- The policy rate was unchanged at 3.75% as expected

- No further changes to balance sheet or funding instruments

- Guidance sets a high data dependent bar against cutting further anytime soon

- Was it right to de-emphasize labour market risks?

- Press conference transcript

- If the Fed’s not cutting, the BoC’s policy rate flexibility is limited

The policy rate held unchanged at 3.75% as universally expected and the bias remains heavily conditional upon future data and developments.

Label this outing “35 unnecessary questions for a press conference that was 47 minutes too long.” You had me at simply saying I'm not changing today, dunno about the future, we’ll see you then after more data. At least the statement was short and sweet.

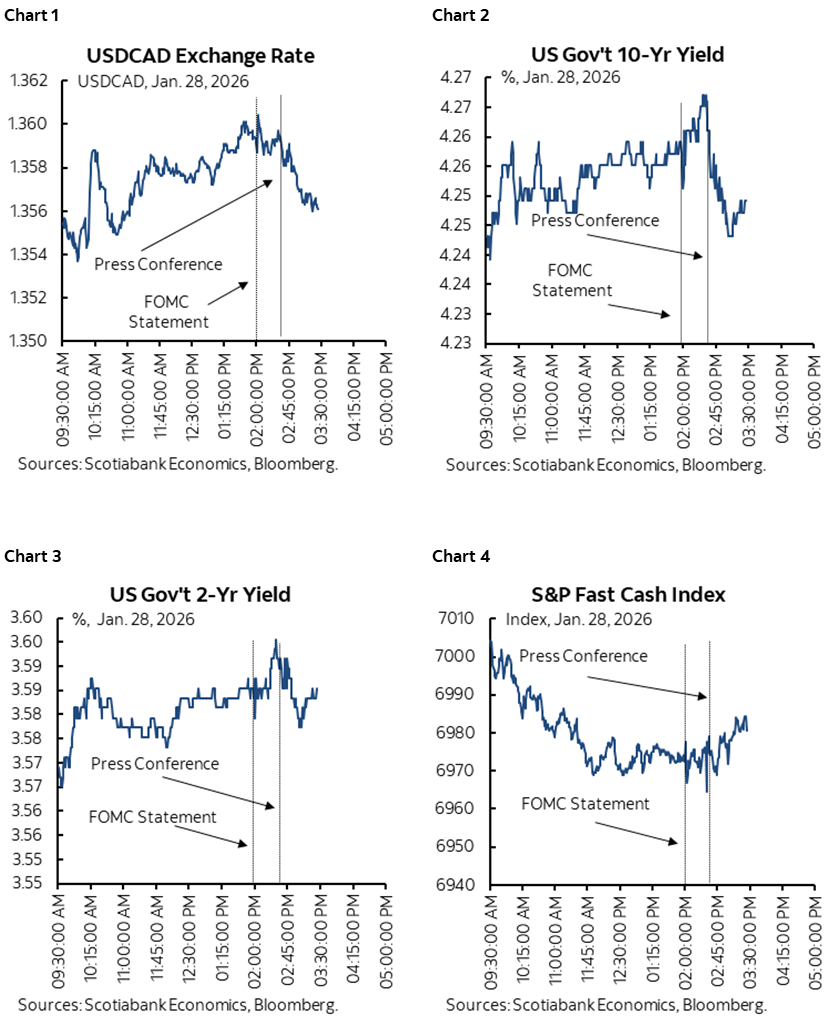

Like the case of the BoC in the morning, markets barely even noticed (charts 1–4). The 2s yield is unchanged. Full year Fed-pricing was unchanged with two cuts still priced but not starting until at least June.

Disappointing tech earnings in the after-market counted more than either central bank from a market standpoint.

STATEMENT CHANGES—QUESTIONABLY DE-EMPHASIZING LABOUR MARKET RISKS

The statement had a slightly more upbeat tone as summarized in the statement comparison at the back of this publication.

Key is the deletion of the reference to how the Committee “judges that downside risks to employment rose in recent months.” That omission counts for more than any additions or tweaks.

They also upgraded the reference to growth (“solid” instead of “moderate”).

On jobs, they now reference job gains as having “remained low” instead of “slowed.” Instead of saying the unemployment rate has “moved up” they now say it “has shown some signs of stabilization.”

And on inflation, the Committee says inflation “remains somewhat elevated” instead of “has moved up.”

The statement also retained ambiguous reference to the “extent and timing” of future policy changes.

There were only two dissenters this time (Governors Miran and Waller) which is mildly surprising given how dovish Governor Bowman was speaking beforehand.

In all, it’s a somewhat more neutral tone than previously but not one that wasn’t already priced.

THE PUSH BACK

I don't agree with their decision to remove reference to “downside risks to employment rose in recent months.”

In fact, doing so while lauding strong GDP growth could come around to backfire. As Powell said himself in the press conference, “Usually when GDP and the labour market get into an argument the labour market wins.”

Much of the explanation for why I don’t see it the same way was included in my last nonfarm payrolls note (here).

You might argue the risks are not accelerating versus remaining significant (to jobs) but I'm not even sure that holds water. How to interpret the health of the US labour market is open to debate.

