- FOMC cut by 25bps as expected

- The Federal Reserve will end QT on December 1st

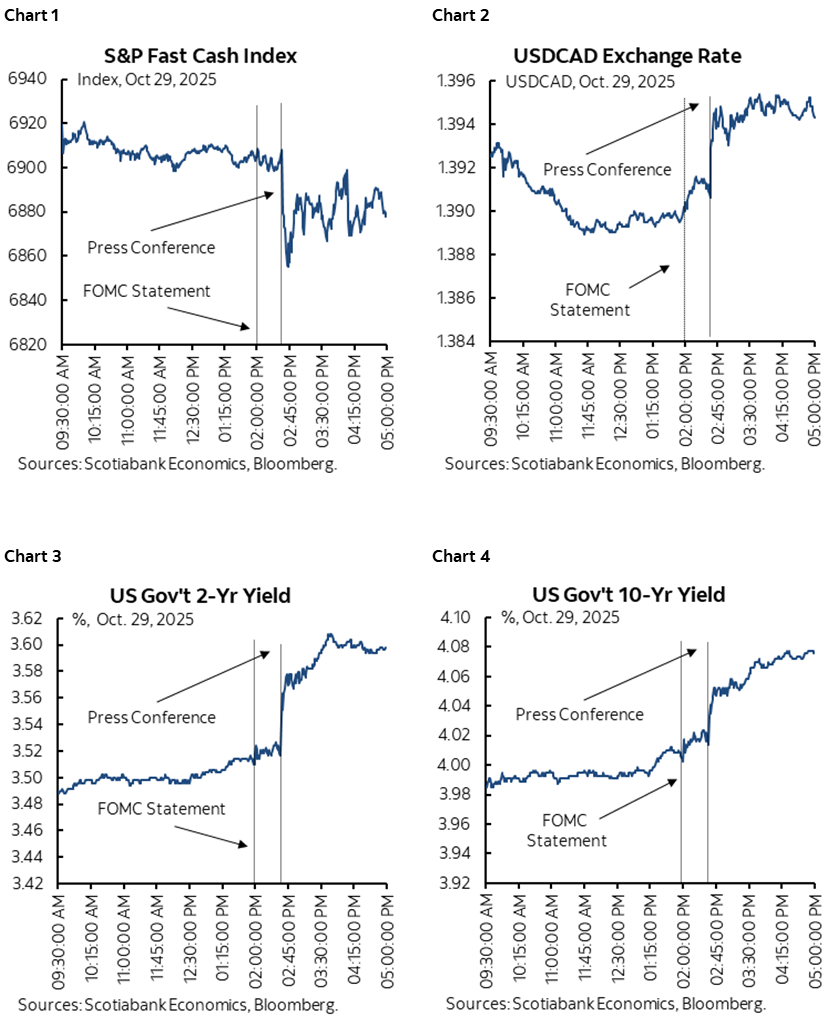

- But the press conference rocked markets…

- ...with language that inserted optionality around the next move…

- ...using some solid arguments, and some weaker ones

- Powell may be too myopic toward broader supply chain pressures on inflation…

- ...and should perhaps remember the opposite experience from a quarter century ago

The FOMC cut its fed funds target rate range by 25bps as widely expected. The new range is 3.75–4%. The end of the policy of Quantitative Tightening was announced and is to be implemented on December 1st. So far so good in terms of expectations.

And none of that mattered. It was Chair Powell’s press conference that rocked markets before handing over to mixed US tech earnings in the aftermarket (charts 1–4). In essence, what Powell and the FOMC did today was to deliberately open up optionality around the next policy decision on December 10th. The Committee was clearly uncomfortable with the fact fed funds futures were pushing them toward another cut at that meeting with the Fed assumed to be on autopilot. That’s not the same as saying they won’t cut, but they’re signalling they want markets to cool their jets for now.

I can’t fault them for doing this. Some of the reasons that were given were solid, while some less so.

