- Retail sales point to strong consumption in Q1 GDP

- Real household income after energy spending is usually resilient in energy shocks

- Producer prices continue to point to firmer coming CPI inflation even without energy shock

- Builder prices point to upward revision in CPI

- There should be tighter limits on the BoC’s data dependency this time

The Canadian consumer is charging back in Q1 as producer prices point to upside risk facing CPI inflation. Neither the Canadian consumer nor inflation risk is dead in Canada before or after the oil shock.

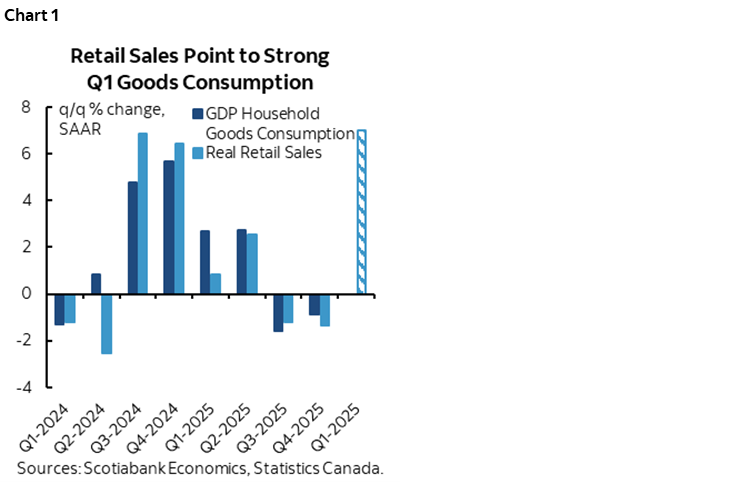

Retail sales volumes are tracking just shy of a 7% q/q jump in Q1 over Q4 at a seasonally adjusted and annualized pace. It could be the strongest quarter since 2024H2.

This matters because of the strong connection between retail sales volumes and consumer spending on goods within GDP accounts (chart 1). Q1 is looking rather explosive. That could be part of the narrative behind stronger final domestic demand than GDP growth once again.

This Q1 tracking of retail volumes is based on what we know from Q4, plus a 1% m/m SA jump in sales volumes during January and a significant part of the preliminary 0.9% m/m SA guidance for February retail sales values showing up as higher volumes. March is assumed flat in the calculations solely to place emphasis upon the known factors thus far. There are bidirectional risks to this preliminary estimate.

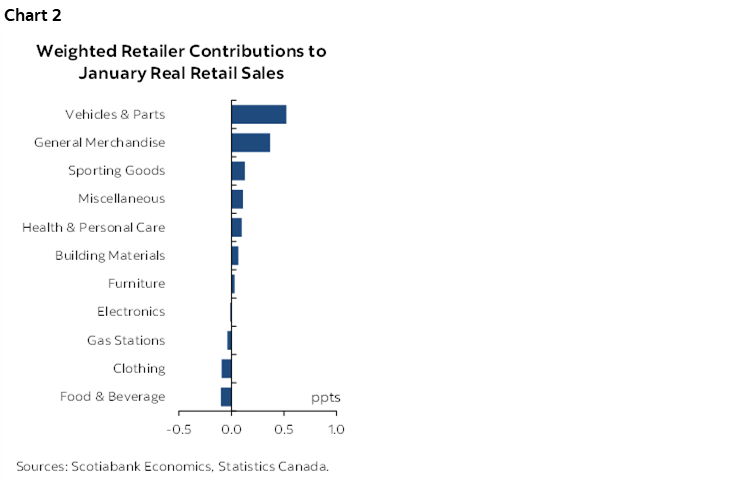

January’s 1% gain in volumes had significant breadth to it (chart 2). Vehicles were the biggest driver of the gain followed closely by general merchandise.

There is never any colour provided by Statcan on its initial guidance for the next month (February in this case) but it’s set against a dip in vehicle sales which might imply a combination of higher prices and strength in sales ex-autos were the drivers of the preliminary 0.9% lift.

