- The simplest measure of core inflation continues to decelerate…

- ….and hit its lowest in nearly a year…

- ...driving cautious optimism that an inflection point may be building

- CDN CPI m/m % NSA // y/y %, October:

- Actual: 0.7 / 6.9

- Scotia: 1.2 / 7.4

- Consensus: 0.8 / 6.9

- Prior: 0.1 / 6.9

- Average ‘Core’ CPI ex-common: 5.1 y/y (5% prior)

Which set of inflation readings one focuses upon can lead to divergent opinions on what they mean to markets and monetary policy, but the one number that I think is the most telling continues to tentatively point to disinflationary pressures at the margin. I’ll come back to that one measure in a moment after highlighting the implications to the BoC.

THE 8TH INNING FOR RATE HIKES

When combined with the fact that Governor Macklem has chosen to downplay wage growth—at least for now—the result may net out to support a further downshifting in the pace of rate hikes at the December meeting and more cautious guidance toward a coming pause. There are still major uncertainties overhanging the inflation picture into 2023 such as the need to open up slack in the economy and labour market compared to little to no real evidence this is happening to date and in order to sustainably drive inflation toward target. There is also the risk that if weakness in 2023 proves to be transitory and minor in nature as the BoC appears to think then it may face the risk of prematurely declaring victory. For now, however, the BoC is likely to be further encouraged by the evidence.

Additional factors inform this perspective in what is probably the 8th inning for near-term policy tightening. The BoC is increasingly pivoting away from rapid tightening into restrictive territory toward a more measured approach to the lagging effects of cumulative changes to date alongside rapidly shrinking its balance sheet. Its reaction function is also more muddled given changes to its new inflation targeting agreement with the Federal government last December that kept the 2% inflation target but mixed in muddled language on maximum sustainable employment. As written in my Global Week Ahead, I think new information in Macklem’s speech last week can be interpreted to mean a willingness to rise in the upper-half of the flexible inflation target range of 1–3% if pushing it lower were to mean weaker employment. Peak concerns about a weakening currency and potential inflationary implications have also eased over the past month via the 5–6 cent appreciation in the C$ in part a function of broad USD movements.

PICK WISELY AMONG MEASURES OF ‘CORE’ INFLATION

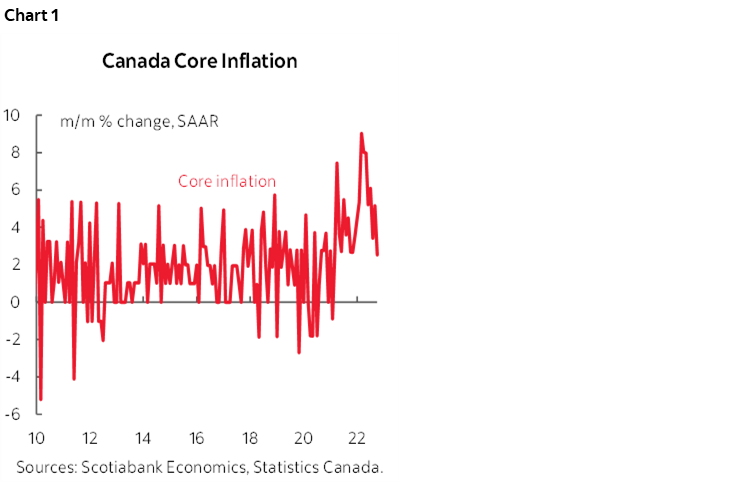

Relative weakness in underlying price pressures is best indicated by traditional core CPI ex-food and energy that was up by only 0.2% m/m SA. That’s the lightest reading since November 2021. The annualized rate of 2.5% m/m SAAR converts to 3.7% on a three-month moving average basis which isn’t exactly a light trend, but continues the deceleration since May. This is the deceleration shown in chart 1. The usual caution applies in that more data is required, but we’re on the right path with greater evidence now than at any other point in quite some time.

That interpretation may be different compared to what are likely inferior measures of core inflation. The average of the two central tendency inflation readings—weighted median and trimmed mean—ticked up to 5.1% y/y from 5.0% which could be interpreted as ongoing pressure upon core inflation (chart 2). This reading has nevertheless been stuck at 5.0–5.2% y/y since May.

The problem with these latter measures is that they turn too slowly as they are different approaches to tracking central tendency price pressures on a monthly compounded basis over the past year. They are not spot year-over-year calculations, but since they drop the earliest month and add in the latest month in a rolling set of calculations that take into account revised estimates along the way over a full year’s worth of data they will never provide the same degree of information at a potential inflection point for inflationary pressures as a purer and simpler m/m ex-food and energy price measure. This is a major shortcoming to the BoC’s roll-out of these over-complicated measures several years ago.