In fairness to what they were trying to do, it starts by recognizing that the December decision is about six weeks away. A great deal could happen in that time, not least of which including (hopefully) the probable end of the government shutdown, a wave of catch-up data releases, and I’m sure more volatility on other policy fronts. It’s easier to inject a bit more optionality around that meeting now and then assess, than to have to shock markets later if the need arises.

The result was that pricing for the December meeting backed up by about 7bps from something that was almost fully priced to now having about 16bps of a cut baked in. The Treasury yield curve jumped with the 2s yield rising by about 9bps compared to just before the statement and the 10s yield moving up by about 6bps.

The S&P initially fell by about ¾%, then clawed most of its way back, before slipping in the aftermarket as earnings from Alphabet, Meta Platforms and Microsoft hit.

THE END OF QT

The Committee announced the end of reductions of its SOMA portfolio effective December 1st. This was widely expected at this meeting. The Fed is following the Bank of Canada’s cessation of Quantitative Tightening that was announced back in January but is burdened by broader shoulders in global markets and different drivers of funding market pressures.

The NY Fed offered details here. Guidance points to rolling over at auction principal payments from Treasury security holdings and reinvestment of principal payments from holdings of agencies into T-bills through the secondary market.

Further details are offered in the statement and FAQs.

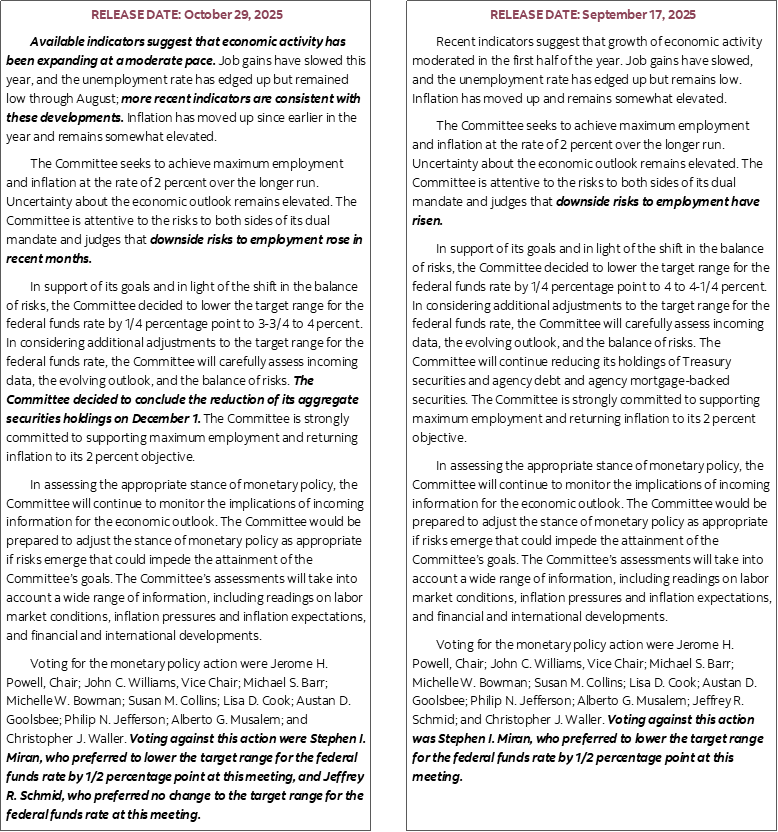

STATEMENT CHANGES

These were very minor. Please see the accompanying statement comparison.

Despite Chair Powell’s remark that “there was a strong, solid vote for this cut” we’re back at having two dissenting voters again after two in July and one in September. This time, KC Fed’s Schmid voted for no change, while Governor Miran—on loan from the Trump administration—once again voted for a 50bps cut. Since 1936, there have been 28 out of 854 meetings when dissenters went in different directions but only three times after 1990. In other words, it’s not an unprecedented situation, but it is rather improbable.

The current conditions paragraph largely just tentatively updated references with the caveat that they are relying upon limited data in light of the government shutdown. Guidance that ‘more recent indicators are consistent with these developments’ in relation to the unemployment rate shows a preference toward continuing to view the labour market as soft even without key reports like nonfarm payrolls. That could be construed as extending the easing bias if the conditions that were foreseen in the September Summary of Economic Projections are still thought to be holding in support of the median Committee participants expectation for another 25bps cut coming next month.

