- Bonds and stocks crushed by CPI, dollar soars

- US core CPI trend remains very hot…

- …as market hope for a Fed pivot remains wishful thinking

- The Fed’s dot plot is very likely to shoot past 4%

- Canada’s curiously timed fiscal stimulus

- Market participants to assess implications of Canada’s sudden holiday on Monday

- US CPI m/m % // y/y %, August:

- Actual: 0.1 / 8.3

- Scotia: 0.1 / 8.1

- Consensus: -0.1 / 8.1

- Prior: 0.0 / 8.5

- US core CPI m/m % // y/y %, August:

- Actual: 0.6 / 6.3

- Scotia: 0.4 / 6.1

- Consensus: 0.3 / 6.1

- Prior: 0.3 / 5.9

Did you hear the one about how US inflation is cooling and the Fed’s about to pivot? Unfortunately the punchline went over like a lead balloon and delivered a sucker punch to markets this morning.

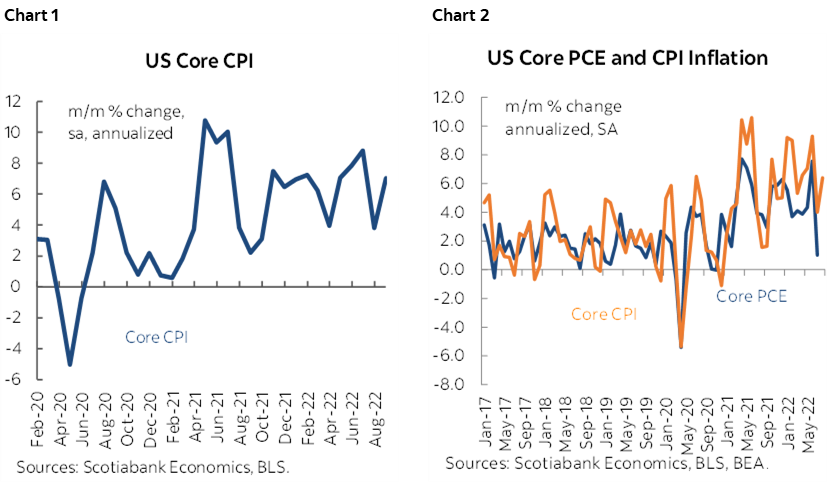

Core CPI soared to 0.6% m/m and a 7% m/m clip in August at a seasonally adjusted and annualized rate. There is zero evidence that the pressures are durably cooling (chart 1). That remains wishful thinking absent empirical supports. Month-end core PCE is likely to rebound to at least 0.6% m/m non-annualized and likely higher after undershooting the prior month (chart 2). To put core in context, 0.6% m/m SA restores the trend from April to June when 0.6–0.7 monthly core cpi prints were being registered before the 0.3% deceleration in July that had some folks prematurely declaring that inflationary pressures are ebbing and the Fed would soon pivot. Not!

The figures cement a 75bps move next week alongside a hawkish dot plot that will likely show the policy rate crossing 4% over Q4/Q1. It’s very unlikely that the FOMC signals a pause at any of its upcoming meetings not least of which because they’d have to have extraordinary faith in the ability of their models to forecast inflation when models cannot do well at capturing regime changes which is what we very well may be going through.

Fed funds futures pricing for next week’s move is now over ~80bps. There was a violent swing in the US front-end as the 2-year Treasury yield jumped by about +24bps after the release. US 10s increased by about 15bps as the 2s10s curve bear flattened. The USD took off and gained over 1¾% on a DXY basis post-data which triggered a massive move away from dollar softening against all major crosses into the data toward a stronger dollar against everyone post-data. The DXY is now back at last Thursday’s levels before the dollar weakened over Friday and Monday. The S&P is down by over 3% on a combination of Fed fears and the natural increase in recession risk. Basically take every risk-on trade before the data and flip it around and that about sums it all up. Raise those recession probabilities and amplify the scenario testing around something that’s a 4-handled Fed funds rate with more upside than downside risk in the ranges.

I was above consensus at 0.4% m/m for core CPI and the Cleveland Fed’s ‘nowcast’ was indicating 0.5% but the 0.6% m/m rise blew past everyone’s estimates. The underlying breadth reinforced how hot inflationary pressures remain in the US economy.

