- The policy rate was left unchanged at 2.25% as universally expected

- There were no changes to balance sheet or funding instruments as expected

- Forecast changes were minor

- There were multiple oddities in the overall package of views

- Key was ambivalence toward the direction and timing of a rate move

- Markets largely ignored it all

The BoC kept its overnight rate unchanged at 2.25% as universally expected. Forward guidance was left broadly intact alongside minor forecast changes. There were no other policy changes affecting balance sheet or funding tools and none were expected.

Basically they're repeating long hold guidance until some new information arrives in either direction, while not signalling any appetite for deviating from 2.25% any time soon which is as expected. The most useful thing that was said was the response to question #10 in the press conference when Macklem was strikingly direct—and honest—in saying they weren’t at all sure in what direction or when the policy rate may be changed next. While headlines emphasize the BoC’s emphasis upon uncertainty, they fail to note that the BoC is speaking of bidirectional uncertainty in terms of what it means to growth and inflation and hence the policy rate. This reinforces our view for a hold through 2026H1 until things get more interesting and we have further information.

Having said that, I’ll explain how I felt that the overall tone of the communications had the feel of forcing arguments to merit leaving the inflation outlook unchanged rather than raising it a touch

CAD depreciated a touch, but so did other currencies against the USD and CAD continues to slightly outperform the rest of them this morning. The Canadian two-year yield is flat compared to pre-communications. Markets continue to price the BoC on hold until about half of a 25bps hike is priced by late year. Our forecast remains for two hikes starting in October and December.

The statement is here and see the comparison of changes in the appendix to this note. The MPR and forecasts is here. Governor Macklem’s remarks are here. I also provide an attempt at a press conference transcript.

STATEMENT CHANGES

Key is that the concluding forward guidance was similar to the last statement in December. They now say:

"Governing Council judges the current policy rate remains appropriate, conditional on the economy evolving broadly in line with the outlook we published today. "

Versus in December:

“Governing Council sees the current policy rate at about the right level to keep inflation close to 2% while helping the economy through this period of structural adjustment.”

Uncertainty references were slightly upgraded, but that could merely reflect the passage of time as January is closer to Summertime trade negotiations, US midterms, US Court rulings on tariffs and the Fed, the Fed Chair appointment etc than October was. Here’s the change:

October: "Uncertainty remains elevated."

January: "Uncertainty is heightened and we are monitoring risks closely."

I remain cautiously optimistic on how the negotiations turn out.

FORECAST CHANGES AND CURIOUSITIES

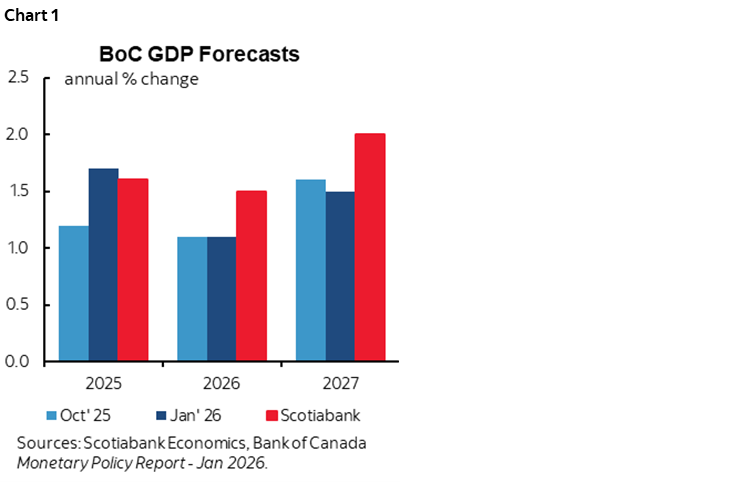

Canadian GDP growth was left intact at 1.1% in 2026 and little changed for 2027 at 1.5% (1.6% previously). Chart 1.

Externally, they upped their US growth forecasts from 2.1% to 2.2% for last year with Q4 GDP still pending, from 2.2% to 2.6% for 2026, and unchanged at 2.1% for 2027. They also revised up the Euro Area, China, and World GDP figures for 2025–26.

That’s all good for a trading nation, so how come they didn’t revise up Canadian GDP growth as well? They basically shrug their shoulders on the direction of trade risks but fade the more positive imported effects of stronger external growth?? That sounds like an imposed bias that was left unexplained and nobody asked why.

