- Markets largely shook off CPI with an eye on bigger concerns

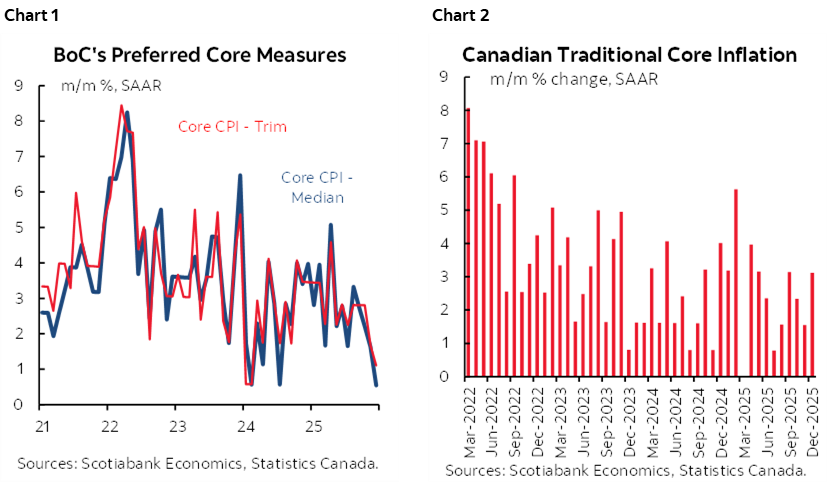

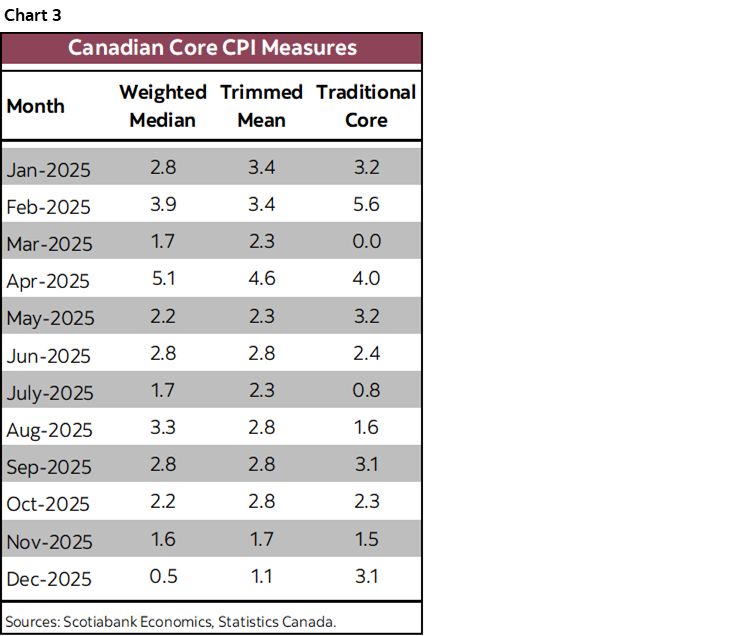

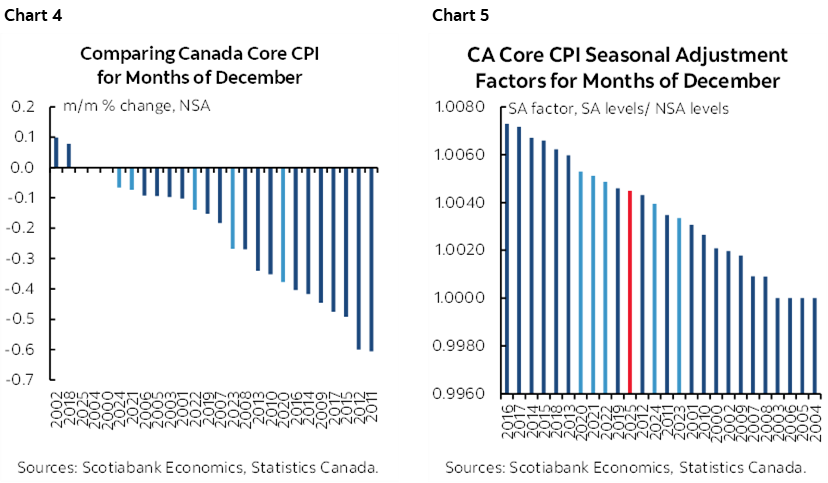

- Traditional core was hot, trimmed mean and weighted median were not

- Why the BoC will ignore the readings

- BoC surveys show stable inflation expectations, but are too stale to matter

- Canadian CPI m/m % / y/y %, SA, December:

