- The Federal Reserve cut by 25bps as widely expected

- Another 50bps of guided cuts this year matches our front-loaded forecast

- Only 25bps of cuts in each of 2026 and 2027 and then flat…

- ...around a highly uncertain neutral rate

- No concern was signalled about nearer-term funding market challenges

- Macro projections were very similar, but imply more easing is needed to get there

- Rates rose slightly, dollar modestly appreciated, S&P shook it off

The Federal Reserve Open Market Committee cut the fed funds policy target range by 25bps as widely expected and priced. Rates rallied at first upon seeing the dot plot of the Committee’s future rate moves, but then quickly sold off on a combination of rethinking the projections and in response to remarks during the press conference. Overall, the effect was largely a wash on the dollar, the overall term structure of rates, and the S&P500. Not rocking the boat on the first resumption of rate cuts since last December was probably exactly what Chair Powell was hoping for.

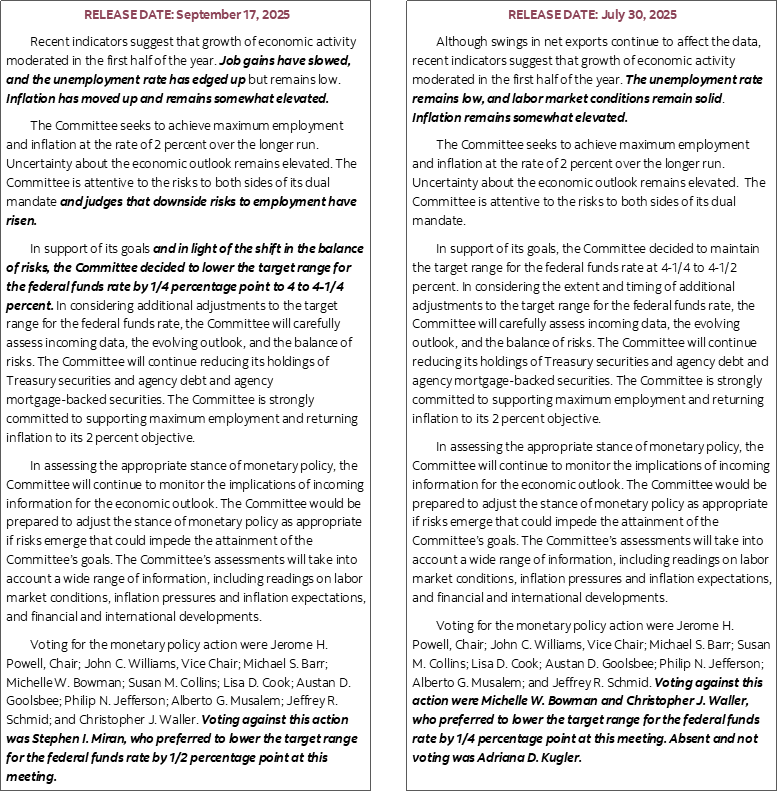

Please see the accompanying statement comparison. The Summary of Economic Projections including the dot plot is here. A press conference transcript is offered.

The market’s first response to the communications drove lower yields because of the following points:

- the dots signalled (barely...) that they're cutting in each of October and December.

- they added a bit more easing next year to retain the same broad outlook.

- There was a statement-codified emphasis upon more job market concerns.

- nobody dissented in the greater or lesser camps except for Miran that few treat seriously.

Rates then sold off during the press conference. Key reasons may have been Chair Powell’s comments that faded the dots, his remark that they are still taking it meeting by meeting with high uncertainty around the projections rather than conviction toward a preset outcome, they there is still a need for a restrictive stance, they are still mindful toward inflation risks, and conflicting comments (I thought) on the job market. On the one hand Powell says the job market has slowed and risks risen, and on the other hand he's saying the breakeven rate for payrolls could be zero or very close to it which would lessen concern about the slowdown in job growth so why all the fuss? Why fade inflation risks in favour of concern over the job market?

STATEMENT CHANGES

Please see the accompanying statement comparison. The statement was equally cogent to the prior one with salient changes as follows:

- the opening current conditions paragraph emphasized more concern about the job market. It also acknowledged that inflation has moved up.

- The Committee now “judges that downside risks to employment have risen.”

- The statement codified concern that the balance of risks has shifted toward the labour market.

ONLY ONE DISSENTER

There was only one dissenter which was surprising given the range of views being expressed by various members into the meeting. That dissenter was the one borrowed from the Trump administration—Governor Miran who preferred a 50bps cut.

