- FOMC stayed on hold as widely expected

- Statement changes were minimal…

- ...except for three dissenting hawks, one dissenting dove

- Powell gave a lengthy, spirited defence of Fed independence…

- ...while committing to stay on the Board…

- ...that could perhaps be until a new Senate convenes in January

- Markets barely reacted with oil remaining the main focus into heavy tech earnings

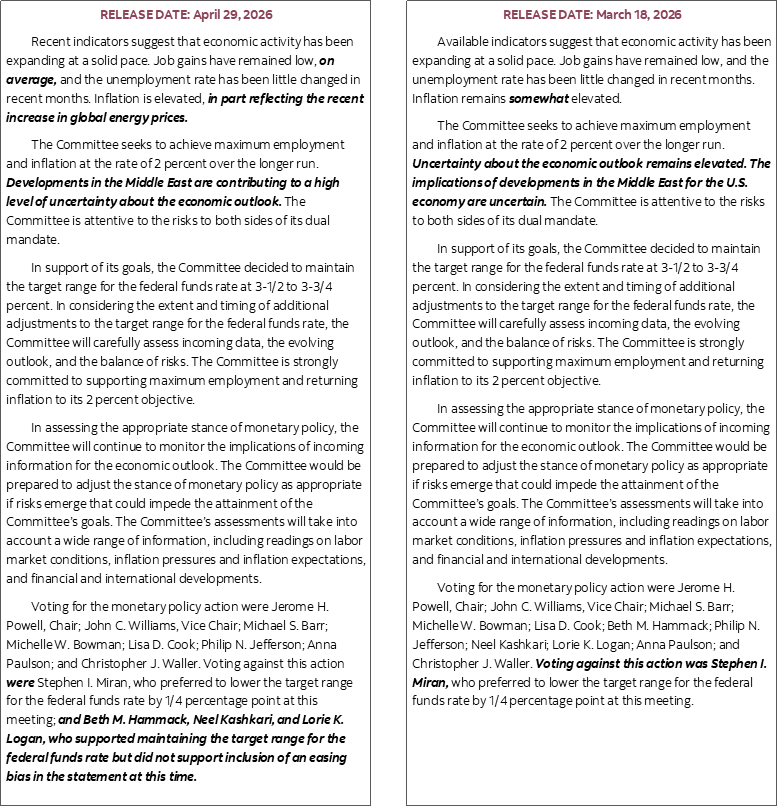

The FOMC left the policy rate range of 3.5–3.75% unchanged along with balance sheet plans as universally expected. Guidance was mixed and tiptoed further yet toward a fully neutral if not hawkish bias that serves as an awkward segue into new leadership.

A 55-minute press conference was well managed by Chair Powell with a lot of emphasis upon staying on the Board and defending Fed independence.

All but the most emotionally vacuous couldn’t help but observe a degree of moroseness as Powell left the room for a final time as Chair. Departing a job he so obviously loved and was passionate about. A weak attempt at a round of hand clapping could have been stronger despite our disagreement on several debates during Powell’s tenure. The role involves enormous sacrifice in the spirit of public service and someone of his stature certainly isn’t doing it for the money. His long 55 minute presser put a lot of emphasis upon putting up a spirited fight in defence of Fed independence at a further cost to himself; others might have been forgiven for relishing the thought of moving on.

Good for you, Jerome Powell. Good for you.

Markets barely reacted to the suite of communications. They were already in neutral territory with nothing priced by way of action for this year. US 2s ended a touch cheaper by 2bps after the full set of communications. Year-end OIS pricing edged about 3bps higher. Most of the market action was Fed driven, as oil’s big spike today was little changed throughout the communications. Tech earnings are dominating in the after-market with Amazon, Alphabet, Meta and Microsoft all out.

STATEMENT CHANGES—A CURIOUS COMBINATION OF DISSENTERS

There were very few minor tweaks to the statement as shown in the comparison within the appendix to this note.

There were, however, some curious dissents. Governor Miran dissenting in favour of easing isn’t the one that caught my eye as it’s kind of expected by now.