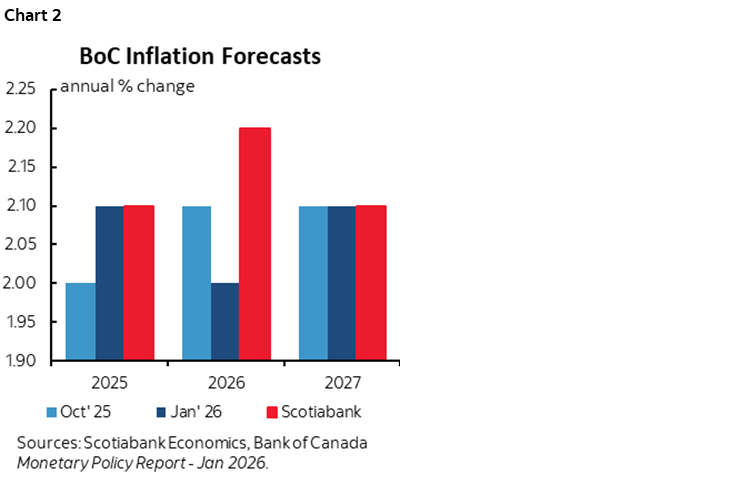

CPI inflation is projected to be 2.0% in 2026 (2.1% previously) and 2.1% in 2027 which is unchanged from October. Chart 2. I’ll come back to debatable ingredients to their views on inflation that upgraded 2025 but slightly lowered 2026 inflation.

The verbiage emphasizes little change by stating "The Bank projects growth of 1.1% in 2026 and 1.5% in 2027, broadly in line with the October projection" and "Inflation was 2.1% in 2025 and the Bank expects inflation to stay close to the 2% target over the projection period, with trade-related cost pressures offset by excess supply."

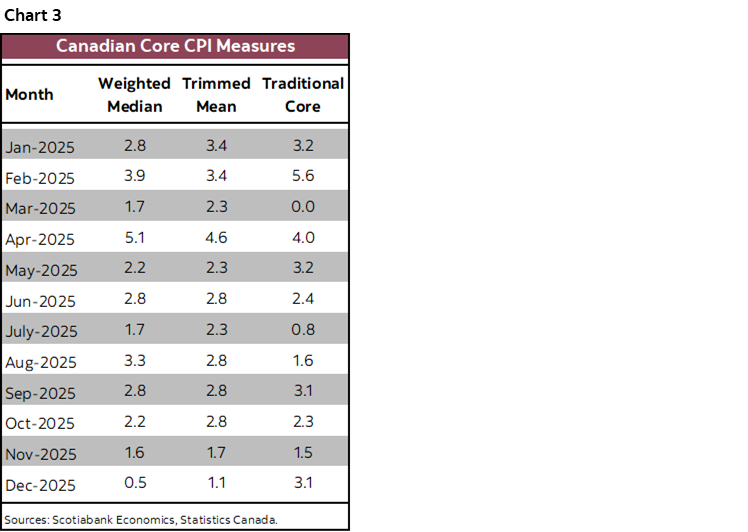

One thing that bothers me about their inflation view is that they cherry-picked the core measures. Chart 7 in their MPR shows that the trimmed mean and weighted median measures of core inflation have eased of late. What was omitted was traditional core (ex-food and energy) that has accelerated of late (chart 3). They have at times indicated a tendency to downplay trimmed mean and weighted median CPI, but when it suits them, they play it up. Again, that’s another bias.

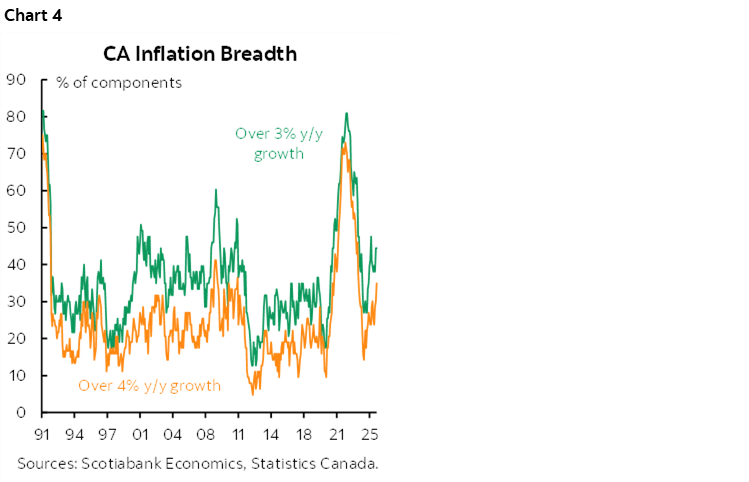

For that matter, do a keyword search for ‘breadth’ of inflationary pressures and you won’t find a single reference in the entire MPR. Not one. Yet look at chart 4 that clearly shows a pick up. Again, their bias is may be clouding their objectivity and that’s never good for a central bank.