Kudos to Chair Powell for maintaining cohesiveness across the rest of them.

A SCATTERED DOT PLOT

Any sense of cohesion quickly went out the window with the dot plot of future rate changes.

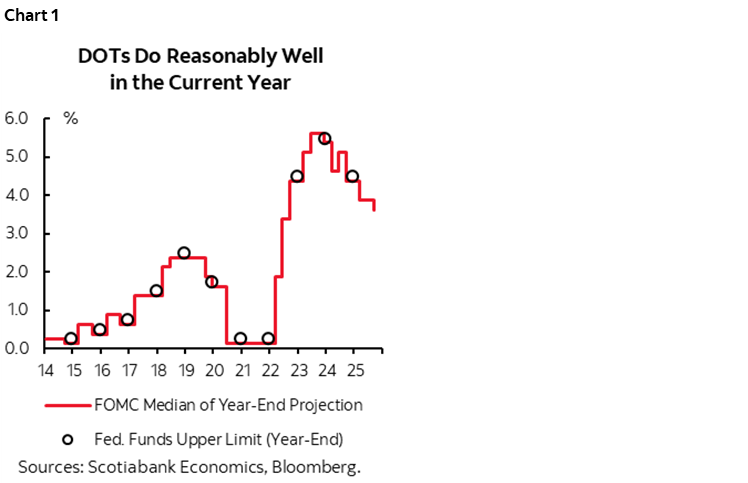

The median projection is compatible with our projection for a straight line of policy rate cuts at least into year-end totally 75bps of cuts. The median expects 50bps of further cuts into the remaining two meetings in October and December on top of today’s 25bps cut. At this late stage of the year—and barring any big shocks—they do what they say by year-end to a very high probability as shown in chart 1.

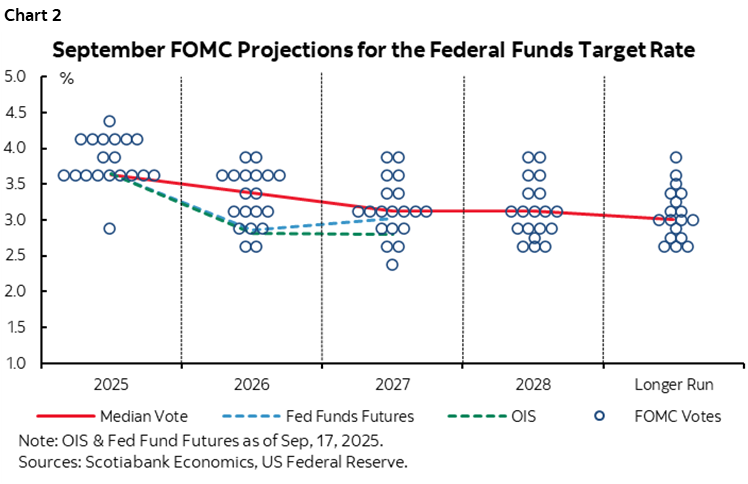

The dispersion of that median view is high (chart 2). Nine expect the fed funds upper limit to land at 3.75% by year-end for a total of 75bps of cuts including today’s. Two think only 50bps of total cuts. Six expect this to have been the only cut this year. One curiously either expected a hike or (much more likely) didn’t support the cut but was a nonvoting member who could not formally dissent. One was a total outlier who preferred a total of 150bps of cuts including today’s; that is most definitely Mr. Miran’s view as he pines for Trump’s affections as the government’s voice. Remove that dot.

Next year’s median projection expects one more cut than previously expected down to a 3½% fed funds rate followed by 3¼% the next year and the year after.

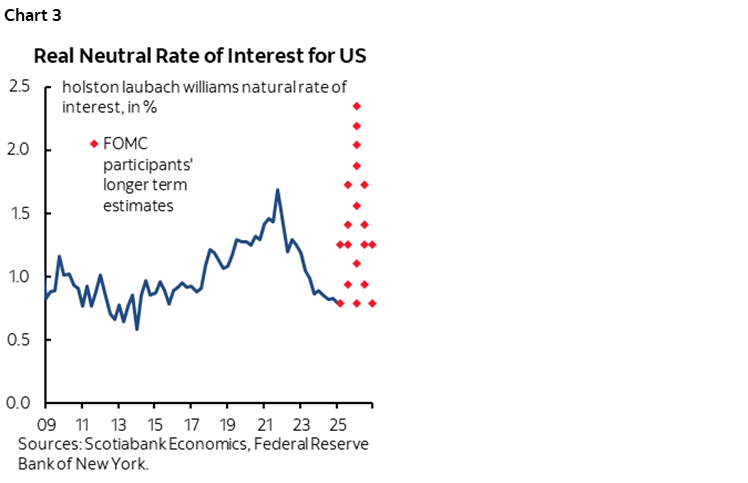

The neutral rate guess was left unchanged, but chart 3 shows not to treat that very seriously in real terms. The Committee is as scattered as you’d expect by yelling ‘homework time’ in a playground.