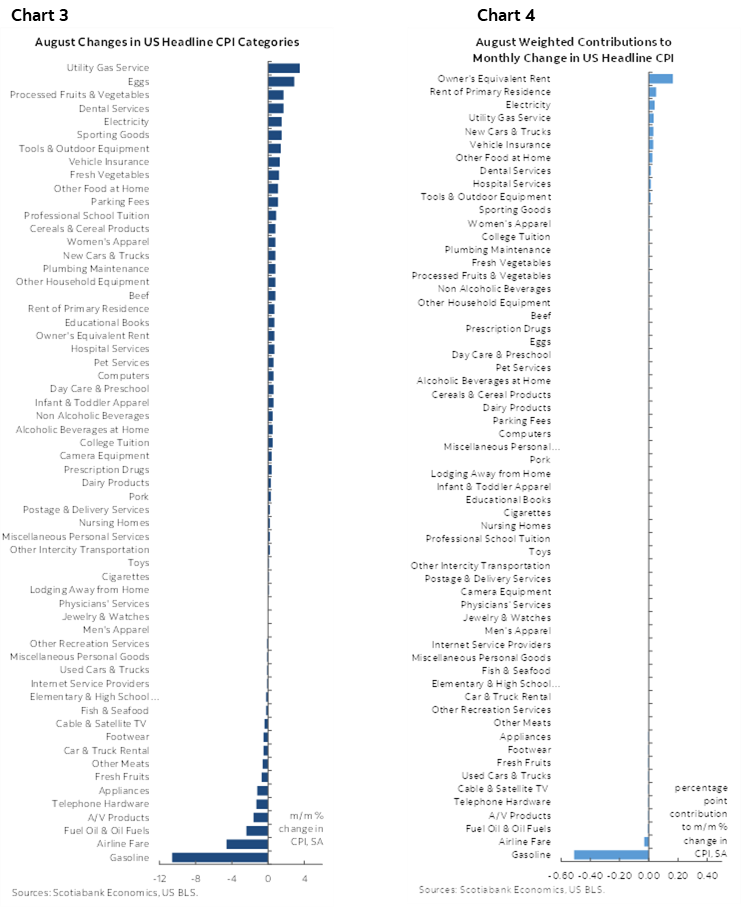

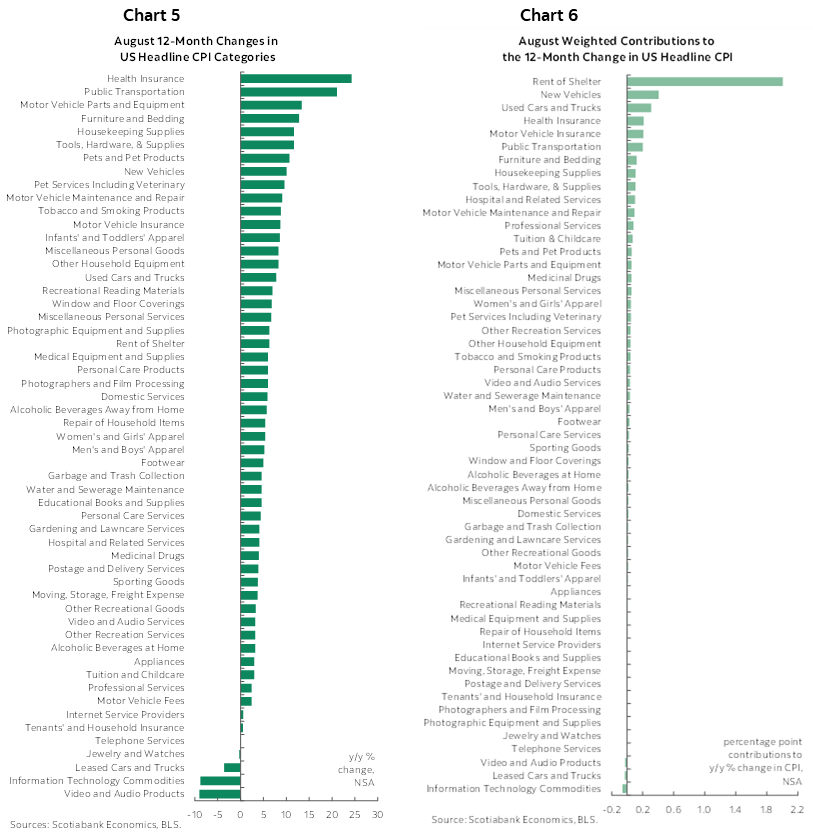

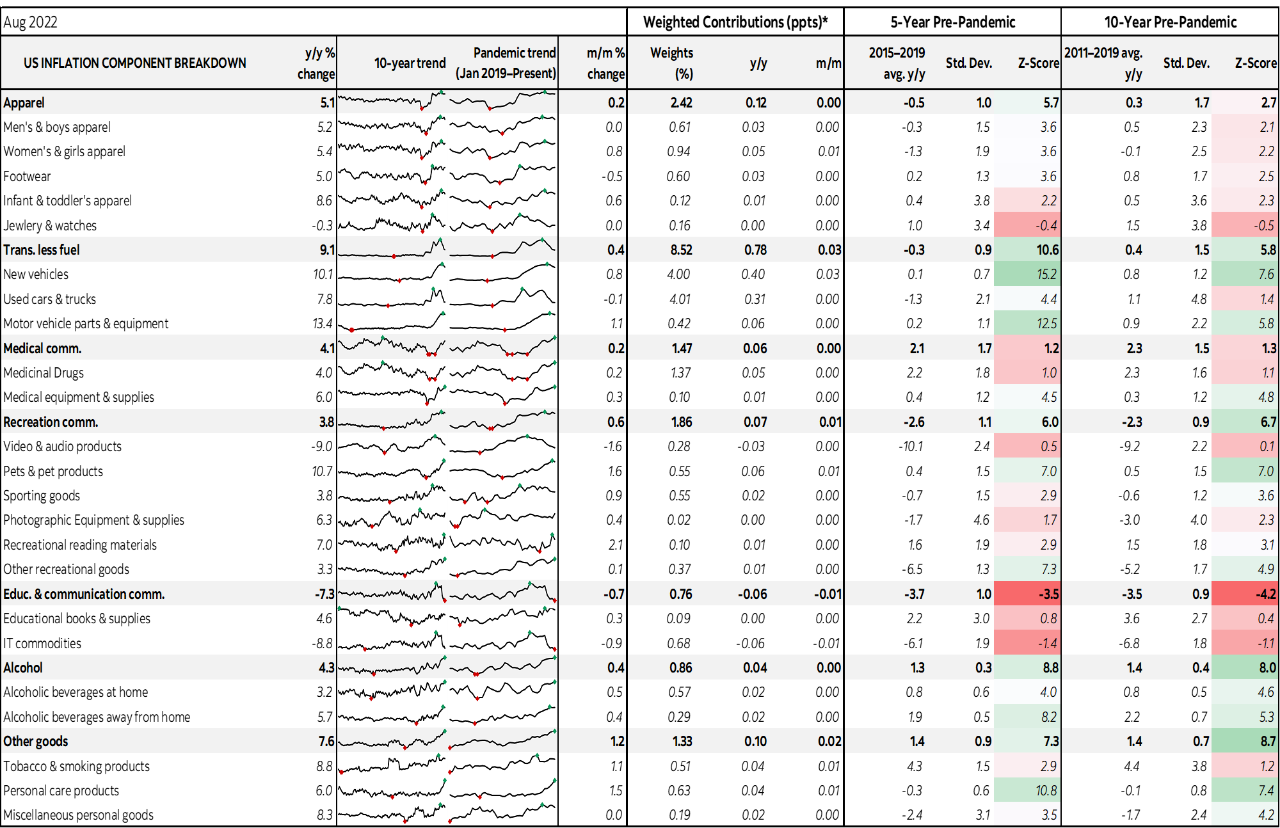

Details (here) reinforce the breadth argument. Please see charts 3 and 4 that show unweighted and weighted contributions to m/m inflation as well as charts 5 and 6 that do likewise for the y/y rate of inflation.