PRESS CONFERENCE—SOME REASONS FOR INJECTING CAUTION WERE STRONGER THAN OTHERS

Here’s where the action was. With some forgiveness for the logic to seeking more policy optionality around December, some of the arguments that Chair Powell gave seemed like an awkward dance.

Powell noted in the press conference that there were strongly differing views on the Committee about how to proceed in December, and that a cut in December is not a foregone conclusion. Indeed, he said “far from it” several times while noting policy is not on a pre-set course. Amid such divisions on the Committee, the Chair conveyed the need for higher caution around the Fed’s next possible step.

One argument that I think resonates is that Powell noted the Committee has now cut by a cumulative 150bps and they are now in the 3–4% range of neutral rate estimates with some higher. He noted that for some on the Committee, it's maybe time to take a step back and really see if there are downside risks to employment and that they have cut 50bps and for some it favours a pause while not for others.

Powell also noted that the government shutdown may or may not be impairing their understanding of what’s happening to the dual mandate and the overall economy. He downplayed this at times but pointing to alternative data sets, but then bluntly stated “If you're driving in the fog you slow down. It's possible that it would make us more cautious but I'm not saying it will.”

Further, Powell emphasized that the US economy continues to outperform expectations with Q3 tracking above earlier GDP expectations with the inference being that the economy might not require a lot of juice from the Fed. The caution here is that GDP is a guide to dual mandate variables, but not an infallible one by any means. Further, what happened to the business of forecasting?

Powell also explained that “We have a situation where the risks are to the upside on inflation and to the downside on employment. Some have different forecasts and different levels of risk aversion. Some will be more averse to inflation overruns and some more to employment undershoots. There were very disparate views in the September SEP. That's what leads me to say we haven't made a decision about December and it's not to be treated as a foregone conclusion and in fact far from it.”

Sensitivity to data unknowns was also signalled in his response to a question on whether improved labour market readings would cause them to reassess and he acknowledged that would have to be “taken into account.”

Some of Powell’s other arguments were less convincing.

For example, Powell was saying that the shutdown isn't crippling their ability to tell what’s going on because they are seeking some comfort in private data through indicators that often bear no resemblance to payrolls. Yet he acknowledges the need to see the official data. A reasonable listener to the press conference would conclude that Powell can’t openly say they are fumbling in the dark, but that they still would like to see some official data before deciding on their next step.

For another, Powell kept repeating that downside risks to employment have risen yet he cited imperfect recent data. Powell noted that they can point to alternate readings of the labour market like initial jobless claims that are not flashing any real warning signs. He said if the labour market was really in trouble, then they should be seeing this in what they have. He should be more cautious in my opinion.

For one thing, his reliance upon initial claims belies the fact it is a poor guide to nonfarm payrolls. Just look at the numbers; initial claims have been floating around 210–250k for much of this year and hence quite low and reasonably stable, yet they did not predict the steep slow down in nonfarm payrolls over recent months and the large downward revisions up to March. Further, if you’re undocumented and are either arrested or hiding, then you're quite unlikely to be qualified for jobless benefits and extra unlikely to make the trek to your local government office to file. Further, you need a job to lose before filing which young entrants wouldn't necessarily have, so claims can be a misleading sign of weakness. Stable initial claims are totally out of sync with other readings like ytd layoffs that are among the highest on record, or ytd hiring that is among the lowest on record. And claims won't reveal if you've lost a higher paying job and been forced to take a more menial one. Further, there can be lags between when layoff packages expire and when folks file claims. I’ll put it this way: when forecasting payrolls, I barely even look at weekly claims not least of which because nonfarm is its own beast with plenty of idiosyncratic quirks.

Powell cited stable long-term measures of inflation expectations as offering cause for neither being concerned about upside or downside risk to longer-term inflation. Yet the measures they use are weak in my view. Market measures thoroughly misjudged inflation coming out of the GFC by overestimating it, then seriously underestimated it through the pandemic period. Consumers form adaptive inflation expectations based upon extrapolating prices for a narrow subset of the basket and don’t understand things like hedonic adjustments.