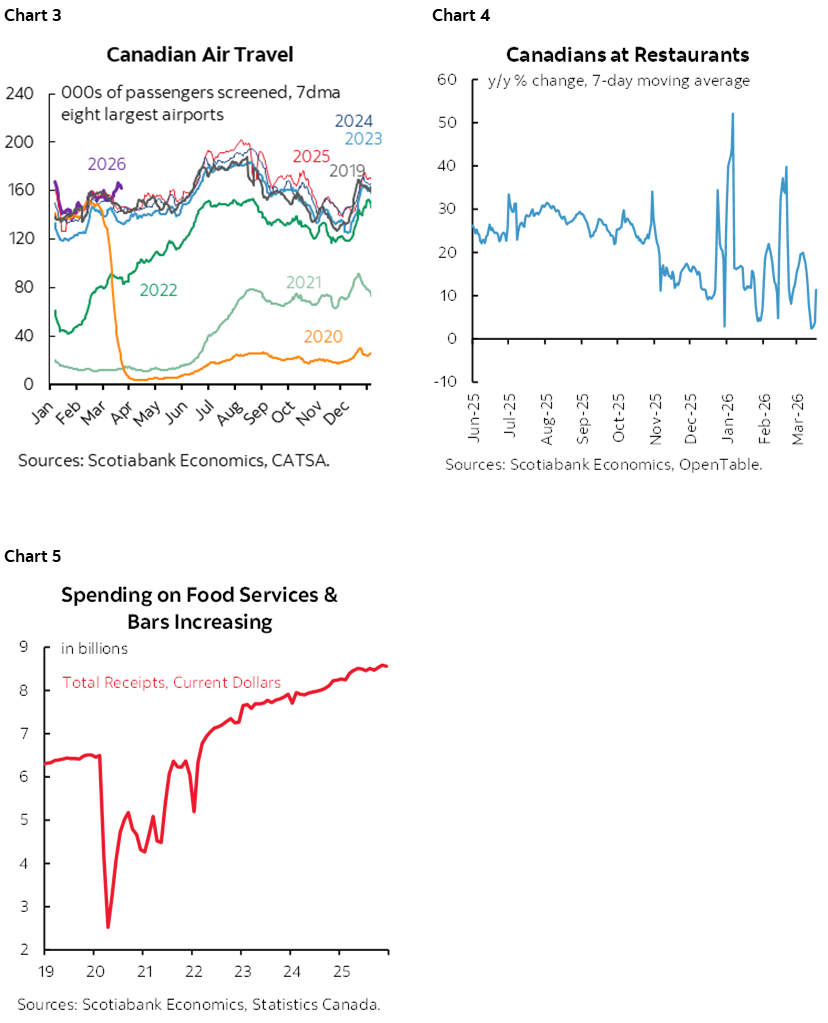

A caution, however, is that retail sales do not include any services spending in Canada unlike the US that at least includes eating/drinking establishments (aka bars/restaurants). Those bar and restaurant figures are in a separate, lagging report in Canada. But anything you're spending in Q1 on hotels, airfare, concerts, sporting events, financial services, movies, etc is not included in Canadian retail sales.

The ability to track services spending is limited. It could either add to or subtract from the momentum shown in the first chart since services account for 57% of total Canadian consumer spending. Some Q1 readings like flights (chart 3) and restaurant bookings (chart 4) are looking solid while bars/restaurants only go to December so far (chart 5).

Still, if tracking of goods consumption in Q1 is anywhere close to the mark, then the 43% weight on goods in total real consumption would still point to a large 2–3%+ weighted contribution to growth in total consumption.

