- The US holiday shopping season got off to a strong start…

- ...as October sales posted a rapid gain…

- ...with high breadth…

- ...that bakes in strong Q4 growth

- Caveats include price effects and rotation from high contact spending

- US industrial output also beat expectations

US retail sales m/m % change, headline / ex-autos, October, SA:

Actual: 1.7 / 1.7

Scotia: 1.7 / 0.9

Consensus: 1.4 / 1.0

Prior: 0.8 / 0.7 (revised from 0.7 / 0.8)

The US holiday shopping season got off to a roaring start. Strong growth in retail sales is baked into the fourth quarter ahead of the start of the holiday shopping season including next week’s US Thanksgiving followed by Black Friday and Cyber Monday sales. There are nevertheless two important caveats.

Sales were up 1.7% m/m last month, matching Scotia’s estimate. Sales ex-autos were up by an identical 1.7% m/m despite the fact that a 1.8% m/m rise in autos and parts should have led to a stronger headline gain than in ex-autos. The reason that didn’t happen was probably because the prior month’s minor revisions added a tick to headline sales but subtracted a tick from sales ex-autos.

The retail sales control group is how this report gets factored into broader consumption within GDP accounts and it was also strong at +1.6% m/m.

Q4 sales are tracking a gain of 11% q/q in seasonally adjusted terms at an annualized rate for Q4 over Q3 (chart 1). That’s a very strong start to the holiday shopping season based on the Q3 average and October’s results while assuming flat readings for November and December only in order to focus upon the effects of what we know so far without adding arbitrary forecast bias.

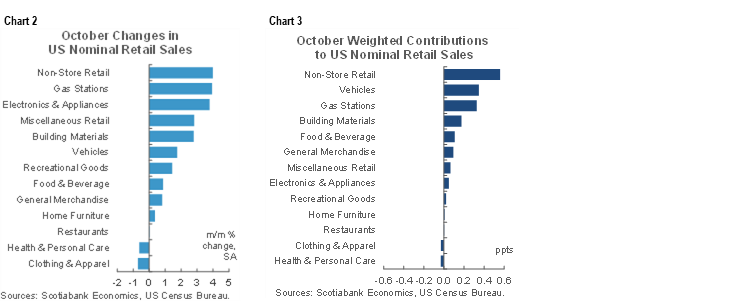

There was high breadth to the gain. Chart 2 shows the changes in the value of sales by category and chart 3 does the same thing in terms of weighted contributions to the overall change in sales by category. The only soft areas were clothing (-0.7% after strong prior) and health/personal care products that were down for a second month.

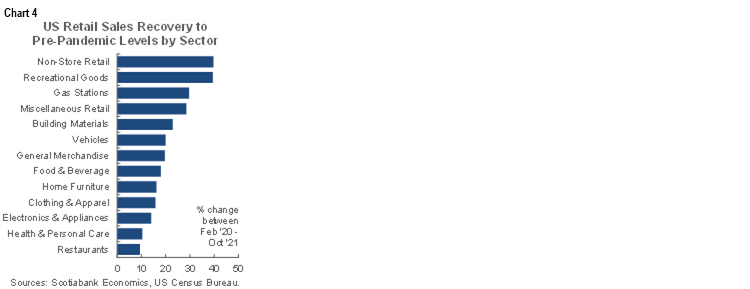

US retail sales are now 21% higher than just before the pandemic. Ditto for sales ex-autos and ex-gas. The retail control group is 23% higher. Chart 4 shows the change in sales by category relative to just before the pandemic.

Now for two caveats. The smaller of the caveats is that this report measures the change in the value of sales, not volumes unlike the convention in other markets like the UK and Germany, or Canada where both nominal and real figures are provided in the same report. Based upon last week’s CPI figures, the retail sales volume gain was likely under 1% m/m which was still solid.

The bigger caution is that we can't tell to what extent spending at retailers rotated away from higher contact services back toward retail. We can see restaurant sales were flat last month (eating/drinking 0% m/m), but most other services are not captured in this report.

US industrial output also beat expectations with a gain of 1.6% m/m (consensus 0.9%). There was a big jump in capacity use at 76.4% (75.2% prior) which puts capacity utilization back above pre-pandemic levels and at the highest since December 2019 but still below earlier peaks (chart 5). Details were ok, but not as good as the headline. Mining output was up 4.1% m/m which was likely significantly due to prices. Utilities were up 1.2%. Manufacturing was up 1.2% m/m and there were solid gains in consumer goods, while business equipment was little changed.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.