- No dovish pivot here…

- ...as BoC’s Macklem sounded more hawkish

- Canada’s negative rate spread to the US narrowed and should narrow by more

- Macklem’s CAD guidance is dicey

- The money question was never asked

- Policy mistake or double jeopardy?

- Common component CPI was thrown out the window

Governor Macklem’s important speech (here), audience Q&A and ensuing press conference was more hawkish than markets anticipated. The 2-year yield moved up by 7bps as US and Canadian yield curves sold off on combined Fed- and BoC-speak. The hawkish BoC-speak may even have fed back upon pricing of Federal Reserve policy moves to reinforce today’s Fed-speaker line-up that leaned against pivot talk.

The communications revealed no signs of a more dovish pivot in the making that some had expected. If the BoC hikes 50+ this month and is signalling the plural form of rate hikes still lies ahead then markets are probably correct in pricing a terminal rate over 4% from 3.25% at present and may not be going high enough. The market’s Canada-US rate differential is closing in keeping with previously expressed views but likely has further room to run in that regard. Because of the Governor’s explicit C$ guidance, the BoC now has a target on its back in FX-land and I’m not sure that was a wise thing to do. Absent from it all was the failure to pose the money question to the Governor. Elaborations on each of these points and others follow.

NO PIVOT!

There had been a narrative offered in the market that October’s hike would be one more and done with a coming dovish pivot. That narrative got flushed today.

Key in this regard was the following quote:

“Simply put, there is more to be done. We will need additional information before we consider moving to a more finely balanced decision-by-decision approach.”

With less than three weeks to go before the next decision on October 26th and about a week-and-a-half before communications black-out on the 18th, the Governor is clearly not thinking that the October communications will involve a dovish pivot versus a largely pre-set path to keep hiking thereafter. You'd likely have to signal that data dependence and downshifting in October and he's not doing that here today. A signal that they are ready to do so may involve indicating that future decisions will be ‘more finely balanced’ and hence more sensitive to incoming data versus the not-predetermined-but-predetermined-path the Governor has in his mind.

The fourth last chunky paragraph in the speech (that even makes my stream-of-thought first-and-only-draft paragraphs look small!) offered hawkish guidance by referencing the following:

“…labour markets remain tight, the economy is in excess demand, and we have yet to see clear evidence that underlying inflation has come down. When combined with still elevated near-term inflation expectations, the clear implication is that further interest rate increases are warranted.”

Note the plural form. Had the Governor wished to prime markets for a dovish pivot after one more rate hike then he obviously would have chosen different language. In fact, read the whole speech and while there are balanced sections, the broad tone is clearly incrementally hawkish.

CANADIAN RATES GAP IS NARROWING

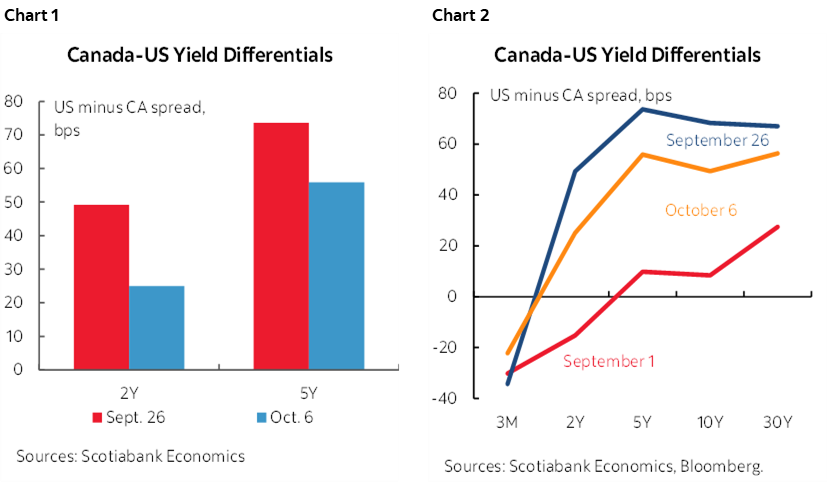

What it leaves us with is a significant narrowing of the Fed-BoC spread in markets which is consistent with what I've been writing about how the BoC was being underpriced relative to the Federal Reserve along with the broader rates curve. See the section titled ‘Does the Bond Market have Canada Right?’ back in the September 23rd issue of the Global Week Ahead (here) and in earlier notes. The 2-year widest point was about 50bps back at about Sept 26th. Now we've cut that in half. The 5s differential was 76bps back on that same peak day and is now 54bps. Both are shown in chart 1. Chart 2 shows that we still have some way to go back to what I think was the more sensible period when the rates curves were more closely aligned. Negative spreads should narrow further in my view as I’m unconvinced that the BoC should undershoot the Fed’s policy rate.