The Committee might be leaning on the October drop of 173k as a one-off and since then nonfarm has been about 50k per month in November and December, but then you get into a whole mess of other issues.

For instance, take health care out and nonfarm and private nonfarm payrolls tumbled in December so when Powell reference private payroll growth was he merely bowing down before President Trump? Nonfarm ex-health care has been down in four of the past six months and flat in one with only one notable gain. I also continue to have a very healthy skepticism toward the quality of the data. For one thing, seasonal adjustment factors have shot off the map and inflated jobs coincidentally after Trump fired the BLS Commissioner. Then take Powell's earlier comments (which he skipped today) that payrolls are overstated by probably 60k +/- per month since April and you've been roughly flat on November and December payrolls even without considering other arguments. Further, next Friday’s payrolls release incorporates the annual benchmarking revisions that will wipe out around 900k+ jobs from last March's level.

In general, headline payrolls have totally stalled on a trend basis since "Liberation Day" before any of these adjustments, and are considerably worsening after these adjustments.

So, either they have good arguments to disagree with these points that I haven't heard so far, or they're having us all on because they simply don't wish to acknowledge a dovish angle on jobs given what that would mean in stoking concern about US economy that policymakers are more reticent to do than private forecasters have to be, or they are truly more concerned about the inflation side of the dual mandate, or something else.

All that said, I'm not too worried. My concern remains moral hazard. The Fed can't point to that. They can't even hint at it or else they'd all be doomed. But I wouldn't blame them one single bit for thinking if they cut 100bps then they'll just embolden more unwise trade policies, more reckless abandon on fiscal policies etc

PRESS CONFERENCE TRANSCRIPT

What follows is an attempt at providing a transcript of the press conference with any errors or omissions to be blamed on my typing abilities.

Q1. Why did you attend the SCOTUS hearing on Cook?

A1. That case is perhaps the most important legal case in the Fed's 113 legal history and it might be harder to explain why I didn't attend. Paul Volcker went to a famous case in 1985. I felt it was appropriate and I did it.

Q2. Last month you mentioned the potential for distorted jobs numbers. Do you see the distortions as smaller?

A2. We're getting to the place where they are no longer material. We saw data coming in that suggest some signs of stabilization and some signs of continued cooling so we felt the same reference to jobs were no long appropriate and we thought economic growth was strong and could support jobs.

Q3. You have to date avoided political remarks. Anything further today?

A3. I have nothing further on that today.

Q4. Have you decided whether you will remain as a Governor after your term as Chair expires?

A4. No, and I have nothing further for you on that today

Q5. Why would you want to leave at all under the circumstances?

A5. Not something I'm going to be getting into today.

Q6. We've seen big movements in the dollar. What is driving it lower? Have you been concerned by the volatility?

A6. We don't comment on the dollar. The Treasury Department has the job of oversight of the currency.

Q7 But what's your view on the market movements and drivers?

A7. We don't talk about that. The Treasury Department has that as their role and we stay off it.

Q8. Is the timing of further rate cuts pushed back compared to what people might have thought in December?

A8. There is a clear improvement in the outlook for growth. Inflation performed about as expected. Some of the labour market data suggests stabilization. Overall it's a strong forecast. After the three recent rate cuts we're well positioned to face the risks on both sides of our dual mandate. We haven't made any decisions on future meetings. We'll be looking to our goal variables and letting the data light the way for us.

Q9. You have previously described the policy rate at the higher end of neutral. Is the Fed still in the process of getting into the middle and what would it take?

A9. Many of my colleagues think it's hard to look at the incoming data and think policy is restrictive.

Q10. Are you still in the mode of bringing the policy rate lower?

A10. The SEP shows further reduction but we've moved now to fed funds at 3.65% so you've moved a good way and we're well positioned here to see how the economy performers after those three cuts.

Q11. Did you discuss a cut at this meeting or in March and is there broad agreement on what it would take?

A11. There was broad agreement for holding today including among non-voters. We're not trying to articulate a test for when to cut. We're making decisions on a meeting by meeting basis. We still have some tension between inflation and employment. The upside risks to one and the downside risks to the other may have diminished. There are differing views on the Committee.

Q12. Have the effects of tariffs already worked through the economy?

A12. Most of the overrun on goods inflation has been because of tariffs. We do think tariffs are likely to move through and be a one-time influence. In services we do see ongoing disinflation which is a healthy development. The expectation is that we will see the effects of tariffs peaking and working through over the course of this year assuming no further tariffs and that would suggest we could be loosening policy. We have a two-sided mandate and need to monitor labour markets as well.

Q13. How would you manage the transition to a new Fed chair?

A13. No comment.

Q14. Is it fair to describe dual mandate risks as roughly balanced now and is the next move necessarily down?

A14. The upside risks to inflation and downside risks to employment have diminished but it's hard to say whether they are fully balanced. We think policy is in a good place. We'll have to see where the data lead us.

Q15. Is there any concern about movements in inflation break evens?

A15. Short-term inflation expectations have come way down in the last few months. In the longer-term inflation expectations have remained consistent with 2% inflation over time. They reflect confidence in the return to 2% inflation.