They played with potential GDP in ways we contest. This year's potential range is up a bit from a range of 0.4-1.4% in October to 0.6-1.6% now but it’s unclear why, but they took that back and then some by downgrading 2027 potential GDP growth to 0.7-1.7% from 1.3-2.3%. I have always found that the BoC fudges potential and gaps to suit themselves on the current bias.

Yet downgrading potential in 2027 while leaving actual GDP projections little changed should have the BoC raising its inflation projection in 2027 through less downward influence from slack. Why didn’t they? I mean, we all know that forecasting that far out has umpteen uncertainties, but why don’t the numbers hang together in an internally consistent fashion? My hunch is that internal consistency would have meant raising the 2027 inflation forecast and thus signalling to markets more concern about upside than downside risk which they’re not yet prepared to do. BoC forecasts are notorious for reflecting what they wish to show.

They left their estimate of the output gap as at the end of 2025 unchanged in a range from -1.5% to -0.5%. ““Potential output has thus been revised up by almost as much as GDP, so the amount of slack in the economy remains largely unchanged." Here too, why? Our group estimates less slack as a result of the GDP revisions by putting a little more weight on the actual GDP revisions than the potential GDP revisions. This reflects our dissection of the underlying causes of the GDP revisions including more investment and how it works through modelling attempts. The BoC doesn’t explain why they raised potential enough to offset higher GDP levels. Frankly, something smells like the foot of the Don River in summertime here.

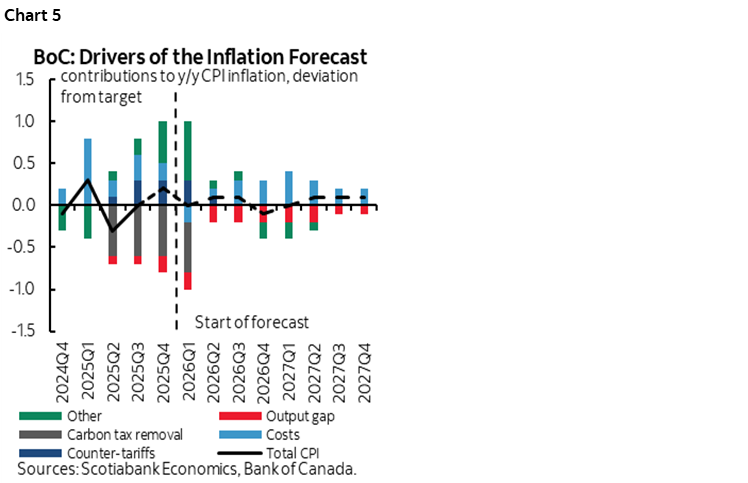

Chart 5 is replicated from the MPR and shows a very slight tilt toward cost pressures on CPI offsetting downward effects of modest slack relative to their previous breakdown in October.

On a quarterly GDP basis they downgraded Q4 from 1% to 0% but the first published forecast for 2026Q1 (they only go out two quarters at a time, beyond the annuals) is 1.8% so they expect a moderate rebound. And by the way, the BoC’s forecasts wouldn't include the GST announcement at the start of the week that is estimated to supercharge Q2 income growth and with it consumption growth (recall here). MPR and forecasts are finalized well in advance.

PRESS CONFERENCE

The following is an attempt at capturing the Q&A exchange during the press conference. Any errors or omissions are to be blamed on my typing abilities! I will say, however, that CPAC needs to fix its feeds and translation issues.

Q1. Is the BoC saying that the outcome of the USMCA negotiations will dictate the next move in interest rates?

A1. We are saying uncertainty is unusually high. There are a number of risks. Geopolitical risk is high, US trade policy is unpredictable, and for Canada the outcome of the CUSMA negotiations is an important part. We have built into our predictions that current tariffs remain in place. That could change. The uncertainty is already having an impact on the economy which is built into our projection but we have that built into our projections. The outcome may be no change. We have highlighted a number of outcomes for CUSMA. We have published a number of scenarios around different trade configurations.