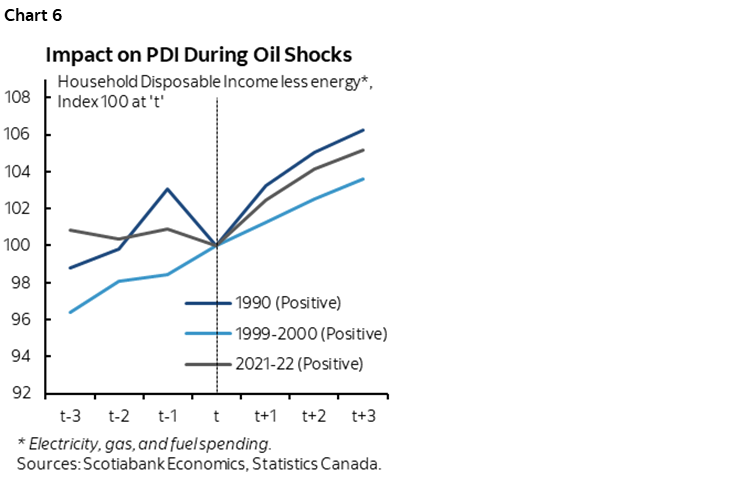

But it’s backward looking data amid an evolving oil shock that’s going to crush the consumer, right? Maybe, but that’s much less clear than the knee jerk arguments out there. The BoC expressed concern about real incomes going forward, yet as chart 6 shows, real disposable income after spending on energy tends to rise in positive oil shocks—not fall. Wages may adjust, the energy patch could hire and pay more and it’s not the job of the BoC to fuss about what regions in which this is happening, shareholder distributions can support incomes, and behaviour can change. All of that could leave something left over to continue driving consumption. If the job market tanks then it’s a downside risk but I’d like more than two lousy months of evidence for a wonky survey that may have been slammed by weather and the flu, and it’s wages that will carry the day for the vast overwhelming majority of consumers anyway. Wages in a country driven significantly by collective bargaining exercises that invoke sticky gains.

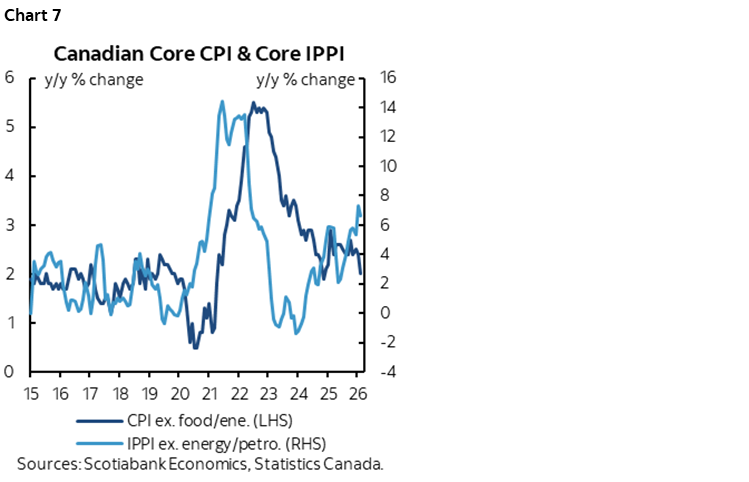

Canadian producer prices posted another gain in February with industrial prices up 0.4%, raw materials prices up 0.6%. Just wait until March. Chart 7 shows that industrial prices continue to point toward future upside risk to core CPI. Unless that’s totally eaten by selling down old inventories for a really long time and/or on profit margins, then it points to the hawkish reemergence from a core inflation soft patch. Time will tell, but the historical connections suggest it’s only a matter of time.

Also note that Canadian new home prices might motivate a tiny upward revision to homeowner replacement cost within February CPI. Statcan's CPI for February initially showed replacement cost of housing down before we got this morning's update showing it increased.

So what do you do if you’re the BoC? It’s all about risk management. There is a bit of time, but don’t assume that you have a lot. Don’t wait until you’re staring straight in the whites of the eyes of another inflation shock. Don’t wait until it’s fully evident in headline and core inflation readings. If—and emphasis upon if—this is a durable energy shock for a commodity-dependent economy and the oil futures curve is anywhere close to being correct over 2026–27, then deal with the uncertainty by staggering the policy rate adjustments. There is still time ahead of the next 2–3 meetings, but if energy markets don’t abruptly cool off, then we should all be open-minded toward insurance hikes, over waiting until its lights out. Get control of the bond market in terms of the belly and long-end parts of the term structure. My worry about Governor Macklem is that he waits and waits and waits and then we’re back in another devastating inflation problem with political consequences for his former partner at the BoC. Insurance hikes leave open the door to stop and/or reverse if needed while also leaving open the door toward doing more while lessening the risk of a massive catch-up overshoot on the policy rate like the last time. That, in my opinion, would be the bigger sin if repeated by the BoC and the final nail in Macklem’s legacy as the end of his term approaches next year.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.