Q16. Is it still true that what you previously said about downside risks to the labour market as bigger than upside risks to inflation?

A16. Those risks are a little less. I'm not making a judgement about how one is more at risk than the other.

Q17. Global investors are hedging their dollar exposures in ways that are different. Do you agree with the BIS?

A17. There isn't a whole lot of data to suggest that.

Q18. What would you need to see in the labour market to resume easing?

A18. We'll always be looking at combinations of labour and inflation readings.

Q19. If inflation picks up and the labour market doesn't deteriorate further then would you be considering hiking?

A19. It isn't in anybody's base case that we'll be hiking. We don't take anything off the table but it's not in our expectations right now.

Q20. Do you worry the US could find itself in a similar fiscal position as Japan?

A20. US interest rates haven't moved a lot for a while. It's more of an over time thing. The fiscal path is on an unsustainable path. The level is not. The sooner we work on that the better.

Q21. Does it reduce the effect of your rate cuts that longer-term rates haven't budged much?

A21. Many things move longer-term rates. It's not mostly what happened on the short-end. It's more assessments of the fiscal path and risks that move the 10 year around.

Q22. Do you support blocking any approval of Chair nominees until your investigation is concluded?

A22. No comment

Q23. General question on independence

A23. It's an institutional arrangement that has served the public well. The reason is monetary policy can be used through a political cycle to influence the economy. This is true of every advanced economy. If you lose that, it would be hard to restore the credibility of the institution. We haven't lost it, I don't believe we will, and I certainly hope we won't.

Q24. How much do you see labour market reading as a data mirage around immigration versus a real weakening over the past six months or so?

A24. Part of it is that growth in labour supply has come to a halt driven by a sudden stop in immigration. Supply came way down. Demand also came way down maybe a little more. The Conference Board's measure of job availability is at a very low reading but it is an indication of softening. Part-time preferring full-time has gone up. There are lots of indications that the labour market has weakened. So has supply. That makes it a difficult time to evaluate the labour market. If demand and supply are both coming down then the labour market is in balance.

Q25. Question on drivers of 2026 growth

A25. Fiscal, financial conditions and consumption are driving growth. Consumer spending overall numbers are good. We're benefiting from the AI build-out of data centres. Growth is on a solid footing.

Q26. What is the conversation around the Committee on unequal outcomes in the economy for upper versus lower income earners?

A26. We're seeing that lower income consumers are still consuming but changing.

Q27. Are you concerned about AI supplanting entry-level jobs and how does that play into your concerns about the labour market?

A27. There is a wide range of possibilities. Every tech wave has created some jobs and eliminated others but ultimately technology drives productivity and wages higher. We don't know if that will remain the case. We may see jobs eliminated in the short-term. We just don't know what will be the overall effects.

Q28. Is your expectation still for inflation to cool over 2026H2 and how far away are you from target?

A28. On net, no progress on y/y inflation in past year but most of the overshoot in goods was on tariffs and we think that's temporary. There is an expectation that sometime in the middle quarters of the year we'll see tariff inflation topping out.

Q29. Canadian PM Carney said there has been a rupture in the global order and how may that impact the US economy?

A29. I can't comment on that speech. Much of our geopolitical risk is around oil but we haven't seen much. Longer than that it's about trade and so far out economy has pushed right through partly because what was implemented wasn't as big as threatened at first and because other countries did not retaliate.

Q30. How could you cut rates and not spur inflation in the environment of strong growth?

A30. Well, we didn't. But it also depends on potential growth and whether that over time is rising as quickly as actual GDP.

Q31. Is productivity driving the gap between GDP and jobs and is AI the reason?

A31. That can be explained by rising productivity but we do see signs of the UR stabilizing. It may be we're beginning to see the resolution of those two things. Usually when GDP and the labour market get into an argument the labour market wins.

Q32. After today you have two meetings left as Chair. What advice do you have to your successor?

A32. Stay out of elected politics, don't do it. Our window into democratic accountability is through Congress. You earn democratic legitimacy through your interactions with members of Congress. There isn't a better cadre of officials more dedicated to the public than work at the Fed.

Q33. How much attention are you paying to gold and silver prices and what message do you take from them?

A33. Don't take much from them. The argument could be you are losing credibility but that isn't true, look at inflation expectations.

Q34. Some prominent critics charge that the Fed's modest are backward looking and should be more forward looking. How do you reconcile this?

A34. Those criticisms just don't make sense. Every FOMC participants writes down projections and that's the basis for the discussion. Models involve great uncertainty when out of sample shocks arrive. When there are technological changes like now we look at prior periods and are all over that. No one is sitting here discounting the possibility of higher productivity, we've been talking about it for years. We're are well aware that higher productivity means higher potential.

Q35. The trade landscape is still in a state of flux. How do you track these in real time?

A35. Our staff has done a really nice job on that. You can track the effects of tariffs on pricing and everything. At the beginning it was more of a forecast and now it's in the data. Our forecasts were not that far off because the tariff changes were smaller than threatened, retaliation did not occur and the incidence effects were uncertain.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.