- Inflation and wage expectations continue to become unmoored

- Businesses expect high inflation, but admit no role

The Bank of Canada’s lagging surveys of consumer (here) and business (here) attitudes continue to highlight growing risks of a wage-price spiral effect as few believe in the credibility of the central bank’s 2% inflation target. That unmooring of inflation expectations places the central bank in dangerous territory and continues to signal that it’s job is far from being done. Of course, the usual caution with these surveys concerns their limited usefulness in terms of what actually winds up happening.

STILL HIGH INFLATION EXPECTATIONS

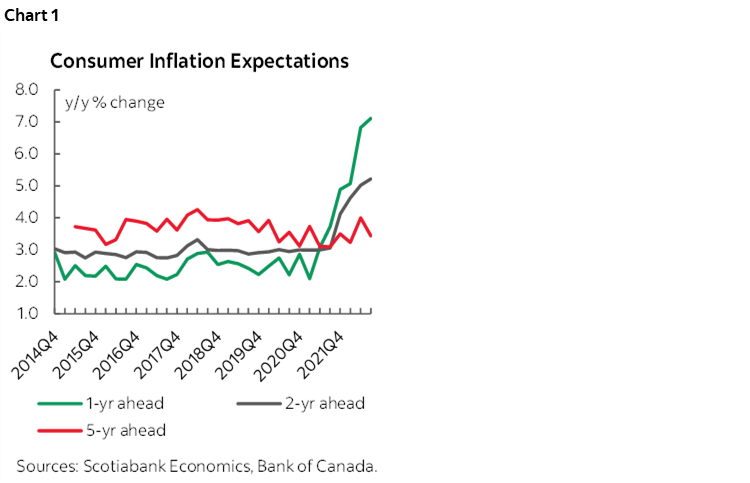

As chart 1 shows, consumers upped their inflation expectations over each of the next one- and two-years ahead to even further dizzying heights. Their five-year inflation expectations edged lower from 4% to 3.44% but this remains well above the BoC’s upper limit of the 1–3% medium-term inflation target range. In all cases, the statistical significance of the moves within what is a consumer attitudes survey is probably pretty low, but notwithstanding this point there is no material evidence that inflation expectations are starting to push back into the target range across all time horizons.

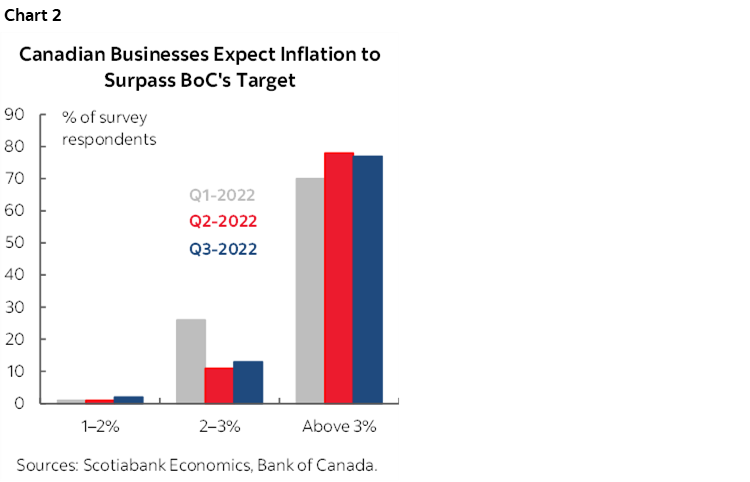

Chart 2 shows that the vast majority of businesses still believe that the BoC won’t achieve its inflation target over the next two years with minor differences that are dismissable given the survey’s statistical noise.

Go to the consumer survey’s link and check out the BoC’s chart 3 that may have had the folks at the BoC spilling their mocha grandes. Those who think Canada even has an inflation target think the target is 2.9% (not 2%) and rising. Those who don't even know that one exists (ha!) think it's 4.9% and rising. Apparently the BoC has some work to do to explain to mainstreet what it’s trying to achieve.

RAISE PRICES? WHO ME??