The three that did were Cleveland’s Hammack, Minneapolis President Kashkari and Dallas President Logan “who supported maintaining the target range for the federal funds rate but did not support inclusion of an easing bias in the statement at this time.”

What they were probably dissenting against was repeated inclusion of the line referencing "the extent and timing of additional adjustments to the target range" which is not new and which theoretically could cut in either direction but has been in there as openness toward restarting an easing cycle that was interrupted after December’s cut.

The three dissenters might have also meant it as a caution against any dovish pivot when Kevin Warsh takes the helm. He passed the Senate Banking Committee this morning which means the next step will be a full Senate vote.

The three dissenters may have also been more open to hikes, although not at this meeting as Chair Powell indicated they had unanimous agreement to stay on hold.

Regardless, the gesture sort of screamed 'welcome!' to the new incoming Fed chair, Kevin Warsh.

It does, however, spawn somewhat of a debate over why only 3 of the 12 dissented against any potential easing bias. Powell wouldn't have. Miran went the other way. That leaves seven other voting members. Does that mean those other seven thought the other 3 dissenters were out of line or that they wished to be more circumspect and keep options open? Chair Powell’s comments in the presser suggest it was the latter interpretation.

The broad takeaways include guidance that the majority is not yet prepared to fully embrace a neutral stance that removes any reference to rate changes but that it would take such a step first before potentially embracing a hiking bias if that is judged to be needed. That seems unlikely with Warsh coming in and the majority unwilllng to join the three more hawkish voting members. Further, I would bet that Powell will stay on the Board for a long time until he has full reason to think that any legal threats against Fed independence have subsided.

That could mean until a new Congress in January should the Dems take the Senate and therefore have greater control over who may be chosen to replace Powell on the Board as a check on the administration’s tactics.

Also worth emphasizing is reference to “as soon as the next meeting” as a possibility for when an easing bias could theoretically be struck out of the statement. Again, Warsh will get a say in that and Powell sounded like his personal view and the majority view he conveyed are prepared to look through tariff and energy effects on inflation while also seeing a still pretty resilient US economy and labour market. Personally, I think the resilience argument on the labour market remains overstated.

PRESS CONFERENCE TRANSCRIPT

Q1. What went into your decision to remain on the Board and how long may you stay?

A1. My concern is repeated political attacks on the Fed. It has nothing to do with political attacks. The legal attacks are unprecedented. I worry that these attacks are battering the Fed and threatening to make the Fed make decision on political grounds. I will leave when I think it is appropriate to do so.

Q2. By remaining on the Board are you taking a political stance and denying the President the opportunity to appoint someone else to the Board?

A2. I don't see it that way. I've long planned on retiring. My intention is not to interfere. I was a Governor for six years. As a soon to be former Chair I understand it is difficult to coordinate 19 strong minded people.

Q3. How has the inflation outlook changed since March before getting to the energy shock that is now on top of tariffs?

A3. For a long time we have been working on the hypothesis that tariffs would be a one-time increase. It's time for that to happen. We really do expect that to happen in the next two quarters. We need to really see that. With energy, it's so hard to say. In the textbook you would look through an energy shock. We're going to be very cautious since we were already looking through tariffs. We want to see the backside of that (energy inflation) as well as tariffs before we change.

Q4. Why still have an easing bias and what more would have to happen to remove it?

A4. We had a vigorous discussion in this meeting about the guidance. The number on the Committee who could support a language change that a hike could be as likely as a cut has changed. We're going to need to see what happens. Three people dissented over the language. The majority of the Committee did not want to do that and I did not. Why do we want to do that now, there doesn't need to be a rush to decide this. What happens in the next 30, 60, 90 day could really change that picture.

Q5. If Brent stays around present levels what's your guess on whether the easing bias is still in the statement next time?

A5. I won't answer that, I won't be the Chair then. We had a discussion, the majority are not supporting the need to move to that level and that's where I am. I get that at a certain point you need to change and that could happen as soon as the next meeting.