DRIVERS AND DETAILS

Headline inflation landed at 0.7% m/m on a seasonally unadjusted basis and the year-over-year rate held at 6.9%. Seasonally adjusted prices were up 0.6% m/m. On the surface, that looks like a hot set of price pressures.

The rub lies in the lack of breadth. Strip out food and energy and prices were little changed (0.2% m/m SA). Gasoline’s 9.2% m/m NSA (9.5% SA) rise added about 0.4 ppts to m/m price pressures which was in line with my tracking. Food’s 16% weight added a generously round 0.1 ppts to m/m SA prices.

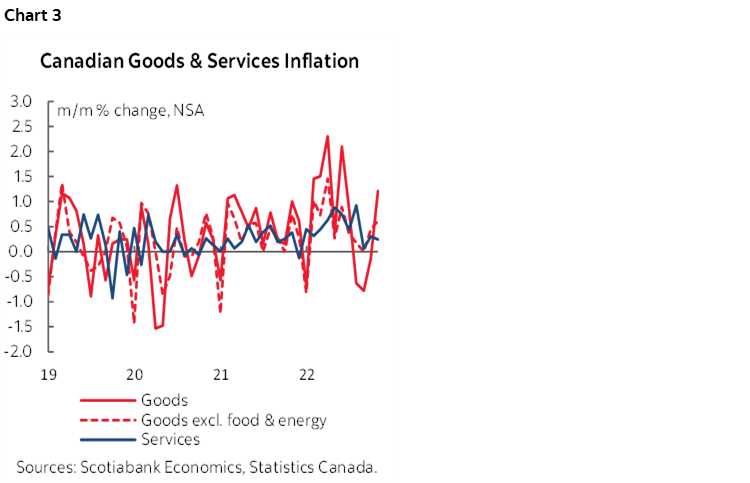

Chart 3 shows services price inflation has noticeably ebbed compared to prior months in m/m NSA terms. Goods price inflation accelerated but goods ex-food and energy has decelerated from earlier peaks.

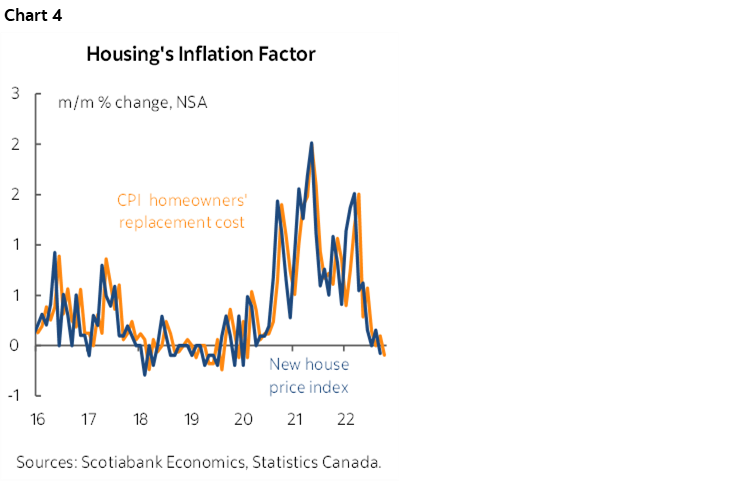

House price inflation is ebbing (chart 4). Canada captures housing very differently compared to the way the US does by using the house only component of the new house price index as the driver to replacement cost within shelter costs. Replacement cost fell –0.1% m/m SA. This involves a much lower weight than how the US captures housing inflation with a different methodology that uses owners’ equivalent rent.

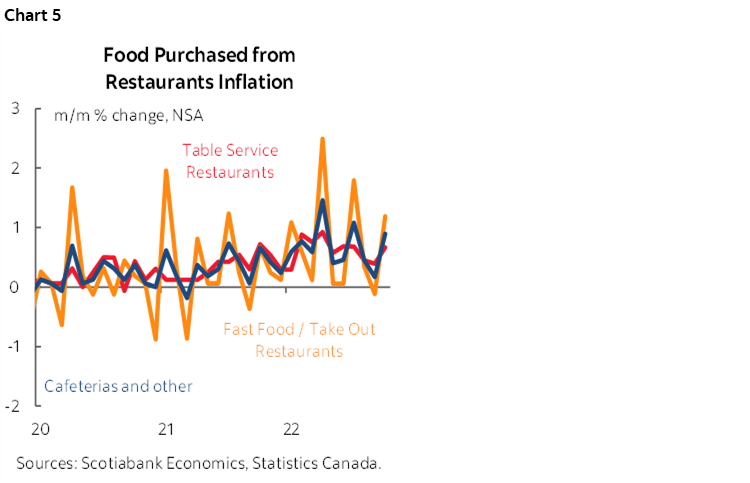

Restaurant price inflation remains elevated (chart 5).