- Actual: -0.2 / 2.4

- Scotia: -0.4 / 2.2

- Consensus: -0.3 / 2.2

- Prior: 0.1 / 2.2

- Trimmed mean CPI m/m % SAAR: 1.1 (prior unrevised from 1.7%)

- Weighted median CPI m/m % SAAR: 0.5 (prior unrevised from 1.6%)

- Traditional core ex-food & energy % SAAR: 3.1 (prior revised to 1.6% from 0.8%)

Markets paid little heed to the latest batch of inflation readings. That’s perhaps because of four reasons. One is that the year-over-year rate picked up by more than expected. Second is that traditional core CPI sharply accelerated. Three is that the smoothed Q4 figures for headline and core gauges were a little firmer than the BoC expected way back in the now partly stale October MPR. Fourth is that inflation’s breadth increased again.

Against these points, however, is that the higher frequency measures for trimmed mean and weighted median ‘core’ measures of inflation continued to decelerate.

In other words, it’s a fine dog’s breakfast and the dog’s turning up its nose at the bowl and marching on by anyway. The dog’s holding out for something better. Something clearer. A bigger treat or shock. The BoC’s clear message is that it is on a prolonged hold.

A quick glance at charts 1 and 2 reveal one reason why they are doing so: we’ve seen soft patches in volatile data multiple times to date. Monetary policy cannot respond to every little quirk in sampled data even without getting into myriad other considerations that I shared in my week ahead focus on the BoC. It needs to give time for easing to date to work through the system amid forward-looking drivers of inflation, not least of which are potential lagging influences of higher costs.

DETAILS

The year over year headline rate of inflation climbed two-tenths to 2.4%. On base effects alone, it would have jumped to 2.6% if nothing else had changed. Part of the reason for this is because of year-ago changes in the GST/HST.

But the headline rate climbed by less than base effects alone, yet more than consensus estimated by landing at 2.4% y/y.

Seasonally unadjusted CPI was down –0.2% m/m but up 0.3% m/m SA.

Food prices were a benign influence (+0.1% m/m NSA, 0.25% m/m SA) but energy prices fell -4.2% m/m NSA (-1.1% m/m SA).

Core measures diverged. Traditional core CPI that removes food and energy climbed by 3.1% m/m SAAR whereas trimmed mean and weighted median were soft again at 1.1% and 0.5% respectively.

The smoothed Q4 averages were nevertheless not so much of a surprise to the BoC. Headline CPI was slightly firmer than the BoC’s now stale October MPR. Back then, the BoC forecast Q4 at 2.0% y/y for Q4 total CPI and instead it was 2.3%. They expected the average of the trimmed mean and weighted median CPI gauges to be 2.9% whereas they landed at 2.8%.

Given that the BoC has been telling markets it’s done with rate adjustments barring big developments, smoothed figures like these won’t change their mindset.

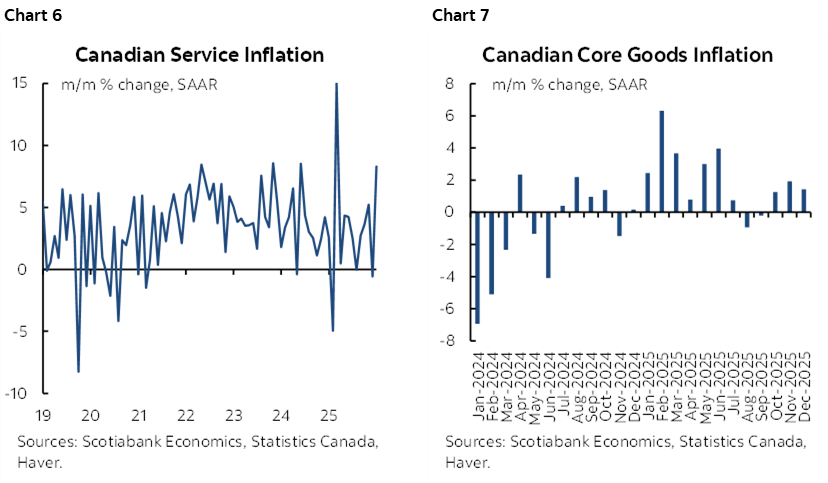

Chart 4 shows this was a firmer than usual month for traditional core CPI in unadjusted terms while chart 5 shows that the SA factor wasn’t terribly unusual.

