- Multiple measures suggest labour slack is going fast if not gone

- Wage growth is ripping higher as perhaps the best signal

- Hours worked reinforce tracking of the H2 GDP recovery

- The BoC will shift to the reinvestment phase on October 27th…

- ...but is falling further behind market pricing for hikes

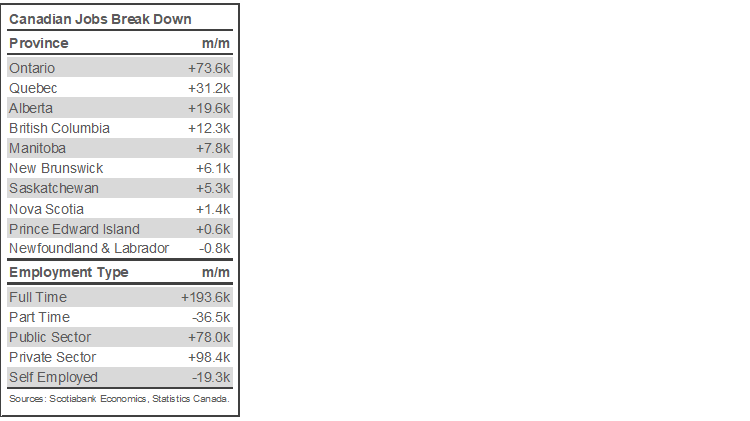

CDN Jobs, m/m 000s // UR %, SA, September:

Actual: 157.1 / 6.9

Scotia: 80 / 6.8

Consensus: 60 / 6.9

Prior: 90.2 / 7.1

The Canadian dollar got a helping hand from jobs numbers on both sides of the border this morning while borrowing costs went up across all Government of Canada bond maturities relative to the US. That’s because Canada registered a stronger-than-consensus gain of 157k jobs while the US posted a weaker-than-consensus gain. See the accompanying table for summary measures.

HAS SLACK ALREADY LEFT THE BUILDING?

Canada has recouped all lost jobs during the pandemic but whether that indicates the country has exhausted all labour market slack is still an open question. Wage gains may be suggesting that slack is gone and I’ll return to what they are showing in a moment. Other measures are a bit more mixed but in my view net out to leaving the rest to policymakers other than at the Bank of Canada.

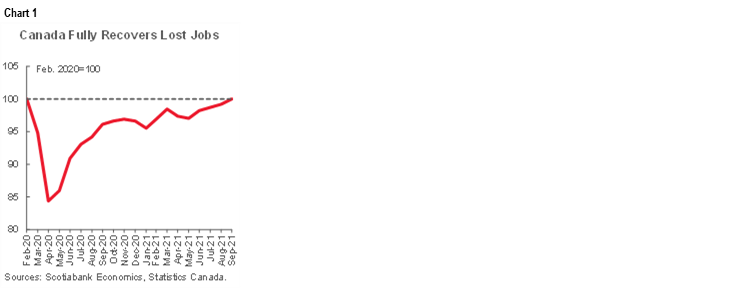

First, the country is now sitting dead flat on total employment compared to February 2020 (or +900 jobs). See chart 1. Check.

Second, Canada has also fully recovered in terms of the labour force participation rate at 65.5% which is back to February 2020 levels and only marginally below the pre-pandemic peak of 65.8% in April 2019. Check that box as well. See chart 2.

Third, the employment rate climbed to 60.9% which is only 0.9% below the pre-pandemic level. Almost check.

Fourth, the unemployment rate is now at 6.9% which remains higher than the 5.7% pre-pandemic level. Bear in mind, however, that the pre-pandemic unemployment rate was hovering around a record low and so targeting that while sitting at a zero policy rate and still buying bonds smells fishy to me. When measured using the same methodology employed in the US, Canada’s unemployment rate pretty much matches the US and yet Canada has a higher natural rate of unemployment than the US (chart 3). Check.

Fifth, the R8 underemployment measure fell by almost two percentage points in one month to 8.3%. That’s below the 8.6% reading in February 2020. Check.

Sixth, compared to the US after adjusting for different methodologies, Canada’s unemployment rate now stands at 5.2% versus 4.8% in the US.

The jobs recovery nevertheless remains uneven which will be highlighted in the further details section below. In my view, this isn't the Bank of Canada’s problem. It is up to the Federal Government and provinces to address this mismatch from a fiscal policy and training perspective. Some of these forms of lost employment might never be fully recovered if the pandemic has ushered in permanent changes in some types of work and some sectors. Monetary policy cannot target equal outcomes for all and it’s disturbing every time I hear unelected central bankers pretend they can do otherwise without causing bigger problems in the process — like generating inflationary pressures. Or creating imbalances in housing.

WAGE GROWTH IS SOARING

Some of us free market types think that price signals are the best arbiters of debates like how much slack exists. Enter wages.