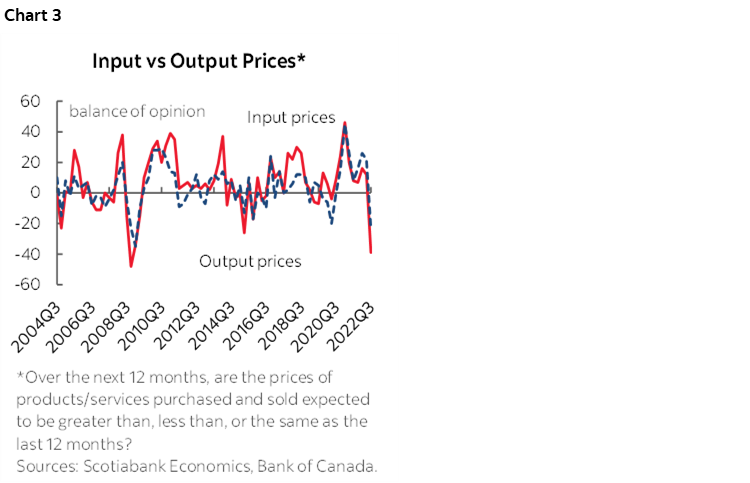

A net 24% of firms are now saying they expect to be pushing through lower output prices over the next year (chart 3) including a gross 47% who say they plan on cutting prices and 23% saying they plan on raising them. Yeah right. That seems rather inconsistent to what they are saying about inflation and the BoC’s inability to hit its target. Don’t pay much attention to that chart since it’s a pretty weak gauge. A year ago, only a net 8% of the little darlings said they were planning on raising prices by now and yet 81% of the CPI basket Is up by more than 2% y/y, 75% is up by more than 3% and 70% by more than 4%. “What, sweet little me raise prices? Nah, must be the evil competition doing that, we’d never raise prices on our customers!” Hogwash.

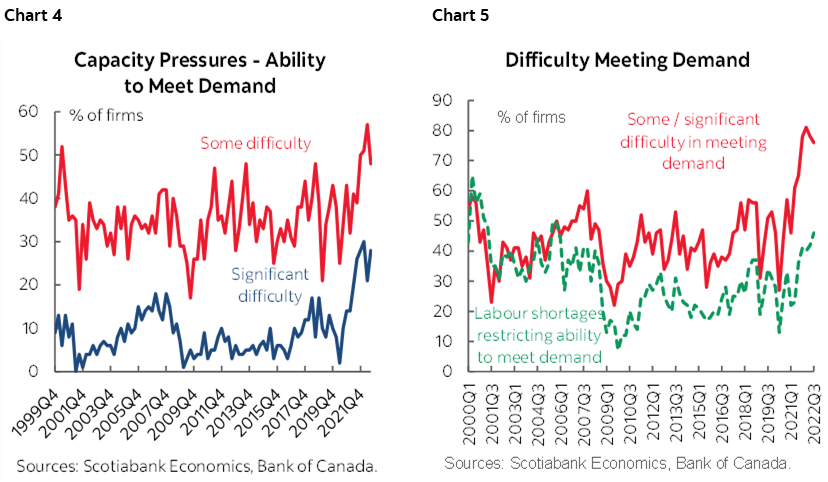

This also seems inconsistent with the share of businesses saying they would have some difficulty meeting unexpected demand that eased a touch but still remains elevated (charts 4, 5).