Here are a few points that I’ve been making on calls/presentations with clients to this effect.

1. There is higher inflation *risk* in Canada than the US. Canada has a tighter labour market with faster wage gains and poorer productivity performance, both of which combine to mean higher wage-price spiral concerns in Canada even before adding in public sector wage demands. Canada continued to push into excess aggregate demand through the summer, the US did not, as Canada's economy ripped through H2 and Q3 has strong support from services and trade. CAD weakness is an added driver in Canada that they can't ignore.

2. The fundamentals picture is more insulated in Canada than the US. The list includes the terms of trade, ongoing fiscal expansion, importing a city of Ottawa or Edmonton roughly every couple of years through immigration increases which requires expansion of the housing stock for a split resale/build housing market, B20 which means less of the rate shock flows through to originations in Canada than in the US, more pent-up demand in Canada for services etc etc.

EXPLICITLY HINGING RATE MOVES ON CAD

The Governor provided his most explicit guidance to date that he is tailoring adjustments to the policy rate conditional upon movements in the Canadian dollar. SDG Rogers had done something similar a while back. I’m not sure how smart that is because FX markets have the BoC’s number now. Regardless, when asked during the press conference whether further depreciation of CAD will influence rate policy decisions in the near-term, Macklem said:

“I won't predict the C$. Normally when we raise interest rates the Canadian dollar appreciates. That does some of our work for us. We're not getting that this time. What that means is that other things equal there is going to be more to do on interest rates. We are going to take those exchange rate movements into account going forward in terms of what we need to do on interest rates.”

The natural next question is whether the BoC has estimates of the rate equivalence to CAD movements which we haven’t heard since the somewhat ill-fated experiment with the Monetary Conditions Index years ago.

This backed up a less direct reference to the C$ in his speech:

"These signs of improving global supply chains are encouraging, but we can’t count on easing pressure on global prices to lower inflation in Canada. At a minimum, improving global factors will take time to filter through to Canadian inflation. And the recent depreciation of the Canadian dollar in the face of US-dollar strength will offset some of this global improvement by making US goods and vacations more expensive for Canadians."

In fact, now what we’re left to ponder is whether the fact that the post-communications sell off in 2s but cheapening in CAD (driven by the resumption of broad-dollar strength today) means that Macklem will think he has to hit harder the next time if this reaction persists. Pile on! We have to be open to either 50bps or 75bps on October 26th.

POLICY MISTAKE REDUX? NOPE

Those who would like to see a nearer term rate pause may be tempted to see avoidance of such guidance as a policy mistake. I don’t.

My view is that the policy mistake occurred when central banks slept walk through obvious signs of building inflationary pressures. What they are doing now is only a policy mistake if you really don’t think central banks are willing to court a recession if necessary as the cost to prior inaction against inflation. The whole narrative that hiking rapidly is a mistake is based upon the assumption they don’t want recessions. I think that’s an incorrect assumption and therefore hesitate to reference what is being done as a mistake. In fact, having let inflation out of control to date requires hitting back hard.

On courting recession risk, however, one should never expect the BoC to come out with Andrew Bailey-style British frankness in forecasting one. Nor the Fed. They’re both too politicized to do so in my opinion.

When Macklem was asked about all of this in the context of whether he believes that a path to a soft landing has narrowed since the last statement, he answered by saying he’ll have new forecasts available at the October 26th decision along with a discussion of risks. Macklem noted that the best chance of getting to a soft landing is to front-load those interest rate increases because “we will start to get demand moving into better balance reasonably soon which should help to keep inflation expectations well anchored.” Front-loading, in my view, would have been hiking last year, not long after the cat was let out the bag on inflation. Therefore, back-loading rate hikes now courts more intense risk of recession.

THE JOURNOS WHIFFED ON THE MONEY QUESTION!

I'm disappointed that none of the journos asked about the neutral rate and what he thinks of that and hence how restrictive he thinks they are now. That was the money question today and they whiffed.

In the September statement, the BoC said “we will be assessing how much higher interest rates need to go to return inflation to target.” Theoretically that’s ambiguous in that it could signal they were moving toward a pause—which they obviously did not deliver upon with today’s guidance—or they are reassessing what constitutes a restrictive policy setting which requires re-evaluating the neutral rate range.

The BoC’s estimate of the neutral rate range over time was last updated in April and set at 2–3% after previously flirting with raising it. Does that still hold with all the new information that has been learned since? Nobody asked! So what if they might wait until April to do it again as it’s a relevant question now. Or, does a current assessment of a time-varying neutral policy rate differ from this range? Again, nobody asked!