Service price inflation accelerated (chart 6) while core goods inflation remained subdued (chart 7).

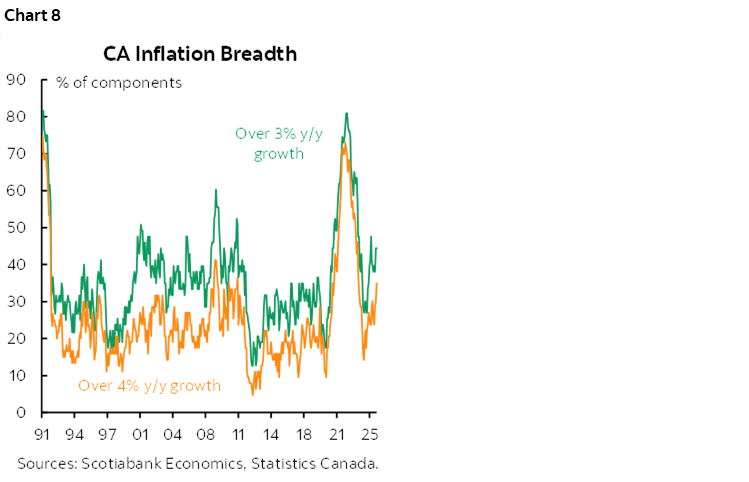

Breadth of inflationary pressures continues to trend higher (chart 8).