FORECAST CHANGES

Changes to the macroeconomic projections—or rather, the absence thereof—drove several lines of questioning in the press conference. The questioning was aimed at why the greater concern about easing if you really haven’t changed the forecasts around. Chair Powell’s answer should have been that it’s because the Committee members are likely assuming that securing a similar outlook in the face of recent developments probably requires a bit more a policy nudge. He did not say so and largely danced around the usefulness of the dots and the uncertainty.

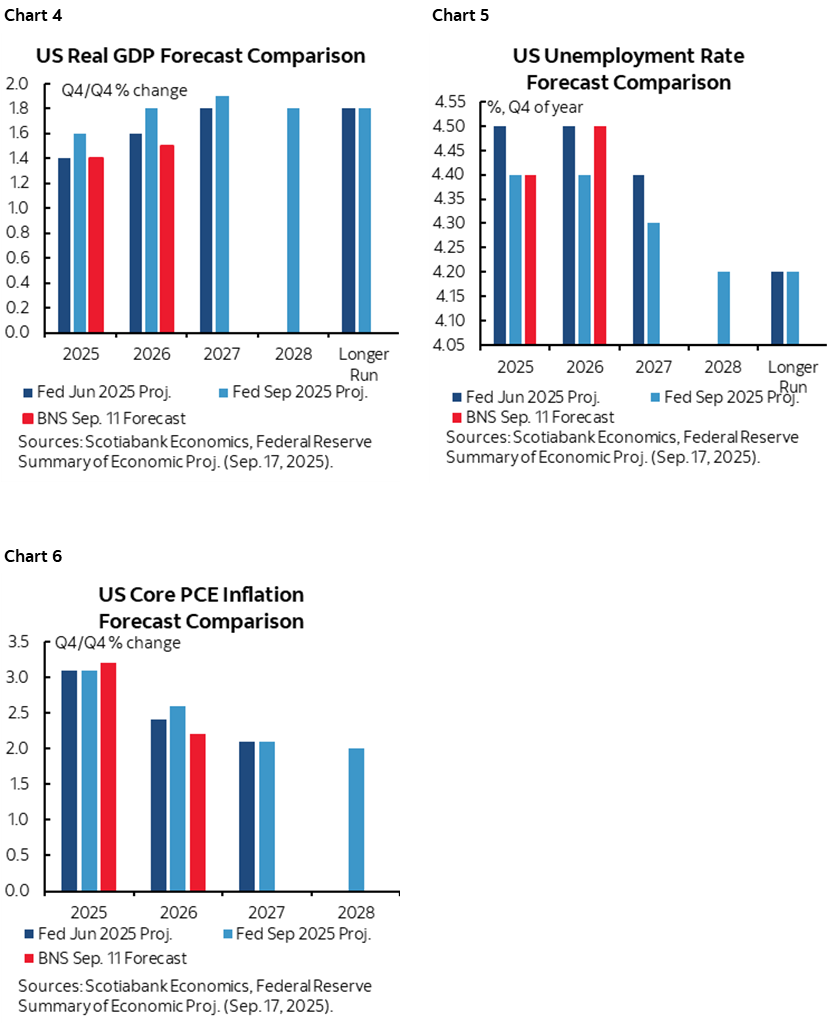

Charts 4–6 compare the FOMC’s new projections with the previous ones from June and against our nearer-term projections.

GDP growth was revised up a bit in 2025–27 on the customary Q4/Q4 basis.

The unemployment rate projection was little changed despite all the hysteria about the job market. They forecast an unchanged 4.5% this year, 4.4% next year which is down a tick from previously, and 4.3% in 2027 which is also down a tick from previously. The estimated long run natural rate of unemployment was unchanged at 4.2

Core PCE inflation was revised up next year to 2.6 (2.4 prior), and left unchanged in each of 2025 and 2027.