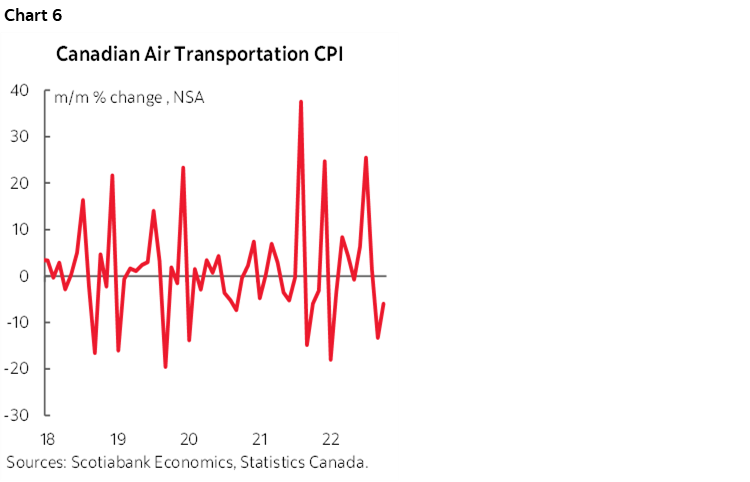

Airfare inflation has sharply ebbed more toward seasonal norms (chart 6).