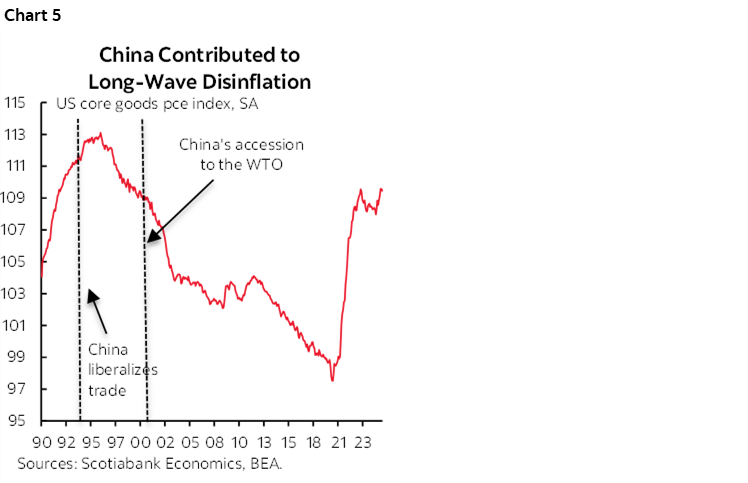

Powell also repeated that his base case is to look through the effects of tariffs on inflation as transitory with the risk it may not be. As I’ve argued, he's biasing the supply chain challenges toward only tariffs which remains incomplete. Further, there are long-wave forces to supply chain challenges, costs, and how prices evolve that cannot be judged in a handful of months or even a year or two.

As an opposite example to today’s circumstances, if Powell were commenting on the disinflationary impact of China's shift to manufactured exports in the 1990s and accession to the WTO in 2001, he would have said there would only be transitory effects in a few inflation reports and nothing further had he applied the same logic he’s using today. Tariff cuts only impact things temporarily, he may have argued. And he would have missed the long wave of disinflationary pressures such as shown in chart 5. It’s very myopic and narrow to focus on just tariffs, rather than a wholesale rewriting of border frictions with multiple drivers that can take many years to work their way through. It’s possible that just-in-time inventory management is dead, legacy assets in higher risk markets will be abandoned, supply chains need to be recreated elsewhere, and often in higher cost western markets. Further, tariff changes can have wide ranging effects on important considerations like investment, productivity, and cost controls and hence carry influences beyond their mere short-term direct effects.

PRESS CONFERENCE TRANSCRIPT

What follows is an attempt at providing a selective transcript of the press conference’s key questions with any errors or omissions to be blamed on my typing fingers!

Q1. Are you uncomfortable with market pricing has assumed a rate cut at the December meeting is a foregone conclusion?

A1. Yes I just said that.

Q2. At what point do you conclude that you've taken out enough insurance? Are you looking for an improvement in the outlook or are you making a series of adjustments and then pausing?

A2. Speaking generally about risk management approach to the past two decisions but going forward is a different thing.

Q3. What arguments were brought up about December? Discussions about AI? Stock prices?

A3. That's a factor in everyone's assessments in the economy but I wouldn't say it was a driving factor. We have a situation where the risks are to the upside on inflation and to the downside on employment. Some have different forecasts and different levels of risk aversion. Some will be more averse to inflation overruns and some more to employment undershoots. There were very disparate views in the September SEP. That's what leads me to say we haven't made a decision about December and it's not to be treated as a foregone conclusion and in fact far from it.

Q4. General Q on ending QT

A4. General answer reinforcing Dec 1st decision

Q5. If labour markets stabilize how would this affect your view on the need for further rate reductions from here?

A5. In principle if the labour market was seen to be stabilizing or growing then that would be taken into account. We have other readings. We're not seeing an uptick in claims or downtick in openings suggests we're seeing gradual cooling but nothing more than that.

Q6. How does the shutdown hinder your ability to make the right decisions and how much is that factoring into your decision for December?