PRESS CONFERENCE TRANSCRIPT

The following is an attempt at capturing the main questions and answers during the press conference. Any errors or omissions are due to my typing abilities! It remains my opinion that Chair Powell is being too dismissive toward inflation risk and has pivoted too far toward concern about the labour market that he inconsistently refers toward. The supply chain drivers of inflation risk are much more complex than tariffs alone and may take years to unfold as opposed to the silliness around near-term data obsessions. If I’m right, then Powell’s pivot to jobs and away from inflation risks a similar mistake as in the pandemic.

Q1. Governor Miran retains his White House position and is on the Fed Board. Does this compromise the Fed's independence? How can you maintain the public's perception of independence?

A1. We did welcome a new member and remain united. We are strongly committed to our independence and beyond that I don't have anything to share.

Q2. If companies are eating the tariffs instead of raising prices then is this why employment is paying the price?

A2. It's certainly possible. The rise in goods prices accounts for most of the rise in inflation over this year. They are not very large effects and we do expect them to continue to build over the next year. Why employment is doing what it's doing is more about immigration. There is little supply of new workers.

Q3. Do economic conditions and the balance of risks no longer warrant a restrictive policy setting?

A3. I don't think we can say that. We kept our policy at a clearly restrictive level over the course of this year. That's because the labour market was in a strong position. I can no longer say that. The risks were clearly tilted toward inflation. I would say they're moving toward equality, or greater equality which suggests we should be moving in the direction of neutral.

Q4. How serious was the option of a greater than 25 move and what criteria would be needed?

A4. I wouldn't say that was seriously discussed. We've made big moves in the past. I don't see those conditions now. We're moving in the direction of balance which warrants a change in policy.

Q5. Is today's cut insurance against the possibility of a weakening job market or because the risk of downturn is thought to be greater? I'm asking because the forecast for the unemployment rate didn't change.

A5. What's different now is that there is a very different picture now for the risks facing the labour market. That tells you it's time to take that account in our policy.

Q6. The median projection doesn't see inflation sustainably at around 2% until 2027–28. Why ease.

A6. I'd say that's because the risks to inflation have lessened and the risks to the labour market have increased.

[ed. he should say the forecasts for UR, PCE and GDP likely held firm because they're cutting more]

Q7. How do you see job weakness due to immigration but merit policy easing despite persistent inflation?

A7. I wouldn't say immigration is the only driver of a weakening job market.

Q8. You keep pushing out the 2% inflation target's achievement. Does this present credibility problems?

A8. No one really knows where the economy will be in three years but the nature of the exercise is to write down numbers that return to policy goals.

Q9. What will the Fed do if prices do pick up more?

A9. Our expectation is that inflation will move up more this year but that those will turn out to be a one time price increase. We can't just assume that though. Our job is to make sure that is what happens. The pass through into inflation from tariffs has been smaller and smaller and the case for an inflation outbreak has been less. That says to us that the risks to the other mandate are greater. When the framework is in tension, we ask which mandate is at risk of being furthest from the goal. Now we see risks in the direction of the job market.

Q10. Missed but seemed repetitive in his answers

Q11. You have not used the term recalibration. Are we in the process of getting back to neutral or going meeting by meeting?

A11. We're in a meeting by meeting process and will be looking at the data. The SEP is an accumulation of the views of 19 people. We don't debate or try to agree. We just write them down. The actual decisions are made on the basis of the incoming data and balance of risks. Ten out of 19 participants wrote down 2 or more cuts over the remainder of the year and 9 who wrote down fewer. Look at the SEP through the lens of probabilities.

Q12. Is the dispersion in the outlook a sign of uncertainty?

A12. We have a situation with two-sided risks with no risk-free path. It's not at all surprising to me that you have a range of views. It's partly about a different range of views on the outlook but also the tension between goals. It would be pretty surprising if you didn't have a pretty wide range of views.

Q13. What should people watch to determine that the Fed is making decisions on the basis of the economic outlook rather than political considerations?

A13. It's deeply in our culture to do what we think is right, not the political environment.

Q14. Is the court case around Lisa Cook related to Fed independence?

A14. It would be inappropriate for me to comment upon a court case.

Q15. How can the Fed basis important decisions on data that seems to be noisy? Referencing job market revisions.