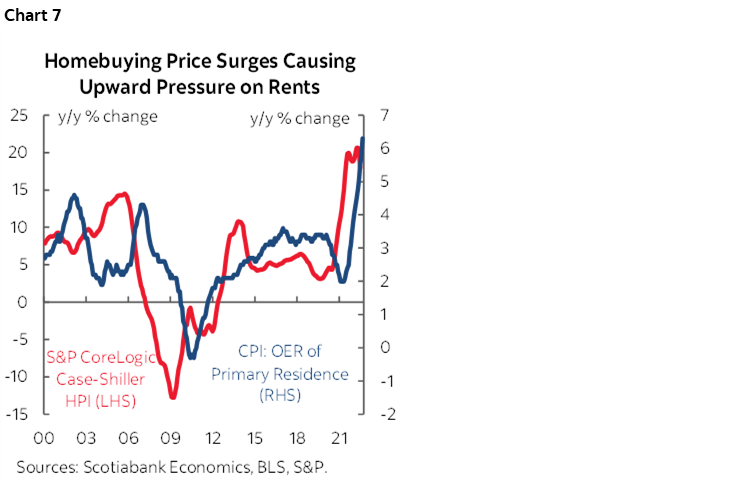

Across the components, owners’ equivalent rent was the hottest category in weighted terms (~24% weight). It was up by another 0.7% m/m. For that to turn lower requires two things to happen. One is that changes in repeat-sales house prices have to softer if not decline. Repeat sales house prices were still rising up to June (July due out on the 27th) albeit at a softer 0.44% m/m SA pace compared to 1– and 2-handled gains prior to that. We need a long trend of very weak or negative changes in house prices and then tack on 6–18 month lags before US OER ebbs as shown in chart 7. In other words, don’t hold your breath hoping for housing to be a disinflationary influence any time soon.

Used vehicles were down by -0.1% m/m but new vehicle prices were up 0.8% m/m although at a 4% weight that's a zero contribution. That’s a big fat meh.

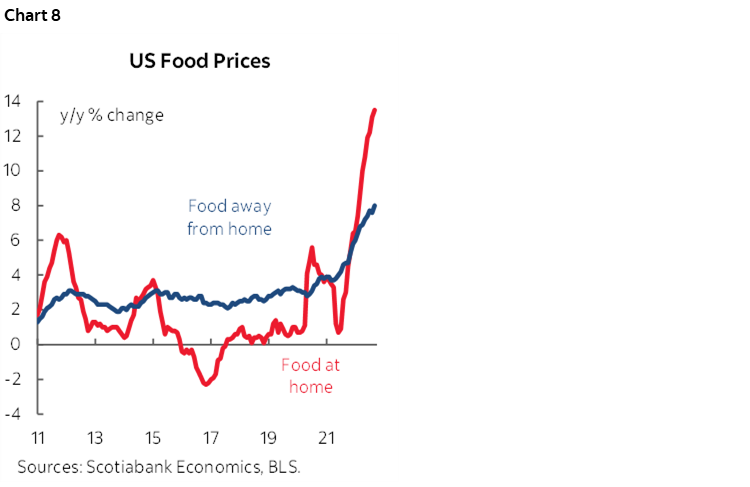

Several high contact price trends were mixed. Food away from home prices (restaurants, take-out etc) were up 0.9% and at-home (ie: groceries) and away-from-home food prices continue to soar in y/y terms (chart 8). Just wait for drought to hit them. Lodging was up by 0.1% m/m. Airfare fell -4.6% m/m and vehicle rentals were down -0.5% m/m.

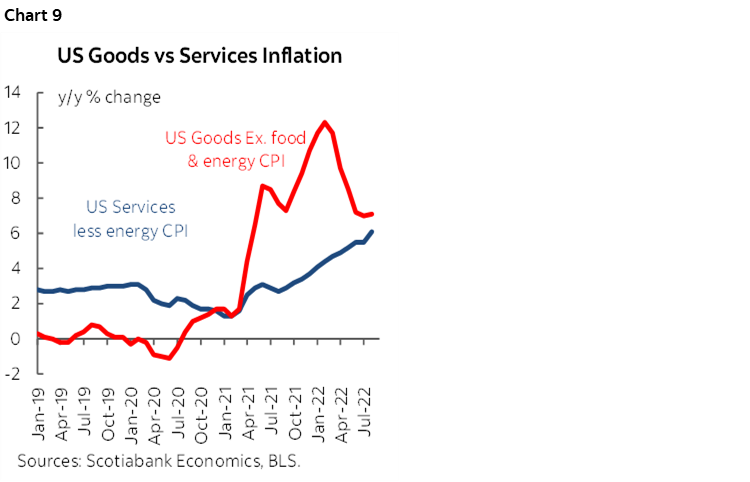

Still, overall services ex-energy prices were up 0.6% m/m and so the broad services inflation picture remains very hot. As chart 9 shows this accelerating trend in service prices is now being accompanied by sticky core goods inflation.