Therefore, we’re still left wondering whether the BoC truly believes that the present 3¼% overnight rate constitutes a restrictive stance or not. If so, then by how much. If not, then by how much?>

SO LONG, COMMON COMPONENT CPI

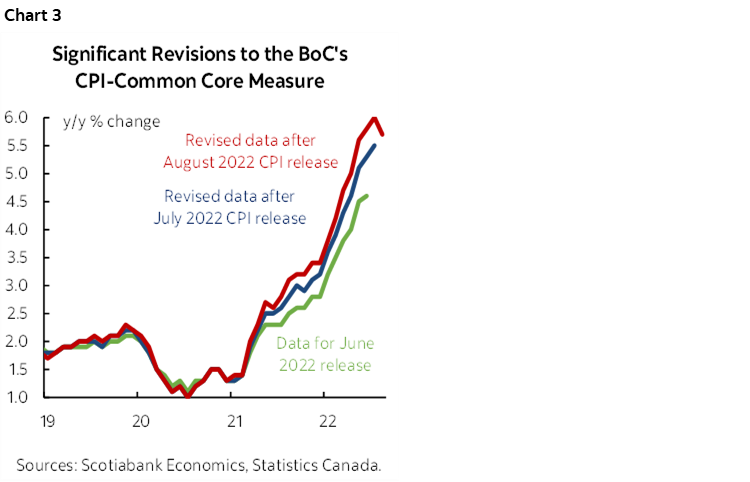

The speech indicated that the BoC is basically booting common component CPI which is a big shift for the BoC to adopt. Since the early days after introducing trimmed mean, weighted median and common component, a lot of folks in the markets were of the belief that common component CPI was the BoC’s preferred core measure despite arguments against such beliefs. It turned out to be of little use with all of the revisions and methodological issues that have surfaced (chart 3).

Here is the relevant passage:

“Of our three measures, CPI-common is becoming more difficult to use in real time because it has been subject to large historical revisions. With price movements becoming much more generalized in the last year, what is included in the common component has changed considerably.2 CPI-trim and CPI-median, in contrast, are more robust to changes in the behaviour of prices. These measures appear to have performed well and have been subject to much smaller revisions. With this in mind, we are more focused on these two measures and we are reassessing CPI-common.”

Going forward, market participants should probably average the two remaining measures (trimmed mean CPI and weighted median CPI) to get a better feel for how the BoC is looking at core inflation.

A HINT AT THE Q3 SURVEYS?

Governor Macklem’s speech said "Survey results also indicate that consumers and businesses are more uncertain about future inflation and more of them expect inflation to be higher for longer. "

What isn’t clear is whether he was referring to already known outcomes of the Q2 consumer and business surveys that the BoC conducts, or whether it’s a loose reference to a sneak peak at the Q3 results. The survey period for the Q3 surveys that land two Mondays from now was over the back half of August and so it’s reasonable to think that the Governor has some sense of what they are showing. I can’t say he was front-running the surveys with this comment without concrete proof, but the issue could have been avoided had he been more explicit by referencing the Q2 surveys.

THE FISCAL TANGO

When asked about whether he thinks governments are fighting his efforts to cool inflation now, Macklem naturally ducked the question and retreated behind IMF guidance. He said he leaves fiscal policy to governments but that the IMF's advice to everyone around the world is that fiscal efforts should be targeted and temporary.

Now, what if fiscal measures are sort of targeted and sort of temporary, but delivered in serial fashion by all levels of government who repeatedly throw more stimulus at the economy in serial fashion? That reality leaves federal-provincial fiscal policy fighting monetary policy.

NO MINUTES

The Governor confirmed that when the BoC beings publishing a summary of deliberations in January that we shouldn’t expect much from it. It sounds like it will just be a token form of enhanced transparency. Macklem basically said it will be an enhanced elaboration upon his opening remarks that are delivered at the start of press conferences as opposed to minutes per se. He also noted that the BoC's consensus-based system is a strength of their system and it encourages colleagues to look for points in common and points of tension. I don’t see it that way as the price paid concerns the fact that the markets and the public never get to peer inside the star chamber to evaluate differences of opinion across Governing Council like they can with many other top global central banks that unleash their officials to speak much more candidly. The IMF’s transparency review should have pushed the BoC for further steps including formal meeting minutes.

DOUBLE JEOPARDY

An interesting question was whether Macklem agreed he should be blamed if tighter monetary policy causes a recession. Naturally he said he’s following his 2% inflation target and price stability mandate. In my opinion, had multiple central banks done what Carney did at the BoC circa 2010 by gently getting off the lower bound with modest rate hikes spread out much earlier when it was apparent that market functioning had been restored and the economy was rebounding with building signs of inflation risk then fewer and more modest hikes might have been more spread out with less damage. The defence against driving recession risk after missing the inflation signals may well prove to be the central banker’s version of double jeopardy.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.