Q2. You see potential for reallocation of capital. What do you mean?

A2. You have a number of hard hit sectors in Canada. Steel, aluminum, some autos etc. They may need to pivot inside of Canada or outside of Canada with new capital or new skills. Our trade relationship with the US is fundamentally changed. Even if CUSMA is left unchanged, businesses are looking for new markets. I would stress that is going to take some time. It does not happen quickly. Through that transition it does lower the economy's potential. Productivity should come back up but that is going to take some time.

Q3. What has changed since October to say that the range of possible outcomes is wider than usual?

A3. There is a sense that geopolitical risk is heightened. The month of January is pretty packed with new geopolitical risks. US trade policy through last Spring there were big changes with new deals through the summer there was more stability and since then there are new threats. US trade policy remains highly unpredictable. It is 2026, CUSMA is under review.

Q4. Are there implications for monetary policy in Canada if you lose confidence in independent monetary policy in the US?

A4. This threat is contributing to this sense of uncertainty. The Federal Reserve is the biggest and most independent central bank in the world. A loss of independence would affect the world and particularly Canada given its integration. [ed. Macklem then went a little too far in saying Powell is doing a good job imo. They both totally blew it on inflation.]

Q5. Is Trump being vindicated on tariffs in that they are not doing much damage?

A5. [Rogers speaking]. It's too early to tell. Rogers also correctly flagging the coincidental effects of AI.

Q6. Can you update mortgage reset views?

A6. [Rogers again]. We don't have a big change in our views. We do expect those rollovers this year to see payment increases. The recent up-tick in the yield curve may marginally add to that risk. Most mortgage borrowers have been prepared for this and mortgage rates have come down. [ed. agreed, micro shock, not macro, doves shouldn’t do the same mistake for a third or fourth year!].

Q7. Will the diversification away from the US only partially offset the trade war impacts?

A7. Yes. Macklem repeating Carney's thesis that rules-based trade is over in the US

Q8. What is driving the USD? Are you concerned about recent appreciation by the C$ and would you lean against it?

A8. We don't target the exchange rate. A flexible exchange rate is an integral part of our monetary policy regime. In the last couple of weeks there has been renewed USD weakness. Many currencies including CAD have appreciated on the USD. What's driving it I think is largely geopolitical events. Currencies are not being driven by traditional things like short-term rate differentials or commodity prices. The USD depreciation over the past year has reflected the safe haven role having been dented while other safe havens like gold are up a lot.

Q9. How do you view the cuts in immigration filtering through the economy?

A9. Lower population growth means lower potential growth. [ed. yet the BoC is only lowering it for 2027 as part of their fudging].

Q10. Does elevated uncertainty create a higher burden for moving in either direction?

A10. We did discuss the future path of interest rates. We agreed that the current policy rate is appropriate if the forecast path is realized. The clear consensus was that it's very difficult to predict either the direction or timing of the next move in our policy interest rate. You need to be able to assign probabilities to the risk to assign probabilities to the rate changes. [ed. ie: full-on-neutral for a while as expected]. Is uncertainty higher than it was a year ago? It's hard to parse at every moment in time but it's high. It is important to step back from the daily noise. Some things are clear. It's clear that the era of rules-based trade is over. It's clear that population growth has come down. It's clear than AI will impact. The Canadian economy needs to adjust to these things. It has started. It is going to take some time. If we do adjust then the economy will be more resilient going forward. The central bank is not at the center of that. We can play a supporting role. We are trying to provide some support to the economy while maintaining inflation close to the 2% target.

Q11. What are your main drivers of GDP changes?

A11. Macklem saying they have exports returning to some modest growth along a lower path. We're importing less from the US and exporting more to other countries. [ed. Macklem seemed to cite an old figure for Cdn export share to US, not 75%, actually 67%]. Saying business investment is held back by uncertainty and it's hard to allocate capital. They are starting to adjust to the days of open trade with the US being over. Governments have also increased their infrastructure investment and incentivized business investment.

[ed. Macklem missed an opportunity to tell Canadian businesses to seize the moment in my opinion. See the section on investment my weekly. CAD depreciation offsets mild tariff shock, Canada is the #2 ranked country in the world for foreign direct investment behind only the US, CAD weakness would offset any further tariff shocks versus China that can't with a dirty managed peg, etc etc. In other words, many (not all) Canadian businesses always seem to latch on to excuses not to invest, not to adopt new tech, not to spend on R&D. That's been true for decades.]

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.