A15. The revisions were almost exactly what we had expected. [ed: ok so why did you act surprised and pivot after getting them?]. Low response rates are a concern. The way to get higher response rates is to make sure the agencies have proper funding. The first response is low but by the second and third months the response rates are much higher.

Q16. Had you known revisions to jobs would you have changed your mind earlier?

A16. We see where we are now and we took that appropriate action today.

Q17. Why is a quarter point going to arrest challenges in the job market and economy?

A17. I didn't say a quarter point would, you have to look at the whole path of rates and market expectations matter. It's important to use our full set of tools.

Q18. Are you concerned about skewness in spending and policy implications?

A18. They're spending. Basically saying they have to look at the macro picture.

Q19. Bessent has said the Fed suffers from mission creep and bloat. Are you open to an independent review?

A19. I'm not going to comment on what the Secretary says. We just went through a lengthy and very successful process to update our monetary policy framework. We're going through a 10% headcount reduction at the Board and all the federal reserve banks. Employment at the Fed will be at the same level as a decade ago and probably more.

Q20. Do you buy the theory that AI is already impacting the job market?

A20. You are seeing some effects but it's not the main thing driving it particularly for young people coming right out of college who are able to use AI more than in the past. It may be part of the story that job creation has slowed down, the economy has slowed down.

Q21. What evidence do you see tariffs showing up in inflation?

A21. Last year goods inflation was negative. Back 25 years goods prices generally went down. That was not the case in the pandemic but we essentially returned to zero or negative inflation. Now we think goods inflation is contributing about 0.3 or 0.4 to core PCE inflation. The tariffs are mostly not being paid by exports. They're mostly being paid by the companies between the exporter and consumer and taking on a lot of those costs and not passing them on yet. All of those companies will tell you they have every intention of passing through but they're not doing that yet. The evidence is very clear that there is some pass through.

Q22. What conditions would you see for you to leave the Fed in May?

A22. I have nothing to say today.

Q23. How can markets and the public interpret Miran's speeches and forecasts?

A23. There are 19 participants of whom 12 vote on a rotating basis. No one voter can move that around other than to be incredibly persuasive with strong arguments. That's how it's going to work.

Q24. There was a lot less dissent today than people expected. Why the strong consensus? Why are the dot plots so scattered?

A24. There is a wide assessment that the situation has changed in the labour market. The new data—and it's not just payrolls—suggest that there is meaningful downside risk which is a reality now. That's broadly accepted and meant different things to different people. Some supported more cuts than others.

Q25. Where do you think the nonfarm breakeven rate is?

A25. It's clearly come way down. You could say it's somewhere between zero and 50,000. A very lower number of people are joining the labour force. That's where a lot of the supply of labour was coming from over recent years. Supply and demand have come down together but unemployment has moved just one tick out of the range of where it has been.

Q26. Are current rate levels hindering the housing market outlook?

A26. Housing is an interest-sensitive activity. We don't set mortgage rates but our policy changes do tend to affect mortgage rates which will raise demand and lower borrowing rates for builders will raise supply. Most would agree you need big changes in rates for it to matter a lot for the housing sector. There is a deeper problem for housing that the Fed cannot address and that is a deep nationwide shortage of housing.

Q27. Do policymakers still lack conviction about their forecasters?

A27. Right now is more uncertain than usual. Most forecasters would say they don't have great confidence in their forecasts.

Q28. Why continue to reduce the size of your balance sheet?

A28. We've said we'll continue cutting until we get to ample reserves. We don't think they will have a large effect on the economy.

Q29. Miran says the Fed has three mandates including moderate long-term interest rates. How do you think about this?

A29. We always think of it as the dual mandate of price stability and full employment because we think of moderate long-term interest rates as being served by this dual mandate. We haven't thought about that in a long time and there is not thought of incorporating this in a different way.

Q30. How concerned about you by the health of consumer finances given default rates?

A30. Lower rates should help. A strong economy with a strong labour market is what we're aiming for with stable prices which should help.

Q31. Could rate cuts overheat financial markets?

A31. Our focus is on maximum employment and price stability. We monitor financial stability very carefully and households and banks are in good shape. We don't have a view that financial assets are properly valued. We look at a range of readings and we don't have that view that they are overvalued right now.

Q32. Short-run inflation expectations have moved up can you comment. Do you think deficits could influence longer-run inflation expectations?

A32. Short-run have moved up. Fortunately except for Michigan the longer-term measures have been running at levels that are consistent with 2% inflation. We don't take that for granted and remain committed to 2% inflation.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.