Wage growth is ripping in Canada. A sharp three-month upward trend makes it impossible to simply ignore, though there is still going to be a fair debate over whether it is sustainable. Absent sustained productivity growth it probably is not without ultimately shortcircuiting, but even a sharp moderation from the recent run-up in wage growth figures would be supportive of the BoC’s inflation targeting framework.

At a seasonally adjusted and annualized rate of growth, wages were up 6.25% m/m in September. This follows 7.3% in August and 7.3% in July. The three-month moving average is a gain of 7% m/m SAAR. Chart 4 shows the recent trend. Meh, doesn’t fit the narrative, didn’t happen, just ignore it, right? The truth is likely somewhere in the middle between indifference and extrapolation at present rates.

This is not the BoC's preferred measure of wage growth (though it used to be…) which is the quarterly wage common measure, but wage common lags like the skinny kid at the back of the ice cream line-up. At rapid turning points we should probably be emphasizing the freshest available readings as a starting point to the debate. The wage common composite only goes up to Q2 since it is mostly derived from quarterly accounts up to Q2 and combined with Q2 readings for wage growth from the lagging payrolls survey and LFS. I would think we would want a measure of wage growth that is not skewed toward when much of the economy was shut given lockdowns in Q2 when the economy contracted. If you want a fresh measure of wage growth at the margin, then it's the measure of average hourly earnings for permanent workers right up to September that we got in today’s report and that measure is screaming higher.

Even on a two-year pandemic smoothed basis, StatCan points out that nominal wages are up 4.6% after adjusting for changes in the composition of employment. This measure of wage growth is slower moving than the one cited above, but even at this pace it is supportive of the BoC’s 2% inflation target in the 1–3% band.

This kicks into higher gear the question of whether it’s just a temporary spurt or whether wage data is a better signal of how tight job markets have become than the panoply of measures the BoC throws at the wall regarding nooks and crannies of underemployed Canadians. Even if it is not sustainable at such reopening rates of occurrence, it could well be supportive of the BoC’s inflation targeting framework at more moderated rate of wage growth.

DETAIL, DETAILS, GIVE ME DETAILS!

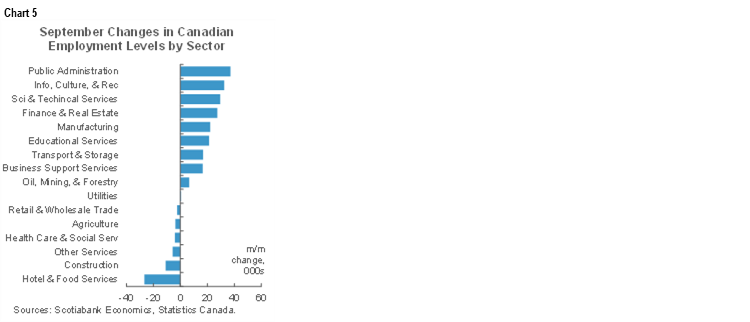

There was solid sectoral breadth to the gain (chart 5). Services were up 142k with the goods sector hiring another 15k workers. Within goods, the gain was mostly in manufacturing. Within services, 7 of 11 sectors were higher.

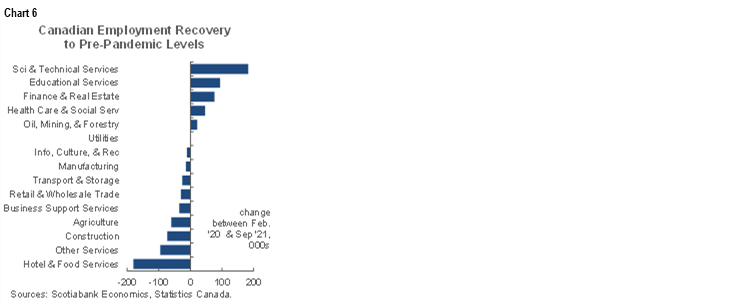

The cumulative recovery to date shows services employment is up a net 129k and it’s the goods sector that is still down a net 128k jobs. Chart 6 shows what subsectors in goods and services are up or down in net terms so far during the pandemic. Note, however, that it’s the public sector jobs that are up in net terms during the pandemic (+257k) as private sector payroll jobs are still down 16k with self-employed (a mixture of public and private) still down 16k.

Full-time employment did the heavy lifting. Full-time jobs were up 193.6k with part-time down 36.5k.

The unemployment rate fell two-tenths to 6.9% as the gain in jobs slightly outpaced the expansion of the labour force (+138.9k).

All of the gain was in payroll positions that were up 176k while self-employed jobs fell by 19k. The gain in payroll positions was more driven by the private sector (+98k) than a gain in the public sector that was up 78k.

The election contributed to the 37k rise in public administration jobs as election enumerators and poll clerks temporarily added jobs. StatCan notes that this category was up 13k in September as advance voting opened into the LFS reference week that includes the 15th day of each month. Even excluding this transitory driver would have still yielded an above consensus pace of job gains.