WAGES

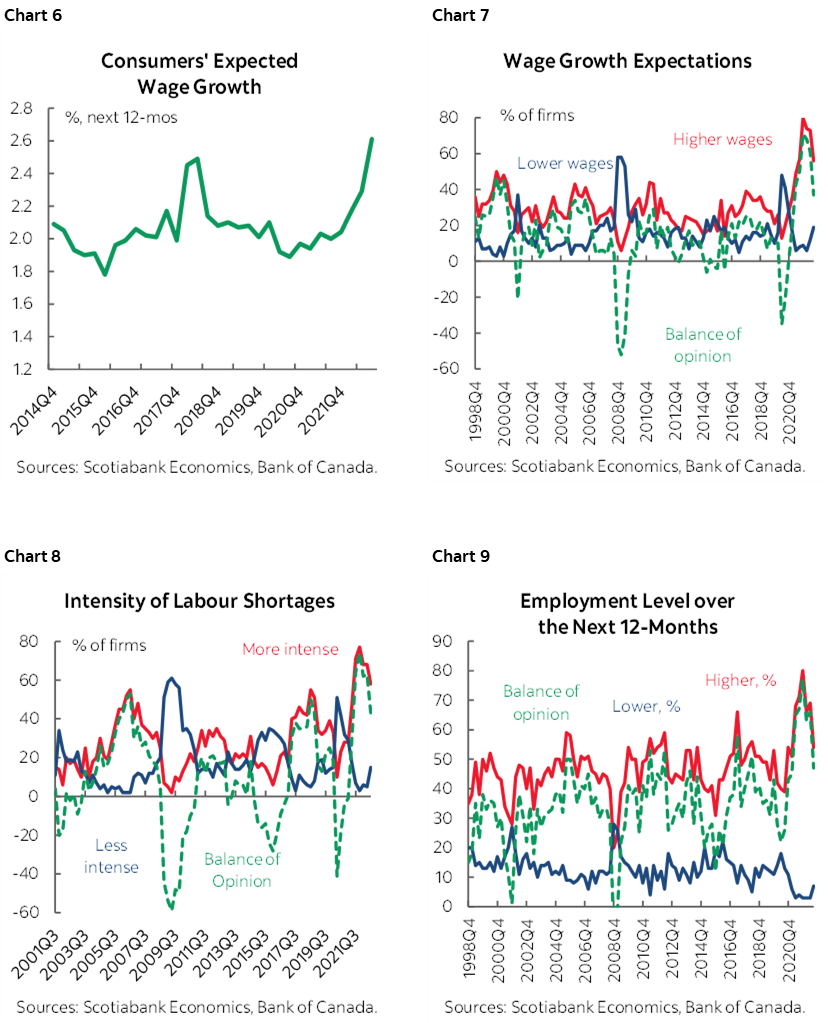

Consumers’ wage expectations over the next year continue to shoot higher (chart 6). This suggests that the wage cycle is reinforcing inflation risks. 40% of workers expect a wage hike of over 4% over the next year.

When businesses are asked about expected wage pressures, there was a decline in the net percentage of firms expecting to pay higher wages but it still remains at elevated levels (chart 7). A somewhat smaller share of businesses—but still a majority—say that labour shortages are more intense (chart 8). Ditto for expected employment levels over the next year (chart 9).

OTHER METRICS

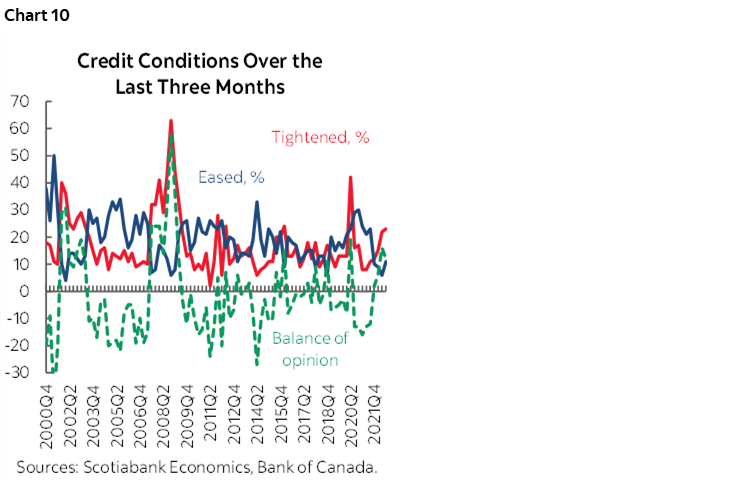

Businesses are indicating tightening credit conditions (chart 10).