Q6. What advice would you give on communications and the dot plot to Warsh?

A6. I'm not going to give that advice. You always look at new ways of communicating.

Q7. Have you been in touch with incoming Chair Warsh. Is it a normal process?

A7. I haven't seen him since a dinner in January when I congratulated him. I haven't seen a normal process. I think this will be a normal process.

Q8. Is the SCOTUS decision on Governor Cook a factor on when you may leave as Governor?

A8. I wasn't thinking of that, no.

Q9. The new framework in 2020 was perhaps driven by elevating the employment mandate. Are you worried that a new Chair would be more motivated to drive a hot job market?

A9. I don't know the answer to that. For a long period of time in the 20teens we saw a tight job market and little wage pressure. A lot of benefits were flowing to the lower income spectrum and training them. Anybody would love to get back to that. I don't think that anything that happened to drive inflation had to do with overweighting the employment side of the mandate. It was a global shock.

Q10. Do you need more assurance from the Justice Dept to step down? What are you waiting for?

A11. I am looking for finality and I will leave when I think it's appropriate to do that.

Q12. Can you elaborate on the two-sided view because some were advocating a need to raise interest rates because of hot inflation even before the war.

A12. The three dissenters and others who could have supported that all supported the decision to hold. Nobody fel there was a need not to be neutral. It's a form of forward guidance. A group of us including me didn't feel like we need to be in a hurry on that. Markets are not confused by our reaction function but it's a good discussion to be having.

Q13. You have 3 dissents in favour of two-sided warning. You are staying on the Board. You have a lot of critics about 2021 inflation. Are you worried about Fed credibility amid all of this and that's why you want to stay on?

A13. I'm no thinking that. The Chair's job is to create consensus and pull them together and move. I think Kevin Warsh has the capabilities and skills to be good at that. I'm not worried about that process. It will work itself out.

Q14. What does keeping a low profile look like? How can you not be a shadow chair?

A14. That's just something I would never do. I don't know what the exact specifics would be. I respect the role of Chair. I was Governor for six years. The authority of the Chair is to develop relationships with people and put forward a consensus and I intend to be constructive to that process out of respect for the Chair.

Q15. How do you see the risks around the bleed into core inflation from commodities?

A15. Those prospects are real but we're going to have to wait and see. The good news is that our policy stance gives us the opportunity to wait and see at the high end of neutral. We can wait here and see how things work out before we react. We'll see how it moves into core, we'll just see.

Q16. Why is it a net positive to adding press conferences to every meeting instead of just SEPs?

A16. During the pandemic when we were moving every meeting it was awkward to do press conferences only with SEPs. It's become the norm now across central banks.

Q17. What changes did you want last year to communications?

A17. We found that making large changes to the dot plot or SEP we couldn't come up with anything that had broad support on the Committee. I was never a big fan of the dot plot. Every new chair is going to look at the suite of new communications. We are the only major central bank that doesn't publish a forecast. That's because we have 19 members. It works, that's fine, but looking at it is natural.

Q18. Are we right to assume the hawkish stance of the FOMC is to just extend the hold and whether the policy rate is restrictive?

A18. We think we're in a good place. If we think we need to cut or hike we'll signal that. We're in a good place. Nobody is calling for a hike now. It's a much closer question on changing the guidance but decided not to.

Q19. At what point does the war and the impact on commodities become a bigger concern?

A19. Given that the economy is more energy independent and energy efficient the effects are less than on much of Europe or Asia. If this goes on for much longer or much higher than we'll see. We're talking aggregate inflation and we know people are paying higher gas. Other products will reflect this.

Q20. Markets don't see a rate cut this year. Are we at the neutral rate and why or why not?

A20. I always had it between 3–4% and we're within the higher end of the range of what I would consider neutral. The labour market is probably cooling off just a little bit. I don't think there is a case for policy looking meaningfully restrictive, maybe neutral or slightly restrictive.

Q20. Are you handing off a divided Fed given dissents?