As the kids went back to school, so did the mothers. Most of the job gain was across adults aged 25+ (+139k) and particularly women (+83k) with men up 56k. Youth employment was up 18k.

STRONG SIGNAL FOR GDP GROWTH

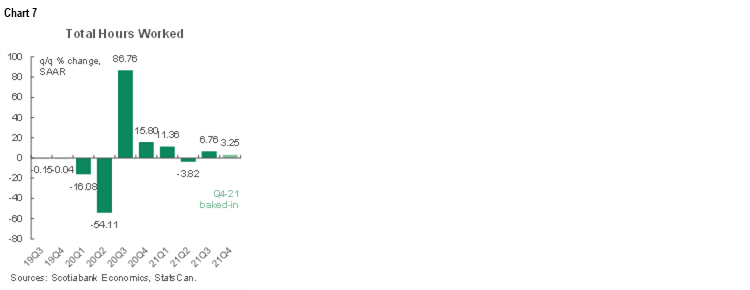

Canadian hours worked were up 6.8% q/q SAAR in Q3 after the 3.8% drop in Q2 (chart 7). 3.2% growth in hours worked is 'baked in' for Q4 given the way the math evolved, meaning even without any further gain in Q4 we'd have a strong lift.

That's important because recall that GDP is an identity expressed as hours times labour productivity. Ergo, H2 is looking like a strong rebound for the overall economy. Put another way, the drop in Q2 was the aberration along the trend of powerful gains.

BANK OF CANADA IMPLICATIONS

There is an ongoing difference between what I think the BoC should do versus reading the signals on what I think they will do. Briefly, I still think they are lagging the cycle and behind on just about every front. Credit goes to them for being the first notable central bank to taper way back a year ago and far ahead of the Fed, but they shouldn’t still be buying any bonds and they should be transitioning toward raising the policy rate now or very soon.

As for what they will do, I think this report cements a transition to the reinvestment phase at the upcoming BoC meeting that culminates in the communications on October 27th. The BoC is likely to boot the C$2B/week rate of gross purchases to the curb on the back of the gain in jobs, overshooting inflation and the speech on reinvestment plans by Governor Macklem on September 9th. That will still have them behaving as active trend buyers in primary and secondary markets not least of which given lumpy and infrequent bond maturities.

But does this jobs report drive the risk of earlier rate hikes? That’s the tricky part for the BoC to manage here. Markets are pushing the BoC to get on with hiking in H1 next year. BAX futures have part of a first hike priced for Q1 and all of it and then some by Q2. OIS markets have a full hike priced by Q2.

Markets might get their way, but the BoC will probably push back at this upcoming meeting by referencing ongoing question marks over the durability of achieving the inflation mandate. We heard Governor Macklem adjust his narrative somewhat yesterday by saying inflation is likely to run a little hotter for a little longer than expected while having backed away from dismissing it as purely base effect driven which was his earlier tendency. I think that’s like arriving a little late to the party. He has not, however, done a full Powell pivot by declaring that the inflation goal has been met and thus lags his US counterpart.

Macklem probably won’t do so at the end of the month either. He’ll likely express the view that there is still net aggregate slack in the economy as measured by output gaps and that there is still some net slack in job markets judged by multiple measures. He’ll convey the notion that shifting to the reinvestment phase is guided by different conditions than when to hike that requires a fully shut output gap in order to have traditional Phillips curve style confidence in the durability of achieving the inflation target.

You could say that the Governor is a bit of a gambling man. The very different performance of inflation to date compared to prior cycles should merit taking out some insurance against inflation risk by hiking ahead of closure of the gap in my view. And remember the big picture here. Extreme stimulus was put into place at the start of the pandemic because of deflation fears, because vaccines were nowhere in sight and because fiscal policymakers were fair weather friends. Standing here today, such conditions for maintaining extreme monetary policy stimulus are gone. The pandemic is not over and we may see further rolling waves especially outside of Canada’s borders, within which vaccination rates are among the highest anywhere. But deflation has been beaten back and with that should be a move toward something less extreme than this level of negative real rates by gently getting off the lower bound and taking it in stride thereafter.

Which concludes with our forecast. If the BoC sticks to script and only hikes once the output gap is shut, then note that this isn’t likely to happen until next summer and possibly later. We still have July pencilled in for a first hike which is less aggressive than markets, but where we remain more aggressive than markets is toward the path thereafter. BAX futures end 2023 about five hikes higher from here versus our seven. Our forecast assumes the BoC hits 2% by the end of 2023 and hence into the bottom end of the BoC’s neutral rate range of 1.75–2.75%. That’s higher than market pricing that far out, but lower than market proxies for where the BoC’s neutral rate may be (chart 8). In all, we may be at risk of being light on starting rate hikes, but are still heavier on the cumulative path for rate hikes that position the Canadian front-end through the belly to be looking rather dear.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.