. General question about tariff effects and other drivers of inflation.

A7. You can see some effects of counter tariffs on categories like food and perishables. Canada has now dropped most of those counter-tariffs. You'd expect those prices to come back down. From a monetary policy perspective, the direct effect of tariffs is a once-off impact and level increase that we would tend to look through that. The risk to us is that a temporary increase in prices has knock on effects on other prices and then it becomes more widespread. The fact that the retaliatory tariffs have been removed takes off that second round effect. [ed. not all retaliatory tariffs are gone through.....autos and metals for instance. but Macklem does a better job on this issue than, say, the strident comments by Fed Gov Waller.]

Q8. How much of a role did the elimination of retaliatory tariffs plays in your decision?

A8. The upward momentum we were seeing in core measures earlier in the year has fallen off. That's telling us that the risk that the inflation pressures will go up further has gone done. The remove of retaliatory tariffs reinforces this. Those two things taken together and alongside a weaker economy tilted the balance today. You have to look at the combination of how all that fits together.

Q9. Ontario Premier Ford said 'good, now keep going.' Reaction? How much support was there on Governing Council for a deeper cut?

A9. We take evidence-based decisions independent of politics. There was a clear consensus on Governing Council to cut and I've outlined the reasons why.

Q10. If the Canadian economy fails to recover as rate cuts continue would QE be justified by Trump tariffs?

A10. We're a long way from there. We have a lot of room on our policy rate. The current tariff scenario expected slow growth that won't feel good but is growth as the economy adjusts to a different US relationship. In the escalation scenario where tariffs escalate, the Canadian economy goes into recession and the situation would be worse. Having said that, we'd still be a long way from QE. In the deescalation scenario growth and the recovery would be stronger.

Q11. How much of the uncertainty reflects trade versus fiscal policy uncertainty?

A11. Rogers answering. It's one of the things we consider. There is a lot of uncertainty. We'll have some time to digest the budget in our last decision of the year. Now Macklem intervening: the way the US has implemented tariffs applies to very specific sectors, same with Chinese tariffs on canola, pork and seafood. For the rest of the economy, tariffs remain very low providing you are compliant with CUSMA. The impact is very specific. Monetary policy is a blunt instrument that can help the economy adjust but we cannot help individual sectors. Fiscal policy can do that and there have been a number of supports introduced. Then there is a broader industrial strategy and business changes. We will be looking at what fiscal policy is doing and take it into account.

Q13. How are you thinking about lag effects of rate adjustments relative to immediate effects of trade shocks?

A13. Yes we do need to factor that in. The lagged effects of the cuts over the last year involve long and variable lags but before we got hit with tariffs we could see lower interest rates were feeding through the economy. Then come February we're hit with tariff threats and reversals and the consequences. Yes we have shortened our horizon in a situation of greater unpredictability but that doesn't mean we're not looking forward at all. We're using scenarios. Those scenarios have been very helpful in our decision making. We have seen some of the tariff uncertainty decline and outside of the most affected sectors tariffs remain low. I expect that if this holds we will be able to get back to a base case projection in October. We'll see.

Q14. Are there any foreseeable upcoming factors that could boost the risk of stagflation?

A14. Could see tariff policy change. We could see more indirect effects of tariffs as businesses pursue measures to protect themselves, re-routing supply chains, investing etc, with general pressure on prices. We'll wait to see what fiscal policy brings.

Q15. How else does the BoC see population growth impacting weakness in the economy and prolong the contraction caused by the trade war?

A15. Population growth adds to demand and supply. Lower population growth means less growth in consumer spending and less new workers looking for jobs so other things equal the UR doesn't go up as much. Over longer periods of time these demand and supply effects are balanced out. When population growth was too warm it was boosting housing and consumption and we're now seeing the other side of that. Historically population growth moved relatively smoothly and we had rules of thumb but we need to adjust those rules. The number of jobs required to keep up with new entrants is lower than historically for example. [ed — I'm still of the view that this is too benign as a viewpoint. Canada does not integrate new arrivals overnight. The immigration dividend can unfold over many years.]

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.