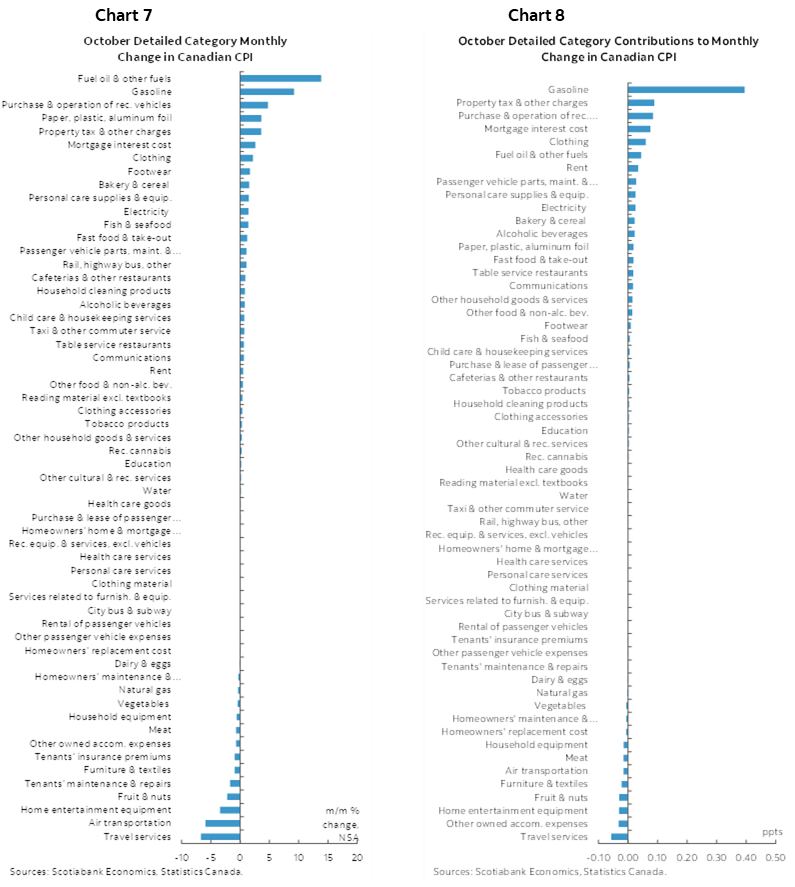

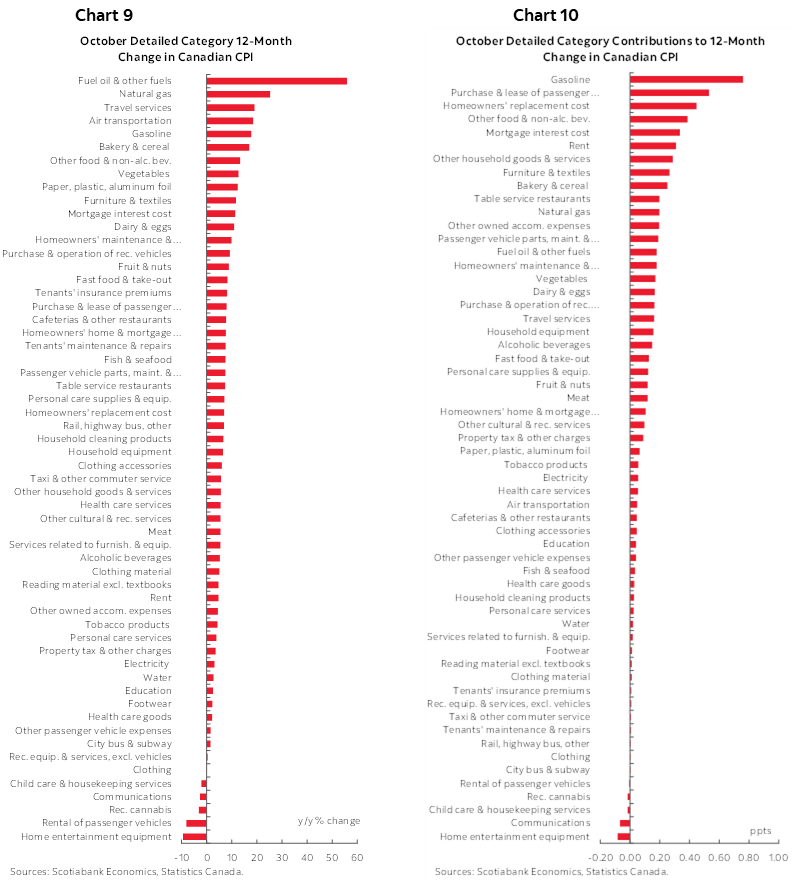

Chart 7 shows the m/m changes in prices in seasonally unadjusted terms across the basket and chart 8 does likewise by weighting the components’ contributions to inflation. Charts 9 and 10 do likewise in y/y terms.