A20. We have always had vigorous debates. We're in an usual situation. We've had four supply shocks, the pandemic, the invasion of Ukraine, tariffs, and now the oil spike. Every supply shock has the potential of driving inflation up and unemployment up. Our framework calls for us to balance the two. These are really difficult things to see so it's only natural to see different views.

Q21. Are you confident Warsh will stand up to President Trump?

A21. He said he would in his testimony and I take him at his word.

Q22. Question on what will happen to gas prices over the rest of the year.

A22. I don't know. Higher gas prices come out of people's pockets. It's a question what happens to demand as an offset to higher gases.

Q23. Where do you see Fed independence coming from? The law? Congress? Actions of the Fed?

A23. It is the law and we've had to go to court to defend it. Part of it is law. There is a set of customs, a boundary line between the Fed and the Treasury department and the rest of the administration. It's more than just monetary policy and it goes beyond the law.

Q24. Is Fed independence as strong as when you became Chair?

A24. I think it's at risk. We've had to defend against the legal attacks to make monetary policy without taking political considerations into account. We've been successful at doing that so far. It's about a central bank that makes decisions on the basis of analysis and decisions independent of what's good for politics.

Q25. Do you have the support of your colleagues to stay on the Board? Have others on the Board conveyed concern about legal attacks on the Fed?

A25. I don't want to report on what my colleagues said, they can do so. There is widespread concern.

Q26. Do you have any tthoughts on centralizing reserve bank functions like Waller's speech?

A26. We try to be good stewards about how we use the public's money. Chris said we want 12 independent central banks that share their views but there is a back and forth coming on about centralizing different overlapping functions. There is also a need to stand against interfering with district bank decisions by the administration.

Q27. How will history think of your stewardship?

A27. That's for someone else to say.

Q28. What's your message on inflation not being under control since the Covid reopening?

A28. Our goal is to bring inflation down sustainably. These events keep happening to drive up costs. We try to get there over time in a way that does the least damage possible.

Q29. How would you describe the economy outside of stubborn inflation?

A29. Some is due to resilience some is driven by insatiable demand for data centers. That's a positive thing. The unemployment rate is pretty close to the natural rate of unemployment. It doesn't feel strong to some, quits and new job creation are low, new people have a hard time breaking in unless someone quits, so it's a mixed picture. We think tariffs and energy inflation should go through but in the meantime we think our policy stance is in a good place to await developments.

Q30. Does the majority of the Committee still have a bias toward cuts?

A30. The center is moving toward a more neutral place. There is a lot of signalling going on when you change guidance. A majority felt we didn't need to send a signal just now. It may come to that. We will move to a neutral bias and then a hiking bias if we feel the need to do so.

Q31. Do you want to stay on as Governor to serve as a check and balance on independence?

A31. I will stay on until I like what I see and yes that is a concern. I'm not looking to be a high profile dissident.

Q32. Are there any decisions you've made that stand out that you are particularly proud of or ones you wish you could reconsider?

A32. We're in an unusual situation with so many supply shocks. It's a different world and a more challenging one. We've tried to do our very best and I'm really proud of the work that my colleagues and I have done.

Q33. Why is this notion of Fed independence so critical? What if SCOTUS rules against Lisa Cook or other political developments arise?

A33. Every major country has taken out of the direct control of elected politicians control over monetary policy. Elected officials are always seeking election and can drive inappropriate decisions. Don't think of an institution being independent. Think of it as wanting officials to focus only upon price stability and full employment conditions and ignore politics only in service to the public. The markets are pricing in Fed credibility.

Q34. Are you seeing effects of higher commodities on spending and how worried are you it will be a drag on growth?

A34. You don't see it in spending. The US economy has been remarkably resilient. Consumers are still spending. How long can that go on if prices go up much more? Right now we don't see much slow down.

Q35. Do you see evidence of pass through from Asian economies into inflation?

A35. All of those factors are in our models. The effects are not that big so far. Imports are a relatively small share of US GDP unlike Europe. We're an oil exporter. We're unlikely to see the kind of pain that western Europe and Asia are experiencing.

Thanked everyone and said "I won't see you next time."

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.