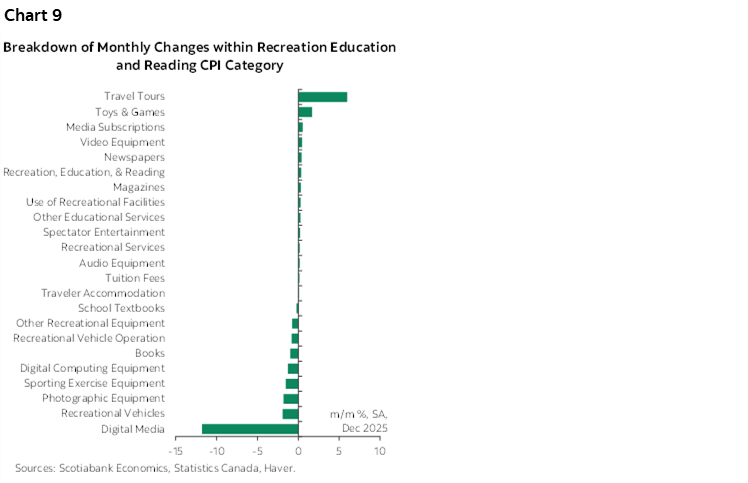

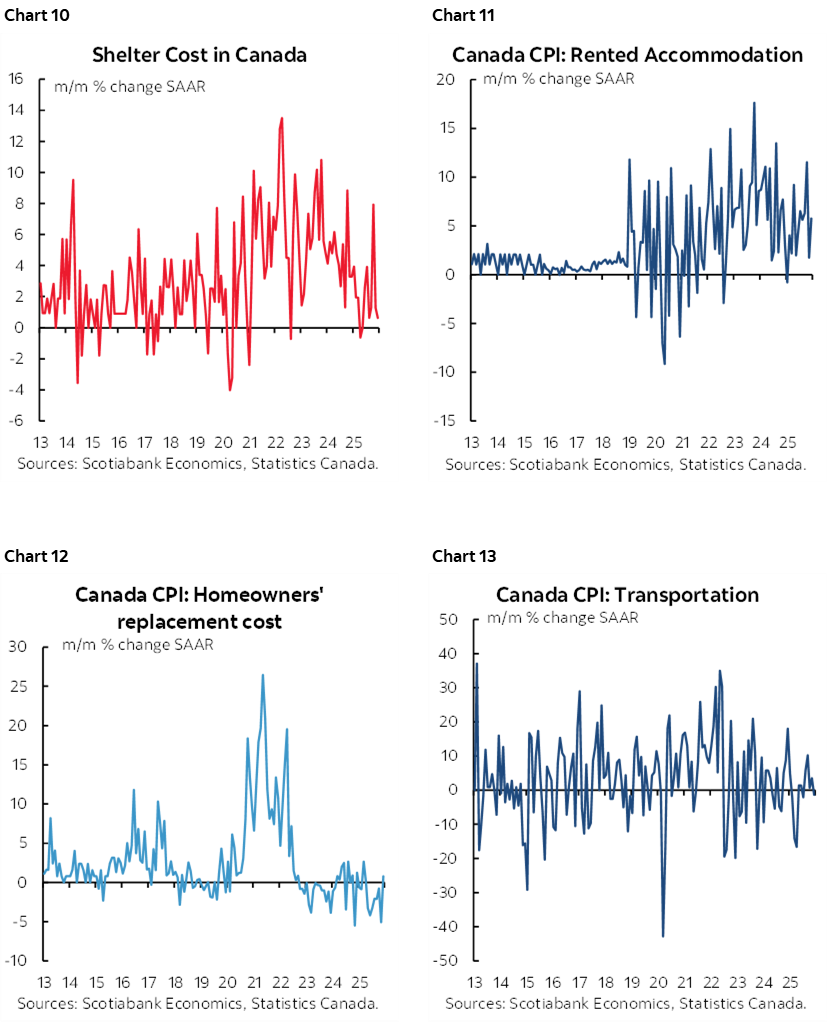

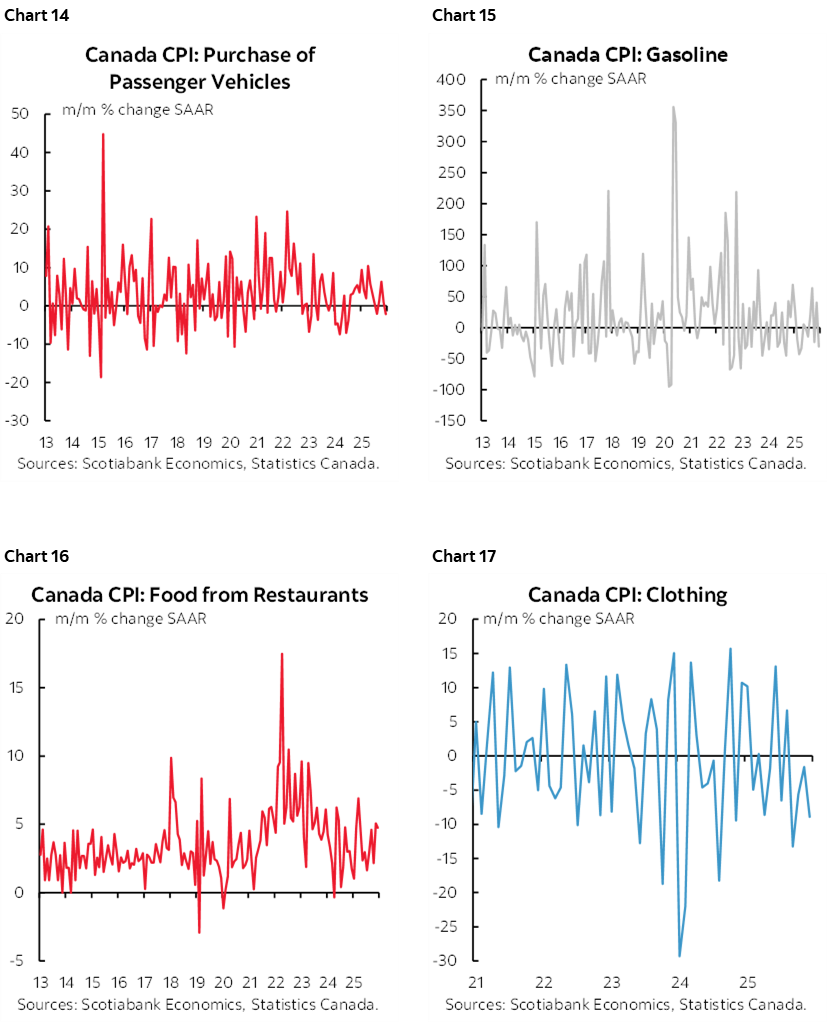

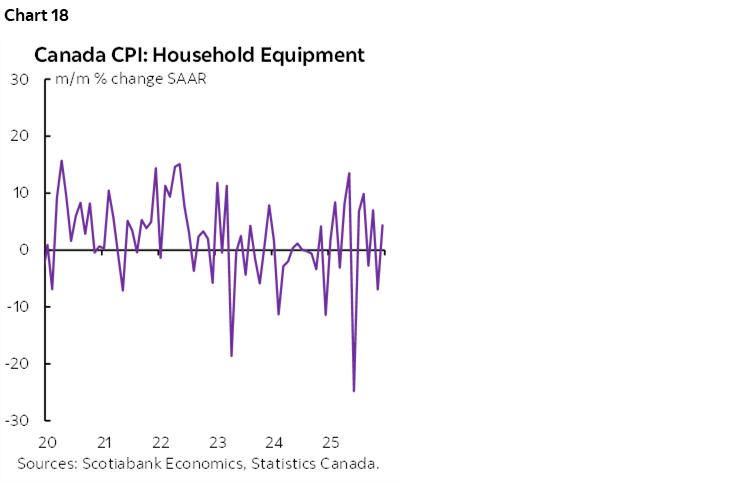

Charts 9–18 show break downs of other price subindices.