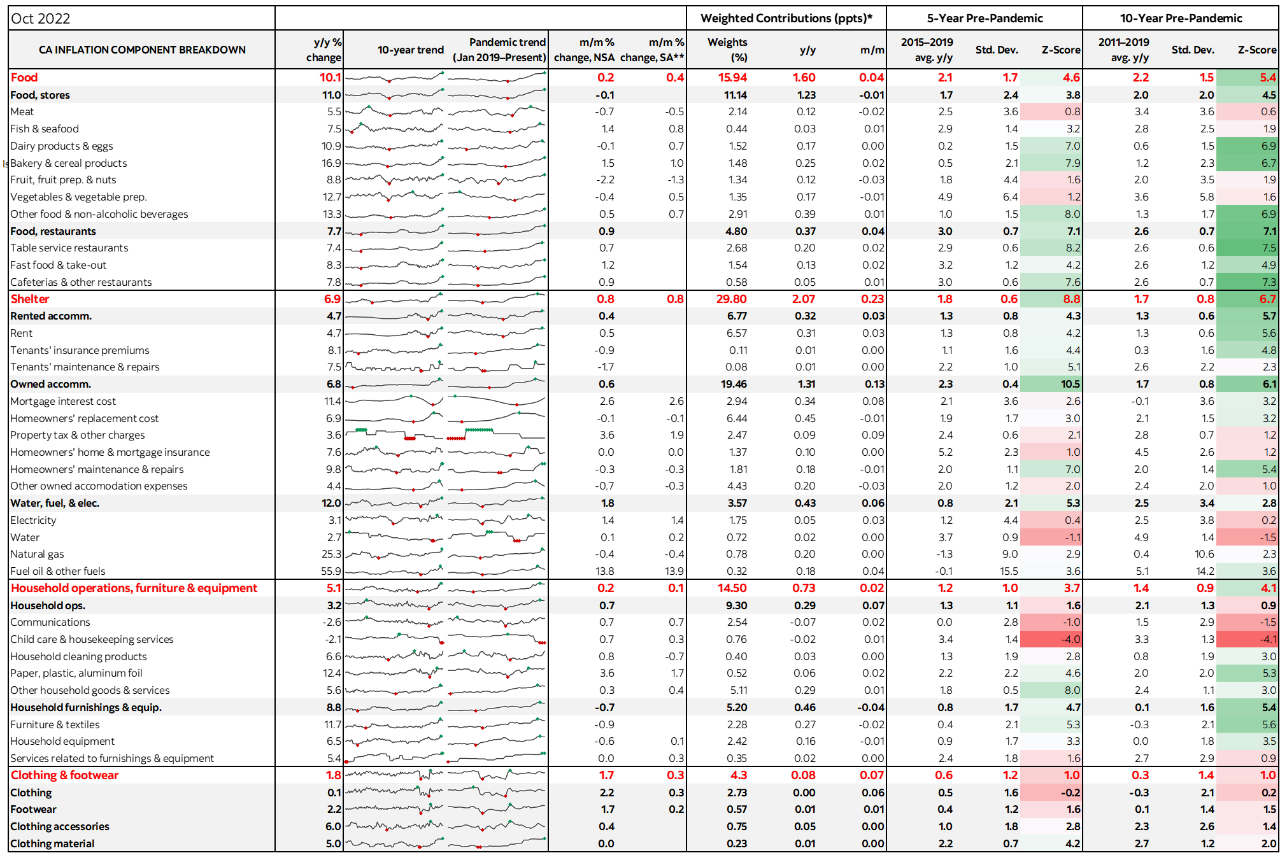

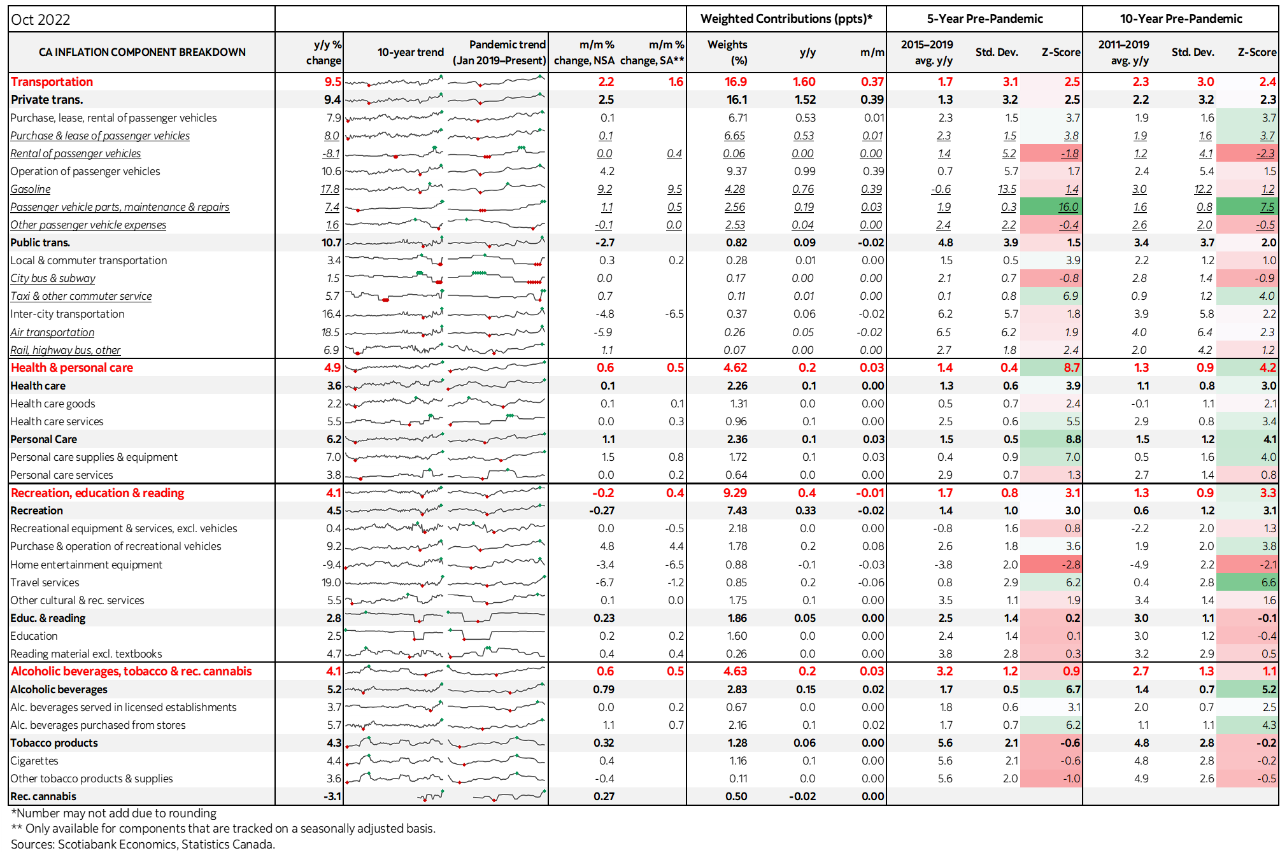

Also please see the accompanying table that provides a more detailed breakdown of the components including micro charts and ‘z-score’ measures of deviations from past multi-year trends.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.