A6. We'll get some data. We'll have a picture. We'll also have the Beige Book. We will not have a detailed feel but I think we'd pick it up through these if there was a material change. December is still six weeks away but we'll have to see how it unfolds.

Q7. Was this a close call this cut? Or maybe the other way?

A7. There was a strong solid vote for this cut. The differing views were more about the future path. Forecasters have raised their forecasts for this year, next year and perhaps beyond and in some cases quite materially.

Powell's comments on the evolution of the future balance sheet largely compatible with how most would have been seeing it in broad terms

Q8. What do you think about the drivers of core inflation? Are you more concerned about the risk of making mistakes on inflation or employment?

A8. We didn't get PCE but we can still make a pretty good assessment based on CPI and then we will maybe adjust when we get PPI. Goods prices are moving inflation up. Housing services inflation has been coming down and is expected to continue coming down. That leaves the biggest category of core services ex-housing and a significant part of that is non-market services and we don't take a signal from the economy on that. So, inflation excluding tariffs is not far from our goal of 2%. Core PCE not including tariffs might be 2.4–2.5% or so which is not far from the goal. The thing about tariffs is that it will come and increase further but as a one-time effect. We've been thinking very carefully about the pathways for persistence and we don't see it through the labour market or through inflation expectations. So it's a risk to be monitored but not a base case.

Q9. Comment on stubborn services inflation?

A9. It's the non-market part of non-housing services. It reflects financial services imputed but not paid, and generally non-market services. We expect it to come down. We're absolutely committed to returning inflation to 2% and there should be no question that's where we're going.

Q10. There is a big investment boom in AI infrastructure. How is the Fed thinking about this in terms of market bubbles?

A10. It's a big deal. I don't think that the spending to build data centres is interest-sensitive. I don't know how those investments will work out but they're not interest sensitive.

Companies making today's investments actually have earnings whereas the ones back in the dot-com didn't. And it’s not just AI as consumers are spending [ed. the two may be connected through the wealth effect on upper income earners. If one falters, so could the other.]

Q11. What are you looking at to track inflation in the absence of government data?

A11. Price stats. Adobe. ADP data. Many different sources including what we get out of the Beige Book. It doesn't replace government data but it gives us a sense that if something material is happening then it would pick that up.

Q12. Do you worry you're going to have to start making policy by anecdote rather than government data?

A12. If you're driving in the fog you slow down. It's possible that it would make us more cautious but I'm not saying it will.

Q13. Have large layoff announcements by some big firms come into your discussions? Some of the stresses are appearing across some households like household health insurance premiums. Are they factoring into your analysis?

A13. Much of the time the layoff announcements and guidance are talking about what AI is doing. It could have implications for jobs. We're not seeing that in initial claims but it doesn't have to or with a lag. On the k-shaped economy, listening to the earnings calls, many consumer companies are saying there is a bifurcated economy with consumers at the lower end being more cautious than the upper end. We think there's something there.

Q14. If December is not a foregone conclusion and it's not government shutdown-related then why else?

A14. We've moved 150bps and you're in that 3–4% range of neutral rate estimates. There are people on the committee who have higher estimates. For some part of the Committee it's maybe time to take a step back and really see if there are downside risks to employment. We've cut 50bps and for some it favours a pause while not for others.

Q15. Why is the job market weakening right now and what will this rate cut do to improve it?

A15. One is a dramatic reduction in the supply of new workers. Part is a cyclical thing through declining labour force participation. Part is through immigration policy. It is mostly a function of the change in supply. Our tool supports demand.

Q16. Should consumers expect higher inflation because of tariffs this year?

A16. It takes a while for tariffs to work through the production chain. That will continue to happen into the Spring. They are not big overall increases. Then it's just a one-time price increase. Once the last tariff is put on something, prices stop going up and then measured inflation comes back down to non-tariff inflation.

Q17. When will the Board make decisions on regional Fed President appointments and can we expect changes?

A17. We're in the middle of that process and we're going to complete it in a timely way and that's really all I can say.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.