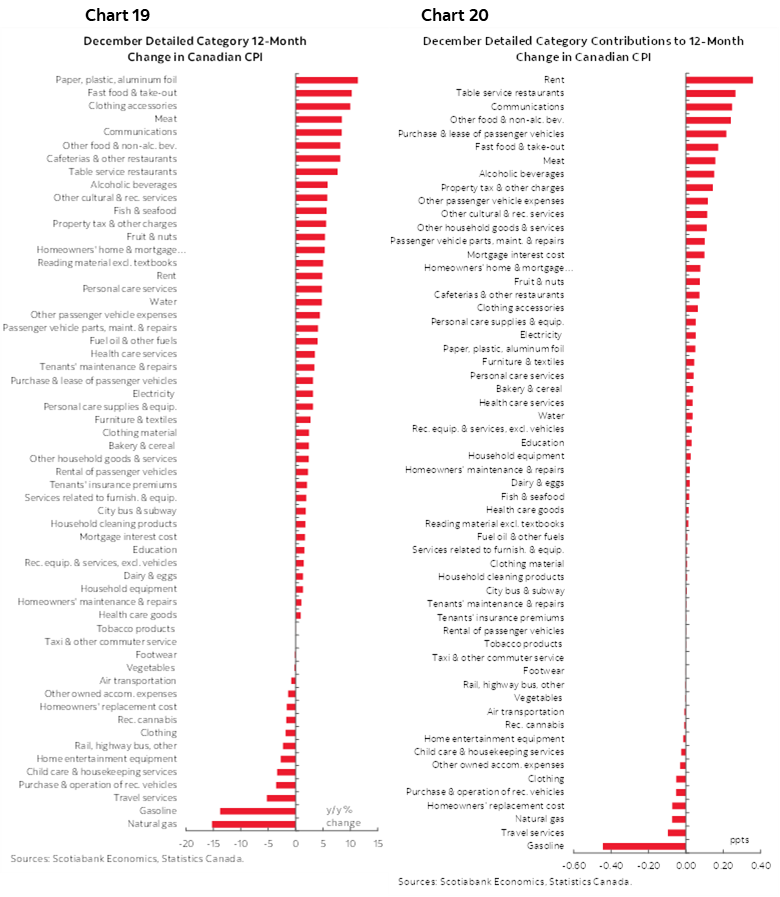

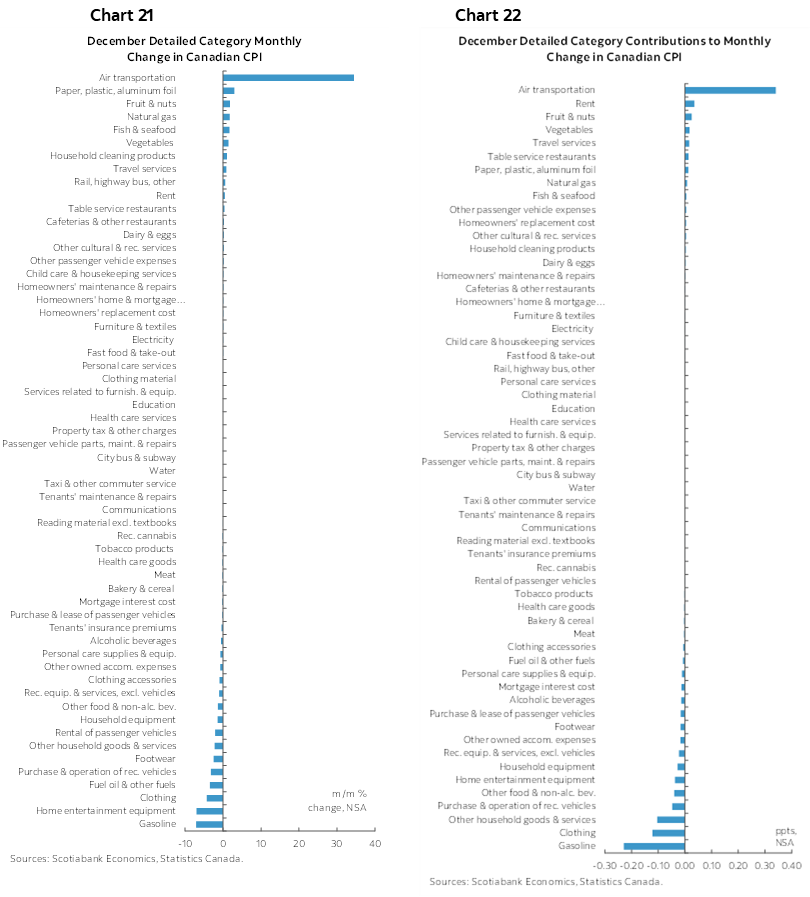

Charts 19–20 break down the CPI basket in y/y terms and weighted contributions to the y/y change in prices. Charts 21–22 do likewise for m/m changes.

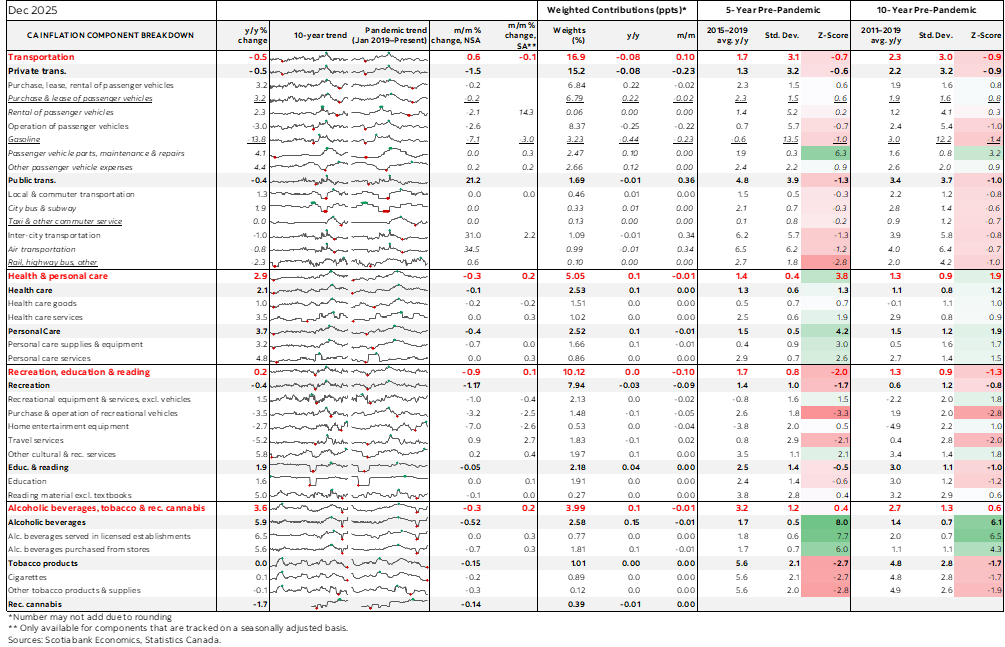

Please also see the accompanying table for further details and micro charts.

I don’t pay much attention to the BoC’s surveys (here and here) but they showed little change in the consumer and business measures of inflation expectations. Businesses expect more firings, but the 100 firms they consult didn’t anticipate the hiring surge over the past four months. Further, they’re so stale, that a private survey firm would be out of business if they did likewise. Imagine an election survey—two months after the election.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.