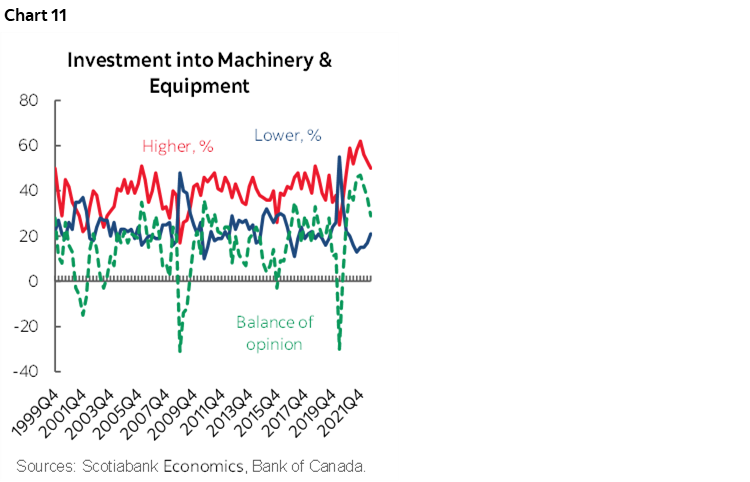

Business plans to invest remained fairly elevated (chart 11), though tightening financing conditions could challenge this expectation.

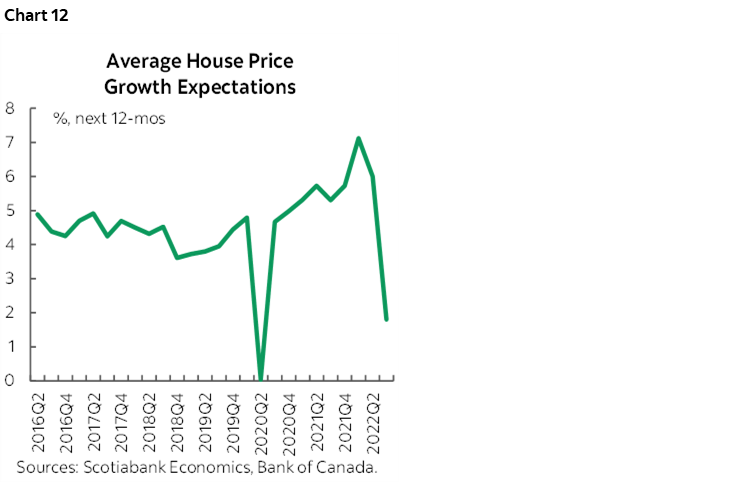

Consumers’ expectations for growth in house prices over the next year fell, but was always underestimated in the past and likely underestimates downside risk going forward (chart 12).

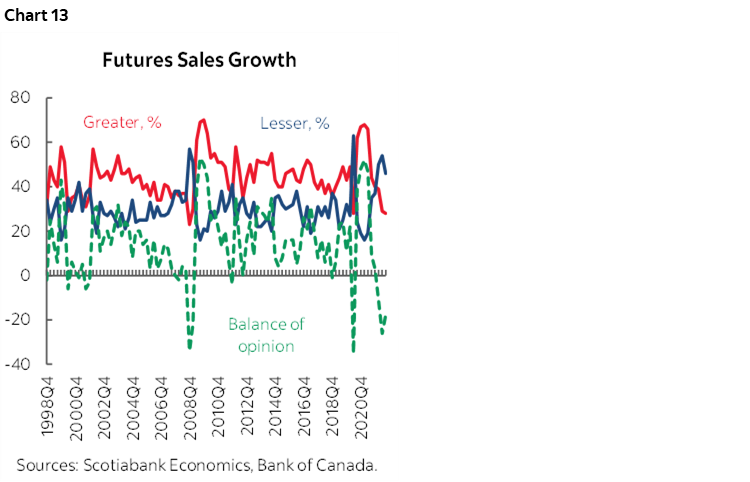

Activity readings point to weakening expected growth (chart 13) that should surprise no one. The BoC will remain overwhelmingly focused upon cooling wage and price pressures and it will take material damage to the economy and job market to achieve such an outcome.

SURVEYS ARE DATED

The surveys are partly stale because they predate much of the turmoil that has recently swept through global financial markets owing in no small part to the UK government’s severe missteps. The consumer survey was conducted between August 2nd and August 23rd (basically two months ago…) and the business survey was conducted from August 15th to September 9th. Frankly it still takes the BoC an absurdly long time to turn around the results, longer than any other sentiment survey I’m aware of including the universe of PMIs and confidence gauges. Perhaps the surveys should be outsourced?

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.