CANADIAN IMPLICATIONS

Canada’s bond curve sold off in sympathy to the US moves. There was a 20bps jump in the 2-year yield and a 16bps increase in 10s. The Canadian dollar depreciated by about 1½ cents to the USD.

Hotter US inflation that drives aggressive Fed tightening and weakens CAD is likely to motivate the Bank of Canada to have greater confidence to shoot past 4% with its policy rate.

Then enter the implications of Canadian fiscal stimulus now that we have details. It will be tough slogging to convince markets on a day like today that spending more won’t drive hotter inflation. In fact, the two-year GoC yield pushed a few basis points even higher as the announcements hit.

- Increased GST Credit (here): At a cost of $2.5 billion a one-time lump-sum payment will be made before the end of this year. Merry Christmas! Payment will be automatic to 11 million individuals and families.

- Dental care (here): Tax-free payments of up to $650/kid will be provided starting on December 1st with the exact amount depending upon the family’s income bracket up to $90k. A half-million kids are estimated to be eligible at a cost of nearly $1 billion. The qualifying criteria appear to be lax given the ‘if required’ need to prove that the amounts received went to actual dental care. It’s unclear how long they will have to show receipts, if ever. Incidence analysis will be key in determining the ability of dentists to absorb any possible increase in demand for their services if the proceeds are spent accordingly and the effects on service prices.

- Canada Housing Benefit top-up (here): At a cost of another $1.2 billion there will be one-time $500 tax-free payments to 1.8 million low-income renters before year-end.

Recall that retail sales equalled about $57 billion in June of this year with July pending. The total ~$4.7 billion cost of the three initiatives is equal to about 8% of nominal retail sales. That’s not to say that a single month of sales will be lifted by this amount. By how much and over what time and on what types of goods and services with the latter underrepresented in retail sales are all highly uncertain and depend upon a number of assumptions but it’s rather likely that some of the amount will be spent.

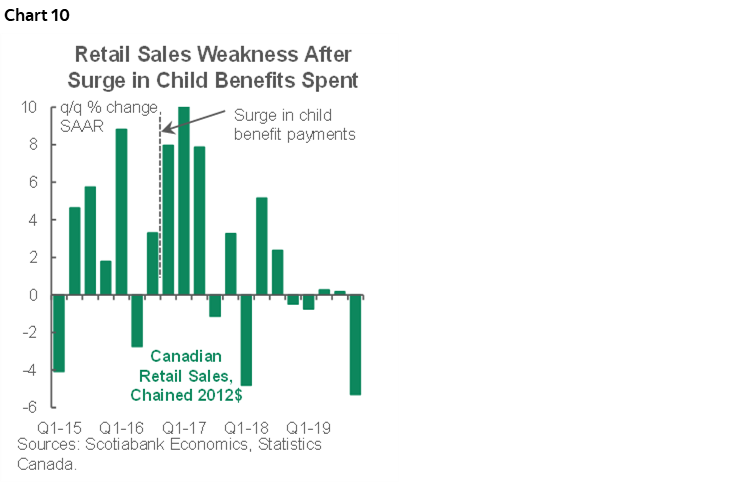

This is what happened when the child benefit payments were sharply increased in years past with no strings attached to what was done with the proceeds as a surge in sales then gave way to a demand vacuum (chart 10). The lift to spending this time around is likely to be focused upon Q1 and Q2 given the timing of implementation and recognition lags.

We will be assessing the implications for price pressures into H1 but it seems sensible to assume that this will add to pressures on measures of core inflation relative to what would have otherwise occurred and hence aggravate the Bank of Canada’s stance on monetary policy. Any belief that it will ease inflationary pressures must have studied different economics textbooks. The information today suggests that the BoC is likely to be dragged along by the Fed with domestic fiscal stimulus reinforcing the likelihood that the policy rate breaches 4% by December if not October.

Also note that Monday will be a Federal holiday to honour Queen Elizabeth II. That means markets will be shut. Market participants are tracing through the suddenly disruptive implications for settlement, contract expiries, deal timing etc.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.